How Different Terrorist Attacks Affect Stock Markets

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808)

Department of History and Civilization Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808) MANUEL PEREZ GARCIA Thesis submitted for assessment with a view to obtaining the degree of Doctor of History and Civilization of the European University Institute Florence, June 2011 Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 EUROPEAN UNIVERSITY INSTITUTE Department of History and Civilization Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808) MANUEL PEREZ GARCIA Examining Board: Bartolomé Yun-Casalilla, supervisor (European University Institute) Luca Molà (European University Institute) Jan De Vries (University of California at Berkeley) Gerard Chastagnaret (Université de Provence) © 2011, Manuel Pérez García No part of this thesis may be copied, reproduced or transmitted without prior permission of the author Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 Abstract How to focus the analysis of the birth of mass consumption society has been a scholarly obsession over the last few decades. This thesis suggests that an analytical approach must be taken in studies on consumption paying special attention to the socio-cultural and economic transfers which occur when different commodities are introduced to territories with diverse socio-cultural values and identities. -

Measuring the Economic Impact of Immigrant Workers Exit from Madrid Region Labor Market

ISSN: 1695-7253 e-ISSN: 2340-2717 [email protected] AECR - Asociación Española de Ciencia Regional www.aecr.org España – Spain Measuring the economic impact of immigrant workers exit from Madrid region labor market Angeles Cámara, Ana Medina Measuring the economic impact of immigrant workers exit from Madrid region labor market Investigaciones Regionales - Journal of Regional Research, 49, 2021/1 Asociación Española de Ciencia Regional, España Available on the website: https://investigacionesregionales.org/numeros-y-articulos/consulta-de- articulos Additional information: To cite this article: Cámara, A., & Medina, A. (2021). Measuring the economic impact of immigrant workers exit from Madrid region labor market. Investigaciones Regionales - Journal of Regional Research, 2021/1 (49). https://doi.org/10.38191/iirr-jorr.21.006 Online First: 14 December 2020 Investigaciones Regionales – Journal of Regional Research (2021/1) 49 https://doi.org/10.38191/iirr-jorr.21.006 Articles Measuring the economic impact of immigrant workers exit from Madrid region labor market Angeles Cámara*, Ana Medina* Received: 08 March 2020 Accepted: 26 October 2020 Abstract: This paper analyses the economic impact of the loss of employment suffered by the immigrant population in Madrid’s regional economy during the years of the latest economic crisis, specifically during the period 2010-2016. First, it examines the labour characteristics of the immigrant population, a community mainly employed in unstable and low-skilled jobs and overrepresented in economic sectors that are sensitive to fluctuations in the labour market. Financial crisis forced these workers exiting labour market and the present work focuses on the modelling of this phenomenon by means of the construction of a multisectoral model of the supply-side type, also known as Ghosh model. -

Terrorism and Capital Markets: the Effects of the Madrid and London Bomb Attacks

International Review of Economics and Finance 20 (2011) 532–541 Contents lists available at ScienceDirect International Review of Economics and Finance journal homepage: www.elsevier.com/locate/iref Terrorism and capital markets: The effects of the Madrid and London bomb attacks Christos Kollias, Stephanos Papadamou ⁎, Apostolos Stagiannis Department of Economics, University of Thessaly, Korai 43, Volos, Greece article info abstract Article history: Using event study methodology and GARCH family models, the paper investigates the effects of Received 23 February 2009 two terrorist incidents – the bomb attacks of 11th March 2004 in Madrid and 7th July 2005 in Received in revised form 23 September 2010 London – on equity sectors. Significant negative abnormal returns are widespread across the Accepted 23 September 2010 majority of sectors in the Spanish markets but not so in the case of London. Furthermore, the Available online 7 October 2010 market rebound is much quicker in London compared to the Spanish markets where the attackers were not suicide bombers. Nevertheless, the overall findings point to only a transitory JEL classification: impact on return and volatility that does not last for a long period. G14 © 2010 Elsevier Inc. All rights reserved. G21 C22 Keywords: Terrorism Capital markets Event study Conditional volatility GARCH 1. Introduction The economic analysis and effects of terrorism are issues that have attracted a considerable and growing body of literature (inter allia:G,Bird, Blomberg, & Hess, 2008; Bruck, 2005, 2007; Enders & Sandler, 2006; Bruck & Wickstrom, 2004; Sandler & Enders, 2004; Sandler, 2003). Beyond the loss of life and personal injuries that the victims of terrorist actions suffer and the atmosphere of fear terrorists seek to create with their premeditated use of brutal violence, terror also has real economic costs. -

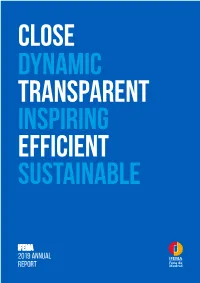

IFEMA 2019 Annual Report

CLOSE DYNAMIC TRANSPARENT INSPIRING EFFICIENT SUSTAINABLE IFEMA 2019 Annual Report MAIN FIGURES OUR ACTIVITY FINANCIAL RESULTS VISITORS COMMUNICATION Events Income Visitors Media impact 898 € 187,2 M. 4,323,775 1,119 M. International visitors Audience .Websites viewed Trade fairs and congresses Expenses 26% 51,518.7 M. 27.7 M. with exhibition €147,2 M. 123 Accredited Social media EXHIBITING COMPANIES journalists followers In-house Externally- Net profit trade fairs organised 13,193 2.1 M. trade fairs € 22,5 M. 61 Participating companies 41 Accredited Economic media valuation Congresses Trade with an fairs Investments 33,292 exhibition abroad 21,225 € 919,245.9 M. 18 3 €16,6 M. Direct International exhibitors exhibitors Festivals, concerts and EBITDA long-term events € 40,0 M. 16,902 22% ECONOMIC IMPACT ON MADRID 26 REGION* Financial debt OCCUPATION Others € 5,104 M. 749 0 € Net surface area 2 Net wealth 1,447,538 M 3.8% 2.2% € 310,1 M. of the GDP of the GDP of the city of of the Madrid Gross surface area Madrid Region 3,500,000 M2 *Source: “Study of IFEMA’s socioeconomic impact”. M.: million. © 2020 KPMG Asesores, S.L. €---M.: millions of euros. 2019 ANNUAL REPORT CLOSE DYNAMIC TRANSPARENT INSPIRING EFFICIENT SUSTAINABLE 02 2019 Annual Report Contents 03 Contents 01 02 03 05 CLOSE DYNAMIC TRANSPARENT EFFICIENT The voice of IFEMA | 04 2019: a lot to celebrate | 14 Communicating more Financial management and better | 54 report | 78 Letter from the Chairman of the The Managing Director’s vision | 16 Governing Board | 06 A year of intense -

Spain in 1830

^OFCAIIFO/?^ ^OFCAllF0Mij>, >^ ^OFC^ <m3DKVS01=<^ %e\iNn-3tf^ %avHan#' *^c?Aavi ^IIIBRARYQ^' -^'EllBRARYOr ^\\\EONIVEW/^ rAjclOSAI '%JBAINn-3HV^ '^<!(0JnYDiO'^ %OJ11VOJO'^ <riUDNVS01^ "^ajAii ^lOSMFI£r^ ^OFCAUFO/?^ ^OFCAllFOff^ ^^lrtMlNIVER% 7» O " ^ I 3 3 uL %a3AINfl3ViV^ <riuoNVsm^ %a3Aii ^ ^AlUBRARYQ^ .\WE11NIVERJ/A ^lOSANCElfj^ ^lUBRARY^/^ ^IIIBR , ^ ^ O <f3l30NVS01^ %a3AiNa-3ftV^ ^^m\m'i^ '^tfOJir ^OFCAlIFOfi';^ ^\\^EUNIVER%. ^lOSANCElfj^ ^OFCAIIFO% i > V/ _ 1^ 5^ >—'I I' ^ <rii30NYsoi^ "^ajAiNnawv ^<?Aaviian#' ^lOSANCElfju% -^lllBRARYQ-c ^lUBRARYQ^" .^WEUNIVER% > so -< %a3AINn3WV^ ^lOSANCEI^^ ^^AHvaan-i^ ^^Aavaani^ <ril3DNYS01^ %a3AIN g <I313DNVS01^ V/SaJAINn-aWv ^.SfOJIlVDJO^ ^tfOJnVDJO^ ,^Wfl)NIVERJ/A avIOSANCEI% .5JAEIJNIVER5; >- oc ._ . _r So if <m33Nvsoi^ "^/^yMAiNnawv** "^(^Aavaani^ '^OAavaan#' <J^0NVSOV -^tUBRARYf?/^ A^IUBRARYQ^^ AWEUNIVER% ^lOSANCElfj^ ^lUBRARY^ u3 ^(tfOJITVJJO"^ '^iSfOJnVJJO^ <ril33NVS01^ %a3AINrt-3ftV' ^iJOJIWDJC ^OFCAllFOi?^ ^OFCAIIFO% .^WEUNIVERJ/A ^lOSANCEUr^ ^OFCAllFOfi >&Aaviian-^^'^ >&Aava8n# <r71J3NVS01^ ^(?AiivaaiH ^^^E•lINIVER5•/A ^lOSANCElfj^ -5>^lUBRARYQr. ^tUBRARY(7/^ .tVWEUNIVERX <IJUDNVS(n'^ "^aiAiNn-art^^ <(^13DNVS0V .^WE•UNIVER5/A ^lOMEl^^ ^OFCAllFO^jk ^OFCAITO^ ^MEUNIVER5} o oe 6 "^JJHONVSOl^ '^(?Aavaan#' ^<?Aava8n# "^J^UDNVSOr ^>MllBRARYac. ^lUBRARYQ^^ ^\\EUNIVERS/A ^VOSANCElfX;> -v>^lllBRARY^ C9 ^ (5 <<^33NVS01^ %a3AiNn3\ft? ^ojnvjjo ^OFCAIIFO^^ ^OFCAUFOff^ ^^MEUNIVERS/^ ^•lOSANCEltr^ ^OFCAIIFO« S •a ^^Aavaani^ <i7iaDNvsoi^ "^aaAiNnjwv^ 3 § V^ 'J '^/sm "^ajA 5 " ^.ffOJIl ^OFCA yo\m %a3Ai c^ I %a3Aii SPAIN IN 1830. — — By the same Authoj-, In 2 vols., Post 8vo., Price 16s. SOLITARY WALKS THROUGH MANY LANDS, —with TALES and LEGENDS. The descriptions are diversified and graphic,—the tales introduced, in- teresting and clever, —and the author's narrative style, sprightly and un- affected. New Monthly Magazine. It is all pleasing, and always interesting, —the author has at once the eye of a keen observer, and the pen of a ready writer. -

The Financial Impact of Terrorism on West European Markets

School of Economics and Management The financial impact of terrorism on West European markets Master Thesis Student name: Koen van Uden Student number: 1266258 Supervisor: dr. K.K. Nazliben Second reader: dr. F. Castiglionesi Submission date: August 2018 Abstract The main focus of this paper is to study the financial impact of terrorism on West European markets. The dataset examined includes 69 terrorist attacks that targeted West European countries over an 18-year time period. An event study approach is used to measure the event day en post-event day reaction of national indexes and industries to terrorism. The results show that the average attack negatively affects the West European market by -0.2%, this impact is only transitory since the results show a significant positive 10-day cumulative abnormal returns. Terrorist attacks with more than 100 casualties have an even more negative impact on the West European markets and are more likely to have a permanent impact. The attacked country suffers the most financial damage and this damage is permanent. The results show that all industries experience negative abnormal returns on the day of the event, two industries show significant results. The oil, gas and water industry is struck the most and is the only one to be permanently damaged. Furthermore, plausible explanations for the results are discussed from a behavioural finance perspective. Keywords: Terrorism; Financial markets; Event study methodology; Reversal effect; Investor sentiment 2 Table of Contents 1. Introduction ...................................................................................................................................... -

Bethany Marie Gilliam Dissertation

The Monstrous Guide to Madrid: The Grotesque Mode in the Novels of the Villa y Corte (1599-1657) DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Bethany Marie Gilliam Graduate Program in Spanish and Portuguese The Ohio State University 2014 Dissertation Committee: Professor Elizabeth B. Davis, Advisor Professor Jonathan Burgoyne Professor Emeritus Donald Larson Copyright by Bethany Marie Gilliam 2014 Abstract This dissertation examines the relationship between the literary grotesque mode and the growing pains of Madrid during the first century of its status as Villa y Corte, capital of the Spanish empire. The six novels analyzed in this study – Guzmán de Alfarache (1599, 1604), El Buscón (1626), Guía y avisos de forasteros (1620), Las harpías en Madrid (1633), El diablo cojuelo (1641) and El Criticón (1651, 1653, 1657) – are significant because their authors employ the grotesque mode to show their perspectives on the changes that they witnessed in Madrid. The central goal of this project is to examine the continued presence of the grotesque mode in these novels and how the use of this mode was motivated by the historical crisis that took place during the years following Philip II’s decision to move the court to Madrid. In this vein, Philip Thomson recognizes that moments of change are particularly conducive to the use of the grotesque in art and literature. Using studies on the grotesque by Thomson, Wolfgang Kayser, Henryk Ziomek, James Iffland and Paul Ilie, this dissertation will present a definition of the grotesque mode as it applies to a carefully chosen grouping of seventeenth-century Spanish novels. -

Annual Report 2020 Ideas Impulse Enthusiasm Innovation

Ideas Impulse Enthusiasm Innovation. Annual Report 2020 Ideas Impulse Enthusiasm Innovation. Annual Report 2020 World’s Best Europe’s Best Spain’s Best Convention Convention Convention Centre Centre Centre IFEMA MADRID | ANNUAL REPORT 2020 Contents. 01. 03. 05. Acknowledgements_ 4 Beyond communication_32 Economic management _44 Greeting from the President of the Governing Board_5 Sharing vision and mission: report Letter from the Chairman of the Executive Committee_6 IFEMA COVID-19 Hospital_33 Economic results_45 Governing bodies_7 IFEMA MADRID in the media_33 Balance sheet_50 Management bodies_8 Expanding the digital community_34 Profit and loss account_51 Summary of expenses and income by activities_52 02. 04. IFEMA MADRID, Transforming ourselves_36 _ 9 much more Actions in Valdebebas_37 Technological advances_38 The General Manager’s vision_10 Other works and investments at the Trade Fair Venue_41 High expectations for a memorial year_11 Security improvements_41 2020: a year cut short by the pandemic_16 Ready for the future_42 At the service of society_18 Objective: resume activity_21 Focused on digital transformation_23 First physical events_26 Recognition of our sponsors_27 Designing the future: Strategic Plan 2021-2023_28 Expanding horizons_30 3 IFEMA MADRID | ANNUAL REPORT 2020 01. Acknowledgements. Greeting from the President of the Governing Board_5 Letter from the Chairman of the Executive Committee_6 Governing bodies_7 Management bodies_8 4 IFEMA MADRID | ANNUAL REPORT 2020 Greetings from the President of the Governing Board. Isabel Díaz Ayuso “As the most senior I am very proud of IFEMA MADRID and what it means to Now it’s time to look to the future. The exhibition centre Madrid. Just like on 2 May, the flag of the seven stars has been getting ready for the recovery, has rebranded representative of the people of and the Puerta de Alcalá, IFEMA MADRID is already, in itself IFEMA MADRID and making a bold commitment Madrid, I can tell you that we its own right, a symbol of our region. -

RLCS-Paper1166en.Pdf

RLCS, Revista Latina de Comunicación Social, 72 – Pages 295 to 320 Funded Research | DOI: 10.4185/RLCS, 72-2017-1166| ISSN 1138-5820 | Year 2017 How to cite this article in bibliographies / References EF Rodríguez Gómez , E Real Rodríguez, G Rosique Cedillo (2017): “Cultural and Creative Industries in the Community of Madrid: context and economic development 2008 – 2014”. Revista Latina de Comunicación Social, 72, pp. 295 to 320. http://www.revistalatinacs.org/072paper/1166/16en.html DOI: 10.4185/RLCS-2017-1166 Cultural and Creative Industries in the Community of Madrid: context and economic development 2008 – 2014 [1] Eduardo Rodríguez Gómez [CV] [ ORCID]. Professor and researcher in training of the Department of Journalism and Audiovisual Communication. Universidad Carlos III de Madrid - [email protected] Elena Real Rodríguez [CV] [ ORCID] [ GS]. Professor in the Department of Journalism III of the Faculty of Information Sciences. Universidad Complutense de Madrid – [email protected] Gloria Rosique Cedillo [CV] [ ORCID] [ GS]. Professor and Researcher in the Department of Journalism and Audiovisual Communication. Universidad Carlos III de Madrid – [email protected] Abstract The Community of Madrid is one of the main focuses of Cultural and Creative Industries in Spain (CCI), therefore it is necessary to measure their socioeconomic impact in the region in aspects such as competitiveness, investment, employment and social cohesion. Objectives: The objective of this article is to introduce a model, using a harmonized and comparable methodology, that identifies the evolution of CCIs in the Community of Madrid (CAM) in the current context of digital change, so to understand public policies and gain awareness, from an Autonomic perspective, about to what extent they contribute to the generation of employment and social wellbeing. -

Measuring the Direct Economic Cost of the Terrorist Attack on March 11, 2004 in Madrid

THE ECONOMIC COST OF MARCH 11: MEASURING THE DIRECT ECONOMIC COST OF THE TERRORIST ATTACK ON MARCH 11, 2004 IN MADRID MIKEL BUESA, AURELIA VALIÑO, JOOST HEIJS, THOMAS BAUMERT and JAVIER GONZÁLEZ GÓMEZ Working paper, nº 54. February 2006. Edita: Instituto de Análisis Industrial y Financiero. Universidad Complutense de Madrid Facultad de Ciencias Económicas y Empresariales. Campus de Somosaguas. 28223 Madrid. Fax: 91 3942457 Tel: 91 3942456 Director: Joost Heijs e-mail: [email protected] Imprime: Servicio de Reprografía de la Facultad de Ciencias Económicas y Empresariales. UCM. Este documento puede ser recuperado a través de INTERNET en las siguientes direcciones This file is available via the INTERNET at the following addresses http://www.ucm.es/bucm/cee/iaif http://www.ucm.es/bucm/cee/iaif Working Paper Nº 54 THE ECONOMIC COST OF MARCH 11: Measuring the direct economic cost of the terrorist attack on March 11, 2004 in Madrid. MIKEL BUESA, AURELIA VALIÑO, JOOST HEIJS, THOMAS BAUMERT and JAVIER GONZÁLEZ GOMEZ * ABSTRACT This paper measures the direct costs that the terrorist attacks of March 11 caused on the economy of the region of Madrid. The evaluation has been made applying a conservative criterion, and the results obtained have to be considered as minimum. The result indicates that the terrorist attacks caused a loss of nearly 212 million euros to the regional economy of Madrid, equivalent to 0,16 per cent of the regional GDP (0,03 of the national GDP). This confirms that the immediate economic dimension of a terrorist attack such as the one of March 11 —apart from human catastrophic consequences— is relatively low. -

The Spread of Political Economy and the Professionalisation of Economists

The Spread of Political Economy and the Professionalisation of Economists This book presents the first systematic research and comparative analysis ever attempted on the rise and early developments of the Economic Associations founded in Europe, the USA and Japan during the nineteenth century. Individual chapters reconstruct the events that led to the foundation of economic societies in Britain, France, Italy, Belgium, Spain, Portugal, the Netherlands, Sweden, Germany, Japan and the USA. Contributors analyse the activities and debates promoted by these associations, evaluating their role in: • the dissemination of political economy • the institutionalisation of economics • the construction of professional self-consciousness among economists With contributions from outstanding experts, this book will be of essential interest not only to historians of economic thought, but also to those working more generally in the fields of economics or the history of scientific thought. Massimo M.Augello is Professor of History of Economic Thought and Head of the Department of Economics at the University of Pisa. He has published Joseph Alois Schumpeter. A Reference Guide (1990), and co-edited Le cattedre di economia politica in Italia (1988), Le riviste di economia in italia (1996), and Associazionismo e diffusione dell’economia politica nell’ltalia dell’Ottocento (2000). He is the managing editor of the journal Il pensiero economico italiano and a member of the Advisory Board of History of Economic Ideas. Marco E.L.Guidi is Associate Professor of History of Economic Thought at the Department of Social Studies at the University of Brescia. He is the author of several works on Bentham and classical utilitarianism. -

The Spanish Enlightenment Revisited

The Spanish Enlightenment Revisited Title: The Spanish Enlightenment Revisited Author: Jesús Astigarraga (ed.) Edition: Oxford: Oxford University Studies in the Enlightenment 2015, 313 pp. ISSN 0435-2866. Marie Christine DUGGAN Hidden crevices of 18th century Spanish intellectual life were revealed to the reviewer by this volume, and the undercurrents of regional division and mixed feelings about Spain’s own past provided insight into modern Spanish intellectual historiography. Jesús Astigarraga gave us in 2003 the contributions of the Basque economic society, La Bascongada. He largely excludes from this volume the political economy of Madrid --Campomanes, Olavide and Jovellanos. Perhaps as a result, the reign of Charles III (1759-1789) takes a back seat in favor of constitu- tional debates between 1812 and 1823, which Astigarraga views as the finest hour of the Span- ish Enlightenment. His definition of enlightenment precludes those who served government, to focus instead on those outside of power. It is an interesting point of view. The danger is this edited volume might convince some unsuspecting Anglo-American gradu- ate student that the enlightenment did not affect Spain in the 1760s, an impression that would only be confirmed by Astigarraga’s introduction which states that the Spanish enlightenment was a weak imitation of the French. It was a relief to find Gabriel Paquette’s essay, which in- cludes enlightened reform from government positions and puts Campomanes back into central position. Yet Astigarraga’s view carries the day in this volume. The solution would be a com- panion volume that focusses on ideas emanating from intellectuals in Madrid in the 1760s and 1770s.