The Financial Impact of Terrorism on West European Markets

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808)

Department of History and Civilization Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808) MANUEL PEREZ GARCIA Thesis submitted for assessment with a view to obtaining the degree of Doctor of History and Civilization of the European University Institute Florence, June 2011 Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 EUROPEAN UNIVERSITY INSTITUTE Department of History and Civilization Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808) MANUEL PEREZ GARCIA Examining Board: Bartolomé Yun-Casalilla, supervisor (European University Institute) Luca Molà (European University Institute) Jan De Vries (University of California at Berkeley) Gerard Chastagnaret (Université de Provence) © 2011, Manuel Pérez García No part of this thesis may be copied, reproduced or transmitted without prior permission of the author Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 Abstract How to focus the analysis of the birth of mass consumption society has been a scholarly obsession over the last few decades. This thesis suggests that an analytical approach must be taken in studies on consumption paying special attention to the socio-cultural and economic transfers which occur when different commodities are introduced to territories with diverse socio-cultural values and identities. -

The Importance of Narrative in Responding to Hate Incidents Following ‘Trigger’ Events

The Importance of Narrative in Responding to Hate Incidents Following ‘Trigger’ Events November 2018 Kim Sadique, James Tangen Anna Perowne Acknowledgements The authors wish to thank all of the participants in this research who provided real insight into this complex area. Researchers: Kim Sadique, Senior Lecturer in Community & Criminal Justice Dr James Tangen, Senior Lecturer (VC2020) in Criminology Anna Perowne, Research Assistant All correspondence about this report should be directed to: Kim Sadique Head of Division of Community and Criminal Justice (Acting) De Montfort University The Gateway, Leicester, LE1 9BH Email: [email protected] | Tel: +44 (0) 116 2577832 To report a hate crime, please contact Tell MAMA Email: [email protected] | Tel: +44 (0) 800 456 1226 www.tellmamauk.org Twitter: @TellMAMAUK Facebook: www.facebook.com/tellmamauk This work is licensed under a Creative Commons Attribution 4.0 International License. To view a copy of the license, visit: https://creativecommons.org/licenses/by/4.0/legalcode 1 Contents Foreword ........................................................................................................... 3 Executive Summary .......................................................................................... 4 Recommendations ............................................................................................ 5 Introduction ....................................................................................................... 6 Aims & Objectives ......................................................................................... -

Measuring the Economic Impact of Immigrant Workers Exit from Madrid Region Labor Market

ISSN: 1695-7253 e-ISSN: 2340-2717 [email protected] AECR - Asociación Española de Ciencia Regional www.aecr.org España – Spain Measuring the economic impact of immigrant workers exit from Madrid region labor market Angeles Cámara, Ana Medina Measuring the economic impact of immigrant workers exit from Madrid region labor market Investigaciones Regionales - Journal of Regional Research, 49, 2021/1 Asociación Española de Ciencia Regional, España Available on the website: https://investigacionesregionales.org/numeros-y-articulos/consulta-de- articulos Additional information: To cite this article: Cámara, A., & Medina, A. (2021). Measuring the economic impact of immigrant workers exit from Madrid region labor market. Investigaciones Regionales - Journal of Regional Research, 2021/1 (49). https://doi.org/10.38191/iirr-jorr.21.006 Online First: 14 December 2020 Investigaciones Regionales – Journal of Regional Research (2021/1) 49 https://doi.org/10.38191/iirr-jorr.21.006 Articles Measuring the economic impact of immigrant workers exit from Madrid region labor market Angeles Cámara*, Ana Medina* Received: 08 March 2020 Accepted: 26 October 2020 Abstract: This paper analyses the economic impact of the loss of employment suffered by the immigrant population in Madrid’s regional economy during the years of the latest economic crisis, specifically during the period 2010-2016. First, it examines the labour characteristics of the immigrant population, a community mainly employed in unstable and low-skilled jobs and overrepresented in economic sectors that are sensitive to fluctuations in the labour market. Financial crisis forced these workers exiting labour market and the present work focuses on the modelling of this phenomenon by means of the construction of a multisectoral model of the supply-side type, also known as Ghosh model. -

The Role of the Online News Media in Reporting ISIS Terrorist Attacks In

The Role of the Online News Media in Reporting ISIS Terrorist Attacks in Europe (2014-present): the Case of BBC Online Agne Vaitekenaite A dissertation submitted in partial fulfilment of the requirements of the Master of Arts in International Journalism COMM5600 Dissertation and Research Methods School of Media and Communication University of Leeds 29 August 2018 Word count: 14,955 ABSTRACT The numbers of ISIS (Islamic State of Iraq and Syria) terrorist attacks have risen in Europe since 2014. Consequently, these incidents have particularly attracted the media attention and received a great amount of news coverage. The study has examined the role of that the online news media in reporting ISIS terrorist attacks during the period between 2014-present, based on the fact, that the online news has overtaken the print media and the television as the most popular source of the news within the last few years (Newman et al., 2018). Hence, this allows it to reach and affect the highest numbers of audience. The research has focused on the case study of the British Broadcasting Corporation news website BBC Online coverage on the Manchester Arena bombing, which was caused by ISIS. The study has investigated the news coverage throughout 29 weeks since the date of the terrorist attack, what includes the period between the 22nd May 2017 and the 11th December 2017. This time slot has provided the qualitative study with 155 articles, what were analysed while conducting the thematic analysis. The findings indicated that some themes are dominant in the content of the online news media coverage on ISIS terrorist attacks. -

Terrorism and Capital Markets: the Effects of the Madrid and London Bomb Attacks

International Review of Economics and Finance 20 (2011) 532–541 Contents lists available at ScienceDirect International Review of Economics and Finance journal homepage: www.elsevier.com/locate/iref Terrorism and capital markets: The effects of the Madrid and London bomb attacks Christos Kollias, Stephanos Papadamou ⁎, Apostolos Stagiannis Department of Economics, University of Thessaly, Korai 43, Volos, Greece article info abstract Article history: Using event study methodology and GARCH family models, the paper investigates the effects of Received 23 February 2009 two terrorist incidents – the bomb attacks of 11th March 2004 in Madrid and 7th July 2005 in Received in revised form 23 September 2010 London – on equity sectors. Significant negative abnormal returns are widespread across the Accepted 23 September 2010 majority of sectors in the Spanish markets but not so in the case of London. Furthermore, the Available online 7 October 2010 market rebound is much quicker in London compared to the Spanish markets where the attackers were not suicide bombers. Nevertheless, the overall findings point to only a transitory JEL classification: impact on return and volatility that does not last for a long period. G14 © 2010 Elsevier Inc. All rights reserved. G21 C22 Keywords: Terrorism Capital markets Event study Conditional volatility GARCH 1. Introduction The economic analysis and effects of terrorism are issues that have attracted a considerable and growing body of literature (inter allia:G,Bird, Blomberg, & Hess, 2008; Bruck, 2005, 2007; Enders & Sandler, 2006; Bruck & Wickstrom, 2004; Sandler & Enders, 2004; Sandler, 2003). Beyond the loss of life and personal injuries that the victims of terrorist actions suffer and the atmosphere of fear terrorists seek to create with their premeditated use of brutal violence, terror also has real economic costs. -

IFEMA 2019 Annual Report

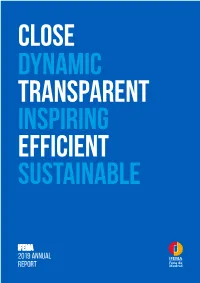

CLOSE DYNAMIC TRANSPARENT INSPIRING EFFICIENT SUSTAINABLE IFEMA 2019 Annual Report MAIN FIGURES OUR ACTIVITY FINANCIAL RESULTS VISITORS COMMUNICATION Events Income Visitors Media impact 898 € 187,2 M. 4,323,775 1,119 M. International visitors Audience .Websites viewed Trade fairs and congresses Expenses 26% 51,518.7 M. 27.7 M. with exhibition €147,2 M. 123 Accredited Social media EXHIBITING COMPANIES journalists followers In-house Externally- Net profit trade fairs organised 13,193 2.1 M. trade fairs € 22,5 M. 61 Participating companies 41 Accredited Economic media valuation Congresses Trade with an fairs Investments 33,292 exhibition abroad 21,225 € 919,245.9 M. 18 3 €16,6 M. Direct International exhibitors exhibitors Festivals, concerts and EBITDA long-term events € 40,0 M. 16,902 22% ECONOMIC IMPACT ON MADRID 26 REGION* Financial debt OCCUPATION Others € 5,104 M. 749 0 € Net surface area 2 Net wealth 1,447,538 M 3.8% 2.2% € 310,1 M. of the GDP of the GDP of the city of of the Madrid Gross surface area Madrid Region 3,500,000 M2 *Source: “Study of IFEMA’s socioeconomic impact”. M.: million. © 2020 KPMG Asesores, S.L. €---M.: millions of euros. 2019 ANNUAL REPORT CLOSE DYNAMIC TRANSPARENT INSPIRING EFFICIENT SUSTAINABLE 02 2019 Annual Report Contents 03 Contents 01 02 03 05 CLOSE DYNAMIC TRANSPARENT EFFICIENT The voice of IFEMA | 04 2019: a lot to celebrate | 14 Communicating more Financial management and better | 54 report | 78 Letter from the Chairman of the The Managing Director’s vision | 16 Governing Board | 06 A year of intense -

Paris, New York, Madrid, London: the City Responds to Terror (10/18/18)

Paris, New York, Madrid, London: The City Responds to Terror (10/18/18) 00:00:25 Alice M. Greenwald: Good evening. Welcome. My name is Alice Greenwald. I'm president and CEO of the 9/11 Memorial and Museum, and it is my pleasure to welcome all of you here this evening to tonight's program, along with any of you who are tuning in live to our web broadcast at 911memorial.org/live. As always, I am delighted to see members, museum members in the audience. We welcome you, and we encourage everyone here to consider the benefits of membership. 00:00:59 You know, the 9/11 Memorial and Museum holds a unique position within the community of sites directly impacted by terrorism. One of the unexpected outcomes of creating the Memorial and Museum is that we developed an unusual expertise in the field of memorialization that other communities now struggling in the aftermath of extreme violence have found helpful. 00:01:25 For example, in the wake of the Boston Marathon bombing, we were called upon to advise the city archivist on what to collect and how best to preserve tribute that had been left all over the city in memory of those who had been killed or injured. Our staff has provided guidance to the planners of the Oslo Government Center and Utoya Island memorials, commemorating the horrific 22 July 2011 bombing and massacre. Members of our team have worked with individuals creating a memorial in Orlando to the victims of the Pulse night club shooting. -

Development of Blast Risk Assessment Framework for Financial Loss and Casualty Estimation

Clemson University TigerPrints All Dissertations Dissertations December 2019 Development of Blast Risk Assessment Framework for Financial Loss and Casualty Estimation Paresh Chandra Poudel Clemson University, [email protected] Follow this and additional works at: https://tigerprints.clemson.edu/all_dissertations Recommended Citation Poudel, Paresh Chandra, "Development of Blast Risk Assessment Framework for Financial Loss and Casualty Estimation" (2019). All Dissertations. 2518. https://tigerprints.clemson.edu/all_dissertations/2518 This Dissertation is brought to you for free and open access by the Dissertations at TigerPrints. It has been accepted for inclusion in All Dissertations by an authorized administrator of TigerPrints. For more information, please contact [email protected]. DEVELOPMENT OF BLAST RISK ASSESSMENT FRAMEWORK FOR FINANCIAL LOSS AND CASUALTY ESTIMATION A Dissertation Presented to the Graduate School of Clemson University In Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy Civil Engineering by Paresh C. Poudel December 2019 Accepted by: Dr. Weichiang Pang, Committee Chair Dr. Brandon Ross Dr. Mohammad B. Javanbarg Dr. Thomas E. Cousins ABSTRACT The entire study can be divided into four main studies. Study I presents the development of probabilistic version of popular Kingery and Bulmash (KB) blast model. The probabilistic model was developed by considering the uncertainty in the model quantified using available experimental data. The model was then applied to generate fragility curves are developed for three types of glazing under three common bombing scenarios and study 1995 Oklahoma City damage. Study II discusses on development a blast loss estimation framework for buildings where demand loads are calculated using the probabilistic blast model and capacity form seismic design. -

Soft Facts and Digital Behavioural Influencing After the 2017 Terror Attacks Full Report

FEBRUARY 2020 SOFT FACTS AND DIGITAL BEHAVIOURAL INFLUENCING AFTER THE 2017 TERROR ATTACKS FULL REPORT Martin Innes Crime and Security Research Institute, Cardiff University This is the full report from the Soft Facts And Digital Behavioural Influencing project, funded by CREST. To find out more about this project, and to see other outputs from the team, visit: www.crestresearch.ac.uk/projects/soft-facts-digital-behavioural-influencing This project reflects a growing awareness and concern amongst policymakers and practitioners about how the community impacts of terrorism and other major crime events are frequently amplified as a result of rumours, deliberately generated ‘false news’ and conspiracy theories. There is interest also in how such effects can be countered through deploying artfully constructed counter-narratives. About CREST The Centre for Research and Evidence on Security Threats (CREST) is a national hub for maximising behavioural and social science research into understanding, countering and mitigating security threats. It is an independent centre, commissioned by the Economic and Social Research Council (ESRC) and funded in part by the UK security and intelligence agencies (ESRC Award: ES/N009614/1). www.crestresearch.ac.uk ©2020 CREST Creative Commons 4.0 BY-NC-SA licence. www.crestresearch.ac.uk/copyright TABLE OF CONTENTS 1. EXECUTIVE SUMMARY ...................................................................................................................5 2. INTRODUCTION ................................................................................................................................7 -

Media Content Analysis of Governmental Impact on Terrorist Reporting

University of Lynchburg Digital Showcase @ University of Lynchburg Undergraduate Theses and Capstone Projects Spring 5-2020 Media Content Analysis of Governmental Impact on Terrorist Reporting Maggie Kaliszak [email protected] Follow this and additional works at: https://digitalshowcase.lynchburg.edu/utcp Part of the International and Area Studies Commons, International and Intercultural Communication Commons, Journalism Studies Commons, Mass Communication Commons, Political Science Commons, and the Speech and Rhetorical Studies Commons Recommended Citation Kaliszak, Maggie, "Media Content Analysis of Governmental Impact on Terrorist Reporting" (2020). Undergraduate Theses and Capstone Projects. 169. https://digitalshowcase.lynchburg.edu/utcp/169 This Thesis is brought to you for free and open access by Digital Showcase @ University of Lynchburg. It has been accepted for inclusion in Undergraduate Theses and Capstone Projects by an authorized administrator of Digital Showcase @ University of Lynchburg. For more information, please contact [email protected]. Media Content Analysis of Governmental Impact on Terrorist Reporting Maggie Kaliszak Senior Honors Project Submitted in partial fulfillment of the graduation requirements of the Westover Honors College Westover Honors College May, 2020 _________________________________ Dr. Marek Payerhin _________________________________ Dr. David Richards _________________________________ Dr. Beth Savage i Abstract When terrorism occurs, the government has to respond to it. The media also has the need to respond to terrorism if it is to report the news. Therefore, if both have a connection to terrorism, how do they work together, how do they impact each other, and is the Agenda Setting Theory useful to them? Using three recent attacks, the Boston Marathon Bombing, the Manchester Arena Attack, and the Orlando Nightclub Shooting, this paper analyzes the kind of wording used by the media reporting on terrorism and how the government influences that wording through press releases. -

DOCTOR of PHILOSOPHY Government Communication And

DOCTOR OF PHILOSOPHY Government Communication and Terrorist Organizations: Towards a Concept of “Crisis Communication” in reaction to 21st Century Islamic Terrorist Attacks for Western Governments Hamm, Dominik Award date: 2019 Awarding institution: Queen's University Belfast Link to publication Terms of use All those accessing thesis content in Queen’s University Belfast Research Portal are subject to the following terms and conditions of use • Copyright is subject to the Copyright, Designs and Patent Act 1988, or as modified by any successor legislation • Copyright and moral rights for thesis content are retained by the author and/or other copyright owners • A copy of a thesis may be downloaded for personal non-commercial research/study without the need for permission or charge • Distribution or reproduction of thesis content in any format is not permitted without the permission of the copyright holder • When citing this work, full bibliographic details should be supplied, including the author, title, awarding institution and date of thesis Take down policy A thesis can be removed from the Research Portal if there has been a breach of copyright, or a similarly robust reason. If you believe this document breaches copyright, or there is sufficient cause to take down, please contact us, citing details. Email: [email protected] Supplementary materials Where possible, we endeavour to provide supplementary materials to theses. This may include video, audio and other types of files. We endeavour to capture all content and upload as part of the Pure record for each thesis. Note, it may not be possible in all instances to convert analogue formats to usable digital formats for some supplementary materials. -

The Psychosocial Response to a Terrorist Attack at Manchester Arena, 2017 : a Process Evaluation

This is a repository copy of The psychosocial response to a terrorist attack at Manchester Arena, 2017 : a process evaluation. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/171122/ Version: Published Version Article: Hind, D. orcid.org/0000-0002-6409-4793, Allsopp, K., Chitsabesan, P. et al. (1 more author) (2021) The psychosocial response to a terrorist attack at Manchester Arena, 2017 : a process evaluation. BMC Psychology, 9 (1). 22. https://doi.org/10.1186/s40359-021-00527-4 Reuse This article is distributed under the terms of the Creative Commons Attribution (CC BY) licence. This licence allows you to distribute, remix, tweak, and build upon the work, even commercially, as long as you credit the authors for the original work. More information and the full terms of the licence here: https://creativecommons.org/licenses/ Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. [email protected] https://eprints.whiterose.ac.uk/ Hind et al. BMC Psychol (2021) 9:22 https://doi.org/10.1186/s40359-021-00527-4 RESEARCH ARTICLE Open Access The psychosocial response to a terrorist attack at Manchester Arena, 2017: a process evaluation Daniel Hind1* , Kate Allsopp2,3, Prathiba Chitsabesan4,5 and Paul French6,7 Abstract Background: A 2017 terrorist attack in Manchester, UK, affected large numbers of adults and young people. Dur- ing the response phase (first seven weeks), a multi-sector collaborative co-ordinated a decentralised response.