The OPAL Exemption Decision: Past, Present, and Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Economics of the Nord Stream Pipeline System

The Economics of the Nord Stream Pipeline System Chi Kong Chyong, Pierre Noël and David M. Reiner September 2010 CWPE 1051 & EPRG 1026 The Economics of the Nord Stream Pipeline System EPRG Working Paper 1026 Cambridge Working Paper in Economics 1051 Chi Kong Chyong, Pierre Noёl and David M. Reiner Abstract We calculate the total cost of building Nord Stream and compare its levelised unit transportation cost with the existing options to transport Russian gas to western Europe. We find that the unit cost of shipping through Nord Stream is clearly lower than using the Ukrainian route and is only slightly above shipping through the Yamal-Europe pipeline. Using a large-scale gas simulation model we find a positive economic value for Nord Stream under various scenarios of demand for Russian gas in Europe. We disaggregate the value of Nord Stream into project economics (cost advantage), strategic value (impact on Ukraine’s transit fee) and security of supply value (insurance against disruption of the Ukrainian transit corridor). The economic fundamentals account for the bulk of Nord Stream’s positive value in all our scenarios. Keywords Nord Stream, Russia, Europe, Ukraine, Natural gas, Pipeline, Gazprom JEL Classification L95, H43, C63 Contact [email protected] Publication September 2010 EPRG WORKING PAPER Financial Support ESRC TSEC 3 www.eprg.group.cam.ac.uk The Economics of the Nord Stream Pipeline System1 Chi Kong Chyong* Electricity Policy Research Group (EPRG), Judge Business School, University of Cambridge (PhD Candidate) Pierre Noёl EPRG, Judge Business School, University of Cambridge David M. Reiner EPRG, Judge Business School, University of Cambridge 1. -

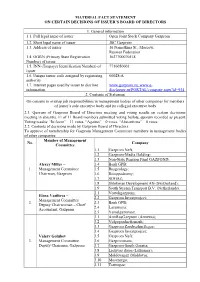

Material Fact Statement on Certain Decisions of Issuer’S Board of Directors

MATERIAL FACT STATEMENT ON CERTAIN DECISIONS OF ISSUER’S BOARD OF DIRECTORS 1. General information 1.1. Full legal name of issuer Open Joint Stock Company Gazprom 1.2. Short legal name of issuer JSC Gazprom 1.3. Address of issuer 16 Nametkina St., Moscow, Russian Federation 1.4. OGRN (Primary State Registration 1027700070518 Number) of issuer 1.5. INN (Taxpayer Identification Number) of 7736050003 issuer 1.6. Unique issuer code assigned by registering 00028-А authority 1.7. Internet pages used by issuer to disclose www.gazprom.ru; www.e- information disclosure.ru/PORTAL/company.aspx?id=934 2. Contents of Statement On consent to overlap job responsibilities in management bodies of other companies for members of issuer’s sole executive body and its collegial executive body 2.1. Quorum of Gazprom Board of Directors meeting and voting results on certain decisions: meeting in absentia, 11 of 11 Board members submitted voting ballots, quorum recorded as present. Voting results: “In favor” – 11 votes, “Against” – 0 votes, “Abstentions” – 0 votes. 2.2. Contents of decisions made by Gazprom Board of Directors: To approve of membership for Gazprom Management Committee members in management bodies of other companies: Member of Management No. Company Committee 1.1 Gazprom Neft; 1.2 Gazprom-Media Holding; 1.3 Non-State Pension Fund GAZFOND; Alexey Miller – 1.4 Bank GPB; 1. Management Committee 1.5 Rusgeology; Chairman, Gazprom 1.6 Rosippodromy; 1.7 SOGAZ; 1.8 Shtokman Development AG (Switzerland); 1.9 South Stream Transport B.V. (Netherlands). 2.1 Vostokgazprom; Elena Vasilieva – 2.2 Gazprom Investproject; Management Committee 2. -

Preisliste 2020 Für Transportbeton Und Betonfördergeräte Gültig Ab 01.01.2020

www.happy-beton.de Preisliste 2020 für Transportbeton und Betonfördergeräte gültig ab 01.01.2020 Mit dem Erscheinen dieser Preisliste verlieren alle vorherigen Preislisten ihre Gültigkeit. (nur gültig für Bauunternehmen des Bauhauptgewerbes) Transportbeton Betonpumpen Kieswerke Schalungssteine Mobile Betonblöcke www.happy-beton.de Unsere Standorte Flensburg 3 Kiel 21 Bergen Kiel Stralsund Stralsund Miltzow 14 19 10 8 2 RostockRostock GrimmenGrimmen Lubmin BadBad A20 Greifswald DoberanDoberan Greves- A20 Jarmen mühlen Wismar 6 Lübeck 9 DemminDemmin A23 Lübeck 24 Güstrow11 1 7 A7 Dorf Mecklenburg 22 A1 Güstrow A20 Gadebusch5Brüsewitz A19 Teterow Anklam Eggesin Pinnow/SN Bremer- Brüsewitz Schwerin 16 haven Schwerin Waren23 Pasewalk HAMBURG HAMBURG A241A14 NeubrandenburgNeubrandenburg A24 WarenMöllenhagen Szczecin 4 Szczecin BoizenburgB5 17 Boizenburg 15 Neustadt- 20 Prenzlau Glewe Röbel A1 LudwigslustLudwigslust PL 12 Pinnow 18 Bremen LüneburgLüneburg Bremen Heiddorf 13 Perleberg Schwedt A14 Hitzacker B189 A7 Uelzen 29 30 A1A111 Geestgott-Geest- HeiligenfeldeSalzwedel gottberg A24 berg 33 25Arneburg OsterburgOsterburg Arneburg 31 Stendal 34 Gardelegen 28 Lindstedt Stendal Tangermünde LüderitzLüderitz 32 Brandenburg BERLIN Wolfsburg A12 Hannover A14 A2 A10 26 A2 Barleben 27 Neuseddin Biederitz A13A13 Magdeburg Magdeburg Zerbst A7 A14 Lutherstadt Wittenberg Cottbus Köthen Dessau A9 A15 A13 Stand: 04/17 Ihre Ansprechpartner 2, 11, 19, 22 1, 7 26, 27 Lars Mieser René Wojtaszyk Jens von Damitz Tel. 03996 1505428 Tel. 0391 3002522 Fax 03996 1505421 Fax 03991 673320 Fax 0391 3002524 Mobil 0171 7354193 Mobil 0174 7365841 Mobil 0172 1420570 [email protected] [email protected] [email protected] 16, 20, 23 3, 6, 8, 10, 14, 21 25, 28, 29, 30, 31, 32, 33, 34 Sebastian Höhr Uwe Schwiaton Carola Gebauer Tel. -

Consolidated Financial Statements 2018

GAZPROM GERMANIA CONSOLIDATED FINANCIAL STATEMENTS 2018 www.gazprom-germania.de Consolidated Financial Statements 2018 GAZPROM Germania GmbH, Berlin Page 2 CONTENTS Contents ................................................................................................................................................. 2 Abbreviations ......................................................................................................................................... 5 Group management report ................................................................................................................... 7 Economic and regulatory conditions ................................................................................................... 7 General economic conditions .......................................................................................................... 7 Energy policy and regulatory environment ...................................................................................... 8 Business performance ......................................................................................................................... 9 Group performance ......................................................................................................................... 9 Marketing and trading business .................................................................................................... 10 Gas storage .................................................................................................................................. -

Motorradtouren Am Stettiner Haff

Bikertouren am Haff idyllische Touren 4 attraktive Ausflugsziele 4 bikerfreundliche Unterkünfte 4 www.motorradfahren-am-haff.de Tour durch das 1 Land der drei Meere (Ueckermünde - Pasewalk - Strasburg - Woldegk - Friedland) ca. 180 km So nämlich wird die Gegend im Nordosten des Landes auch bezeichnet. Zwei davon sind das Wald-Meer und das Land-Meer. Das dritte „Meer“ könnt ihr selbst herausfinden. Am Stettiner Haff entlang geht es durch die Ueckermünder Heide und die Brohmer Berge, vorbei am Galenbecker See. Der Helpter Berg ist mit 179 m die höchste Erhebung des Landes. Von hier aus gelangt man direkt in die Windmühlenstadt Woldegk. Ueckermünde Altwap Friedland . Hintersee Rothemühl Torgelow Strasburg Woldegk Pasewalk Löcknitz Woldegker Windmühle Schloss Rattey Ukranenland Helpter Berg Ukranen-Tour 2 (Ueckermünde - Torgelow - Rothemühl - Anklam) ca. 130 km Durch die Ueckermünder Heide geht es direkt in das Ukranenland nach Torgelow mit der historischen Bootswerft und der Ukranensiedlung. Die Brohmer Berge, der Galenbecker See und die Große Friedländer Wiese sind echte landschaftliche Höhepunkte- die Straßen ein Hochgenuß für Cruiser. Sehenswert in Anklam: das Otto Lilienthal- Museum. Das Peenetal-Moor bei Ducherow (hier gibt es auch ein Motorradmuseum) ist ein Muss auf dem Weg zurück nach Ueckermünde. Anklam Strippow Ducherow Ueckermünde Torgelow Rothemühl Torgelow Kirche Mönkebude Peenetal Grambin Ostvorpommern-Tour 3 (Ueckermünde - Anklam - Wolgast - Lubmin) ca. 225 km Ausgangspunkt ist wiederum die Hafenstadt Ueckermünde. Weiter geht es und auf bestens präparierten, kurvenreichen Nebenstrecken über Anklam wieder nach Greifswald vorbei am ehemaligen KKW Lubmin, dort gibt es eine sehr interessante Ausstellung zur Geschichte der Kernkraft. Im Fischereihafen von Freest empfehlen wir eine Pause, denn hier gibt es die leckersten Fischbrötchen südlich des Nordpols. -

Wirtschaftsstandort Landkreis Ostvorpommern

Wirtschaftsstandort LANDKREIS OSTVORPOMMERN 7%+! INFOI RMATIONSBROSCH¶REN &¶R+OMMUNEN ,ANDKREISE +LINIKEN )NDUSTRIE UND(ANDWERKSORGANISATIONEN "ILDUNGS UND INFORMATIV 3OZIALEINRICHTUNGEN &REMDENVERKEHRSVEREINE ODER5NTERNEHMENUNSERE0RODUKTESINDIMMER PRAKTISCH DASIDEALE-EDIUMF¶RFFENTLICHKEITSARBEIT ÎIM0RINT UND)NTERNETBEREICH AKTUELL 5NSEREBREITE0RODUKTPALETTEWIRDAUCH3IE KOMPETENT ¶BERZEUGEN)NDUSTRIE (ANDWERK (ANDEL UND$IENSTLEISTUNGNUTZENUNSERE"ROSCH¶REN KREATIV ALSOPTIMALE0LATTFORMF¶R5NTERNEHMENS PRSENTATIONEN SOLIDE 7IR¶BERZEUGENDURCH%RFAHRUNG 1UALITT FINANZIERT UNDMITGUTEN)DEEN5NDDASSEITMEHR ALS*AHREN 7%+!INFOVERLAGGMBH ,ECHSTRAEØ-ERING 4ELEFON % -AILINFO WEKA INFODE WWWWEKA INFODE Landkreis Ostvorpommern G r u ß w o r t G r e e t i n g „Gestatten Ostvorpommern“ “Introducing Ostvorpommern” Sehr geehrte Damen und Herren, Dear Sir or Madam, die aktuelle Broschüre „Wirtschaftsstandort Landkreis The idea behind this current “Ostvorpommern Rural District as Ostvorpommern“möchte Sie über die Wirtschaftsstruktur a Business Location” brochure is to give you information on and im Bereich Ostvorpommern informieren und interessie- arouse your interest in the economic structure of the Ostvorpom- ren. mern region. Für die Gemeinden und den Landkreis ist die wirt- The economic development of the Ostvorpommern region is of schaftliche Entwicklung der Region Ostvorpommern von primary importance to the municipalities and the rural district. Its erstrangiger Bedeutung. Wichtiges Planungsinstrument key planning instrument is the Regional -

Transporting Russian Natural Gas to Western Europe – from Source to Market

FACT SHEET December 2013 Transporting Russian Natural Gas to Western Europe – From Source to Market Overview of the pipelines connecting to Nord Stream Owner of the pipeline Operator 1 Bovanenkovo-Ukhta pipeline 2 SRTO-Torzhok pipeline 3 Brotherhood pipeline Gazprom Gazprom 4 Pochinki-Gryazovets pipeline 5 Gryazovets-Vyborg pipeline 6 Nord Stream Pipeline Nord Stream AG shareholders: Nord Stream AG OAO Gazprom (51%), Wintershall Holding GmbH (15.5%), E.ON SE (15.5%), N.V. Nederlandse Gasunie (9%), GDF SUEZ (9%) OPAL Gastransport W & G Beteiligungs-GmbH & Co. KG (80%), GmbH & Co. KG, 7 OPAL pipeline Lubmin-Brandov Gastransport GmbH (20%) Lubmin-Brandov Gastransport GmbH NEL Gastransport GmbH, NEL Gastransport GmbH (51%), Gasunie Gasunie Ostseeanbindungsleitung GmbH 8 NEL pipeline Ostseeanbindun (25%), gsleitung GmbH, Fluxys Deutschland GmbH (24%) Fluxys Deutschland GmbH 1 Industriestrasse 18 Moscow Branch 6304 Zug, Switzerland ul. Znamenka 7, bld. 3 Tel. +41 (0) 41 766 91 91 119019 Moscow, Russia Fax +41 (0) 41 766 91 92 Tel. +7 (0) 495 229 65 85 www.nord-stream.com Fax +7 (0) 495 229 65 80 Gas production sources Russia is one of the countries with the largest gas reserves in the world. With 32,900 bcm, Russia has 17.6% of the world's currently known natural gas reserves.1 This is equal to around 56 years of Russian gas production at 2012 levels or around 74 years of EU gas demand at 2012 levels. The International Energy Agency (IEA) estimates the ultimately recoverable gas resources2 in Russia to be three times as high – 127,000 bcm, of which 21,000 bcm have already been produced. -

Jarmen , Den O5

- Die Veröffentlichung dieser Bekanntmachung erfolgt am 23.07.2018 - Gemeinde Völschow Beschlüsse der Gemeindevertretersitzung der Gemeinde Völschow vom 18.06.2018 Beschluss zur Festsetzung der Jahresrechnung 2017 Die Gemeindevertretung stellt das Ergebnis der Jahresrechnung 2017 der Gemeinde Völschow fest. Beschlussnummer: 010-04/2018 Abstimmungsergebnis: gesetzl. Mitgliederzahl: 8 Anwesend: 7 Dafür: 7 Dagegen: 0 Stimmenenthaltung: 0 Beschluss zur Entlastung des Bürgermeisters für das HH-Jahr 2017 Aufgrund der geprüften und festgestellten Ergebnisse der Jahresrechnung der Gemeinde Völschow für das Haushaltsjahr 2017 und der vorbehaltlosen Empfehlung des RPA wird die Entlastung des Bürgermeisters gemäß § 60 Abs.5 Satz 2 KV M-V erteilt. Beschlussnummer: 011-04/2018 Abstimmungsergebnis: gesetzl. Mitgliederzahl: 8 Anwesend: 6 Dafür: 6 Dagegen: 0 Stimmenenthaltung: 0 Aufgrund des § 24 der Kommunalverfassung haben folgende Mitglieder der Gemeindevertretung weder an der Beratung noch an der Abstimmung mitgewirkt: Herr Breitsprecher Beschluss über die Entgegennahme von Spenden für das Haushaltsjahr 2017 Die Gemeindevertretung der Gemeinde Völschow beschließt über die Entgegennahme von Spenden gemäß § 5 Abs.2 der Hauptsatzung vom 13.05.2015 für das Haushaltsjahr 2017 lt. beiliegenden Anla- gen. Beschlussnummer: 012-04/2018 Abstimmungsergebnis: gesetzl. Mitgliederzahl: 8 Anwesend: 7 Dafür: 7 Dagegen: 0 Stimmenenthaltung: 0 Genehmigung einer Eilentscheidung des Bürgermeisters zu einer überplanmäßigen Ausgabe Die Gemeindevertretung der Gemeinde Völschow genehmigt die Eilentscheidung des Bürgermeisters vom 24.05.2018 gemäß § 39 Abs.3 KV M-V zur Finanzierung einer überplanmäßigen Ausgabe in Höhe von 15.600 € für anfallende Personalkosten durch das befristete Arbeitsverhältnis eines weiteren Ge- meindearbeiters vom 14.5.2018 bis zum 30.09.2018 und der Arbeitszeiterhöhung des bisherigen Ge- meindearbeiters auf 35 Arbeitsstunden von März bis August 2018. -

The Real Financial Cost of Nord Stream 2

THE REAL FINANCIAL COST OF NORD STREAM 2 – ECONOMIC SENSITIVITY ANALYSIS OF THE ALTERNATIVES TO THE OFFSHORE PIPELINE THE REAL FINANCIAL COST OF NORD STREAM 2 – economic sensitivity analysis of the alternatives to the offshore pipeline Author: Piotr Przybyło Economy and Energy Programme Warsaw 2019 TABLE OF CONTENTS I. Pipeline from nowhere to nowhere 6 II. A €17.2 billion investment 7 III. The construction cost of offshore vs onshore 8 IV. Three times cheaper alternative onshore routes 9 V. The true motives behind the Nord Stream 2 14 PIPELINE FROM NOWHERE Siberia to Baltic coast in Russia. Similarly, newly TO NOWHERE constructed pipelines will transport 55 bcma of gas over 800 km down south from the Baltic shore In any economic analysis of Nord Stream 2 the first in Germany to one of the biggest European gas question to be considered is the actual cost of the hubs in Austria, its final destination. Consequently, project. Over the last couple of years, a variety of the overall construction cost of Nord Stream 2 publications have provided widely differing cost route should include all the additional necessary projections. The recent data suggest that Nord infrastructure to achieve this objective. Conclusively, Stream 2 capital investment will reach €9,5-10 the construction cost of the offshore pipeline is billion. only a portion of the bigger project which aims to deliver Russian gas to South-West of Europe. Yet, the €9,5-10 billion is not the final construction cost of the project. Nord Stream 2 will not fulfil its Here, the main focus will be put on the economic function in isolation. -

Nord Stream Delivers Gas to Lubmin

European gas grid gas European gas from Nord Stream is delivered to the the to delivered is Stream Nord from gas At the landfall facility in Lubmin, Germany, Germany, Lubmin, in facility landfall the At LUBMIN HEATH: European Mainland European High Tech AN ENERGY SITE A Connecting Nord the at Arrives Natural Gas Gas Natural for Quality In the context of the energy Hub on the strategy 2020 of Mecklenburg- Stream and Safety Western Pomerania, Lubmin developed into an energy hub German Coast with a range of energy sources Delivers More than 167 million standard cubic metres feeding electricity into the German (later: cubic metres) of natural gas can be distribution grid. The Lubmin landfall The Bovanenkovo oil and gas gas transport systems. Currently, condensate deposit is the main up to 36 billion cubic metres of processed in the receiving station in Lubmin facility is the logistical natural gas base for the Nord gas can flow through the OPAL every day. A sophisticated series of valves, filters, link between the Nord Gas to Lubmin DISMANTLING AND Stream Pipeline. Discovered and pipeline annually. This amount preheating, measuring and control facilities Stream Pipeline and CONSTRUCTION estimated gas reserves amount is enough to supply a third of ensure that the gas is of top quality, and the right the European gas to 4.9 trillion cubic meters which Germany with natural gas for a quantities are flowing to the connecting pipelines distribution grid. The makes the Bovanenkovo field a year. The pipeline runs south at the right pressure and temperature. In 1995, the Nord nuclear power natural gas that arrives reliable source of natural gas for from Lubmin to Brandov, in the plant in Lubmin was shut down. -

Stakeholder Engagement Plan – Germany

Stakeholder Engagement Plan – Germany Nord Stream 2 AG | Mar-19 W-PE-EMS-PGE-PLA-800-SEPGEREN-06 Page 2 of 44 Table of Contents Abbreviations and Definitions ............................................................................................................... 4 Executive summary ................................................................................................................................ 5 1 Brief description of the Project ..................................................................................................... 7 1.1 Project Overview .................................................................................................................. 7 1.2 The Nord Stream 2 Project in Germany ............................................................................... 7 1.3 Relevant Non-Project Activities and Facilities ...................................................................... 9 1.4 Stages of Project Implementation......................................................................................... 10 2 Applicable Stakeholder Engagement Requirements .................................................................. 10 2.1 German Regulatory Requirements for Community Engagement ......................................... 10 2.2 Requirements of International Conventions ......................................................................... 11 2.3 Performance Standards of International Financial Institutions ............................................. 11 2.4 Internal Policies and -

Amtsblatt-2020-02-Februar Hp.Pdf

ZZÜSSOWERZZZÜÜÜÜSSOWERSSOWERSSOWERSSOWER AMTSBLATTAMTSBLATTAMTSBLATTAMTSBLATT BEKANNTMACHUNGEN UND INFORMATIONEN DES AMTES ZÜSSOW mit der amtsangehörenden Stadt Gützkow und den Gemeinden Bandelin, Gribow, Groß Kiesow, Groß Polzin, Karlsburg, Klein Bünzow, Murchin, Rubkow, Schmatzin, Wrangelsburg, Ziethen und Züssow Jahrgang 16 Mittwoch, den 12. Februar 2020 Nummer 02 Turnierwochenende in Gützkow „Amtliches Bekanntmachungsblatt“ - kostenlos Postwurfsendung sämtliche Haushalte sämtliche Postwurfsendung Züssow – 2 – Nr. 02/2020 Inhaltsverzeichnis Informationen aus dem Amtsbereich 17. Jahresrechnung 2018 der Gemeinde Schmatzin 22 1. Öffnungszeiten des Amtes 3 18. Beschlüsse der Gemeindevertretung Wrangelsburg 2. Sprechzeiten der Amtsvorsteherin und vom 19.12.2019 22 der Bürgermeister 3 19. 3. Satzung zur Änderung der Satzung über 3. Erreichbarkeit der Mitarbeiter des Amtes 3 die Erhebung von Gebühren zur Deckung 4. Öffnungszeiten der Bibliotheken 5 der Beiträge und Umlagen des Wasser- und 5. Sprechzeiten der Schiedsstelle des Amtes Züssow 6 Bodenverbandes der Gemeinde Wrangelsburg 22 6. Sitzungstermine 6 20. Jahresrechnung 2018 der Gemeinde Wrangelsburg 23 7. Höchstgeschwindigkeit in den Ortschaften 6 21. Beschlüsse der Gemeindevertretung Züssow 8. Grabstellenaufruf 6 vom 16.01.2020 23 9. Öffentlich-rechtlicher Vertrag zur Bildung 22. Bekanntmachung der Gemeinde Züssow über den einer Verwaltungsgemeinschaft zur Inanspruchnahme Beschluss vom 05.12.2019 über die Änderung eines Rechnungsprüfungsamtes des Aufstellungsbeschlusses vom 07.11.2018 für die örtliche Rechnungsprüfung 6 zur 2. Änderung des Flächennutzungsplanes 10. Information bezüglich der Verteilung der Gemeinde Züssow 25 des Amtsblattes im Dezember 9 23. Jahresrechnung 2018 der Gemeinde Züssow 26 Amtliche Bekanntmachungen und Informationen Schulen und Kita 1. Haushaltssatzung des Amtes Züssow 1. Teilnahme an der Kreismathematikolympiade 26 für das Haushaltsjahr 2020 9 2. Orchestermusiker zu Gast 26 2.