ITC Limited: Rating Reaffirmed

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A STUDY on BEHAVIOUR PATTERN of DIVIDEND PAY-OUT: SELECTED BLUE-CHIP COMPANIES in INDIA Author Co - Author Dr.K.R.Sivabagyam A.Ranjitha Assistant Professor K

Compliance Engineering Journal ISSN NO: 0898-3577 A STUDY ON BEHAVIOUR PATTERN OF DIVIDEND PAY-OUT: SELECTED BLUE-CHIP COMPANIES IN INDIA Author Co - Author Dr.K.R.Sivabagyam A.Ranjitha Assistant Professor K. Madhu Varshini Department of Commerce N.Deekshithaa Sri Krishna Arts and Science College S. Kabilambika E-mail Id: [email protected] II M.Com Students MOB: 7871809789 E-mail Id: [email protected] [email protected] [email protected] [email protected] Mob: 9486939255; 9715184177; 9025868186 ABSTRACT Reliance Industries, Tata Consultancy services (TCS) and WIPRO in India and The term blue-chip was used to describe observe the behaviour pattern of the three high- priced stocks in 1923 when Oliver measures of dividend policy of the blue- Gingold, an employee at Dow Jones chip companies in India. observed certain stocks trading at $200 or more per share. Poker players bet in blue, KEYWORDS: Blue Chip Companies, white and red chips with blue chips having Dividend Policy, Investment Proposals. more value than both red and white chips. INTRODUCTION Today, blue chips stocks don’t necessarily refer to stocks with a high price tag, but In the exchange of India there are literally more accurately to stocks of high-quality thousands of companies but when it comes companies that have with stood the test of to financial stability only few companies time. A blue-chip company is a are financially stable and in other financial multinational firm that has been in aspects. Long term investors seek out for operation for a number of years. -

Name Surname

Aniket Agarwal Partner Emerald House 1B Old Post Office Street Kolkata 700 001 India T: +91 33 2248 7000 F: +91 33 2248 7656 E: [email protected] Practices: Aniket Agarwal is a Partner in the Corporate and Commercial Corporate and Commercial practice group in the Kolkata office. He specialises in corporate Mergers and Acquisitions restructuring, mergers, acquisitions, demergers, Dispute Resolution reconstructions and capital and debt reorganisation. Aniket also has considerable experience in varied other areas of Education: practice and advises clients on various aspects of law, including LL.B., University of Calcutta family arrangements, securities laws, joint ventures and other (1991) commercial contracts, constitutional writs, suits, mismanagement and oppression petitions, insolvency and Professional Affiliations: winding up and other commercial and civil litigation. Bar Council of West Bengal Aniket has handled mergers, acquisitions, demergers and Incorporated Law Society of litigation in various jurisdictions in the country, including Kolkata Kolkata, Mumbai, Delhi, Chennai, Bengaluru, Hyderabad, Sectors: Ahmedabad, Bhubaneswar Jodhpur, Gwalior, Allahabad, FMCG Gauhati, Shillong and Shimla. Manufacturing Representative Matters: In his areas of expertise, Aniket has represented and advised the following clients: Mergers and Acquisitions: . ITC Limited and its subsidiaries on various mergers and demergers, including Merger of ITC Bhadrachalam Paperboards Limited and ITC Hotels Limited with ITC Limited and Demerger of Non-Engineering Business of Wimco Limited to ITC Limited; . Hooghly Met Coke & Power Company Limited on its merger with Tata Steel Limited; . TATA Global Beverages Limited (TGBL) and its subsidiaries on various Mergers and Reconstructions, including Merger of Mount Everest Mineral Water Limited with TGBL, reconstruction by transfer of plantation business to Amalgamated Plantations Private Limited and Merger of wholly owned subsidiaries of TGBL with TGBL; . -

Risk Profile Performance Vs Benchmark Asset Mix Performance

Performance Summary May 31, 2019 RICH Fund III ULIF 050 17/03/08 LRICH3 105 Fund Objective: Inception Date March 17, 2008 The objective of the fund is to generate ₹ superior long-term returns from a diversified Assets Invested 248.3 Million portfolio of equity and equity related instruments of companies operating in four Fatema Pacha important types of industries viz., Resources, Fund Manager(s) Funds Managed: 8 (8 Equity) Investment-related, Consumption-related and Human Capital leveraged industries. Benchmark BSE 200 NAV ₹ 26.0105 as on May 31, 2019 Return Risk Profile Fund Performance (As on May 31, 2019 ) Since 1 Month 6 Month 1 Year 2 Year 3 Year 4 Year 5 Year Inception Fund Return 1.62% 8.41% 3.84% 6.2% 9.95% 6.58% 10.13% 8.9% Benchmark Return 1.45% 7.78% 7.14% 9.41% 13.14% 8.98% 11.05% 9.31% Performance Vs Benchmark Asset Mix (As on May 31, 2019) 30.00 4% ₹ 9.28 Million 25.00 20.00 ) ₹ V in ( NA 15.00 10.00 5.00 Jan 10 Jan 12 Jan 14 Jan 16 Jan 18 96% ₹ 238.99 Million Period Equity and Equity related securities Minimum 80% RICH Fund III BSE 200 Debt, Money Market and Cash Maximum 20% Details are as per IRDAI Product Filing. Returns greater than 1 year are annualized. Past performance is not indicative of future performance. Performance Summary May 31, 2019 % of Invested Top 10 Sectors * Assets Financial and insurance activities 24.42% Computer programming consultancy and related activities 12.16% Infrastructure 9.13% Manufacture of coke and refined petroleum products 6.74% Manufacture of chemicals and chemical products 5.75% Manufacture of tobacco products 4.81% Manufacture of motor vehicles trailers and semi-trailers 3.71% Manufacture of pharmaceuticalsmedicinal chemical and botanical 2.98% products Manufacture of electrical equipment 2.44% Manufacture of other non-metallic mineral products 2.32% OTHERS 25.54% *As per IRDAI NIC industry classification Details are as per IRDAI Product Filing. -

Charting Dynamic Trajectories: Multinational Firms in India

Charting Dynamic Trajectories: Multinational Firms in India The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Choudhury, Prithwiraj, and Tarun Khanna. "Charting Dynamic Trajectories: Multinational Firms in India." Special Issue on Business, Networks, and the State in India. Business History Review 88, no. 1 (Spring 2014): 133–169. Published Version http://dx.doi.org/10.1017/S000768051300144X Citable link http://nrs.harvard.edu/urn-3:HUL.InstRepos:28538431 Terms of Use This article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Open Access Policy Articles, as set forth at http:// nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of- use#OAP Prithwiraj Choudhury and Tarun Khanna Charting Dynamic Trajectories: Multinational Firms in India In this article, we provide a synthesizing framework that we call the “dynamic trajectories” framework to study the evolution of multinational firms (MNCs) in host countries over time. We argue that a change in the policy environment in a host country presents a focal MNC with two sets of interrelated decisions. First, the MNC has to decide whether to enter, exit, or stay in the host country at the onset of each policy epoch; second, conditional on the first choice, it has to decide on its local responsiveness strategy at the onset of each policy epoch. India, which experienced two policy shocks—shutting down to MNCs in 1970 and then opening up again in 1991—offers an interesting laboratory to explore the “dynamic trajectories” perspective. -

Business Organizations

CHAPTER 3 BUSINESS ORGANIZATIONS LEARNING OUTCOMES After studying this unit, you will be able to: w Have an overview of corporate history of some of the selected Indian and Global companies. w Gain information about management teams of selected companies. w Know the vision, mission and core values of dierent companies. w Know the market and nancial performance of dierent companies. w Gain vital information on products and services of famous brands of dierent companies. w Analyse a company’s information as a business analyst. © The Institute of Chartered Accountants of India ICAI _ICAI_Business and Commercial Konwledge_Chp_03-nw.indd 1 7/27/2017 3:53:35 PM 3.2 BUSINESS AND COMMERCIAL KNOWLEDGE CHAPTER OVERVIEW OVERVIEW OF SELECTED COMPANIES INDIAN COMPANIES GLOBAL COMPANIES • Adani Ports and Special Economic Zone Ltd. • Deutsche Bank • Asian Paints Ltd. • American Express • Axis Bank Ltd. • Nestle • Bajaj Auto Ltd. • Microsoft Corporation • Bharti Airtel Ltd. • IBM Corporation • Bharat Petroleum Corporation Ltd. • Intel Corporation • Cipla Ltd. • HP • Coal India Ltd. • Apple • Dr. Reddy’s Laboratories Ltd. • Walmart • GAIL (India) Ltd. • HDFC Bank Ltd. • ICICI Bank Ltd. • Indian Oil Corporation Ltd. • Infosys Ltd. • ITC Ltd. • Larsen & Toubro Ltd. • NTPC Ltd. • Oil & Natural Gas Corporation Ltd. • Power Grid Corporation of India Ltd. • Reliance Industries Ltd. • State Bank of India • Tata Sons Limited • Wipro Ltd. © The Institute of Chartered Accountants of India ICAI _ICAI_Business and Commercial Konwledge_Chp_03-nw.indd 2 7/27/2017 3:53:35 PM BUSINESS ORGANIZATIONS 3.3 3.1 INTRODUCTION A company overview is the most eective way to acquire business intelligence and gain vital information about a company, its businesses, their products, services and processes, prospects, customers, suppliers, competitors; etc. -

Board of Directors and Committees

Board of Directors Chairman & Managing Director Non-Executive Directors Sanjiv Puri Shilabhadra Banerjee Anand Nayak Hemant Bhargava Nirupama Rao Executive Directors Arun Duggal Ajit Kumar Seth Atul Jerath Meera Shankar Nakul Anand Sunil Behari Mathur David Robert Simpson Sumant Bhargavan Rajiv Tandon (also Chief Financial Officer) Board Committees Audit Committee CSR and Sustainability Nomination & S B Mathur Chairman Committee Compensation Committee S Banerjee Member S Puri Chairman S Banerjee Chairman H Bhargava Member H Bhargava Member A Nayak Member A Duggal Member A Jerath Member S Puri Member R Tandon Invitee N Rao Member M Shankar Member M Ganesan Invitee A K Seth Member R K Singhi Secretary (Head of Internal Audit) M Shankar Member Representative of Invitee D R Simpson Member the Statutory Auditors R K Singhi Secretary R K Singhi Secretary Securityholders Independent Directors Relationship Committee Committee A Nayak Chairman S Banerjee Member B Sumant Member A Duggal Member R Tandon Member S B Mathur Member R K Singhi Secretary A Nayak Member N Rao Member A K Seth Member M Shankar Member Corporate Management Executive Vice President & Company Secretary Rajendra Kumar Singhi Committee General Counsel S Puri Chairman Angamuthu Shanmuga Sundaram N Anand Member Investor Service Centre 37 Jawaharlal Nehru Road, Kolkata 700 071, India B Sumant Member Telephone nos. : 1800-345-8152 (toll free) R Tandon Member 033 2288 6426 / 0034 Facsimile no. : 033 2288 2358 C Dar Member e-mail : [email protected] S K Singh Member Statutory Auditors S Sivakumar Member S R B C & CO LLP R K Singhi Secretary Chartered Accountants, Mumbai Registered Office Virginia House 37 Jawaharlal Nehru Road, Kolkata 700 071, India Telephone no. -

Birla Insurance Fund Pager Individual

ABSLI Fund Features Individual funds Individual funds Defined asset allocation Fund Date of Equity Debt Money Market & Cash management Name of fund inception Risk profile charges Min Max Min Max Min Max Equity funds Large cap funds Maximiser 12-Jun-07 80% 100% 0% 20% 0% 20% 1.35% High Maximiser Guaranteed 01-Jan-14 80% 100% 0% 20% 0% 20% 1.35% High Magnifier 12-Aug-04 50% 90% 10% 50% 0% 40% 1.35% High Super 20 06-Jul-09 80% 100% 0% 20% 0% 20% 1.35% High Capped Nifty Index 24-Sep-15 90% 100% 0% 10% 0% 10% 1.25% High MNC 15-Feb-19 80% 100% 0% 20% 0% 20% 1.35% High Dividend yield fund Value & Momentum 9-Mar-12 80% 100% 0% 20% 0% 20% 1.35% High Mid cap fund Multiplier 30-Oct-07 80% 100% 0% 20% 0% 20% 1.35% High Pure investing fund Pure Equity 09-Mar-12 80% 100% 0% 20% 0% 20% 1.35% High Asset allocation fund Asset Allocation 24-Sep-15 10% 80% 10% 80% 0% 40% 1.25% High Balanced funds Creator 23-Feb-04 30% 50% 50% 70% 0% 40% 1.25% Medium Enhancer 22-Mar-01 20% 35% 65% 80% 0% 40% 1.25% Medium Balancer 18-Jul-05 10% 25% 75% 90% - - 1.25% Medium Builder 22-Mar-01 10% 20% 80% 90% 0% 40% 1.00% Medium Protector 22-Mar-01 0% 10% 90% 100% 0% 40% 1.00% Medium FixedFixed income income funds funds Income Advantage 22-Aug-08 0% 0% 100% 100% 0% 40% 1.00% Low Income Advantage Guaranteed 01-Jan-14 0% 0% 100% 100% 0% 40% 1.00% Low Assure 12-Sep-05 0% 0% 100% 100% 0% 90% 1.00% Low Liquid Plus 09-Mar-12 0% 0% 100% 100% 0% 90% 1.00% Low Benchmark Composition Fund Name SFIN Weightage Index Weightage Index Weightage Index Maximiser 90% BSE 100 - - 10% Crisil Liquid -

Dabur India (DIL) Continue to Report Robust Results with 18.1% Domestic Volume Growth Led by Strong Traction in Health Supplement, Oral Care, OTC

DaburTAT India (DABIND) CMP: | 515 Target: | 620 (20%) Target Period: 12 months BUY January 31, 2021 Best placed to ride naturals, herbal consumption trend Dabur India (DIL) continue to report robust results with 18.1% domestic volume growth led by strong traction in health supplement, oral care, OTC & ethical businesses. The company reported 16% consolidated revenue growth with 19.5% India FMCG growth & 13% international business Particulars growth. The higher penetration led growth continued in health supplement and oral care segments with 34.7% & 28% jump in sales, respectively. DIL Particular (| crore) Amount raised its ad spends (170 bps higher) behind core & power brands, which, in Market Capitalization 90,521.2 Total Debt (FY20) 471.8 turn, benefited most new launches under core brands. New products Cash and Investments (FY20) 3,611.6 Update Result (launched in the last three quarters) contributing 4-5% to the sales now. The EV 87,381.4 company maintained its gross margins at 50.4% (31 bps higher) while 52 week H/L (|) 552 / 385 employee spends sustained at corresponding quarter level. DIL was able to Equity capital 176.6 save 113 bps overhead spends by cost rationalisation efforts in a post Face value (|) 1.0 pandemic period. Operating profit increased 16.5% to | 574.2 crore. The company was able to maintain its operating margins at 21% despite higher Key Risk ad-spends. PAT grew 23.7% to | 493.5 crore mainly on account of higher operating profit, lower interest cost & lower tax provisioning. Any steep increase in raw material prices could impact operating New launches driving growth margins negatively going forward The company continued to aggressively launch new products across The growth in health supplement categories. -

Itc Infotech India Limited

ITC INFOTECH INDIA LIMITED Other employees employed for a part of the year and in receipt of remuneration aggregating ` 8,50,000/- or more per month Name Age Designation Gross Net Qualifications Experience Date of Previous Employment/ Remuneration Remuneration (Years) Commencement Position held ` ` of Employment 1 2 3 4 5 6 7 8 9 TALWAR ANAND 61 Senior Vice President 10339686 6049657 M.B.A. 35 9-Apr-01 Reliance Telecom Ltd Vice President - HRM S.G VENKATESH 50 Senior Vice President - IT Services 9641519 6401901 M.B.A. 27 26-Sep-16 Infosys Associate Project Manager RANADE AJIT ## 45 Senior Manager - Business Development 6632816 3170173 M.E 18 18-Apr-16 Capgemini Business Development Manager N.K. KRISHNAN SANTOSH ## 45 Senior Manager - Key Accounts 5653346 5653346 M.B.A. 20 31-Jan-13 Core Dynamics General Manager - Sales GHOSH DEEPANKAR 58 Senior Vice President - IT Services 4923022 3652614 B.TECH. 35 8-Jun-05 Geometric Software Head Engineering PAUL DEBJYOTI 47 President - IT Services 3548173 2534109 PGDM 22 30-Dec-19 Microsoft Architect Manager GHOSH TAPAS 58 Vice President - IT Services 3178032 2490124 M.TECH. 33 1-Jul-01 ITC Ltd., Head Corporate IT Purchase Committee VAKKALAGADDA SRIDHAR ## 43 Senior Project Manager 2560373 1569320 M.C.A 16 2-Jan-20 Tata Consultancy Services Ltd., Program Manager SHANKARAN SUNDARESH 50 President - IT Services 2475704 1850790 B.E. 29 6-Jan-20 Infosys Vice President SRINATH SUDARSHAN 55 Vice President - IT Services 2250677 1783235 M.S. 29 7-Feb-17 ANTZ MCS Private Limited Director & Partner CHAUDHARY ROHIT 35 Account Manager 1962759 1570257 PGDM 11 23-Jan-14 Infinite Computer Solutions Team Lead RAJAGOPALAN SUSHMA 56 - 1703375 1313236 M.B.A. -

NN Group's Exclusion List

NN Group’s Exclusion List Companies Country 22nd Century Group Inc United States _ Adani Enterprises Limited India _ Adani Ports and Special Economic Zone Limited India _ Aerojet Rocketdyne Holdings Inc. United States _ Agritrade Resources Limited Hong Kong _ Alliance Resource Partners LP United States _ Altius Minerals Corp Canada _ Altria Group, Inc. United States _ Anhui GreatWall Military Ltd. China _ Arch Coal Inc United States _ Aryt Industries, Ltd. Israel _ Ashot Ashkelon Israel _ Athabasca Oil Corporation Canada _ AviChina Industry & Technology Company Limited China _ BAE Systems Plc United Kingdom _ Banpu Public Company Limited Thailand _ Bharat Dynamics Limited India _ British American Tobacco (Malaysia) Berhad Malaysia _ British American Tobacco Plc.1 United Kingdom _ Canadian Natural Resources Limited Canada _ Cenovus Energy Inc. Canada _ Ceylon Tobacco Company Plc. Sri Lanka _ China Coal Energy Company Limited China _ China National Nuclear Power Co., Ltd. China _ China Shenhua Energy Co Ltd China _ China Shipbuilding Industry Company Limited China _ China Spacesat China _ Cloud Peak Energy Inc. United States _ CNNC International, Ltd. China _ Coal India Limited India _ Controversial Tobacco Oil sands production and Thermal coal Violations of international weapons and/or production controversial pipelines mining standards of business arms trade conduct Companies Country Concern PVO Almaz-Antey OJSC Russia _ Connacher Oil & Gas Ltd Canada _ CONSOL Energy Inc. United States _ Datong Coal Industry Co Ltd China _ Deep Well Oil & Gas, Inc Canada _ DMCI Holdings, Inc. Philippines _ Eastern Co SAE Egypt _ Elbit Systems Ltd. -

Aditya Birla Management Corporation Ltd. Airtel Amicorp Andhra Bank

Aditya Birla Management Corporation Ltd. Airtel Amicorp Andhra Bank Apollo Munich Health Insurance Co. Ltd. Arvind Ltd. Ashok Leyland Ltd Asian Paints Aviva Life Insurance AXA Business Services Axis Bank B C Management Services Pvt. Ltd. Bank of America BANK OF BARODA Bank of India Bank of Ireland Bank Of Maharashtra Bharat petroleum Corporation Ltd BHEL Binani Industries Broadridge Financial Solutions India Cairn Energy India Pty Ltd Canara HSBC OBC Life Insurance Capgemini Consulting India Pvt Ltd Carrefour WC & C India Pvt Ltd CEAT Coal India Limited Colgate Palmolive India Corporation Bank Cosmos Bank DCM Shriram Consolidated Ltd Department of Income Tax Diageo DMA Yellow Works Ltd Dr Reddys Lab DTDC Courier & Cargo Ltd Ericsson Telecom Escorts Limited Essar Enenrgy Fidelity Business Services India FLUXONIX CORPORATION PVT LTD Ford Motor Company FRanklin Templeton International Services India Franklin Templeton Intl Srvs (I) Pvt Ltd GAIL GalxoSmithKline Pharmaceuticals Ltd. GENERAL ELECTRIC APPLIANCES & LIGHTING GENERAL MILLS COMPANY Godrej Consumer Products Ltd. Government of Kerala Grupo HDI HCL HDFC LTD Hero MotoCorp Ltd. Hewlett Packard India Sales Pvt Ltd Hindustan Petroleum Corporation Ltd Hindusthan National Glass & Industiries Ltd ICICI Lombard general Insurance ICICI Prudential Life Insurance IDBI Bank Limited Idea Cellular Limited India First Life Insurance Indian Oil Corporation Ltd Indian Overseas Bank IndusInd Bank Ltd INTERGLOBE ENTERPRISES LTD IREO ITC Limited JBM Group Jewelex India Pvt. Ltd. JM financial JSW Steel Jubilant Life Sciences Ltd. Karur Vyasa Kotak Mahindra Bank Ltd KPMG India Liberty Videocon General Insurance Lupin Ltd Mahindra & Mahindra Mahindra Finance Mahindra Group Mahindra Logistics Ltd C/o Mahindra&Mahindra Marico Ltd Maruti Suzuki India Limited Max Life Insurance Co. -

Annual Report 2016

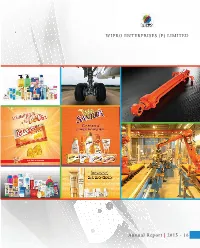

WIPRO ENTERPRISES (P) LIMITED “C” Block, CCLG Division, Doddakannelli, Sarjapur Road, Bangalore - 560 035, India. Ph: +91-80-28440011 Fax: +91-80-28440054 CIN No.: U15141KA2010PTC054808 email: [email protected] Website: www.wiproel.com Annual Report | 2015 - 16 21600795_Wipro Enterprises AR 2016_Cover.indd 1 6/30/2016 8:15:36 PM Inside Corporate Information About Wipro Infrastructure Engineering i BOARD OF DIRECTORS CEO – WCCLG AND EXECUTIVE REGISTRAR AND SHARE TRANSFER DIRECTOR AGENTS Azim H. Premji – Chairman About Wipro Consumer Care and Lighting ii Vineet Agrawal Karvy Computershare Private Ltd. Suresh C. Senapaty CEO – WIN AND EXECUTIVE Directors Report 01 REGISTERED OFFICE ADDRESS OF DIRECTOR WIPRO ENTERPRISES (P) LIMITED Vineet Agrawal Pratik Kumar Standalone Financial Statements 29 “C” Block, CCLG Division, Doddakannelli, Pratik Kumar CHIEF FINANCIAL OFFICER Sarjapur Road, Bangalore - 560 035, India. Consolidated Financial Statements 63 Raghavendran Swaminathan Rishad Premji Ph: +91-80-28440011 COMPANY SECRETARY Fax: +91-80-28440054 Chethan CIN No.: U15141KA2010PTC054808 STATUTORY AUDITORS email: [email protected] About Wipro Enterprises (P) Limited BSR & Co. LLP. Chartered Accountants Website: www.wiproel.com Wipro Enterprises (P) Limited comprises of two main businesses namely Wipro Consumer Care and Lighting, primarily into Personal Care products, Lighting solutions & Office furniture and Wipro Infrastructure Engineering, which provides Hydraulic Solutions for a wide range of diverse applications including Aerospace & Defense, complete end to end solutions in Water and Wastewater treatment for industrial applications and 3D Printing solutions. Wipro Consumer Care and Lighting (WCCLG), a part of Wipro Enterprises (P) Ltd, is among the fastest growing FMCG businesses in India. Wipro Consumer Care’s businesses include Personal wash products, toiletries, personal care products, baby care products, wellness products, electrical wire devices, Domestic and Commercial lighting and Modular office furniture.