Download (Pdf)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 1980

Annual Report 1980 The Depository• Trust Company The ability of Depository Trust to conduct its activities rests largely on modern computer technology, reflecting a long chain of developments in several disciplines. Automated calculating and recordkeeping are the essence of DTC's book-entry capability. Telecommunications devices facilitate the flow of information among Participants, transfer agents, and others throughout the financial community. The ability to utilize minute intervals of time permits computers to operate in billionths of a second. The illustrations in this report depict historical developments in each of these disciplines. The graphic theme and appearance of this Annual Report were conceived by David S. Jobrack, Executive Assistant to the Chairman, who also acted as Creative Director throughout the production process, and wrote, edited and/or compiled the text, illustrations and captions. 1980 Annual Report Highlights. 2 Computer Communications A Message from Management. ..... 3 Facility (CCF) . 28 History, Ownership and Policies. ....... 4 Other Automation Developments .... 28 Growth in 1980 .... 6 Interfaces in a National Clearance and Settlement System .. ....... 30 Eligible Issues. .8 Municipal Bond Program ..... 8 Protection for Participants' Securities ..... 32 Outlook for Institutional Use. 10 Officers and Directors of The Institutional Delivery (ID) Depository Trust Company.. 38 System. 14 1980 in Retrospect . .40 Basic Services 16 Financial Statements. ............ 46 Fast Automated Securities Participants. 54 Transfer (FAST) .' 17 Stockholders. ........ 56 Ancillary Services. 20 Depository Facilities ... 56 ...... 20 Dividends Pledgees .............. 57 Voting Rights. 21 Banks Reported to be Participating in Other Ancillary Services. 22 the Depository on an Indirect Basis 57 The Automation of Depository Services. 26 Investment Companies Reported Participant Terminal System (PTS). -

Bank Holding Companies • June 1970

June 1970 A 94 BANK HOLDING COMPANIES • JUNE 1970 BANK HOLDING COMPANIES, DECEMBER 31y 1969 (Registered pursuant to Section 5, Bank Holding Company Act of 1956) Location of Holding company principal office Holding company Montana Western Bancorporation Great Falls... Bancorporation of Montana Central Banking System, Inc. New Hampshire Nashua New Hampshire Bankshares, Inc. Colorado CNB Bankshares, Inc. Denver U. S. Bancorporation, Inc. New Mexico The First National Bancorporation, Inc. Alamogordo.. Bank Securities, Inc. (NSL) First Colorado Bankshares, Inc. New York District of Columbia Buffalo Marine Midland Banks, Inc. Washington Financial General Bankshares, Inc.1 New York The Bank of New York Company, Inc. New York Bankers Trust New York Corporation New York Charter New York Corporation United Bancshares of Florida, Inc. New York Empire Shares Corporation Atlantic Bancorporation New York The Morris Plan Corporation The Atlantic National Bank of Jacksonville Rochester.... Lincoln First Banks Inc. Barnett Banks of Florida, Inc. Rochester.... Security New York State Corporation Charter Bankshares Corporation Warsaw Financial Institutions, Inc. Trustees, Estate of Alfred I. duPont Warsaw Geneva Shareholders, Inc. Central Bancorp, Inc. 2 Commercial Bancorp, Inc. Ohio Pan American Bancshares, Inc.2 Cincinnati.. .. The Central Bancorporation, Inc. Southeast Bancorporation, Inc. Cleveland.... Society Corporation First at Orlando Corporation Columbus.... American Bancorporation Exchange Bancorporation, Inc. Columbus.... BancOhio Corporation First Financial Corporation Columbus First Banc Group of Ohio, Inc. First Florida Bancorporation Columbus.... Huntington Bancshares Incorporated The First National Bank of Tampa Union Security & Investment Co. South Dakota Aberdeen Dacotah Bank Holding Co. Trust Company of Georgia Tennessee Trust Company of Georgia Associates Chattanooga.. Hamilton National Associates, Incorporated Citizens and Southern Holding Company Johnson City. -

US Accounts in 24 Hours

U.S. Accounts In 24 Hours - eBook Thank you for purchasing our featured "U.S. Accounts In 24 Hours" eBook / Online Information Packet offered at our web site, U.S. Account Setup.com Within our featured online information packet, you will find all of the resources, tools, information, and contacts you'll need to quickly & easily open a NON-U.S. Resident Bank Account within 24 hours. You'll find lists of U.S. Banks, Account Application Forms, Information on how to obtain a U.S. Mailing Address, plus so much more. Just point and click your way through our Online Information Packet using the links above. If you should have any questions or experience any difficulties in opening your Non-U.S. Resident Account, please feel free to email us at any time, and one of our representatives will get back with you promptly. For Support, Email: [email protected] Homepage: www.usaccountsetup.com Application Forms UPDATE - E-TRADE'S NEW ACCOUNT OPENING POLICIES Etrade is changed the rules in which they open International Banking/ Brokerage accounts for foreigners. They now require all new applications be submitted to the local branch office in your region. Once account is opened, you will be able to use it as a U.S. Bank/Brokerage Account out of your home country. Below, you will find a list of International Etrade Phone Numbers & Addresses. Contact the etrade office that best reflects where you reside or would like your account based out of and where you would like to receive your debit card. U.S. -

1985 0101 NSCCAR.Pdf

National Securities Clearing Corporation Corporate Office 55 Water Street New York, New York 10041 (212) 510-0400 Boston One Boston Place Boston, Massachusetts 02108 Chicago 135 South LaSalle Street Chicago, Illinois 60603 Cleveland 900 Euclid Avenue Cleveland, Ohio 44101 Dallas Plaza of the Americas TCBTower Dallas, Texas 75201 Denver Dominion Plaza Table of Contents 600 17th Street Denver, Colorado 80202 To NSCC Participants 2 Detroit NSCC Board of Directors 4 3153 Penobscot Building Detroit, Michigan 48226 NSCC Officers 8 Jersey City Introduction 9 One Exchange Place Jersey City, New Jersey 07302 The Year in Review 10 Los Angeles Municipal Bond Program 12 615 South Flower Street Los Angeles, California 9001.7 Fund/SERV 14 Milwaukee Automated Customer Account Transfer Service 16 777 East Wisconsin Avenue Milwaukee, Wisconsin 53202 International Securities Clearing Corporation 18 Minneapolis Audited Financial Statements 20 IDS Center 80 South 8th Street Participating Organizations 26 Minneapolis, Minnesota 55402 New York 55 Water Street New York, New York 10041 St. Louis One Mercantile Tower Cover: 1985 was a year during which NSCC anticipated and St. Louis, Missouri 63101 responded to the expanding needs of the financial services San Francisco industry ... 50 California Street • As marketplace self-regulatory organizations, represented San Francisco, California 94111 here by a New York Stock Exchange Guide/Constitution Toronto and Rules, proposed new rules on broker-dealers' transfer Two First Canadian Place of client accounts, NSCC implemented the Automated Toronto, Ontario, Canada M5X lA9 Customer Account Transfer Service. • While continuing to serve its traditional equity, corporate bond and municipal bond marketplaces, represented by volume charts on the computer screen, NSCC expanded its comparison services to include municipal bond syndi cates, when-issued and extended-settlement trades. -

School of Economics & Business Administration Master of Science in Management “MERGERS and ACQUISITIONS in the GREEK BANKI

School of Economics & Business Administration Master of Science in Management “MERGERS AND ACQUISITIONS IN THE GREEK BANKING SECTOR.” Panolis Dimitrios 1102100134 Teti Kondyliana Iliana 1102100002 30th September 2010 Acknowledgements We would like to thank our families for their continuous economic and psychological support and our colleagues in EFG Eurobank Ergasias Bank and Marfin Egnatia Bank for their noteworthy contribution to our research. Last but not least, we would like to thank our academic advisor Dr. Lida Kyrgidou, for her significant assistance and contribution. Panolis Dimitrios Teti Kondyliana Iliana ii Abstract M&As is a phenomenon that first appeared in the beginning of the 20th century, increased during the first decade of the 21st century and is expected to expand in the foreseeable future. The current global crisis is one of the most determining factors affecting M&As‟ expansion. The scope of this dissertation is to examine the M&As that occurred in the Greek banking context, focusing primarily on the managerial dimension associated with the phenomenon, taking employees‟ perspective with regard to M&As into consideration. Two of the largest banks in Greece, EFG EUROBANK ERGASIAS and MARFIN EGNATIA BANK, which have both experienced M&As, serve as the platform for the current study. Our results generate important theoretical and managerial implications and contribute to the applicability of the phenomenon, while providing insight with regard to M&As‟ future within the next years. Keywords: Mergers &Acquisitions, Greek banking sector iii Contents 1. Introduction ................................................................................................................ 1 2. Literature Review .......................................................................................................... 4 2.1 Streams of Research in M&As ................................................................................ 4 2.1.1 The Effect of M&As on banks‟ performance .................................................. -

Staff Study 174

Board of Governors of the Federal Reserve System Staff Study 174 Bank Mergers and Banking Structure in the United States, 1980–98 Stephen A. Rhoades August 2000 The following list includes all the staff studies published 171. The Cost of Bank Regulation: A Review of the Evidence, since November 1995. Single copies are available free of by Gregory Elliehausen. April 1998. 35 pp. charge from Publications Services, Board of Governors of 172. Using Subordinated Debt as an Instrument of Market the Federal Reserve System, Washington, DC 20551. To be Discipline, by Federal Reserve System Study Group on added to the mailing list or to obtain a list of earlier staff Subordinated Notes and Debentures. December 1999. studies, please contact Publications Services. 69 pp. 168. The Economics of the Private Equity Market, by 173. Improving Public Disclosure in Banking, by Federal George W. Fenn, Nellie Liang, and Stephen Prowse. Reserve System Study Group on Disclosure. November 1995. 69 pp. March 2000. 35 pp. 169. Bank Mergers and Industrywide Structure, 1980–94, 174. Bank Mergers and Banking Structure in the United States, by Stephen A. Rhoades. January 1996. 29 pp. 1980–98, by Stephen A. Rhoades. August 2000. 33 pp. 170. The Cost of Implementing Consumer Financial Regula- tions: An Analysis of Experience with the Truth in Savings Act, by Gregory Elliehausen and Barbara R. Lowrey. December 1997. 17 pp. The staff members of the Board of Governors of the The following paper is summarized in the Bulletin Federal Reserve System and of the Federal Reserve Banks for September 2000. The analyses and conclusions set forth undertake studies that cover a wide range of economic and are those of the author and do not necessarily indicate financial subjects. -

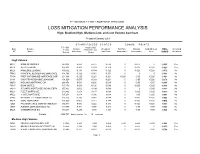

LOSS MITIGATION PERFORMANCE ANALYSIS High, Medium-High, Medium-Low, and Low Volume Servicers

FY 2000 SINGLE FAMILY MORTGAGE SERVICING LOSS MITIGATION PERFORMANCE ANALYSIS High, Medium-High, Medium-Low, and Low Volume Servicers Prepared January 2001 S T A N D A R D I Z E D S C O R E S B O N U S P O I N T S FY 1999 Actual Loss/ Svcr Servicer Loans Default Potential Loss Weighted FirstTime Minority UnderServed FINAL Increased ID * Name Scored Rate Score Score Total Score Homeowner Homeowner Area SCORE Incentives High Volume MUL1 BANK OF AMERICA 240,318 0.059 -0.727 -0.530 0 -0.025 0 -0.555 Yes MUL6 WELLS FARGO 656,303 -0.005 -0.503 -0.379 0 -0.025 -0.025 -0.429 Yes MUL5 HOMESIDE LENDING 439,502 -0.136 -0.384 -0.322 0 -0.025 -0.025 -0.372 No 75640 PRINCIPAL RESIDENTIAL MORTGAGE 191,398 -0.122 -0.361 -0.301 0 0 0 -0.301 No 77396 FIRST NATIONWIDE MORTGAGE COR 211,449 -0.125 -0.227 -0.201 -0.025 -0.05 -0.025 -0.301 No 64141 COUNTRYWIDE HOME LOANS INC 491,029 -0.075 -0.243 -0.201 0 -0.05 -0.025 -0.276 No 39276 MIDLAND MORTGAGE CO 266,458 0.521 -0.286 -0.085 0 -0.05 -0.05 -0.185 No 73815 BANK UNITED 117,179 0.039 -0.120 -0.080 0 -0.025 -0.025 -0.130 No 68013 ATLANTIC MORTGAGE AND INVESTM 155,832 -0.032 -0.104 -0.086 0 0 -0.025 -0.111 No MUL3 FLEET MORTGAGE 319,862 -0.258 0.137 0.038 0 -0.025 -0.025 -0.012 No MUL2 CHASE MORTGAGE 597,276 -0.018 0.096 0.068 0 -0.05 -0.025 -0.007 No 38092 NATIONAL CITY MORTGAGE CO 105,256 -0.236 0.142 0.048 0 -0.025 -0.025 -0.002 No MUL4 GMAC MORTGAGE 136,099 -0.057 0.211 0.144 0 -0.025 -0.025 0.094 No 12621 PNC MORTGAGE CORP OF AMERICA 102,937 0.082 0.222 0.187 0 -0.025 -0.025 0.137 No 10757 AURORA LOAN -

Rank Total Assets Bank Name 1 $2138002000000

Rank Total Assets Bank Name 1 $2,138,002,000,000 JPMorgan Chase Bank 2 $1,749,176,000,000 Wells Fargo Bank 3 $1,707,215,000,000 Bank of America 4 $1,369,304,000,000 Citibank 5 $442,985,106,000 U.S. Bank 6 $360,348,645,000 PNC Bank 7 $282,071,109,000 Capital One 8 $274,106,659,000 TD Bank 9 $260,306,000,000 The Bank of New York Mellon 10 $233,542,890,000 State Street Bank and Trust Company 11 $214,562,871,000 Branch Banking and Trust Company 12 $201,282,949,000 SunTrust Bank 13 $200,405,288,000 HSBC Bank USA 14 $180,506,000,000 Charles Schwab Bank 15 $156,156,000,000 Goldman Sachs Bank USA 16 $137,903,926,000 Fifth Third Bank 17 $132,807,446,000 Chase Bank USA 18 $132,288,338,000 KeyBank 19 $127,377,000,000 Morgan Stanley Bank 20 $123,636,430,000 Regions Bank 21 $122,682,502,000 Manufacturers and Traders Trust Company 22 $122,313,000,000 Ally Bank 23 $121,086,840,000 The Northern Trust Company 24 $118,240,305,000 Citizens Bank 25 $116,115,695,000 MUFG Union Bank 26 $105,873,901,000 Capital One Bank (USA) 27 $105,498,391,000 BMO Harris Bank 28 $99,868,655,000 The Huntington National Bank 29 $93,651,365,000 Discover Bank 30 $83,988,195,000 Compass Bank 31 $83,695,723,000 Bank of the West 32 $81,283,142,000 USAA Federal Savings Bank 33 $80,375,731,000 Santander Bank, N.A. -

Download (Pdf)

THIS COMPILATION IS DERIVED LARGELY FROM SECONDARY SOURCES. NOT AN OFFICIAL REPORT OF CHANGES IN THE BANKING STRUCTURE.' NOT FOR PUBLICATION BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM L. 4.5 October 22, 1962 CHANGES IN STATUS OF BANKS AND BRANCHES DURING SEPTEMBER 1962 Class Date of MAP ? ae and location of banks and branches of bank change New Banks (Except successions and conversions) First State Bank Lake Village, Ark. Ins. non. 9-19-62 Chicot County First National Bank Fresno, Calif. National 9-14-62 Fresno County- Colfax National Bank Denver, Colo. National 9-24-62 Denver County Republic National Bank Pueblo, Colo. National 9- 4-62 Pueblo County Bank of Commerce Fort Lauderdale, Fla. Ins. non. 9-11-62 Broward County First National Bank of North Broward County- Lighthouse Point, Fla. National 9- 4-62 Broward County Trail National Bank P. 0. Sarasota, Fla. National 9-26-62 Manatee County Hampshire National Bank South Hadley, Mass. National 9- 4-62 Hampshire County Troy National Bank Troy, Mich. National 9-20-62 Oakland County Grant Square Bank & Trust Co. Oklahoma City, Okla. Ins. non. 9-24-62 Oklahoma County First National Bank Owasso, Okla. National 9- 8-62 Tulsa County Bassett National Bank El Paso, Tex. National 9-27-62 El Paso County Coronado State Bank El Paso, Tex. Ins. non. 9- 4-62 El Paso County Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis Class Date of Name and location of banks and "branches of bank change New Banks (Cont'd) ' (Except successions and conversions) Wolfforth State Bank Wolfforth, Tex. -

Mergers of National Banks, Or National and State Banks, by States

1970 TABLEB-17 Mergers* of National banks, or National and State banks, by States, calendar 1970 Effective Merging banks Outstanding Undivided date Resulting bank capital Surplus profits and Total assets stock reserves Total: 60 merger actions CALIFORNIA Apr. 10 Los Padres National Bank, Santa Maria (15271) $500,000 $375,000 $356,628 $12,438,566 Wells Fargo Bank, National Association, San Fran- cisco (15660) 91,757,810 185,242,820 56,400,610 5,436,787,409 Wells Fargo Bank, National Association, San Fran- cisco (15660) 92,257,810 185,542,420 56,757,238 5,449,225,975 June 11 Gateway National Bank, El Segundo (15239) 1,595,226 1,126,314 265,311 31,745,184 Southern California First National Bank, San Diego (3050) 7,062,495 13,285,305 12,044,200 601,086,646 Southern California First National Bank, San Diego (3050) 7,062,495 13,285,305 15,031,052 632,831,830 July 31 Bank of Sacramento, Sacramento 2,262,750 2,447,250 127,667 42,497,359 Security Pacific National Bank, Los Angeles (2491). 168,000,000 182,000,000 122,362,960 6,722,389,757 Security Pacific National Bank, Los Angeles (2491). 170,262,750 189,737,250 116,522,457 6,758,034,271 Nov. 6 The First National Bank of Holtville, Holtville (9770). 400,000 400,000 179,980 13,927,142 Wells Fargo Bank, National Association, San Fran- cisco (15660) 92,419,970 185,455,260 65,490,961 5,514,746,846 Wells Fargo Bank, National Association, San Fran- cisco (15660) 92,859,970 185,815,260 65,670,942 5,527,924,917 CONNECTICUT Apr. -

169 Bank Mergers and Industrywide Structure, 1980–94

169 Bank Mergers and Industrywide Structure, 1980–94 Stephen A. Rhoades Staff, Board of Governors The staff members of the Board of Governors of The following paper, is summarized in the the Federal Reserve System and of the Federal Bulletin for February 1996. The analyses and Reserve Banks undertake studies that cover a conclusions set forth are those of the author and wide range of economic and financial subjects. do not necessarily indicate concurrence by the From time to time the studies that are of general Board of Governors, the Federal Reserve Banks, interest are published in the Staff Studies series or members of their staffs. and summarized in the Federal Reserve Bulletin. Board of Governors of the Federal Reserve System Washington, DC 20551 January 1996 Bank Mergers and Industrywide Structure, 1980–94 The period from 1980 to 1994 was one of record Background merger activity for banks. Indeed, this period was marked not only by a record number of bank As the data in this paper will show, during the mergers but also by a remarkable number of very 1980s merger activity reached record levels in the large mergers including several that surpassed the banking sector as it did in the industrial sector. size of all past bank mergers. These mergers For at least three reasons, the activity in banking played a major role in the beginning of what appears to be not just a temporary response to portends to be a long-term restructuring of the more cautious antitrust enforcement and general banking industry. economic conditions of the 1980s but a tendency This paper presents data on all bank mergers that is likely to persist and to result in a restructur- for the period, including the number, sizes, ing of the industry.2 locations, and types for more than 6,300 bank First, the removal of the legal restraints on mergers and the identification of the largest geographic expansion by banks, both within and mergers. -

1977 Ail.Il.1.L.Al Report

1977 AIl.Il.1.l.al Report The Depository Trust C01npany Summary of Depository Services The Depository Trust Company performs Custody three major functions: it is a custodian for DTC holds deposited securities in clJstody the securities of its Participants, a channel and records each Participant's position on for communications between Participants its books in any eligible security issue. and between Participants and the transfer agents of their securities, and an account Dividend and ing system for the book-entry delivery .~nd Interest pledge among its Participants of secuntles Payments immobilized in its custody. The nature of its DTC passes on to Participants cash and major services is indicated below. stock dividends distributions and interest Deposits related to securities held in custody. DTC accepts deposits of securities certifi Voting Rights cates from or for its Participants at its office DTC facilitates the voting of deposited se or at cObperating Depository Facilities curities by assigning the voting rights in across the country. equity issues to the appropriate Partici pant. Confirmations Withdrawals and Acknowledgments By Transfer DTC provides users the ability to confirm DTC arranges for the transfer and delivery securities trades and to acknowledge those to Participants of securities registered in confirmations, whether or not the transac the name of any person, reducing Partici tions are in DTC-eligible security issues. pants' pOSitions accordingly. Deliveries Urgent and Settlement Withdrawals DTC makes book-entry deliveries of depos DTC provides for withdrawals by Partici ited securities between Participants and pants of certificates on demand (CODs) between a Participant, clearing corpora within approximately three hours.