House Prices and Turnover in Amsterdam, 1582-1810∗

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

De Drooglegging Van Amsterdam

DE DROOGLEGGING VAN AMSTERDAM Een onderzoek naar gedempt stadswater Jeanine van Rooijen, stageverslag 16 mei 1995. 1 INLEIDING 4 HOOFDSTUK 1: DE ROL VAN HET WATER IN AMSTERDAM 6 -Ontstaan van Amsterdam in het waterrijke Amstelland 6 -De rol en ontwikkeling van stadswater in de Middeleeuwen 6 -op weg naar de 16e eeuw 6 -stadsuitbreiding in de 16e eeuw 7 -De rol en ontwikkeling van stadswater in de 17e en 18e eeuw 8 -stadsuitbreiding in de 17e eeuw 8 -waterhuishouding en vervuiling 9 HOOFDSTUK 2: DE TIJD VAN HET DEMPEN 10 -De 19e en begin 20e eeuw 10 -context 10 -gezondheidsredenen 11 -verkeerstechnische redenen 12 -Het dempen nader bekeken 13 HOOFDSTUK 3: ENKELE SPECIFIEKE CASES 15 -Dempingen in de Jordaan in de 19e eeuw 15 -Spraakmakende dempingen in de historische binnenstad in de 19e eeuw 18 -De bouw van het Centraal Station op drie eilanden en de aanplempingen 26 van het Damrak -De Reguliersgracht 28 -Het Rokin en de Vijzelgracht 29 -Het plan Kaasjager 33 HOOFDSTUK 4: DE HUIDIGE SITUATIE 36 BESLUIT 38 BRONVERMELDING 38 BIJLAGE: -Overzicht van verdwenen stadswater 45 2 Stageverslag Geografie van Stad en Platteland Stageverlener: Dhr. M. Stokroos Gemeentelijk Bureau Monumentenzorg Amsterdam Keizersgracht 12 Amsterdam Cursusjaar 1994/1995 Voortgezet Doctoraal V3.13 Amsterdam, 16 mei 1995 DE DROOGLEGGING VAN AMSTERDAM een onderzoek naar gedempt stadswater Janine van Rooijen Driehoekstraat 22hs 1015 GL Amsterdam 020-(4203882)/6811874 Coll.krt.nr: 9019944 3 In de hier voor U liggende tekst staat het eeuwenoude thema 'water in Amsterdam' centraal. De stad heeft haar oorsprong, opkomst, ontplooiing, haar specifieke vorm en schoonheid, zelfs haar naam te danken aan een constante samenspraak met het water. -

Amsterdam Web.Indd

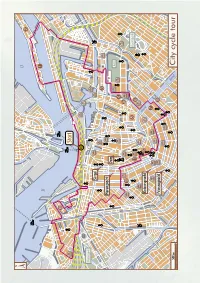

17 km City cycle tour 10.5 miles This tour will show you many of the different faces of Amsterdam. Of course you’ll see its historic centre with the famous canals where dur- ing the 17th century rich merchants built their stately homes. Next you’ll cycle through the Jordaan district, which used to be a working-class area in the early 17th century. Nowa- days it’s a pleasant neighbourhood with narrow streets and many little shops and pubs, an area which is greatly favoured by youngsters and yuppies. In the Jordaan you may want to visit some almshouses, dat- ing right back to the 17th century. In the Plantage district you’ll find the splendid urban villa’s of the ear- ly 19th century. And in the Spaar- dammer neighbourhood you‘ll see some beautiful examples of wor- king class apartment-buildings, de- signed by architects of the Amster- dam School in the early years of the 20th century. This architectural style made use of rounded shapes and brick ornaments to decorate the buildings. The buildings in the Spaarndammer- buurt are among the most important examples of the Amsterdam School. Last but not least you may be surprised by very modern houses on the banks of the River IJ, built in the late 20th century. Not only old warehouses have been con- verted into modern apartments, brand new residential areas have been built there as well, designed with a variety of architecture. On many occasions you may observe how modern buildings fit very well within the existing architecture. -

Het Verkeer Verdeelt De Stad Tot Op Het Bot Ruimte, Doorstroming En Verbinden, Het Klinkt Goed Als Uitgangspunt Voor De Mo- Biliteit in De Drukte Van Amsterdam

Berichten uit de Westelijke Binnenstad Uitgave van De beleving van een kind A. van Wees distilleerderij De Ooievaar Dit blad biedt naast buurtinformatie Wijkcentrum Jordaan & Gouden Reael waarbij saamhorigheidsgevoel en begrip zich Op de uiterste noordwestpunt van de Jordaan, een platform waarop lezers hun visie op actuele jaargang 13 nummer 3 begon te ontwikkelen. De winnende staat al bijna 100 jaar A. van Wees distilleer- zaken kenbaar kunnen maken. Lees ook onze juni t/m augustus 2015 inzending van de verhalenwedstrijd derij De Ooievaar; de laatste ambachtelijke Webkrant: www.amsterdamwebkrant.nl de Jordaan door Henk de Hoogd Pagina 3 distilleerderij van Amsterdam Pagina 5 Haarlemmerbuurt Het verkeer verdeelt de stad tot op het bot Ruimte, doorstroming en verbinden, het klinkt goed als uitgangspunt voor de mo- biliteit in de drukte van Amsterdam. Maar schijn bedriegt: het verkeer verdeelt de stad tot op het bot. Een verkeersluwere Haarlemmerbuurt is goed voor de handel, zegt wethouder Pieter Litjens (VVD) die lof en kritiek oogstte. ‘Niet waar, dat kost omzet’, klinkt het uit de hoek van de Haarlemmerbuurtondernemers. T MI Amsterdam is gebouwd voor paard en wagen winkelstraatmanager Nel de Jager. Auto’s S en niet voor de 400.000 autobewegingen, en fietsers zijn nodig voor de klandizie. ‘De AN K J I 350.000 OV-reizigers en 1,1 miljoen fietsbe- Haarlemmerdijk is een boodschappenstraat. R wegingen, daarom wil Pieter Litjens wat aan Het is geen toeristengebied, zoals de Negen END het verkeer in de stad doen, zei hij half mei in Straatjes. Daar loop je alle straatjes door. De H O de Posthoornkerk aan de Haarlemmerstraat. -

Openbaar Vervoer Op Dit Station Tram Metro Bestemmingen Vanaf Dit Station

Openbaar vervoer op dit station Public transport at this station Rokin Tram 4 Centraal Station 4 Station RAI 14 Centraal Station N 14 Flevopark 24 Centraal Station 24 VU medisch centrum Metro M52 Noord M52 Zuid M52 Noord M52 Zuid 1 4 Station RAI 14 Flevopark 24 VU medisch centrum 4 Centraal Station M52 Noord 14 Centraal Station M52 Zuid 24 Centraal Station 1 u staat hier you are here Bestemmingen vanaf dit station Destinations near this station lopen walk adres 1 Allard Pierson 2 min. Oude Turfmarkt 127 – 129 Lift naar metro 1 Elevator to metro 13 min. Prinsengracht 263-267 2 Anne Frank Huis RKN-02-A 3 Amsterdam Museum 2 min. Kalverstraat 92 e 5 min. Singel d Bloemenmarkt a Da Costabuurt B Anjeliersbuurt Haarlemmerbuurt 4 k l Anjeliersbuurt R o Westelijke ta o em s Groenmarktkadebuurt ze s o Noord n tr Bloemgrachtbuurt Noord West C g a Zuid L L r a eilanden a a a ac t D u u t ri r R ht 2 cht W 6 min. Dam a er ie o Korte Prinsengra a g r ze e Da Costabuurt s t 5 Dam Ja tr ra tr n a W s co s c a str t b x h a a e e i t t a s r r v n a t Haarlemmerbuurt W d a Zuid r L t t s e o n i e j L n n r k n N e b d s Ma e nn aa t e o s p e a W n e n s Oost k t l p d s a ht i s e e 10 min. -

Herengracht 1015 BR AMSTERDAM H02025

Herengracht 1015 BR AMSTERDAM H02025 Asking price Euro 2975.00 Herengracht H02025 This fantastic fully furnished bright 1 (could be made 2) bedroom apartment is situated on the 3rd and 4th floor of a traditional building on the fabulous Herengracht. 3rd floor: The bright living room is situated at the front of the apartment overlooking the Herengracht canal and has a large open hearth and original oak beams. The floor covering is a beautiful high quality wood and gives it a real classic feel. The large open kitchen has built-in all desired appliances for modern living. Through the back of the 3rd floor you enter the large roof terrace perfect for cocktails or just basking in the sunlight. 4th floor: The whole 4th floor is 1 large bedroom with an all-white luxurious floor covering. This etage has a very ambient feel which combines the classic and the modern. This huge space can be divided to create a second bedroom. Due to the quality of this apartment and the desirability of the location we dont think this will be on the market very long so hurry if you want to make an appointment for a viewing. Location: Central and Jordaan Forming a horseshoe around the Old Centre, the Canal Ring is made up of the city’s original moat, the Singel, and the Herengracht, Keizersgracht and Prinsengracht. It begins its loop west of Centraal Station along Brouwersgracht, until it meets the River Amstel. In a way, the Canal Ring forms a crossover from the more bustling Centre to the gentler outer neighbourhoods of Jordaan, Museum District, Plantage and De Pijp. -

De Herengracht En Keizersgracht in 1768 En Nu

AmsterdamseGrachtenhuizen.info de Herengracht en Keizersgracht in 1768 en nu Ter herinnering aan Janna Vera Dijk © 2017 Erwin Meijers fotografie en eo Bakker tekst en opmaak Alle rechten voorbehouden Uitgegeven door: AmsterdamseGrachtenhuizen.info Druk en bindwerk: Pumbo - Zwaag Lettertype: Garamond, een lettertype dat vernoemd is naar de Franse stempelsnijder Claude Garamond (ca. 1480-1561) ISBN: 978-94-92733-00-9 NUR: 680 website: amsterdamsegrachtenhuizen.info Behoudens de in of krachtens de Auteurswet van 1912 gestelde uitzonderingen mag niets uit deze uitgave worden verveelvoudigd, opgeslagen in een geautomatiseerd gegevensbestand, of openbaar gemaakt, in enige vorm of op enige wijze, hetzij elektronisch, mechanisch, door fotokopieën, opnamen of enige andere manier, zonder voorafgaande schriftelijke toestemming van de uitgever. www.amsh.nl/H 2 3 Inhoud 5 Inhoudsopgave 89 Herengracht 474-488, tekeningen 1700 en 1767 474 - 488 7 Voorwoord 90 Nieuwe Spiegelstraat – Vijzelstraat 466 - 482 9 De site, het boek en de QR codes 92 Vijzelstraat – Reguliersgracht 498 - 532 11 Eerste en tweede uitleg 95 Tekeningen Herengracht 502 502 15 Derde en vierde uitleg 96 Reguliersgracht – Utrechtsestraat 534 - 558 19 Caspar Jacobsz Philips 98 Utrechtsestraat – Amstel 560 - 600 21 Uitgiftekaarten 101 Panorama’s Keizersgracht Huisnummers 23 Panorama’s Herengracht Huisnummers 102 Brouwersgracht – Herenstraat 1 - 95a 24 Brouwersgracht – Roomolenstraat 1 - 33 106 Herenstraat – Leliegracht 95b - 157 26 Roomolenstraat – Korsjespoortsteeg 33 - 77 110 Leliegracht -

Nummer Toegang: LEYP Ley, P. (Paul) De / Archief

Nummer Toegang: LEYP Ley, P. (Paul) de / Archief Het Nieuwe Instituut (c) 2000 This finding aid is written in Dutch. 2 Ley, P. (Paul) de / Archief LEYP LEYP Ley, P. (Paul) de / Archief 3 INHOUDSOPGAVE BESCHRIJVING VAN HET ARCHIEF......................................................................5 Aanwijzingen voor de gebruiker.......................................................................6 Citeerinstructie............................................................................................6 Openbaarheidsbeperkingen.........................................................................6 Archiefvorming.................................................................................................7 Geschiedenis van de archiefvormer.............................................................7 Ley, Paul de..............................................................................................7 Bronnen.........................................................................................................11 BESCHRIJVING VAN DE SERIES EN ARCHIEFBESTANDDELEN........................................19 LEYP.110492531 Opleiding; 1964-1973 Opleiding Academie van Bouwkunst Amsterdam en diverse stages.......................................................................19 LEYP.110492532 Onderwijsactiviteit..............................................................21 LEYP.110492533 Beroepspraktijk...................................................................22 LEYP.110492534 Documentatie.....................................................................36 -

Ontdek Amsterdam

ONTDEK | DISCOVER AMSTERDAM BIJ | AT GRAND HOTEL AMRÂTH AMSTERDAM Welkom in Amsterdam! Welcome to Amsterdam! Behoeft deze stad nog enige introductie? Met musea van Does this city need any introduction? With world-class museums, wereldklasse, tal van karakteristieke straatjes, theater, numerous characteristic streets, theater, live music, cozy bars livemuziek, relaxte bars en heerlijke restaurants is er altijd and delicious restaurants, there is always something to do and wat te doen en beleven in Amsterdam! Dwaal over de grachten experience in Amsterdam! Meander through the canals with met haar smalle gevelhuizen of ontdek de stad per boot of its narrow canal houses or discover the city by boat or bicycle; fiets; er is zoveel te zien! Cultuurliefhebbers halen hun hart op there is so much to see! Culture lovers can enjoy themselves in in het Museumkwartier met het Van Gogh, Rijks- en Stedelijk the Museum Quarter with the Van Gogh, Rijks- and Municipal Museum als grote trekpleisters. Shop naar hartenlust in de vele Museum as major attractions. Shop till you drop in the many authentieke boetiekjes of internationale brand stores. Maar authentic boutiques or international brand stores. A visit to ook voor de kinderen is een bezoek aan Amsterdam zeker de Amsterdam is also definitely worthwhile for children with moeite waard met attracties als Madame Tussaud, NEMO of attractions such as Madame Tussaud, NEMO Science Museum or Artis. Kortom genoeg redenen voor een bezoek aan de meest Artis Zoo. In short, enough reasons to visit the most versatile city veelzijdige stad van ons land, wij maken u graag wegwijs! in our country, we are happy and proud to show you around! Graagbij Amrâth tot Hôtels ziens! Pleaseat Amrâthbe Hôtelswelcome! EG G ORAW F IJD AWE K FL LO O D OR R M K FL A AW OR N A L N I O A K M T EG E N P A LA U E R L P A W R Z O I A BINNEN- N E I ZE G M E R H M G N E R ST E E W O F Buikslotermeer IJ A HOF D M R K E W P O M O N M A G A E O W K O A R W E O RN E S A N SJ L L STR. -

Historische Straatnamen Amsterdam

HISTORISCHE STRAATNAMEN AMSTERDAM Enkele opmerkingen In de lijst zijn verschillende spellingsvarianten opgenomen; noteert u voor het project ‘Ja, ik wil!’ s.v.p. de spelling zoals die in de akte vermeld is! Straatnamen beginnend met 1e, 2e, etc. > zie Eerste, Tweede, etc. Straatnamen zijn alfabetisch gerangschikt, inclusief voorvoegsel: Nieuwe Looierstraat vindt u dus onder de N van Nieuwe Voor de ligging van de straten en hun huidige namen: zie http://www.islandsofmeaning. -

De Vierde Uitleg Van Amsterdam Van 1662

De vierde uitleg van Amsterdam van 1662 Stedenbouwkundige ontwikkeling en verkaveling Anouk Rosenhart (3238121) Onderzoekswerkgroep II: architectuurgeschiedenis ‘Huizen in Nederland’ Dr. Paul Rosenberg 2 juli 2010 Inhoud 1. Inleiding p. 2 2. Historisch kader p. 3 3. De verkaveling p. 7 - De indeling en afmetingen van de percelen per woonblok p. 7 - De verkoop van de percelen p. 9 - De bebouwing van de percelen p. 9 - De prijzen van de percelen p. 10 4. Huistypen p. 12 5. Conclusie p. 14 6. Literatuurlijst p. 16 7. Noten p. 17 8. Bijlagen Inleiding In 1662 was het ontwerp klaar voor de vierde uitleg van Amsterdam; vanaf het einde van de derde uitleg uit 1613, ter hoogte van de huidige Leidsegracht, werden de grachten doorgetrokken. Bij deze stadsuitbreiding ging het stadsbestuur uit van een doordacht ontwerp en men had geleerd van de fouten die waren ontstaan tijdens de derde uitleg, zodat men deze keer systematischer en pragmatischer te werk wilde gaan. Het stadsbestuur liet het stratenplan en de verkaveling ontwerpen door de stadsarchitect. Hoe zag dit ontwerp eruit en hoe kwam de verkaveling tot stand? Welke keuzes zijn er gemaakt met betrekking tot de verdeling van de percelen per woonblok, de bouwvoorschriften en de verkoop van de percelen? Kortom: hoe verliep de stedenbouwkundige ontwikkeling en het bouwproces vanaf het idee van een nieuwe stadsuitbreiding tot de uiteindelijke bebouwing van de percelen? De bestaande literatuur geeft een inzicht in de stedenbouwkundige ontwikkeling van de vierde uitleg met de motieven van de stadsuitbreiding, de aanleg, het ontwerp, de verkaveling, de bebouwing en de bouwvoorschriften. -

Binnenk®Ant 41

JAARGANG 9 NUMMER 41 LENTE 2008 De BINNENK ANT Onafhankelijke uitgave van en voor de bewoners van de binnenstadsbuurten: Groot Waterloo Amstelveld Leidse / Wetering Buurt 6 De redactie vroeg om een kort verhaal over het Huis van de Buurt. Wat is dat, wat gaat er gebeuren? Op dit moment valt daar wel in algemene termen iets over te zeggen, maar nog niet heel concreet. Ik zal dat proberen uit te leggen, ook al had ik liever een meer concreet verhaal geschreven. HUIS VAN DE BUURT Het wijkcentrum d’Oude Stadt wordt niet helemaal zelf kunnen redden, of ook vanuit één locatie te gaan doen. een van de dragers van het nieuwe met die hulp sterker worden. In het Of misschien vanuit meer locaties, Huis van de Buurt. In het Huis van Huis van de Buurt komt iedereen bij maar dan wel samen vanuit elk van de Buurt gaan de welzijnsinstellingen elkaar: bewoners die zelf acties or- die locaties. Wat is anders een Huis voor de bewoners van de binnenstad ganiseren en bewoners die hulp nodig van de Buurt? Het moet meer zijn samenwerken. hebben. Die bewoners en activiteiten dan een nieuw bord op de gevel en Figuurlijk, door in samenwerking hun kunnen elkaar versterken. een mooi logo. Maar het probleem is diensten aan te bieden en in principe dat iedere verhuisbeweging in de bin- ook letterlijk, door vanuit één locatie Wat gaat er nu concreet gebeuren en nenstad heel snel tot hogere huren kan te gaan werken. Er komen drie van die veranderen? Want samenwerken en leiden. Voor d’Oude Stadt is een be- Huizen in de binnenstad. -

Brochure Schatkamer

DeThe Schatkamer Amsterdam vanTreasure Amsterdam Room The city’s history in twenty-four striking stories and photographs Voorwoord De geschiedenis van Amsterdam is een schatkamer vol verhalen en bijzondere documenten. Het Stadsarchief Amsterdam beheert meer dan 50 kilometer aan historische archieven met oude boeken en papieren, foto’s, kaarten, tekeningen en prenten, die zorgvuldig worden bewaard in onze depots. Het archief verwelkomt iedereen om in het monumentale gebouw De Bazel de rijke geschiedenis van de stad te ontdekken. Dwaal door de Schatkamer, gebouwd in 1926. Bekijk een historisch film in de gezellige filmzaal. Ontmoet Rembrandt, Johan Cruyff en hun tijd. Bewonder de middeleeuwse charterkast. En beleef de verandering van een kleine stad in de middeleeuwen tot een wereldstad in de 21ste eeuw. Bert de Vries Directeur Schatkamer Stadsarchief Amsterdam 06 05 04 B 03 02 01 08 09 10 -1 C 11 A 12 E 06 F D 05 0 -2 04 03 H 02 G 08 01 09 10 I -2 11 I 12 J I K A D L 0 -2 4 Vitrines -1 Vitrines -2 Fotografen zien de De geschiedenis van de stad geschiedenis van de stad in twaalf verhalen 07 01 De eerste foto’s van 01 Het ontstaan van 08 Amsterdam Amsterdam 02 Jacob Olie 02 Bidden en vechten 03 Jacob Olie 03 Wederdopers Immigranten 04 George Hendrik Breitner 04 in de Gouden Eeuw 05 Bernard F. Eilers 05 Amsterdam en slavernij 06 Fotostudio Merkelbach 06 Vondelingen 07 Frits J. Rotgans 07 Natura Artis Magistra 08 Wim van der Linden 08 Wereldtentoonstelling 1883 09 Publieke Werken 09 Februaristaking 10 Cor jaring 10 Van Provo’s tot krakers 11 Archieffotografen 11 Geef mij maar Amsterdam 12 Stichting IJbeeld 12 Naar buiten 07 A Ingang Schatkamer E Zichtdepot 08 B Ingang Filmzaal F Beeld van Mercurius C Toiletten G Middeleeuwse Charterkast D Lift (tussen 0 en -2) H Tijdelijke presentaties I Kofferkluizen J Weeskamerladen K Zichtdepot L Voormalige Stookruimte 5 6 Fotografen zien de geschiedenis van de stad Vitrines 1 De eerste foto’s van Amsterdam 7 Frits J.