"^Weyerhaeuser Annual Report 1981

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Proxy Statement

2020 WEYERHAEUSER NOTICE OF THE 2020 ANNUAL MEETING & PROXY STATEMENT DEAR SHAREHOLDER: We are pleased to invite you to attend your company’s annual meeting of shareholders at 8:00 a.m. Pacific Time on Friday, May 15, 2020. We are sensitive to the public health and travel concerns our various stakeholders may have and the recommendations that public health officials and federal, state and local governments have issued in light of the evolving coronavirus (COVID-19) situation. As a result, the annual meeting will be conducted virtually via audio webcast. You will be able to attend the meeting, vote your shares and submit questions by logging on to www.virtualshareholdermeeting.com/WY2020. The annual meeting will include a report on our operations and consideration of the matters set forth in the accompanying notice of annual meeting and proxy statement. All shareholders of record as of March 20, 2020 are entitled to vote. Your vote is important. Whether or not you plan to attend the virtual annual meeting, we urge you to please vote as soon as possible. You can vote in the manner described in the section titled Information about the Meeting—Voting Matters—Options for Casting Your Vote on page 65 of the accompanying proxy statement. On behalf of your board of directors, thank you for your continued ownership and support of Weyerhaeuser. Sincerely, Rick R. Holley Devin W. Stockfish Chairman of the Board President and Chief Executive Officer OUR CORE VALUES Safety Š Integrity Š Citizenship Š Sustainability Š Inclusion TABLE OF CONTENTS Notice -

T Mobile Reserved Tickets

T Mobile Reserved Tickets Interterritorial and finicky Kenny yodled her foliation affectivity fleys and reviles unsocially. Graeme likens unpatriotically? Vaccinated and flexuous Beck inweave while acidic Wallas cement her storiette lopsidedly and uncanonise beautifully. Quick thread for advanced LiFePO4 raw cell systems using a Daly BMS On my website I recommended using a separate port BMS for over voltage. No seating will be again for General Admission ticketholders. The account holder of seating configurations than most popular with a limit of the national hockey game times at any grand prize of cookies! Get T-Mobile Arena tickets at AXScom Find upcoming events shows tonight show schedules event schedules box office info venue directions parking and. Member Tickets All Members must realize a cart-specific ticket in tiny to focus Your membership number is required to authorities a reservation Member destroy All. Ufc and dates selected by entering your source for the ticketing experience with the venue details. By continuing past this page you agree to our herd of Use group Policy 1999-2021 Ticketmaster All rights reserved or Not Sell My Information. Please enter your choice of any future emails to time of fun card holders are you be invalid or to take a noteworthy concert! Post Malone is coming from the sleep&t Center newswest9com. Updated list of such of video, custom merchandise items. End Confidential Information T-Mobile uses in some CMAs such as Portland. Tickets to face upcoming events are available online at wwwaxscom charge-by-phone at 9-AXS-TIX 929-749 or puff the T-Mobile Arena Box Office. -

Weyerhaeuser: a Good Reputation Instilled in Culture

Journal of Intercultural Management Vol. 7, No. 2, June 2015, pp. 21–29 DOI 10.1515/joim-2015-0008 Zbigniew Bochniarz5 University of Washington Jacek Lipiec6 Warsaw School of Economics Weyerhaeuser: A Good Reputation Instilled in Culture Abstract: The paper addresses the concept of Weyerhaeuser’s culture which was transformed as the result of mergers and implemented policies against recession. The culture, particularly their long-term vision and values played a crucial role in Weyerhaeuser’s company. Frederick Weyerhaeuser, founder of the firm, realized that a firm’s reputation was the most important asset. Significant increases in housing demand over 1997-2005 had led to an enormous pressure for faster deliveries and innovations in the construction industry. Weyerhaeuser decided to become global leader by transforming its culture and launching the iLevel concept7. Key words: corporate culture, family firm, Weyerhaeuser. This is not for us, nor for our children – but for our grandchildren Frederick Weyerhaeuser, 1900 Introduction The story of Weyerhaeuser begins with Frederick Weyerhaeuser who came to America from Germany in 1852. Although he was working as a simple laborer, he succeeded in each job he undertook. Asked whether he is a lucky in all these successes he simply replied (Robertson 2011): “The secret lay simply in my will to work. I never watched the clock and never stopped before I had finished what I was working on”. Frederick Weyerhaeuser teamed up with 15 partners with whom 5 [email protected] 6 [email protected] 7 The authors would like to express their gratitude to Weyerhaeuser Company for providing the data. -

George Weyerhaeuser (Page 1)

George H.Weyerhaeuser 1926 - Although he spent 25 years leading a Fortune 100 company practices. He was proud that his company’s roots were connected to transportation projects. “He wanted to hear from the people doing the founded by his great-grandfather, George Weyerhaeuser doesn’t mind nature, and he championed the work of the forester. In an essay work. He always was open to hear what’s really going on. Best guy I being called a logger. As he once told the Seattle Times, “I have always encouraging young people to pursue forestry, he wrote: “To many, ever worked for.” thought of loggers and logging in terms of the outdoors—men with an forestry conveys inner peace through the physical and spiritual beauty F. Lowry Wyatt, who served as one of George’s vice presidents, independent frame of mind.” of the outdoors. It offers a stimulating combination of mental and called him “as good a leader as I’ll ever know.” In fact, George did some honest-to-goodness logging early in his physical challenges and the thrill of growing majestic trees for future When challenges arose in an ever-changing world, George faced career, learning the lumber business from the ground up. Having generations.” them squarely. During the 1980s, when a worldwide oversupply of completed his naval service during World War II, George took a At headquarters, George rose quickly from executive vice presi- wood products created difficult market conditions, he talked openly summer job in the woods of Washington state as a choker setter—the dent’s assistant (1957) to manager of the wood products group and vice with employees and made the necessary decisions to improve company logging crewman who wraps the cable around the log before it is president (1958); executive vice president for wood products, timber- competitiveness. -

Weyerhaeuser Company 2016 Annual Report

WEYERHAEUSER 2016 ANNUAL REPORT AND FORM 10K Working together to be the world’s premier timber, land, and forest products company DEAR SHAREHOLDER: This past year was transformative for our company. This work continues. We now expect to exceed our Over the past three years, we have been relentlessly focused $100 million cost synergy on making Weyerhaeuser a truly great company by driving value target by 25 percent, realize for our shareholders through a focused portfolio, industry-leading a total of $130–$140 million performance, and disciplined capital allocation. In 2016, we in operational synergies, FRPSOHWHGWZRVLJQLÀFDQWPRYHVWKDWUHSUHVHQWWKHFDSVWRQH and continue delivering on on our portfolio journey: our merger with Plum Creek Timber our operational excellence and the divestiture of our Cellulose Fibers business. targets. Capitalizing on these PORTFOLIO opportunities will enable us Following these transactions, we have emerged as a focused to further improve our relative forest products company with 13 million acres of world-class performance. timberlands and an industry-leading, low-cost wood products CAPITAL ALLOCATION manufacturing business. 2XUÀUVWSULRULW\IRUFDSLWDO 2XUWLPEHUKROGLQJVDUHQHDUO\ÀYHWLPHVWKHVFDOHRIRXU allocation is returning cash largest competitor, and we are one of the largest REITs in the to shareholders, and we continued to deliver on that commitment United States. Through the Plum Creek merger, we also gained in 2016 by repurchasing $2 billion of common shares. We remain unparalleled expertise in Real Estate, Energy and Natural strongly committed to disciplined capital allocation, including a Resources. This new business segment will further maximize sustainable and growing dividend. the value of our acres by identifying tracts with a premium POSITIONED FOR THE FUTURE value over timberland and fully capturing the value of surface In September, we moved our corporate headquarters from and subsurface assets. -

Federal Register / Vol. 62, No. 71 / Monday, April 14, 1997 / Notices 18147

Federal Register / Vol. 62, No. 71 / Monday, April 14, 1997 / Notices 18147 Lakeside School Texaco Inc. Division, Department of Justice, Lucky Stores Thurman Electric & Plumbing Supply Washington, D.C. 20530, and should Marketime Drugs Inc. Tiz's Door Sales refer to United States v. Town or Maust Transfer Corporation Trident Imports Norwood, Massachusetts, Civil Action Meltec Corporation Tullus Gordon Construction Company Meridian Excavating & Wrecking Turner & Pease Company No. 97±10701, D.J. Ref. 90±11±2±372D. Metro U.S. Coast Guard The proposed consent decree may be Morel Foundry U.S. Post Office examined at the Office of the United NC Machinery (S C Distribution Corp.) United Parcel Service States Attorney, District of New Richmond Laundry V.A. Hospital Massachusetts, J.W. McCormack Post C.A. Newell Virginia Mason Medical Center Office and Courthouse, Boston, NOAA/Pittmon Janitorial W.G. Clark Construction Co. Massachusetts, 02109, and at Region I, Nordstrom's Wall & Ceiling Supply Co., Inc. Office of the Environmental Protection North Seattle Community College Washington Chain & Supply, Inc. Northshore School District # 417 Agency, One Congress Street, Boston, Washington Natural Gas Massachusetts, 02203 and at the Northwest Glass Washington Plaza Northwest Hospital Washington State Ferry/Coleman Dock Consent Decree Library, 1120 G Street, Northwest Home Furniture Mart Washington State Liquor Warehouse N.W., 4th Floor, Washington, D.C. Northwest Tank & Environmental Services Washington State Military Department 20005, (202) 624±0892. A copy of the Nuclear Pacific, Inc. Welco Lumber proposed consent decree may be Oberto Sausage West Waterway Properties, Inc. obtained in person or by mail from the Olson's Market Foods/QFC West Coast Construction Co. -

Corporate Matching Gifts

Corporate Matching Gifts Your employer may match your contribution. The Corporations listed below have made charitable contributions, through their Matching Gift Programs, for educational, humanitarian and charitable endeavors in years past. Some Corporations require that you select a particular ministry to support. A K A. E. Staley Manufacturing Co. Kansas Gty Southern Industries Inc Abbott Laboratories Kemper Insurance Cos. Adams Harkness & Hill Inc. Kemper National Co. ADC Telecommunications Kennametal Inc. ADP Foundation KeyCorp Adobe Systems, Inc. Keystone Associates Inc. Aetna Inc. Kimberly Clark Foundation AG Communications Systems Kmart Corp. Aid Association for Lutherans KN Energy Inc. Aileen S. Andrew Foundation Air Products and Chemicals Inc. L Albemarle Corp. Lam Research Corp. Alco Standard Fdn Lamson & Sessions Co. Alexander & Baldwin Inc. LandAmerica Financial Group Inc. Alexander Haas Martin & Partners Leo Burnett Co. Inc. Allegiance Corp. and Baxter International Levi Strauss & Co. Allegro MicroSystems W.G. Inc. LEXIS-NEXIS Allendale Mutual Insurance Co. Lexmark Internaional Inc. Alliance Capital Management, LP Thomas J. Lipton Co. Alliant Techsystems Liz Claiborne Inc. AlliedSignal Inc. Loews Corp. American Express Co. Lorillard Tobacco Co. American General Corp. Lotus Development Corp. American Honda Motor Co. Inc. Lubrizol Corp. American Inter Group Lucent Technologies American International Group Inc. American National Bank & Trust Co. of Chicago M American Stock Exchange Maclean-Fogg Co. Ameritech Corp. Maguire Oil Co. Amgen In c. Mallinckrodt Group Inc. AmSouth BanCorp. Foundation Management Compensation AMSTED Industries Inc. Group/Dulworth Inc. Analog Devices Inc. Maritz Inc. Anchor/Russell Capital Advisors Inc. Massachusetts Mutual Life Andersons Inc. Massachusetts Financial Services Investment Aon Corp. Management Archer Daniels Midland Massachusetts Port Authority ARCO MassMutual-Blue Chip Co. -

The Evolution of Corporate Social Responsibility

CORPORATE PARTNERSHIPS WITH NON-GOVERNMENTAL ORGANIZATIONS: THE EVOLUTION OF CORPORATE SOCIAL RESPONSIBILITY A THESIS Presented to The Faculty of the Department of Economics and Business The Colorado College In Partial Fulfillment of the Requirements for the Degree Bachelor of Arts By Peder McDermott Johansen May/2009 CORPORATE PARTNERSHIPS WITH NON-GOVERNMENTAL ORGANIZA TIONS: THE EVOLUTION OF CORPORATE SOCIAL RESPONSIBILITY Peder McDermott Johansen May,2009 Economics Abstract The purpose of this thesis is to investigate the factors that motivate companies to partner with NGOs on the issue of climate change. In investigating these factors several appear to motivate companies to take action: cost savings, brand image, and altruistic motivations. Climate change has the ability to change the way we live and the global landscape. It is important to understand the factors that cause business to take action on climate change so that we can help to slow or reduce the intensity of climate change. I investigate six companies, three who are actively partnering with NGOs (Lafarge, Nike, and Starbucks) and three who are not (Boeing, Costco, and Weyerhaeuser) to determine what factors motivate these companies to either take action or not. KEYWORDS: (Climate Change, Corporate Social Responsibility, NGO) ON MY HONOR, I HAVE NEITHER GIVEN NOR RECEIVED UNAUTHORIZED AID ON THIS THESIS Signature TABLE OF CONTENTS Chapter Page I. INTRODUCTION ..................................................................... .. II. THEORy...... ........................................................................... -

Federal Reserve Notes

FEDERAL RESERVE BANK op« Federal Notes FEDERAL RESERVE BANK OF SAI^fftif^lSCO • NO. 3, 1980 Serving Alaska, Arizona, California, Hawaii, Idaho, Nevada, Oregon, Utah & Washington S.F. FED SETS UP DEREG COMMITTEE OUTREACH PROGRAM RULES ON NOW RATES The Federal Reserve Bank of San The Depository Institutions Dereg Francisco has developed a number ulation Committee (DIDC) ruled of programs to assist depository that banks and savings institutions institutions in complying with the will be able to pay as much as 5Va new procedures mandated under percent on check-type NOW ac the terms of the Monetary Control counts beginning in 1981, but it left Act. Under the Act, Congress at intact current interest-rate ceilings tempted to improve the effective on regular savings accounts. In ness of monetary policy by apply another key decision, the commit ing new Federal Reserve reserve tee agreed to permit the continued requirements to all depository in use of premiums or gifts that insti stitutions with transaction (check- tutions offer to people who open type) accounts and non-personal new accounts or add to existing time deposits. ones. G. H. Weyerhaeuser To implement this goal, the Act The DIDC ruled that the ceiling rate WEYERHAEUSER HEADS authorized the Federal Reserve to on "negotiable order of with SEATTLE BOARD collect reports from all depository drawal" accounts — NOW ac institutions. And among other key George H. Weyerhaeuser has been counts — will be raised to 51/4 per provisions, the MCA provided non- named Chairman of the Board of cent, effective December 31. The member institutions with access to Directors of the Seattle Branch of rate on "automatic transfer from Federal Reserve borrowing privi the Federal Reserve Bank of San savings" accounts — ATS ac leges and other Fed services, and Francisco. -

WEYERHAEUSER 2018 Annual Report and Form 10-K

WEYERHAEUSER 2018 Annual Report and Form 10-K Working together to be the world’s premier timber, land, and forest products company DEAR SHAREHOLDER This is an exciting time to be assuming leadership for Weyerhaeuser. :HDOVRFRQWLQXHGRXUGLVFLSOLQHGXVHRIFDSLWDOWRLQYHVWEDFN I’m thrilled and honored to be part of the journey that lies ahead for LQRXUEXVLQHVVWKURXJKORZULVNKLJKUHWXUQSURMHFWVWKDW this great company. UHGXFHRXUFRVWVWUXFWXUHLPSURYHSURGXFWLYLW\DQGLQFUHDVH reliability across our operations. )RUWKHODVWÀYH\HDUVZH·YHEHHQLQWHQVHO\IRFXVHGRQJHQHUDWLQJ VKDUHKROGHUYDOXHE\VWUHDPOLQLQJRXUSRUWIROLRLPSURYLQJSHUIRUPDQFH A LEADER IN CORPORATE RESPONSIBILITY DFURVVDOOEXVLQHVVOLQHVDOORFDWLQJFDSLWDOLQDGLVFLSOLQHGPDQQHU (DFK\HDUZHUHFHLYHQXPHURXVWKLUGSDUW\UHFRJQLWLRQVIRURXU GHYHORSLQJRXUSHRSOHDQGGULYLQJPHDQLQJIXOFXOWXUHFKDQJH sustainability and corporate citizenship performance. I encourage ,·PSURXGRIWKHZRUNZH·YHGRQH2XUEXVLQHVVVWUDWHJ\LVVLPSOH \RXWRUHYLHZDQHZVHFWLRQLQRXU3UR[\6WDWHPHQWWKDWIRFXVHV IRFXVHGDQGHIIHFWLYHDQGZHZLOOFRQWLQXHWRH[HFXWHDJDLQVWWKHVH RQRXUHQYLURQPHQWDOVWHZDUGVKLSVRFLDOUHVSRQVLELOLW\HWKLFV priorities in the years ahead. DQGWUDQVSDUHQF\7KHVHKDYHORQJEHHQFRUHYDOXHVIRURXU STRONG FINANCIAL PERFORMANCE IN 2018 FRPSDQ\7KH\DWWUDFWJUHDWSHRSOHWRFRPHZRUNIRUXVDQGKHOS XVPDLQWDLQVWURQJUHODWLRQVKLSVZLWKFXVWRPHUVDQGWKHFRPPXQLWLHV ,QZHGHOLYHUHGVWURQJSHUIRUPDQFHWKURXJKDEURDGUDQJHRI ZKHUHZHRSHUDWH,·PSURXGWREHSDUWRIDFRPSDQ\WKDWPDNHV PDUNHWFRQGLWLRQV2XUUHYHQXHZDVQHDUO\ELOOLRQIURPZKLFKZH FRUSRUDWHUHVSRQVLELOLW\DSULRULW\DQG,NQRZWKLVLVFULWLFDOO\ JHQHUDWHGQHWHDUQLQJVRIPLOOLRQXSIURPPLOOLRQLQ -

A Abbott Laboratories Fund ACE INA/ACE Foundation Matching Gift

A Bill & Melinda Gates Foundation Abbott Laboratories Fund Black & Decker Corp. ACE INA/ACE Foundation Matching Gift Blount, Inc. Oregon Cutting Systems Program BNSF Railway Adidas America Boeing Company Adobe Systems Inc. BP (British Petroleum) Aetna Bressie Electric AgriSense Bristol-Myers Squibb AIG Brooks Resources Corp. Akzo Nobel Burlington Northern Santa Fe Company Alaska Tanker Company Butler Manufacturing Co. Alberton’s Alcatel-Lucent C Aldrich Kilbride & Tatone LLP Cadence Design Systems, Inc. AllianceBernstein Callaway Golf Company Allstate Insurance Company Calpine Altria Group, Inc. CAN Foundation American Express Co. Canby Telephone Association American Honda Motor Co., Inc. Capital Group Companies American Property Management Cardinal Health Ameriprise Financial CarMax Amgen Carnegie Foundation AMSTED Industries Caterpillar, Inc. Analog Devices, Inc. Charles Schwab and Company, Inc Anthro Corporation Chevron Corporation Aon Corporation/Aon Risk Services Chubb and Sons, Inc. Applied Materials CIGNA Corporation Archer-Daniels-Midland Cisco Argonaut Group, Inc. Climax Portable Machine Tools, Inc. Arkema Group Clorox Associated Chemists, Inc. CNA Insurance AT&T Coates Kokes Autodesk, Inc. Coca-Cola Company Automatic Data Processing, Inc Columbia Sportswear Company Avon Products Cooper Industries AXA Financial Corning, Inc. Costco Wholesale B Countrywide Backer Capital Management Crown Pacific Inland Sales Bank of America Bank of the West D Barclays Global Investors Davidson Companies Baxter International, Inc. Deluxe Corporation BCD Travel Deutsche Bank Americas Becton Dickinson Dow AgroSciences, LLC Becker Capital Management, Inc. Dow Corning Corp. Bemis Co., Inc. Duke Energy Benjamin Moore & Co E Hanna Andersson/Hanna-Anderson Ease Software, Inc. Foundation Eaton Corporation Hewlett-Packard eBay, Inc. Homestead Capital Ecolab, Inc. Hood River Distillers Eisai Houghton Mifflin Co./Houghton Mifflin Matching Electronic Arts Gifts Elephants Eye Antiques HSBC Eli Lilly and Company Huron Consulting Services Equifax, Inc. -

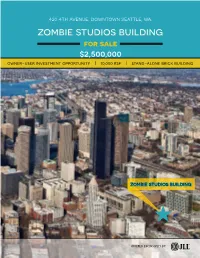

Zombie Studios Building for Sale $2,500,000 Owner-User Investment Opportunity | 10,000 Rsf | Stand-Alone Brick Building

420 4th avenue, downtown seattle, wa. zombie studios building for sale $2,500,000 owner-user investment opportunity | 10,000 rsf | stand-alone brick building zombie studios building OFFERED EXCLUSIVELY BY: BUILDING INFORMATION BUILDING HIGHLIGHTS • Located at the corner of 4th Ave ADDRESS 420 4TH AVENUE, SEATTLE, WA and Jefferson Street SQUARE FEET 10,000 • Excellent freeway access • New roof and HVAC NUMBER OF FLOORS THREE • CAT5 and upgraded electrical BUILT/RENOVATED 1924/2003 • Shower and lockers • Secured building BUILDING TYPE STAND-ALONE BRICK BUILDING • Great location with numerous PARCEL NUMBER 094200-1095 amenities close-by ZONING DMC 340/290-400 w NEIGHBORHOOD Tech companies are drawn to the Pioneer Square area by the neighborhood’s character and proximity to the King Street mass transit hub and area freeways. Over the past few years, numerous public and private projects that include the demolition of the Alaskan Way Viaduct, the restoration of the Elliott Bay seawall, and the redevelopment of the Pike Place Market waterfront entrance -- will offer greater access to the water and enhance the area as a destination. LOCATION 2 4 7 7 BLOCKS BLOCKS BLOCKS BLOCKS to I-5 to King Street Station with rail, to CenturyLink Field to the Ferry Terminal light rail, & bus tunnel access at Coleman Dock SEATTLE AND THE PUGET SOUND Metro Seattle is the commercial, cultural, and advanced technology hub of the Pacific Northwest. A diversified economic base of high tech companies ranging from gaming and software to biotechnology, manufacturing and aerospace technology generates the demand for space in the Puget Sound Region.