WEYERHAEUSER 2018 Annual Report and Form 10-K

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

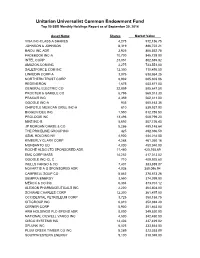

Unitarian Universalist Common Endowment Fund Top 50 SSB Monthly Holdings Report As of September 30, 2014

Unitarian Universalist Common Endowment Fund Top 50 SSB Monthly Holdings Report as of September 30, 2014 Asset Name Shares Market Value VISA INC-CLASS A SHARES 4,275 912,156.75 JOHNSON & JOHNSON 8,319 886,722.21 BAIDU INC ADR 3,925 856,552.75 FACEBOOK INC-A 10,700 845,728.00 INTEL CORP 23,051 802,635.82 AMAZON.COM INC 2,275 733,551.00 SALESFORCE COM INC 12,350 710,495.50 LINKEDIN CORP-A 3,075 638,954.25 NORTHERN TRUST CORP 8,902 605,603.06 REGENERON 1,675 603,871.00 GENERAL ELECTRIC CO 22,859 585,647.58 PROCTER & GAMBLE CO 6,795 569,013.30 PRAXAIR INC 4,359 562,311.00 GOOGLE INC-A 935 550,163.35 CHIPOTLE MEXICAN GRILL INC-A 810 539,937.90 BIOGEN IDEC INC 1,550 512,755.50 PROLOGIS INC 13,496 508,799.20 NIKE INC-B 5,692 507,726.40 JP MORGAN CHASE & CO 8,286 499,148.64 THE PRICELINE GROUP INC 425 492,396.50 ASML HOLDING NV 4,900 484,218.00 KIMBERLY CLARK CORP 4,288 461,260.16 MONSANTO CO 4,000 450,040.00 ROCHE HLDG LTD SPONSORED ADR 11,480 425,168.69 EMC CORP MASS 14,252 417,013.52 GOOGLE INC-CL C 710 409,925.60 WELLS FARGO & CO 7,401 383,889.87 NOVARTIS A G SPONSORED ADR 4,038 380,096.94 CAMPBELL SOUP CO 8,862 378,673.26 SEMPRA ENERGY 3,550 374,099.00 MERCK & CO INC 6,304 373,701.12 ALEXION PHARMACEUTICALS INC 2,200 364,804.00 SCHWAB CHARLES CORP 12,300 361,497.00 OCCIDENTAL PETROLEUM CORP 3,725 358,158.75 CITIGROUP INC 6,810 352,894.20 CERNER CORP 5,900 351,463.00 ARM HOLDINGS PLC-SPONS ADR 8,000 349,520.00 NATIONAL OILWELL VARCO INC 4,500 342,450.00 CISCO SYSTEMS INC 13,406 337,429.02 SPLUNK INC 6,025 333,544.00 PLUM CREEK TIMBER CO INC -

Proxy Statement

2020 WEYERHAEUSER NOTICE OF THE 2020 ANNUAL MEETING & PROXY STATEMENT DEAR SHAREHOLDER: We are pleased to invite you to attend your company’s annual meeting of shareholders at 8:00 a.m. Pacific Time on Friday, May 15, 2020. We are sensitive to the public health and travel concerns our various stakeholders may have and the recommendations that public health officials and federal, state and local governments have issued in light of the evolving coronavirus (COVID-19) situation. As a result, the annual meeting will be conducted virtually via audio webcast. You will be able to attend the meeting, vote your shares and submit questions by logging on to www.virtualshareholdermeeting.com/WY2020. The annual meeting will include a report on our operations and consideration of the matters set forth in the accompanying notice of annual meeting and proxy statement. All shareholders of record as of March 20, 2020 are entitled to vote. Your vote is important. Whether or not you plan to attend the virtual annual meeting, we urge you to please vote as soon as possible. You can vote in the manner described in the section titled Information about the Meeting—Voting Matters—Options for Casting Your Vote on page 65 of the accompanying proxy statement. On behalf of your board of directors, thank you for your continued ownership and support of Weyerhaeuser. Sincerely, Rick R. Holley Devin W. Stockfish Chairman of the Board President and Chief Executive Officer OUR CORE VALUES Safety Š Integrity Š Citizenship Š Sustainability Š Inclusion TABLE OF CONTENTS Notice -

Weyerhaeuser: a Good Reputation Instilled in Culture

Journal of Intercultural Management Vol. 7, No. 2, June 2015, pp. 21–29 DOI 10.1515/joim-2015-0008 Zbigniew Bochniarz5 University of Washington Jacek Lipiec6 Warsaw School of Economics Weyerhaeuser: A Good Reputation Instilled in Culture Abstract: The paper addresses the concept of Weyerhaeuser’s culture which was transformed as the result of mergers and implemented policies against recession. The culture, particularly their long-term vision and values played a crucial role in Weyerhaeuser’s company. Frederick Weyerhaeuser, founder of the firm, realized that a firm’s reputation was the most important asset. Significant increases in housing demand over 1997-2005 had led to an enormous pressure for faster deliveries and innovations in the construction industry. Weyerhaeuser decided to become global leader by transforming its culture and launching the iLevel concept7. Key words: corporate culture, family firm, Weyerhaeuser. This is not for us, nor for our children – but for our grandchildren Frederick Weyerhaeuser, 1900 Introduction The story of Weyerhaeuser begins with Frederick Weyerhaeuser who came to America from Germany in 1852. Although he was working as a simple laborer, he succeeded in each job he undertook. Asked whether he is a lucky in all these successes he simply replied (Robertson 2011): “The secret lay simply in my will to work. I never watched the clock and never stopped before I had finished what I was working on”. Frederick Weyerhaeuser teamed up with 15 partners with whom 5 [email protected] 6 [email protected] 7 The authors would like to express their gratitude to Weyerhaeuser Company for providing the data. -

George Weyerhaeuser (Page 1)

George H.Weyerhaeuser 1926 - Although he spent 25 years leading a Fortune 100 company practices. He was proud that his company’s roots were connected to transportation projects. “He wanted to hear from the people doing the founded by his great-grandfather, George Weyerhaeuser doesn’t mind nature, and he championed the work of the forester. In an essay work. He always was open to hear what’s really going on. Best guy I being called a logger. As he once told the Seattle Times, “I have always encouraging young people to pursue forestry, he wrote: “To many, ever worked for.” thought of loggers and logging in terms of the outdoors—men with an forestry conveys inner peace through the physical and spiritual beauty F. Lowry Wyatt, who served as one of George’s vice presidents, independent frame of mind.” of the outdoors. It offers a stimulating combination of mental and called him “as good a leader as I’ll ever know.” In fact, George did some honest-to-goodness logging early in his physical challenges and the thrill of growing majestic trees for future When challenges arose in an ever-changing world, George faced career, learning the lumber business from the ground up. Having generations.” them squarely. During the 1980s, when a worldwide oversupply of completed his naval service during World War II, George took a At headquarters, George rose quickly from executive vice presi- wood products created difficult market conditions, he talked openly summer job in the woods of Washington state as a choker setter—the dent’s assistant (1957) to manager of the wood products group and vice with employees and made the necessary decisions to improve company logging crewman who wraps the cable around the log before it is president (1958); executive vice president for wood products, timber- competitiveness. -

Weyerhaeuser Company 2016 Annual Report

WEYERHAEUSER 2016 ANNUAL REPORT AND FORM 10K Working together to be the world’s premier timber, land, and forest products company DEAR SHAREHOLDER: This past year was transformative for our company. This work continues. We now expect to exceed our Over the past three years, we have been relentlessly focused $100 million cost synergy on making Weyerhaeuser a truly great company by driving value target by 25 percent, realize for our shareholders through a focused portfolio, industry-leading a total of $130–$140 million performance, and disciplined capital allocation. In 2016, we in operational synergies, FRPSOHWHGWZRVLJQLÀFDQWPRYHVWKDWUHSUHVHQWWKHFDSVWRQH and continue delivering on on our portfolio journey: our merger with Plum Creek Timber our operational excellence and the divestiture of our Cellulose Fibers business. targets. Capitalizing on these PORTFOLIO opportunities will enable us Following these transactions, we have emerged as a focused to further improve our relative forest products company with 13 million acres of world-class performance. timberlands and an industry-leading, low-cost wood products CAPITAL ALLOCATION manufacturing business. 2XUÀUVWSULRULW\IRUFDSLWDO 2XUWLPEHUKROGLQJVDUHQHDUO\ÀYHWLPHVWKHVFDOHRIRXU allocation is returning cash largest competitor, and we are one of the largest REITs in the to shareholders, and we continued to deliver on that commitment United States. Through the Plum Creek merger, we also gained in 2016 by repurchasing $2 billion of common shares. We remain unparalleled expertise in Real Estate, Energy and Natural strongly committed to disciplined capital allocation, including a Resources. This new business segment will further maximize sustainable and growing dividend. the value of our acres by identifying tracts with a premium POSITIONED FOR THE FUTURE value over timberland and fully capturing the value of surface In September, we moved our corporate headquarters from and subsurface assets. -

The Evolution of Corporate Social Responsibility

CORPORATE PARTNERSHIPS WITH NON-GOVERNMENTAL ORGANIZATIONS: THE EVOLUTION OF CORPORATE SOCIAL RESPONSIBILITY A THESIS Presented to The Faculty of the Department of Economics and Business The Colorado College In Partial Fulfillment of the Requirements for the Degree Bachelor of Arts By Peder McDermott Johansen May/2009 CORPORATE PARTNERSHIPS WITH NON-GOVERNMENTAL ORGANIZA TIONS: THE EVOLUTION OF CORPORATE SOCIAL RESPONSIBILITY Peder McDermott Johansen May,2009 Economics Abstract The purpose of this thesis is to investigate the factors that motivate companies to partner with NGOs on the issue of climate change. In investigating these factors several appear to motivate companies to take action: cost savings, brand image, and altruistic motivations. Climate change has the ability to change the way we live and the global landscape. It is important to understand the factors that cause business to take action on climate change so that we can help to slow or reduce the intensity of climate change. I investigate six companies, three who are actively partnering with NGOs (Lafarge, Nike, and Starbucks) and three who are not (Boeing, Costco, and Weyerhaeuser) to determine what factors motivate these companies to either take action or not. KEYWORDS: (Climate Change, Corporate Social Responsibility, NGO) ON MY HONOR, I HAVE NEITHER GIVEN NOR RECEIVED UNAUTHORIZED AID ON THIS THESIS Signature TABLE OF CONTENTS Chapter Page I. INTRODUCTION ..................................................................... .. II. THEORy...... ........................................................................... -

No Point Griping About CEO

What the Boss Makes; Compensation by the Numbers The Seattle Times David Bowermaster July 9, 2006 Pay comes in a variety of packages that may be hard to identify, but the bottom line can still shock investors. The $18.2 million Nike paid William Perez in 2005 made him the highest-paid chief executive in the Northwest last year, according to The Seattle Times' annual calculation of how the region's public companies compensated their leaders. In Perez's case, it would be hard to argue he earned it. During his one-year tenure, Nike's stock price fell by more than $7 per share and The Swoosh lost nearly $2 billion in market value. Nike's board did not demand a refund when it asked the underperforming Perez to leave in January. Just the opposite. On top of his 2005 compensation, Nike gave Perez $8.3 million in severance pay, including $150,000 to cover moving expenses. "The board thought it was a reasonable accommodation to make his transition out of Nike as smooth as possible," said Shannon Shoul, a Nike spokeswoman. In this post-Enron era, such excesses have disturbed investors, who may grouse but have failed at curbing pay packages regardless of performance, and federal regulators, who proposed changes in January so investors can get a clearer picture of what CEOs make. "Over the last decade and a half, the compensation packages awarded to directors and top executives have changed substantially," said Christopher Cox, chairman of the Securities and Exchange Commission. "Our disclosure rules haven't kept pace .. -

The 1995 Plum Creek Lectures Nick Baker, Editor

Maluolm Hunter .' , Hamish Kimmins Nick Baker, lditor ' . Biodiversity: Toward Operational Definitions Hal Salwasser .._ Jack Ward Thomas .._ Alan Randall ~ F. Henry Lickers Malcolm Hunter .._ Hamish Kimmins The 1995 Plum Creek Lectures Nick Baker, Editor School of Forestry The University of Montana-Missoula Au.gust 1997 School of Forestry The University of Montana-Missoula The School of Forestry at The University of Montana-Missoula is a comprehensive natural resource education and research in stitution offering Bachelor's, Master's and Doctoral programs in forest and range re source management, wildlife biology, natu ral resource recreation, and natural resource conservation. The School's Montana Forest and Conservation Experiment Station, insti tutes, and centers administer its research and outreach programs. Comprehensive information about the School and its programs is available at our WEBsite: http://www.forestry.umt.edu © 1997 School of Forestry The University of Montana-Missoula 1/ Partnerships in Forestry Research and Education The University of Montana School of Forestry has developed productive partnerships in research and education with the forestry industry, conservation organizations, and public agencies. This lecture series and the associated Plum Creek Fellowship are the product of such a partnership. The Plum Creek Fellowship The Plum Creek Fellowship provides a 12-month stipend and tuition for a doctoral candidate in the School of Forestry atThe University of Mont.ana -Missoula. A gift from the Plum Creek Timber Company established the UM Foundation endowment which supports the Fellowship. The Fellow assists the Plum Creek Lecture Committee in developing and hosting the Plum Creek Lectures. Plum Creek Timber Company Plum Creek Timber Company, the largest private forest landowner in Montana (1.5 mill ion acres), strives to manage its lands according to environmental principles based on sound sc ience, and to balance economic returns with protection for the environment. -

Federal Reserve Notes

FEDERAL RESERVE BANK op« Federal Notes FEDERAL RESERVE BANK OF SAI^fftif^lSCO • NO. 3, 1980 Serving Alaska, Arizona, California, Hawaii, Idaho, Nevada, Oregon, Utah & Washington S.F. FED SETS UP DEREG COMMITTEE OUTREACH PROGRAM RULES ON NOW RATES The Federal Reserve Bank of San The Depository Institutions Dereg Francisco has developed a number ulation Committee (DIDC) ruled of programs to assist depository that banks and savings institutions institutions in complying with the will be able to pay as much as 5Va new procedures mandated under percent on check-type NOW ac the terms of the Monetary Control counts beginning in 1981, but it left Act. Under the Act, Congress at intact current interest-rate ceilings tempted to improve the effective on regular savings accounts. In ness of monetary policy by apply another key decision, the commit ing new Federal Reserve reserve tee agreed to permit the continued requirements to all depository in use of premiums or gifts that insti stitutions with transaction (check- tutions offer to people who open type) accounts and non-personal new accounts or add to existing time deposits. ones. G. H. Weyerhaeuser To implement this goal, the Act The DIDC ruled that the ceiling rate WEYERHAEUSER HEADS authorized the Federal Reserve to on "negotiable order of with SEATTLE BOARD collect reports from all depository drawal" accounts — NOW ac institutions. And among other key George H. Weyerhaeuser has been counts — will be raised to 51/4 per provisions, the MCA provided non- named Chairman of the Board of cent, effective December 31. The member institutions with access to Directors of the Seattle Branch of rate on "automatic transfer from Federal Reserve borrowing privi the Federal Reserve Bank of San savings" accounts — ATS ac leges and other Fed services, and Francisco. -

Fish Creek State Park Draft Management Plan

FISH CREEK STATE PARK Draft Management Plan DECEMBER 2013 Explore More. Montana State Parks Our Mission is... To preserve and protect our state’s heritage and the natural beauty of our public lands for the benefit of our families, communities, local economies and out-of-state visitors. Our Objectives are... To provide excellent land stewardship, public safety and service through recreation, innovation and education. Our Goals are... To provide an extraordinary experience for our visitors and to keep our state park system strong now and for generations to come. Prepared by Montana State Parks A Division of Montana Fish, Wildlife & Parks 1420 6th East Avenue P.O. Box 200701 Helena, MT 59620-0701 (406) 444-3750 www.stateparks.mt.gov FISH CREEK STATE PARK DRAFT MANAGEMENT PLAN Fish Creek State Park Management Plan Approved Signatures Recommended by: ________________________________ ____________ Chas Van Genderen Date Administrator, Montana State Parks Approved by: ________________________________ ____________ Tom Towe Date Chairman, Montana State Parks & Recreation Board ________________________________ ____________ Jeff Hagener Date Director, Montana Fish, Wildlife & Parks i FISH CREEK STATE PARK DRAFT MANAGEMENT PLAN Acknowledgements Montana State Parks would like to thank the following people for their thoughtful insight and contributions to the Fish Creek State Park Management Plan: Members of the public, neighboring landowners and interested organizations who took time to attend scoping meetings, review the plan and provide constructive -

Matching Gift Programs

Plexus Technology Group,$50 SPX Corp,d,$100 TPG Capital,$100 U.S. Venture,$25 Maximize the Impact of Your Gift Plum Creek Timber Co Inc.,$25 SPX FLOW,d,$100 TSI Solutions,$25 U.S.A. Motor Lines,$1 Pohlad Family Fdn,$25 SSL Space Systems/Loral,$100 Tableau Software,$25 UBM Point72 Asset Mgt, L.P. STARR Companies,$100 Taconic Fdn, Inc.,$25 UBS Investment Bank/Global Asset Mgt,$50 Polk Brothers Fdn Sabre Holdings Campaign (October 2017),$1 Taft Communications,$1 Umpqua Bank,$1 Polycom Inc.,$20 Safety INS Group, Inc.,$250 Takeda Pharma NA,$25 Unilever North America (HQ),s,d Portfolio Recovery Associates,$25 Sage Publications, Inc.,$25 Talent Music,$5 Union Pacific Corp MoneyPLUS,d Match Your Gift PotashCorp,d,$25 Salesforce.com,$50 Tallan Union Pacific Corp TimePLUS,$25 Potenza,$50 Sallie Mae Dollars for Doers,d Talyst,$25 United States Cellular Corp,$25 when you donate to Power Integrations,$25 Saltchuk,$25 Tampa Bay Times Fund,r,$25 United Technologies Corp - UTC,d,$25 Praxair,d,$25 Samaxx,$5 TargetCW,$1 UnitedHealth Group Precor,$25 Samuel Roberts Noble Fdn Inc.,d,$100 Teagle Fdn, Inc.,d UnitedHealth Group (Volunteer) Preferred Personnel Solutions SanMar Technology Sciences Group,$10 Universal Leaf Tobacco Corp,$25 Preformed Line Products Co,r,d,$25 Sandmeyer Steel Co,r,$50 Teichert, Inc. Unum Corp,2:1,d,$50 Premier, Inc.,$50 Sanofi,$50 Teknicks,$1 Premier, Inc. Volunteer,$25 Schneider Electric Co (Cash & Volunteer),d,$25 Tektronix, Inc.,d,$20 Principal Financial Group,r,$50 Scripps Networks Interactive,r,$25 Teleflex,r,d,$50 V/W/X/Y/Z VISA Intl ProLogis,d,$50 Scripps Networks Volunteer,d,$250 Teradata Campaign (October),$25 VMware Inc.,$31 ProQuest LLC,$25 Securian Financial Group,r,d,$35 Terex Corp,$50 Vanderbilt Ventures, Inc. -

Employer Matching Funds Companies

Current Organizations already Associated Chemists, Inc. Cooper Industries participating: AT & T Corning, Inc. IBM Autodesk, Inc. Countrywide Microsoft Automatic Data Processing, Inc. Crown Pacific Inland Sales Morgan Stanley Wealth Management Avon Products Davidson Companies Time Warner AXA Financial Deluxe Corporation Bank of America Deutsche Bank Americas Find your organization here! Bank of Clark County Dow AgroSciences, LLC 3Com Corporation Barclays Global Investors Dow Corning Corp. 3M Baxter International, Inc. Duke Energy Abbott Laboratories Becker Capital Management, Inc. Ease Software, Inc. ACE INA Bemis Co., Inc. Eaton Corporation Adobe Systems Benjamin Moore & Co. Ecolab, Inc. The AES Corporation Black & Decker Corp. Eli Lilly and Company Aetna BNSF Railway Equifax, Inc. AgriSense Boeing Company ExxonMobil Akzo Nobel BP Federated Department Stores, Inc. Alaska Tanker Company Brooks Resources Corp. FIJI Water Aldrich Kilbride & Tatone LLP Butler Manufacturing Co. First Data Corporation Allstate Insurance Company Cadence Design Systems, Inc. First Independent Bank Altria Group, Inc. Calpine FM Global American Express Co. Capital Group Companies FMC Technologies, Inc. American Honda Motor Co., Inc. Cardinal Health Freddie Mac Ameriprise Financial Carnegie Foundation Gannett Company, Inc. AMSTED Industries Caterpillar, Inc. Gap, Inc Analog Devices, Inc. ChevronTexaco Corporation Gartner Group Anthro Corporation Chubb and Sons, Inc. GATX Corporation Aon Corporation CIGNA Corporation GE Applied Materials Circuit City Stores, Inc. General Mills, Inc. Archer-Daniels-Midland Climax Portable Machine Tools, Inc. The Gillette Company Argonaut Group, Inc. CNA Insurance GlaxoSmithKline Arkema, Inc. Coca-Cola Company Goodrich Corporation W.W. Grainger, Inc. Lubrizol National Computer Systems Gramco Construction Mallinckrodt, Inc. National Instruments Hallock Modey, Inc. Management Compensation NCR Corporation Hanna Andersson Group/Dulworth, Inc.