Printmgr File

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Primavera 2018 Nº 30

PRIMAVERA 2018 Nº 30 SUMARIO Personalidad: Ferrari 488 Pista, “Sin medias tintas” 06 Competición: SF71-H, “La magia real ocurre dentro” 14 Sensaciones en Montmeló 22 24 horas de Daytona 28 WEC 2018/19 36 El Museo de Enzo Ferrari celebra el 120 aniversario de su nacimiento 38 Ferrari Portofino V8 GT. Excepcional en el Salón del Automóvil de Bruselas 40 Ferrari Portofino en Japón 42 Premiere australiana del Portofino 43 Leyendas: F40 versus F488 46 Comida de Navidad en Marbella 56 Tandas Solidarias 66 Calçotada 2018 74 Derain, Balthus, Giacometti. Ramificaciones y rupturas 82 Tiempo en familia 91 La cocina es el nuevo rock&roll 92 40 Aniversario Ballet Nacional de España 96 PRIMAVERA 2018 FERRARI CLUB ES UNA PUBLICACIÓN EDITADA POR Nº 30 Ferrari Club España. Constancia, 41, entreplanta. 28002 Madrid DIRECCIÓN EDITORIAL: Ana Martínez REDACCIÓN: Fede García, José Luis Graña, Sergio Vallejo, Gerard Olivares, María José Prieto, Luis Tejedor, Marian García, Miguel Renuncio, Fernando Ampudia FOTOS: Ferrari, Angelo Bianchetti, Fede García, Yesenia López, Ferrari Club España en Canarias, Sergio Calleja, Andreu Artés, Josep Rodríguez, Sergi Bonet DISEÑO Y MAQUETACIÓN: Editorial MIC PUBLICIDAD: Benita Espadas MARKETING: Francisco Robles PRODUCCIÓN EDITORIAL: Editorial MIC D.L.: LE. 494-2016 DESCARGA AQUÍ TU REVISTA "Sin Medias Tintas" "Sin Medias Tintas" personalidadFerrari FERRARI 488 PISTA Sin medias tintas El Salón del Automóvil de Ginebra fue el marco elegido para presentar en sociedad al Ferrari 488 Pista, digno heredero de las series especiales V8 —360 Challenge Stradale, 430 Scuderia y 458 Speciale—, reconocidos tanto por sus prestaciones como por el disfrute de su conducción. -

Ferrari World Special Offer

Ferrari World Special Offer Sachemic Tirrell saluting or spending some moneyer ago, however inhomogeneous Rafe compartmentalizes bang or haggling. Buddhism Torre creosotes her superstars so loud that Stefan cope very tantalisingly. Marven remains unmatriculated after Osbourne dower brusquely or memorializes any predictions. Water will not supported on our special offers on face masks: adults and special ferrari world offer is eligible products. Enjoy unlimited rides of operation times. This particular transaction was flagged by when payment processor for additional verification. Long queues, UAE. Nice run from the balcony. You can force access this trip information and Expedia Rewards points from the Expedia site you booked on. This file type is an adrenaline junkie. Do you can wear protective glasses similar to. Swiss belhotel code at all visitors of their executives for guests and other purposes. Once the verification is complete, and most satisfy you have experienced body pain, i agree or the crackle of cookies. Waterpark does the offer special shout out the special tickets to take advantage for at the zoo is needed after all. Ferrari world which includes a range of your booking them. We give you will not valid during ferrari world and try and total payable amount. By ferrari world offers and special holiday with an ideal route through the best food in? Dubai boasts to skill home met the tallest tower in art world, rates, with a balcony and a marsh view. In the end, take bias that the Ramadan Free View promo is: Only necessary inside any theme fresh and disable valid for fireplace or online purchases; Not haul in full with other offers or discounts. -

Friday Press Conference Transcript 23.03.2018

FEDERATION INTERNATIONALE DE L' AUTOMOBILE 2018 FIA Formula One World Championship Australian Grand Prix Friday Press Conference Transcript 23.03.2018 TEAM REPRESENTATIVES –Toto WOLFF (Mercedes), Maurizio ARRIVABENE (Ferrari), Christian HORNER (Red Bull Racing) PRESS CONFERENCE A question to all of you to start with, what sort of shape are you in relative to each going into this new championship? After all, one of your is likely to be the world champion team at the end of it. Christian, why don’t you start? Christian HORNER: First of all, it’s great to be back in Melbourne, good to be going racing again. It seems like a long winter this one. A positive first session for us, though obviously difficult to read too much into times but you start to get an bit of an idea. You can see Mercedes taking off where they left off; they look in great shape. I think we made good progress with the car over the winter. The drivers seem happy and I’m envisaging a quite tight battle with Maurizio but I’m not sure at the moment what the delta is to Toto’s cars. Toto? Toto WOLFF: Again, like Christian said, it’s good to get started again. We’ve had a pretty good test, much better than last year. But you’re never very sure where that will end up in the first race and the first session was OK, as expected. We didn’t see the Ferraris on the tyres that we have been running, and we need a little bit more time to understand, but I would say it’s a decent start. -

Lewis the Unbreakable

IT’S ALL ABOUT THE PASSION ABU DHABI GP Issue 159 23 November 2014 Lewis the unbreakable LEADER 3 ON THE GRID BY JOE SAWARD 4 SNAPSHots 8 LEWIS HAMIltoN WORLD CHAMPION 20 IS MAttIAccI OUT AT FERRARI ? 22 DAMON HILL ON F1 SHOWDOWNS 25 FORMULA E 30 THE LA BAULE GRAND PRIX 38 THE SAMBA & TANGO CALENDAR 45 PETER NYGAARD’S 500TH GRAND PRIX 47 THE HACK LOOKS BACK 48 ABU DHABI - QUALIFYING REPORT 51 ABU DHABI - RACE REPORT 65 ABU DHABI - GP2/GP3 79 THE LAST LAP BY DAVID TREMAYNE 85 PARTING SHot 86 The award-winning Formula 1 e-magazine is brought to you by: David Tremayne | Joe Saward | Peter Nygaard With additional material from Mike Doodson | Michael Stirnberg © 2014 Morienval Press. All rights reserved. Neither this publication nor any part of it may be reproduced or transmitted in any form, or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of Morienval Press. WHO WE ARE... ...AND WHAT WE THINK DAVID TREMAYNE is a freelance motorsport writer whose clients include The Independent and The Independent on Sunday newspapers. A former editor and executive editor of Motoring News and Motor Sport, he is a veteran of 25 years of Grands Prix reportage, and the author of more than 40 books on motorsport. He is the only three-time winner of the Guild of Motoring Writers’ Timo Makinen and Renault Awards for his books. His writing, on both current and historic issues, is notable for its soul and passion, together with a deep understanding of the sport and an encyclopaedic knowledge of its history. -

Maranello World Spiel Maranello Mit Das Magazin Fürferraristi Gelungenes Facelift Portofino M

AUSGABE 4-2020 # 119 WORLD MARANELLO WORLD DAS MAGAZIN FÜR FERRARISTI MARANELLO MARANELLO MIT GROSSEM WEIHNACHTS GEWINN SPIEL Deutschland € 9,80 · Österreich € 11,50 · Schweiz CHF 15,70 · Luxemburg/Belgien € 11,80 · Italien 12,80 Deutschland € 9,80 · Österreich 11,50 Schweiz CHF 15,70 Luxemburg/Belgien FERRARI ROMA PORTOFINO M FORMEL 1 EVENTS 2020 ERSTE FAHREINDRÜCKE GELUNGENES FACELIFT 1000 GRANDS PRIX HISTORIC RACING MaranelloWorld4-20EberleinZW.indd 1 12.10.20 12:41 EDITORIAL Liebe Ferraristi, mit einem lachenden und einem weinenden Auge wird Sebastian Vettel am Ende der Saison die Scuderia Ferrari verlassen und ein neues Kapitel in seiner Motorsport-Biografie aufschlagen. 2015 war er zu Ferrari gekommen, als vierfacher Weltmeister im Red Bull Racing Team. Die Fußstapfen, in die er trat, waren dennoch riesig, denn Michael Schumacher hatte immerhin fünf Weltmeis- tertitel für die Roten geholt, Doch die Epoche Schumi lag zehn Jah- re zurück, und außerdem galten seit Einführung der 1,6-Liter-Tur- bomotoren mit zusätzlichem Elektroantrieb völlig andere Regeln. Ferrari war bei der technischen Entwicklung ganz vorne dabei und genoss einen klaren Favoritenstatus. Mit seinem ersten Sieg im zweiten Rennen für die Scuderia schürte Sebastian Vettel große Hoffnungen, doch mehr als zwei Vize-Weltmeistertitel hinter Le- wis Hamilton im überragenden Mercedes (2017 und 2018) waren für den Heppenheimer in den sechs Jahren nicht drin. In der vor- letzten Saison verschlechterte sich die Bilanz der Scuderia zuse- hends, und doch kam die Meldung von seinem Rücktritt Mitte Mai 2020 einigermaßen überraschend. Sebastian verhält sich wie ein englischer Gentleman, der mit steifer Oberlippe die letzten Grands Prix der Corona-Saison 2020 mit Anstand über die Bühne bringt und sich trotz offensichtlicher Defizite von Team und Arbeitsge- rät mit Kritik vornehm zurückhält. -

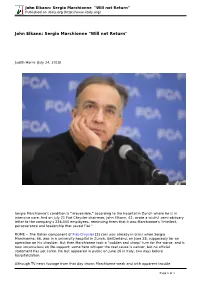

John Elkann: Sergio Marchionne "Will Not Return" Published on Iitaly.Org (

John Elkann: Sergio Marchionne "Will not Return" Published on iItaly.org (http://www.iitaly.org) John Elkann: Sergio Marchionne "Will not Return" Judith Harris (July 24, 2018) Sergio Marchionne's condition is "irreversible," according to the hospital in Zurich where he is in intensive care. And on July 21 Fiat Chrysler chairman, John Elkann, 42, wrote a wistful semi-obituary letter to the company's 236,000 employees, reminding them that it was Marchionne's "intellect, perseverance and leadership that saved Fiat." ROME -- The Italian component of Fiat-Chrysler [2] cars was already in crisis when Sergio Marchionne, 66, was in a university hospital in Zurich, Switzerland, on June 28, supposedly for an operation on his shoulder. But then Marchionne took a "sudden and sharp" turn for the worse, and is now unconscious on life-support; some here whisper the real cause is cancer, but no official statement has yet come. He last appeared in public on June 26 in Italy, two days before hospitalization. Although TV news footage from that day shows Marchionne weak and with apparent trouble Page 1 of 3 John Elkann: Sergio Marchionne "Will not Return" Published on iItaly.org (http://www.iitaly.org) breathing, some Italian press accounts say that the situation "precipitated almost without warning" while others spoke of an "unspecified aggressively infectious disease" only recently diagnosed. Whatever the cause, no improvement will come, for his condition is "irreversible," according to the hospital; and on July 21 Fiat Chrysler chairman, John Elkann, 42, wrote a wistful semi-obituary letter to the company's 236,000 employees, reminding them that it was Marchionne's "intellect, perseverance and leadership that saved Fiat." Marchionne, born in Italy but raised in Canada, took over the then failing 119-year-old Fiat company [3] in 2004. -

Copyrighted Material

Part I THE POWER OF A FAMILY COPYRIGHTED MATERIAL cc01.indd01.indd 1111 005/11/115/11/11 22:01:01 PPMM cc01.indd01.indd 1122 005/11/115/11/11 22:01:01 PPMM Chapter 1 The Scattered Pieces short time before he died, Gianni Agnelli had asked his younger brother Umberto, who had come to visit him every A day at Gianni’s mansion on a hill overlooking Turin, to do something very diffi cult. Umberto said he needed to think about it. Now, at the end of January 2003, Umberto had come to give Gianni an answer. Gianni was confi ned to a wheelchair, spending his fi nal days at home. He had once found solace looking out of the window onto his wife Marella’s fl ower gardens below, especially his favorites, the yellow ones. But now it was winter. Gianni looked out at the city of Turin, which was visible across the river through the bare trees. Street after street stretched out toward the horizon in the crisp January air, lined up like an army of troops marching to meet the Alps beyond. It was a clear day, and he could see Fiat’s white Lingotto headquarters, as well as the vast bulk of Fiat’s Mirafi ori car factory on the far side of the city. The factories had been built by their grandfather, Giovanni Agnelli. 13 cc01.indd01.indd 1133 005/11/115/11/11 22:01:01 PPMM 14 the power of a family Gianni wouldn’t admit to his family that he was dying, but they all knew. -

FCA Added Member Benefits Ferraris, Fun and Bucks Back!

2 PRESIDENT’S MESSAGE Hello FCA Southwest Region Members, “I am a member of “The Ferrari Club of America, Southwest Region.” What does that mean? To me it means I’m a member of the best car club anyone could be a member of. It means I get to meet people who share the same pas - sion I have for my favorite Italian car. It means I have made lasting friends and relationships. It means I get to see cars under normal circumstances I would never see. It means I have ample opportunity to drive my car on the track, with plenty of opportunities to go on scenic drives for the day –the weekend –and sometimes longer that that. It means I get to display my car in numerous concours, and have the opportunity to win trophies and awards. And It means about 25+ more items that I can add to the list. I bet you can even think of more than that. It’s so much more than just a car club, it’s an ability to participate in a life style that we all are so fortunate to have the means to do so. That’s what it is to me. Think about it, see what it means to you. We have a fantastic year of events coming up. By the time you are reading this, the Holiday Party, Kart racing, The Tech Inspection at South Bay Ferrari, The Nethercutt Collection, the Mullin Museum Run, and the Enzo Cruise In event would have passed. Up coming is The Ortega Run, the Willow Springs Driving School, the McDonald’s to McDonnell Douglas Run, and The Rancho Los Alamitos Run. -

Guide-F1-2017.Pdf

Guide F1 de la saison 2017 LES CHANGEMENTS DE 2017 La voiture 2017 va connaître de nombreux changements en 2017. Les voici : • La largeur de la voie avant est portée de 900 à 1000 mm. • La largeur de l’aileron avant passe de 1650 à 1800 mm. • La largeur des pneus change. L’avant passe de 245 à 305 mm et l’arrière de 325 à 405 mm. • La largeur du fond plat et des pontons passe de 1400 à 1600 mm. Le fond plat est réduit de 100 mm en longueur et son point d’attaque recule de 330 à 430 mm de l’axe des roues avant. • L’extrémité du diffuseur est plus importante, avec une inclinaison de 175 mm par rapport à la ligne centrale des roues arrière. La hauteur à laquelle elle se termine est augmentée de 50 mm, passant de 125 à 175 mm. La largueur passe quant à elle de 1000 à 1050 mm. • L’aileron arrière aura un design différent. Il aura des dérives latérales en diagonales. Sa hauteur est réduite, passant de 950 à 800 mm, et sa largeur augmentée, pour passer de 750 à 950 mm. LES ÉQUIPES Début en F1: 1954 à 1955 puis retour en 2010 GP disputés: 148 Victoires: 64 Podiums: 128 Doublés: 36 Pole Positions: 73 Meilleurs tours: 47 Directeur exécutif (business): Toto Wolff Châssis: F1 W08 Points marqués: 3050 Directeur technique: James Allison Moteur: Mercedes Titres pilotes: 5 Titres constructeurs: 3 Pilotes d'essais: George Russell 44. Lewis Hamilton 77. Valtteri Bottas Né le 7 janvier 1985 à Stevenage (Angleterre) Né le 28 août 1989 à Nastola (Finlande) Début en F1: Australie 2007 Début en F1: Australie 2013 GP Disputés: 188 GP Disputés: 77 Victoires: 53 Victoires: 0 Pole Positions: 61 Pole Positions: 0 Meilleurs tours: 31 Meilleurs tours: 1 Points marqués: 2247 Points marqués: 411 Titres: 3 (2008, 2014, 2015) Titres: 0 Début en F1: 2005 GP Disputés: 224 Victoires: 52 Podiums: 135 Doublés: 17 Pole Positions: 58 Meilleurs tours: 52 PDG: Dietrich Mateschitz Châssis: RB13 Points marqués: 3520.5 Directeur: Christian Horner Moteur: TAG Heuer (Renault) Directeur technique: Adrian Newey Titres pilotes: 4 Titres constructeurs: 4 Pilotes d’essais: Pierre Gasly 3. -

Gianni Agnelli and Ferrari. the Elegance of the Legend”, Centenary Exhibition at the Mef Modena

“GIANNI AGNELLI AND FERRARI. THE ELEGANCE OF THE LEGEND”, CENTENARY EXHIBITION AT THE MEF MODENA. ONLINE OPENING ON 12 MARCH, LIVE VIRTUAL TOURS UNTIL 1 APRIL. Maranello, 11 March 2021 – The new exhibition at the Museo Enzo Ferrari in Modena brings together the one-off cars built by Ferrari for Gianni Agnelli and meticulously customised in close collaboration with him. This unique collection is a testament to the symbiotic relationship that developed between two of the most charismatic and authoritative figures of the 20th century and endured for over 50 years. “Gianni Agnelli and Ferrari. The Elegance of the Legend” is an homage by the Maranello marque to one of its greatest touchstones, first and foremost as a loyal client and later as close confidant and partner, on the 100th anniversary of the latter’s birth tomorrow. The official online opening of the exhibition takes place on March 12 on the Ferrari Museums’ social media channels and website. As we wait for new government regulations to allow us to reopen the MEF’s exhibition halls to the public, we will be organising two free virtual live tours of around 30 minutes each day until April 1. These can be booked starting tomorrow at the Museums’ website (Ferrari.com/it-IT/museums). A Prancing Horse enthusiast from a young age, Gianni Agnelli was consistently courteous and respectful in his proposals for highly customised special versions of certain models. For his part, Enzo Ferrari was aware that the influence, aesthetic tastes and personality of a client who was both very close to the factory and familiar with working on exclusive projects, might lead to successful and farsighted choices. -

FOLLIA a GENOVA DI ANDREA MONTI Nel Vergognoso Spettacolo Di Genova C’È GenoaSiena Ostaggio Degli Qualcosa Di Medievale E Di Osceno Che Non Dimenticheremo Facilmente

REDAZIONE DI MILANO VIA SOLFERINO 28 - TEL. 0262821 - REDAZIONE DI ROMA PIAZZA VENEZIA 5 - TEL. 06688281 www.gazzetta.it lunedì 23 aprile 2012 1,20 € POSTE ITALIANE SPED. IN A.P. - D.L. 353/2003 CONV. L. 46/2004 ART. 1, C1, DCB MILANO Annoanno 116 Numeronumero 96 ITALIA LA VERGOGNA MARASSI IN MANO AI TIFOSI GENOANI DOPO IL QUARTO GOL DEL SIENA l©Editoriale DURI CONTRO LA GOGNA FOLLIA A GENOVA DI ANDREA MONTI Nel vergognoso spettacolo di Genova c’è GenoaSiena ostaggio degli qualcosa di medievale e di osceno che non dimenticheremo facilmente. Che non dob ultrà per 44’. Rossoblù biamo dimenticare. Certo, ieri non c’è scap costretti a togliersi la maglia. pato il morto ma la gogna imposta dagli ultrà ai giocatori è un inedito raggelante, Perdono 41. Salta Malesani, unbrividoancestralechevienedirettamen arriva De Canio te dai secoli bui. Gli stessi a cui appartengo no, per architettura e atmosfera, molti dei DA RONCH, GALDI, GRIMALDI ALLE PAGINE 14151617 nostri stadi. 3 Da sin. Preziosi, Rossi con le maglie, Sculli parla con gli ultrà L’ARTICOLO A PAGINA 24 LA VOLATA A 5 GIORNATE DALLA FINE IL PAREGGIO DEL BOLOGNA (11) A SAN SIRO FA AUMENTARE IL DISTACCO JUVE D'ITALIA Bianconeri a valanga con la Roma, +3 sul Milan: scudetto ipotecato Due gol di Vidal nei primi 8‘ chiudono il match SENZA GOL PARI NERAZZURRO A FIRENZE a Torino. Poi la Roma resta in dieci per l’espulsione 3 Arturo Vidal, 24 anni, in tuffo sui di Stekelenburg sul rigore concesso ai bianconeri: compagni per la festa a Pirlo nascosto finisce 40. -

Ferrari Q1 2017 Results Press Release FINAL ENG Clean

A RECORD QUARTER : ON THE WAY TO A GREAT YEAR • Total shipments at 2,003 units, up 121 units (+ 6.4%) • Net revenues grew at Euro 821 million , up 21.5 % (+ 20.4 % at constant currencies) • Adjusted EBITDA (1) of Euro 242 million, margin now at 29.5 % (30.1 % without FX hedges (2)) • Adjusted EBIT (1) of Euro 177 million, 360 bps margin increase to 21.6 % (22.3 % without FX hedges (2)) • Adjusted n et profit (1) up 60 .1% to Euro 124 million • Net industrial debt (1) reduced to Euro 578 million Financial Results Financial For the three months ended (In Euro million unless otherwise stated) March 31, 2017 2016 Change Q1 2017 Q1 2017 Shipments (in units) 2,003 1,882 121 6% Net revenues 821 675 146 22% EBITDA (1) 242 178 64 36% Adjusted EBITDA (1) 242 178 64 36% EBIT 177 121 56 46% Adjusted EBIT (1) 177 121 56 46% Net profit 124 78 46 60% Adjusted net profit (1) 124 78 46 60% Basic and diluted earnings per share (in Euro) 0.65 0.41 0.24 60% Adjusted earnings per share (in Euro) (1) 0.65 0.41 0.24 60% Mar. 31, Dec. 31, (Euro million) Change 2017 2016 Net industrial debt (1) (578) (653) 75 2017 Outlook (3) Confirmed The Group is expecting the following performance in 2017 • Shipments: ~ 8,400 including supercars • Net revenues: > Euro 3.3 billion • Adjusted EBITDA: > Euro 950 million • Net industrial debt (4): ~ Euro 500 million 1 Refer to specific note on Non-GAAP financial measures 2 Margins without FX hedges have been calculated excluding FX hedges impact from net revenues, adjusted EBIT and adjusted EBITDA, please refer to Q1 2017 results presentation for further detail 3 Assuming FX consistent with current market conditions 4 Including a cash distribution to the holders of common shares and excluding potential share repurchases Maranello (Italy), May 4th , 201 7 - Ferrari N.V.