Dream Incubator / 4310

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Published 22 February 2019 LKFF 2012

THE LONDON KOREAN FILM FESTIVAL 제7회 런던한국영화제 1-16 NoVEMBER StARTING IN LONDON AND ON TOUR IN BOURNEMOUTH, GlASGOW AND BRISTOL 12�OZE�293 OZ Quadra Smartium(Film Festival).pdf 1 10/18/12 6:14 PM A MESSAGEUR ROM O TOR LONDON-SEOUL, DAILY F TIC DIREC ASIANA AIRLINES ARTIS is redefining It is with great pride and honour that I welcome you to the 7th London Korean Film Festival. Regardless of whether you are a connoisseur of Korean cinema or completely Business Class. new to the country’s film scene, we have created an exciting and varied C Beginning November 17th, all the comforts of programme that will delight, thrill, scare and, most importantly, entertain you. M our new premium business class seat, Y the OZ Quadra Smartium, can be yours. We start off large with our return to the Odeon West End with one of the CM There’s a wonderful new way to get back and biggest Korean films in the last ten years;The Thieves. Our presentation MY forth to Seoul everyday. Announcing Asiana Airlines’ innovative of this exciting crime caper also sees its director, Choi Dong-hoon, and new premium business class seat, the OZ Quadra Smartium, lead actor Kim Yoon-suk gracing London’s Leicester Square. CY offering you both the privacy of your own space CMY and the relaxation of a full-flat bed. From the 2nd of November through to the 10th in London (continuing until the 16th in K Glasgow, Bristol and Bournemouth) we will show everything from the big box office hits to the smallest of independents, ending with the much-lauded Masquerade, as our closing Gala feature. -

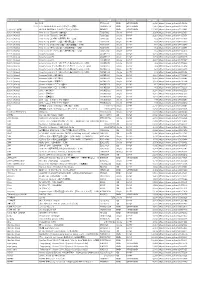

アーティスト 商品名 品番 ジャンル名 定価 URL 100% (Korea) RE

アーティスト 商品名 品番 ジャンル名 定価 URL 100% (Korea) RE:tro: 6th Mini Album (HIP Ver.)(KOR) 1072528598 K-POP 2,290 https://tower.jp/item/4875651 100% (Korea) RE:tro: 6th Mini Album (NEW Ver.)(KOR) 1072528759 K-POP 2,290 https://tower.jp/item/4875653 100% (Korea) 28℃ <通常盤C> OKCK05028 K-POP 1,296 https://tower.jp/item/4825257 100% (Korea) 28℃ <通常盤B> OKCK05027 K-POP 1,296 https://tower.jp/item/4825256 100% (Korea) 28℃ <ユニット別ジャケット盤B> OKCK05030 K-POP 648 https://tower.jp/item/4825260 100% (Korea) 28℃ <ユニット別ジャケット盤A> OKCK05029 K-POP 648 https://tower.jp/item/4825259 100% (Korea) How to cry (Type-A) <通常盤> TS1P5002 K-POP 1,204 https://tower.jp/item/4415939 100% (Korea) How to cry (Type-B) <通常盤> TS1P5003 K-POP 1,204 https://tower.jp/item/4415954 100% (Korea) How to cry (ミヌ盤) <初回限定盤>(LTD) TS1P5005 K-POP 602 https://tower.jp/item/4415958 100% (Korea) How to cry (ロクヒョン盤) <初回限定盤>(LTD) TS1P5006 K-POP 602 https://tower.jp/item/4415970 100% (Korea) How to cry (ジョンファン盤) <初回限定盤>(LTD) TS1P5007 K-POP 602 https://tower.jp/item/4415972 100% (Korea) How to cry (チャンヨン盤) <初回限定盤>(LTD) TS1P5008 K-POP 602 https://tower.jp/item/4415974 100% (Korea) How to cry (ヒョクジン盤) <初回限定盤>(LTD) TS1P5009 K-POP 602 https://tower.jp/item/4415976 100% (Korea) Song for you (A) OKCK5011 K-POP 1,204 https://tower.jp/item/4655024 100% (Korea) Song for you (B) OKCK5012 K-POP 1,204 https://tower.jp/item/4655026 100% (Korea) Song for you (C) OKCK5013 K-POP 1,204 https://tower.jp/item/4655027 100% (Korea) Song for you メンバー別ジャケット盤 (ロクヒョン)(LTD) OKCK5015 K-POP 602 https://tower.jp/item/4655029 100% (Korea) -

Super Junior

Super Junior Super Junior ((hangulhangul: )?, también conocido co- momo SuJu o o SJ SJ, es unauna boy boy band, proveniente dede Corea Corea del Sur. Formada en el 2005 porpor SM SM Entertainment,, Suju consconstabataba orioriginaginalmelmentente de 12 miemiembrmbros,os, espespe-e- cializados en el ámbito del entretenimiento musical y actoral. Los miembros originales eran:eran: Leeteuk Leeteuk (el lí- der),der), Heechul,, Yesung Yesung,, Shindong,, Kang-in Kang-in,, Sungmin Sungmin,, Eunhyuk,, Donghae Donghae,, Siwon Siwon,, Kibum Kibum,, Ryeowook Ryeowook yy Han Geng. Luego se agregó un decimotercer miembmiembroro llama- dodo Kyuhyun Kyuhyun en el 2006. Super Junior ha realizado siete álbumes de estudio y unun sencillo sencillo desde el 2005, alcanzando el reconocimien- to internacional tras el lanzamiento de su álbum “Sorry, Seúl, ciudad donde se formó Super Junior. Sorry” en el 2009. Además de su éxito comercial, Super Junior ha ganado trece premios en los Mnet Asia Music Awards, dieciséis en los Golden Disk Awards, once pre- 1.1 20002000–200–2005:5: ForFormacmaciónión y DDebebutut popularidadmios en los Seoul de Golden Music Disk Awards Awards, además los años del 2009,premio 2010 a la y 2011. En 2002000,0, SM SM Entertainment tuvo su primer casting En el 2012, fueron nominados como “Mejor Acto Asiá- en el extranjero enen Pekín Pekín,, China China, y descubrió aa Han tico” en loslos MTV MTV Europe Music Awards, mostrando una Geng, quien se presentó a la audición junto con otros vez más su popularidapopularidadd en el mundo. 3.000 participantes. Ese mismo año,año, Leeteuk Leeteuk,, Yesung Yesung yy Eunhyuk Eunhyuk fueron seleccionados después de audicionar Kibum, está como miembro inactivo para seguir con su para la compañía en un sistema de casting anual enen Seúl Seúl. -

Dream Incubator / 4310

Dream Incubator / 4310 COVERAGE INITIATED ON: 2013.10.29 LAST UPDATE: 2020.10.29 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Dream Incubator / 4310 RCoverage LAST UPDATE: 2020.10.29 Research Coverage Report by Shared Research Inc. | www.sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Executive summary ----------------------------------------------------------------------------------------------------------------------------------- 3 Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 5 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 7 Highlights -

Super Junior

Super Junior From Wikipedia, the free encyclopedia For the professional wrestling tournament, see Best of the Super Juniors. Super Junior Super Junior performing at SMTown Live '08 in Bangkok,Thailand Background information Origin Seoul, South Korea Genres Pop, R&B, dance, electropop, electronica,dance-pop, rock, e lectro, hip-hop, bubblegum pop Years active 2005–present Labels S.M. Entertainment (South Korea) Avex Group (Japan) Associated SM Town, Super Junior-K.R.Y., Super Junior-T,Super acts Junior-M, Super Junior-Happy, S.M. The Ballad, M&D Website superjunior.smtown.com,facebook.com/superjunior Members Leeteuk Heechul Han Geng Yesung Kangin Shindong Sungmin Eunhyuk Donghae Siwon Ryeowook Kibum Kyuhyun Korean name Hangul 슈퍼주니어 Revised Romanization Syupeojunieo McCune–Reischauer Syupŏjuniŏ This article contains Koreantext. Without proper rendering support, you may see question marks, boxes, or other symbolsinstead of Hangul or Hanja. This article contains Chinesetext. Without proper rendering support, you may see question marks, boxes, or other symbolsinstead of Chinese characters. This article contains Japanesetext. Without proper rendering support, you may see question marks, boxes, or other symbolsinstead of kanji and kana. Super Junior (Korean: 슈퍼주니어; Japanese: スーパージュニア) is a South Korean boy band from formed by S.M. Entertainment in 2005. The group debuted with 12 members: Leeteuk (leader), Heechul, Han Geng, Yesung, Kangin, Shindong, Sungmin, Eunhyuk, Donghae, Siwon,Ryeowook, Kibum and later added a 13th member named Kyuhyun; they are one of the largest boy bands in the world. As of September 2011, eight members are currently active,[1] due to Han Geng's lawsuit with S.M. -

Stream Media Corporation / 4772

Stream Media Corporation / 4772 COVERAGE INITIATED ON: 2021.07.20 LAST UPDATE: 2021.07.20 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Stream Media Corporation/ 4772 RCoverage LAST UPDATE: 2021.07.20 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Executive summary ----------------------------------------------------------------------------------------------------------------------------------- 3 Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 5 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- -

Cho Kyuhyun. Th

This thesis belongs to one of the graduates who graduated from Kyunghee University Post Modern Music Degree – Cho Kyuhyun. This is the English version of Kyuhyun’s Thesis and it is translated by the 6 of us as below:- Please respect our translation work, no re-editing or commercial use are allowed. Please remember to give credits if you reupload. Translators: SUJU Memories, Happiezappie, elfxlove, heenimed, InezGenn and kyuju32810 Review: SUJU Memories Mapping: SUJU Memories, Happiezappie, heenimed etc. Thank you for your cooperation. Master Degree Thesis The status and future development of K-POP – As K-POP itself In countries like Japan and China We take their success stories cases as a basic, looking at America, Europe markets of K-POP, their marketing strategy – Associate Professor Lee Woo Chang Kyunghee University Graduate School Post Modern Music Major Cho Kyuhyun Year 2016 February 2nd Master Degree Thesis The status and future development of K-POP – As K-POP itself In countries like Japan and China We take their success stories cases as a basic, Looking at America, Europe markets of K-POP, their marketing strategy – Associate Professor Lee Woo Chang Kyunghee University Graduate School Post Modern Music Major Cho Kyuhyun Year 2016 February 2nd The status and future development of K-POP – As K-POP itself In countries like Japan and China We take their success stories cases as a basic, Looking at America, Europe markets of K-POP, their marketing strategy – Associate Professor Lee Woo Chang This Thesis is set as a master’s degree thesis Kyunghee University Graduate School Post Modern Music Major Cho Kyuhyun Year 2016 February 2nd Cho Kyuhyun of Post Modern Music Department Master’s Degree Thesis Acknowledgement Chief examiner Lim Dong Gyun Review Professor Lee Woo Chang Review Professor Michelle Review Professor Han Kyung Hoon Kyung Hee University Graduate School Year 2016 February 2nd Content <ABSTRACT> ................................................................................................................................................... -

Stream Media Corporation / 4772

Stream Media Corporation / 4772 COVERAGE INITIATED ON: 2021.07.20 LAST UPDATE: 2021.08.11 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Stream Media Corporation/ 4772 RCoverage LAST UPDATE: 2021.08.11 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Executive summary ----------------------------------------------------------------------------------------------------------------------------------- 3 Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 5 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- -

Spotlight on Fitness

March-April 2013 VOL. 28 THE VIDEO REVIEW MAGAZINE FOR LIBRARIES N O . 2 IN THIS ISSUE ALA Notables | Spotlight on Fitness | Into the Cold | Detropia | Inocente | Birders | Escape Fire | Putin’s Kiss | The Qatsi Trilogy BAKER & TAYLOR’S scene & heard ENTERTAINMENT SOLUTIONS Baker & Taylor offers all the A/V products, services and expertise that your library needs to meet rising patron demand for movie and music products. • Expertise and a wide selection of CD, DVD and Blu-ray releases, including top new releases, classics, children’s and family, and more • Extensive on-hand inventory in strategically located warehouses and fast delivery nationwide • A wide variety of library-friendly programs and services including: Digital Media Processing services, Automatically Yours™ standing order programs, Music & Movie Parade auto-ship plans, exclusive NPR Discover Songs program and TechXpress cataloging and processing services • Customized buying guides and The Red Carpet and The Green Room websites to help you and your library obtain the most appropriate content • Experienced, dedicated A/V Sales Consultants and easy ordering 24/7 through Title Source™ 3 www.baker-taylor.com 800-775-2600 x2666 [email protected] Spotlight Review Into the Cold the lunar-like landscape of older ice (which HHHH is alarmingly decreasing, thanks to global (2010) 87 min. DVD: warming); and transparent sheets of ice like $24.98 (avail. from most a thin glass floor over a freezing ocean. The Publisher/Editor: Randy Pitman distributors, Apr. 9), $199 numerous difficulties the men encounter Associate Editor: Jazza Williams-Wood w/PPR: public libraries, while trying to survive in this inhospitable $249 w/PPR: colleges environment (where temperatures plunge Copy Editor: Kathleen L. -

Copyright by Chuyun Oh 2015

Copyright by Chuyun Oh 2015 The Dissertation Committee for Chuyun Oh Certifies that this is the approved version of the following dissertation: K-popscape: Gender Fluidity and Racial Hybridity in Transnational Korean Pop Dance Committee: Rebecca Rossen, Supervisor Omi Osun Joni L. Jones Paul Bonin-Rodriguez Cherise Smith Heather Hindman Youjeong Oh K-popscape: Gender Fluidity and Racial Hybridity in Transnational Korean Pop Dance by Chuyun Oh, B.A.; M.A. Dissertation Presented to the Faculty of the Graduate School of The University of Texas at Austin in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy The University of Texas at Austin May 2015 Acknowledgements I would like to extend my thanks to PPP faculty members whose advice and help significantly contributed to my dissertation. I offer the deepest appreciations to my academic advisor, Rebecca Rossen, for supporting my dissertation and academic progress for the last five years with great enthusiasm, insight, and mentorship. I am also thankful to Omi Osun Joni L. Jones and Paul Bonin for their generous help and inspiring scholarship. I want to thank each member of my committee, Cherise Smith, Heather Hindman, and Youjeong Oh, for the time to read and respond to my work with advice. I also offer thanks to my colleagues, friends, and Theatre and Dance faculty members whose artistic and scholarly endeavors have significantly inspired my work. Lastly, I express my sincere gratitude and love to my family members and loved one. Without their help, care, love, and patience, everthing I have achieved would not have been possible. -

Smtown the Stage Eng Sub Full Movie 13

1 / 5 Smtown The Stage Eng Sub Full Movie 13 Jun 10, 2020 — The movie to be released in Korean theaters on 8/13 for two weeks (until 8/26),.... 176 cm (1.76 m) ... April 9, 2016: Made his debut on the sub-unit .... Smtown The Stage Eng Sub Full Movie 176 by Tyler Brantley. ... The following Law Of The Jungle In Costa Rica Episode 175 Eng Sub has been released. ... episode 7, ep 8, ep 9, episode 10, Korean Drama ep 11, ep 12, ep 13, epi 14, ep 15, .... The group was divided into two subgroups, EXO-K ("K" Korean in English) by South ... (HEART FOR YOU) EPISODE 7 XIUMIN [SUB INDO] Anisya Danoewinoto. ... See you at 4:45PM KST on Netflixkr/SMTOWN/EXO's NAVER V-LIVE Channel!!! ... Jul 13, 2020 · EXO-SC's Chanyeol and Sehun appeared on Naver's VLive to .... SM Town Live World Tour III was the 2012–13 worldwide live concert tour by SM Town. The tour commenced with one show in Anaheim, California on May 20, .... [ENG SUB] [HD] 150710 SMTown The Stage Documentary Movie Teaser ... 4:55 AM - 12 Jul ... Review] Korean Weekend Box Office 2012.07.13 ~ 2012.07.15 . Unofficial Streaming: YouTube (Eng Sub). SMTown The Stage (2015). Release Date: Aug. 13, 2015. Genre: Documentary Network: ... SMTown Live in. Madison .... The film was directed by Bae Seong-san and produced by Lee Soo-man , Jung Chang- hwan, and Han Se-min. In Korea, the film premiered on August 13, 2015, .... May 26, 2021 — EXO - ENG SUB Videos [엑소 | EXO Planet sub thread]. -

Url 430 Run Fty12001 Dvd Ot

アーティスト 商品名 オーダー品番 フォーマットジャンル名 定価(税抜) URL 430 RUN FTY12001 DVD OTHER DVD 2,314 https://tower.jp/item/3141062 2700 2700 NEW ALBUM ラストツネミチ-ヘ長調- YRBN90516 DVD OTHER DVD 2,857 https://tower.jp/item/3205636 (スポーツ・野球) WORLD BASEBALL CLASSIC プレミアムBOX DEWBC1 DVD OTHER DVD 12,000 https://tower.jp/item/2161881 100% (Korea) How to cry (Type-A) <通常盤> TS1P5002 Single K-POP 1,204 https://tower.jp/item/4415939 100% (Korea) How to cry (Type-B) <通常盤> TS1P5003 Single K-POP 1,204 https://tower.jp/item/4415954 100% (Korea) How to cry (ミヌ盤) <初回限定盤>(LTD) TS1P5005 Single K-POP 602 https://tower.jp/item/4415958 100% (Korea) How to cry (ロクヒョン盤) <初回限定盤>(LTD) TS1P5006 Single K-POP 602 https://tower.jp/item/4415970 100% (Korea) How to cry (ジョンファン盤) <初回限定盤>(LTD) TS1P5007 Single K-POP 602 https://tower.jp/item/4415972 100% (Korea) How to cry (チャンヨン盤) <初回限定盤>(LTD) TS1P5008 Single K-POP 602 https://tower.jp/item/4415974 100% (Korea) How to cry (ヒョクジン盤) <初回限定盤>(LTD) TS1P5009 Single K-POP 602 https://tower.jp/item/4415976 100% (Korea) Song for you (A) OKCK5011 Single K-POP 1,204 https://tower.jp/item/4655024 100% (Korea) Song for you (B) OKCK5012 Single K-POP 1,204 https://tower.jp/item/4655026 100% (Korea) Song for you (C) OKCK5013 Single K-POP 1,204 https://tower.jp/item/4655027 100% (Korea) Song for you メンバー別ジャケット盤 (ロクヒョン)(LTD) OKCK5015 Single K-POP 602 https://tower.jp/item/4655029 100% (Korea) Song for you メンバー別ジャケット盤 (ジョンファン)(LTD) OKCK5016 Single K-POP 602 https://tower.jp/item/4655032 100% (Korea) Song for you メンバー別ジャケット盤 (チャンヨン)(LTD) OKCK5017 Single K-POP 602 https://tower.jp/item/4655033