For Personal Use Only Use Personal For

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

June 2019 42

y 4 6 Equit 2019 June High Conviction High Quarterly NewsletterQuarterly No. Selector Fund In this quarterly edition, we review performance and attribution for the quarter. We highlight the importance of innovation and culture within organisations and profile ResMed and Cochlear, two leading healthcare businesses. We visit Fisher & Paykel Healthcare in New Zealand and look at one of the biggest growth industries in the world today, cyber security. Photo. Selector analyst trekking through the Atlas Mountains and local Berber kids. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 8, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au P Selector is a boutique fund manager. Our team, combined, have over 150 years of experience in financial markets. We believe in long-term wealth creation and building lasting relationships with our investors. We focus on stock selection, the funds are high conviction, concentrated and index unaware. As a result, the portfolios have low turnover and produce tax effective returns. Selector has a 15-year track record of outperformance and we continue to seek businesses with leadership qualities, run by competent management teams, underpinned by strong balance sheets and with a focus on capital management. Selector High Conviction Equity Fund Quarterly Newsletter #64 CONTENTS IN BRIEF – JUNE QUARTER 3 PORTFOLIO OVERVIEW 5 PORTFOLIO CONTRIBUTORS 7 MARKET INSIGHTS AND OBSERVATIONS 13 INNOVATION + CULTURE = SUCCESS 17 RESMED INC. 20 WAKE-UP CALL 31 FISHER & PAYKEL HEALTHCARE – JUNE 2019 42 RISK OUT…UPFRONT 45 COMPANY VISIT DIARY – JUNE 2019 QUARTER 57 2 Selector Funds Management IN BRIEF – JUNE QUARTER Dear Investor, Looking back on 2019, it would be fair to say that few identify the businesses we want to own on a case by case foresaw how the events of the financial year would basis, understand them to the best of our abilities and unfold. -

Australian Investment Strategy

2 November 2016 Asia Pacific/Australia Equity Research Investment Strategy Australian Investment Strategy Research Analysts STRATEGY Hasan Tevfik ,CFA 61 2 8205 4284 [email protected] Aussie darlings Peter Liu 61 2 8205 4071 ■ Aussies love their darlings: Australia currently has the most expensive [email protected] equity market "Darlings" in the world. Our darlings trade on a forward P/E Damien Boey of 38x. The other commodity-focused market, Canada, has the second 61 2 8205 4615 [email protected] most expensive darlings. Darlings in Australia have been more expensive only during the Nasdaq bubble when they touched 45x. ■ Darling derating: Buying Australian darlings at these valuations has been a poor strategy in the past. Also, the current high valuation for Australia's darlings suggest they are especially vulnerable to rising bond yields and the coming end of the Australian profits recession. A rising discount rate and a lower premium for growth suggest investors should focus on stocks that could be future darlings. ■ Hello Daaarling: Future market darlings have shared many similar characteristics over the last 20 years. They are generally well managed, have strong balance sheets and operate on high margins. Our "Hello Daaarling" strategy highlights potential future darlings and they currently trade on just 17x P/E and include Caltex, Eclipx, Mayne Pharma, Nufarm, Star Entertainment and South 32. We add Eclipx to our long Portfolio. Figure 1: Australia has the most expensive darlings in the world Median 12-month forward P/E of "market darlings" around the world* 40 35 30 25 20 15 10 Australia Canada Cont. -

Participant List

PARTICIPANT LIST Please find below a list of current participants in the Quarterly Salary Review. For a complete list by super sector, sector and segment refer to Mercer WIN®. 3M Australia API 7-Eleven Stores API Management A Menarini Australia APL Co. (Aus) - BR A.P.Moller-Maersk AS (AU) Apotex Abbott Australasia APT Management Services (APA Group) AbbVie Aquila Resources Actelion Pharmaceuticals Australia Arrium Mining & Materials Adama Australia Arrow Electronics Australia Adelaide Brighton Asahi Beverages Australia Adelaide Football Club Asaleo Care Australia adidas Australia Ascendas Hospitality Australia Fund Management Adventist Healthcare Aspen Australia AECOM Astrazeneca Afton Chemical Asia Pacific LLC AT & T Global Network Services Australia Aggreko Australia ATCO Australia AIA Australia Atlas Iron Aimia Proprietary Loyalty Australia Ausenco Air New Zealand – Australia AusGroup Akzo Nobel Australia Australia Post Alcatel-Lucent Australia Australian Catholic University Alcon (Novartis) Laboratories Australia Australian Computer Society Alexion Australasia Australian Fashion Labels Allergan Australian Red Cross Blood Service Alphapharm Avaloq Australia Alstom Transport Australia Aveo Group Amadeus IT Pacific Aviall Australia American Express Global Business Travel Australia AVJennings Holdings Amgen Australia Avon Products AMT Group BaptistCare NSW & ACT Amway of Australia Barminco Apex Tool Group BASF Australia © March 2017 Mercer Consulting (Australia) Pty Ltd Quarterly Salary Review 4.1 PARTICIPANT LIST Beam Global Australia -

Smallco Investment Fund

Smallco Investment Fund Quarterly Update 30 September 2014 SIF Portfolio Commentary SIF Performance Smallco Investment Fund (SIF) delivered 6.8% during the Return to 30 September 2014 September quarter and for the 12 months was up a solid 12.3%. During the quarter Iress, Isentia Group and Sirtex 3 months 6.8% Medical performed positively, while Carsales.com, Ozforex 1 year 12.3% Group and Macquarie Atlas Roads were negative 3 year p.a. 36.4% contributors. 5 year p.a. 22.5% For the September quarter the Small Ordinaries index was 10 year p.a. 13.6% modestly positive at 1.5% while for the year to 30 Since inception (31.10.00) p.a. 14.2% September it was down -0.1%. Value of $100,000 invested at inception $631,173 In general the Australian market had a solid reporting Fund returns calculated after all fees and expenses and based season and that was reflected in share prices during upon exit price and reinvestment of distributions. August, particularly for Industrial companies. However, towards the end of the quarter, the Australian and international markets became concerned about global political tensions – Ukraine, Iraq and Hong Kong – with a falling iron ore price having a significant negative impact on the Australian resources index. SIF Structure: by sector (look through) One of our major holdings is IRESS (IRE). SIF originally invested in IRE in 2002 when it had a market capitalisation of $260m. At the time we invested it was already the dominant provider of information systems to the professional equity market in Australia and New Zealand (ANZ). -

Content/Dam/Mercer/Attachments/Asia

Participant profile List of contributors The following 370 organisations contributed to the 2020 Australian Benefits Review. 3M Australia Aquila Resources 7-Eleven Aristocrat Technologies Australia A. Menarini Australia Arrow Electronics Australia Abbott Australasia ARTC AbbVie Ascender Accenture Australia* Aspen Australia Acrux DDS Astellas Pharma Australia ADCO Constructions Astrazeneca Adelaide Brighton AT&T Global Network Services Australia* Adobe Systems Australia* ATCO Australia AECOM Australia Aurizon Holdings Agilent Technologies Ausenco AGL AusGroup AIA Australia Australian Premium Iron Management Akamai Technologies Netherlands Australian Turf Club Alliance Mineral Asset Autodesk* Alliance Mining Commodities AVJennings Amazon* B. Braun Australia AMD Australia* B. Braun Avitum Amdocs Australia* Baker McKenzie Amgen Australia Bausch and Lomb Amway Of Australia Baxter Healthcare APA Group Bayer Apple* Bechtel Australia 2.14 Australian Benefits Review © 2020 Mercer Consulting (Australia) Pty Ltd Participant profile Becton Dickinson Celine Australia* beIN Media Group CenturyLink Technology Australia Besins Healthcare Christian Dior Australia* Biogen Church & Dwight BIS Industries Cipla Bluewaters Power 2 Cisco Systems Australia* Bluewaters Power Services Citrix* Boehringer Ingelheim Clean TeQ Bolton Clarke Cleanaway Boston Scientific Clough Projects Bouygues Construction Australia CNH Industrial Bowen and Pomeroy Cochlear BP Australia Colgate-Palmolive* Brisbane City Council Collins Foods Bristol-Myers Squibb Computershare British -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Australian Technology, Media & Telecom

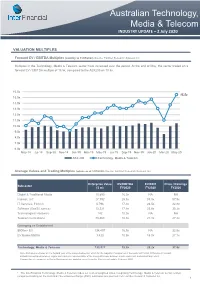

Australian Technology, Media & Telecom INDUSTRY UPDATE – 2 July 2020 VALUATION MULTIPLES Forward EV / EBITDA Multiples (monthly to 31/05/2020) Source: FactSet Research Systems Inc. Multiples in the Technology, Media & Telecom sector have increased over the period. At the end of May, the sector traded on a forward EV / EBITDA multiple of 15.5x, compared to the ASX200 on 10.5x. 16.0x 15.5x 15.0x 14.0x 13.0x 12.0x 11.0x 10.0x 9.0x 8.0x 7.0x 6.0x May-18 Jul-18 Sep-18 Nov-18 Jan-19 Mar-19 May-19 Jul-19 Sep-19 Nov-19 Jan-20 Mar-20 May-20 ASX 200 Technology, Media & Telecom Average Values and Trading Multiples (values as at 1/07/2020) Source: FactSet Research Systems Inc. Enterprise Value EV/EBITDA EV/EBIT Price / Earnings Subsector ($ m) FY2020 FY2020 FY2020 Digital & Traditional Media 10,890 16.9x NA NA Internet, IoT 27,792 25.3x 33.3x 57.9x IT Services, Fintech 5,796 17.3x 24.5x 32.8x Software (SaaS/Licence) 13,221 17.9x 23.9x 35.2x Technological Hardware 142 10.0x NA NA Telecommunications 73,468 10.3x 21.1x 27.2x Emerging vs Established $500m+ EV 134,497 16.9x NA 32.9x EV Below $500m 1,420 10.9x 15.0x 27.7x Technology, Media & Telecom 135,917 15.5x 29.2x 31.8x Note: Multiples are based on the forward year of the unreported period, which for the majority of companies in the sector is FY2020. Difference in forward EV/EBITDA multiples between Figure and Table are representative of the timing difference between month-end result, and current day result. -

Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 3, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612

2 2 nd nd Fu No.3 201 Ex 50 50 Ex Aust Equities Aust Quarterly Newsletter Quarterly December Selector In this quarterly edition we review performance and attribution. We review and share some of our macro thoughts on energy, interest rates and bank regulation. Finally we focus on health insurance specialist NIB. Photo: An ACT Fire and Rescue team. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 3, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au About Selector We are a boutique fund manager and we have a combined experience of over 60 years. We believe in long term wealth creation and building lasting relationships with our investors. Our focus is stock selection. Our funds are high conviction, concentrated and index unaware. As a result we have low turnover and produce tax effective returns. First we identify the best business franchises with the best management teams. Then we focus on valuations. When we arrive at work each day we are reminded that; “The art of successful investment is the patient investor taking money from the impatient investor”. Our fund is open to new subscriptions. Please forward to us contact details if you would like future newsletters to be emailed to family, friends or business colleagues. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 3, 10 Bridge Street Sydney NSW 2000, Australia Telephone 612 8090 3612 Web www.selectorfund.com.au December 2012 Selector Australian Equities Fund Quarterly Newsletter #32 Dear Investor, This time last year the world was in turmoil. -

Stoxx® Australia 150 Index

STOXX® AUSTRALIA 150 INDEX Components1 Company Supersector Country Weight (%) Commonwealth Bank of Australia Banks Australia 8.37 CSL Ltd. Health Care Australia 7.46 BHP GROUP LTD. Basic Resources Australia 7.23 National Australia Bank Ltd. Banks Australia 4.37 Westpac Banking Corp. Banks Australia 4.09 Australia & New Zealand Bankin Banks Australia 3.75 Wesfarmers Ltd. Retail Australia 3.30 WOOLWORTHS GROUP Personal Care, Drug & Grocery Australia 2.87 Macquarie Group Ltd. Financial Services Australia 2.84 Rio Tinto Ltd. Basic Resources Australia 2.48 Fortescue Metals Group Ltd. Basic Resources Australia 2.27 Transurban Group Industrial Goods & Services Australia 2.20 Telstra Corp. Ltd. Telecommunications Australia 2.05 Goodman Group Real Estate Australia 1.77 AFTERPAY Industrial Goods & Services Australia 1.54 Coles Group Personal Care, Drug & Grocery Australia 1.39 Woodside Petroleum Ltd. Energy Australia 1.28 Newcrest Mining Ltd. Basic Resources Australia 1.27 Aristocrat Leisure Ltd. Travel & Leisure Australia 1.11 XERO Technology Australia 1.00 SYDNEY AIRPORT Industrial Goods & Services Australia 0.93 Brambles Ltd. Industrial Goods & Services Australia 0.91 Sonic Healthcare Ltd. Health Care Australia 0.90 ASX Ltd. Financial Services Australia 0.82 SCENTRE GROUP Real Estate Australia 0.80 Cochlear Ltd. Health Care Australia 0.74 QBE Insurance Group Ltd. Insurance Australia 0.73 SUNCORP GROUP LTD. Insurance Australia 0.71 South32 Australia Basic Resources Australia 0.71 Santos Ltd. Energy Australia 0.68 Ramsay Health Care Ltd. Health Care Australia 0.66 Insurance Australia Group Ltd. Insurance Australia 0.65 Mirvac Group Real Estate Australia 0.60 DEXUS Real Estate Australia 0.59 SEEK Ltd. -

Introduction

INTRODUCTION LIST OF CONTRIBUTORS (ALPHABETICALLY) 7-Eleven Stores Amcor A.P. MOLLER- MAERSK A/S AMEC Mining & Metals ABB Australia AMEC Oil & Gas Abbott Australasia Amgen Australia AbbVie Australia AMP Services Accolade Wines AMT Group Acrux DDS Amway of Australia Actavis Australia Anglican Retirement Villages Diocese of Sydney Actelion Pharmaceuticals ANL Container Line Adelaide Brighton APL Co Adidas Australia Apotex AECOM Australia APT Management Services (APA Group) Afton Chemical Asia Pacific Arch Wood Protection (Aust) AGC Arts Centre Melbourne AGL Energy ASC AIA Australia Ashland Hercules Water Technologies (Australia) Aimia Association of Professionals, Engineers, Scientists and Managers Australia Air Liquide Australia Astellas Pharma Alcon Laboratories Australia AstraZeneca Alfa Laval Australia ATCO Australia Alinta Servco (Alinta Energy) Aurora Energy Allergan Australia AUSCOAL Services Allianz Global Assistance Auscript Australasia Allied Mills Ausenco Alpha Flight Services Aussie Farmers Direct Alphapharm Aussie Home Loans Alstom Australand Property Group Ambulance Victoria Australian Agricultural Company © March 2013 Mercer Consulting (Australia) Pty Ltd Quarterly Salary Review 1.5 INTRODUCTION Australian Catholic University Billabong Australian Football League Biogen Idec Australia Australian Institute of Company Directors BioMerieux Australia Australian Nuclear Science and Technology Bio-Rad Laboratories Organistaion (ANSTO) Biota Holdings Australian Pharmaceutical Industries (Priceline, Soul Pattinson Chemist) BISSELL -

2005 State of the Health Funds Report

Private Health Insurance Ombudsman STATE OF THE HEALTH FUNDS REPORT 2005 (Relating to the financial year 2004-05) Report required by paragraph 82ZRC (ba) of the National Health Act 1953 i THE STATE OF THE HEALTH FUNDS – 2005 ___________________________________________________________________ FOREWORD I am pleased to present the second annual State of the Health Funds report relating to the financial year 2004/2005. The National Health Act requires the Private Health Insurance Ombudsman to publish this report after the end of each financial year, to provide comparative information on the performance and service delivery of all health funds during that financial year. The main aim of publishing the report is to give consumers some extra information to help them when making decisions about private health insurance. For existing fund members the report provides information that will assist them to compare the performance of their fund with all other health funds. For those considering taking out private health insurance it provides an indication of the services available from each fund and provides a comparison on some service and performance indicators at the fund level. In choosing the range of issues and performance information to include in this report, I have had to take account of the availability of reliable data and whether the information is reasonably comparable across funds. Much of the information included in the report is based on data collected by the Private Health Insurance Administration Council as part of their role in statistical reporting and monitoring the financial management of health funds. Some additional data has been gathered from the funds but I have sought to keep the extra administrative burden for funds to a minimal level, so as not to contribute to undue extra administration costs.