G021 Microeconomics Lecture Notes Ian Preston

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Budgetary Effects of the Raise the Wage Act of 2021 February 2021

The Budgetary Effects of the Raise the Wage Act of 2021 FEBRUARY 2021 If enacted at the end of March 2021, the Raise the Wage Act of 2021 (S. 53, as introduced on January 26, 2021) would raise the federal minimum wage, in annual increments, to $15 per hour by June 2025 and then adjust it to increase at the same rate as median hourly wages. In this report, the Congressional Budget Office estimates the bill’s effects on the federal budget. The cumulative budget deficit over the 2021–2031 period would increase by $54 billion. Increases in annual deficits would be smaller before 2025, as the minimum-wage increases were being phased in, than in later years. Higher prices for goods and services—stemming from the higher wages of workers paid at or near the minimum wage, such as those providing long-term health care—would contribute to increases in federal spending. Changes in employment and in the distribution of income would increase spending for some programs (such as unemployment compensation), reduce spending for others (such as nutrition programs), and boost federal revenues (on net). Those estimates are consistent with CBO’s conventional approach to estimating the costs of legislation. In particular, they incorporate the assumption that nominal gross domestic product (GDP) would be unchanged. As a result, total income is roughly unchanged. Also, the deficit estimate presented above does not include increases in net outlays for interest on federal debt (as projected under current law) that would stem from the estimated effects of higher interest rates and changes in inflation under the bill. -

Social Sciences: Achievements and Prospects Journal 3(11), 2019

Social Sciences: Achievements and Prospects Journal 3(11), 2019 Contents lists available at ScienceCite Index Social Sciences: Achievements and Prospects Journal journal homepage: http://scopuseu.com/scopus/index.php/ssap/index What are the differences between the study of Micro Economics and Macro Economics and how are they interrelated with regard to the drafting of economic policies to remain current and relevant to the global economic environment Azizjon Akromov 1, Mushtariybegim Azlarova 2, Bobur Mamataliev 2, Azimkhon Koriev 2 1 Student MDIST 2 Students Tashkent State University Economic ARTICLE INFO ABSTRACT Article history: As economics is mostly known for being a social science, studying production, Received consumption, distribution of goods and services, its primary goal is to care about Accepted wellbeing of its society, which includes firms, people, and so forth. The study of Available online economics mainly consists of its two crucial components, which are Keywords: microeconomics and macroeconomics. Together these main parts of economics are concerned with both private and public sector issues including, inflation, economic Macroeconomics, growth, choices, demand and supply, production, income, unemployment and many microeconomics, other aspects. It is already mentioned that wellbeing of society would be indicators, production, established when government, while making economics policies, assume all factors consumers, companies, including those people who are employed or unemployed, so that no one gets hurt economics, government or suffer in the end. When it comes to making economic decisions and policies, governments should take into consideration that decisions made on a macro level has huge impact on micro and the same with micro, firms, households, individuals’ behaviors and choices come as aggregate in total, then turns into macro level, which triggers the introduction of some policies. -

Macroeconomics Course Outline and Syllabus

City University of New York (CUNY) CUNY Academic Works Open Educational Resources New York City College of Technology 2018 Macroeconomics Course Outline and Syllabus Sean P. MacDonald CUNY New York City College of Technology How does access to this work benefit ou?y Let us know! More information about this work at: https://academicworks.cuny.edu/ny_oers/8 Discover additional works at: https://academicworks.cuny.edu This work is made publicly available by the City University of New York (CUNY). Contact: [email protected] COURSE OUTLINE FOR ECON 1101 – MACROECONOMICS New York City College of Technology Social Science Department COURSE CODE: 1101 TITLE: Macroeconomics Class Hours: 3, Credits: 3 COURSE DESCRIPTION: Fundamental economic ideas and the operation of the economy on a national scale. Production, distribution and consumption of goods and services, the exchange process, the role of government, the national income and its distribution, GDP, consumption function, savings function, investment spending, the multiplier principle and the influence of government spending on income and output. Analysis of monetary policy, including the banking system and the Federal Reserve System. COURSE PREREQUISITE: CUNY proficiency in reading and writing RECOMMENDED TEXTBOOK and MATERIALS* Krugman and Wells, Eds., Macroeconomics 3rd. ed, Worth Publishers, 2012 Leeds, Michael A., von Allmen, Peter and Schiming, Richard C., Macroeconomics, Pearson Education, Inc., 2006 Supplemental Reading (optional, but informative): Krugman, Paul, End This Depression -

Journal of Econometrics Consumption and Labor Supply

Journal of Econometrics 147 (2008) 326–335 Contents lists available at ScienceDirect Journal of Econometrics journal homepage: www.elsevier.com/locate/jeconom Consumption and labor supply Dale W. Jorgenson a,∗, Daniel T. Slesnick b a Department of Economics, Harvard University, Cambridge, MA 02138, United States b Department of Economics, University of Texas, Austin, TX 78712, United States article info a b s t r a c t Article history: We present a new econometric model of aggregate demand and labor supply for the United States. Available online 16 September 2008 We also analyze the allocation full wealth among time periods for households distinguished by a variety of demographic characteristics. The model is estimated using micro-level data from the Consumer JEL classification: Expenditure Surveys supplemented with price information obtained from the Consumer Price Index. An C81 important feature of our approach is that aggregate demands and labor supply can be represented in D12 D91 closed form while accounting for the substantial heterogeneity in behavior that is found in household- level data. As a result, we are able to explain the patterns of aggregate demand and labor supply in the Keywords: data despite using a parametrically parsimonious specification. Consumption ' 2008 Elsevier B.V. All rights reserved. Leisure Labor Demand Supply Wages 1. Introduction employed, we impute the opportunity wages they face using the wages earned by employees. The objective of this paper is to present a new econometric Cross-sectional variation of prices and wages is considerable model of aggregate consumer behavior for the United States. The and provides an important source of information about patterns model allocates full wealth among time periods for households of consumption and labor supply. -

Lecture 4 " Theory of Choice and Individual Demand

Lecture 4 - Theory of Choice and Individual Demand David Autor 14.03 Fall 2004 Agenda 1. Utility maximization 2. Indirect Utility function 3. Application: Gift giving –Waldfogel paper 4. Expenditure function 5. Relationship between Expenditure function and Indirect utility function 6. Demand functions 7. Application: Food stamps –Whitmore paper 8. Income and substitution e¤ects 9. Normal and inferior goods 10. Compensated and uncompensated demand (Hicksian, Marshallian) 11. Application: Gi¤en goods –Jensen and Miller paper Roadmap: 1 Axioms of consumer preference Primal Dual Max U(x,y) Min pxx+ pyy s.t. pxx+ pyy < I s.t. U(x,y) > U Indirect Utility function Expenditure function E*= E(p , p , U) U*= V(px, py, I) x y Marshallian demand Hicksian demand X = d (p , p , I) = x x y X = hx(px, py, U) = (by Roy’s identity) (by Shepard’s lemma) ¶V / ¶p ¶ E - x - ¶V / ¶I Slutsky equation ¶p x 1 Theory of consumer choice 1.1 Utility maximization subject to budget constraint Ingredients: Utility function (preferences) Budget constraint Price vector Consumer’sproblem Maximize utility subjet to budget constraint Characteristics of solution: Budget exhaustion (non-satiation) For most solutions: psychic tradeo¤ = monetary payo¤ Psychic tradeo¤ is MRS Monetary tradeo¤ is the price ratio 2 From a visual point of view utility maximization corresponds to the following point: (Note that the slope of the budget set is equal to px ) py Graph 35 y IC3 IC2 IC1 B C A D x What’swrong with some of these points? We can see that A P B, A I D, C P A. -

Preview Guide

ContentsNOT FOR SALE Preface xiii CHAPTER 3 The Behavior of Consumers 45 3.1 Tastes 45 CHAPTER 1 Indifference Curves 45 Supply, Demand, Marginal Values 48 and Equilibrium 1 More on Indifference Curves 53 1.1 Demand 1 3.2 The Budget Line and the Demand versus Quantity Consumer’s Choice 53 Demanded 1 The Budget Line 54 Demand Curves 2 The Consumer’s Choice 56 Changes in Demand 3 Market Demand 7 3.3 Applications of Indifference The Shape of the Demand Curve 7 Curves 59 The Wide Scope of Economics 10 Standards of Living 59 The Least Bad Tax 64 1.2 Supply 10 Summary 69 Supply versus Quantity Supplied 10 Author Commentary 69 1.3 Equilibrium 13 Review Questions 70 The Equilibrium Point 13 Numerical Exercises 70 Changes in the Equilibrium Point 15 Problem Set 71 Summary 23 Appendix to Chapter 3 77 Author Commentary 24 Cardinal Utility 77 Review Questions 25 The Consumer’s Optimum 79 Numerical Exercises 25 Problem Set 26 CHAPTER 4 Consumers in the Marketplace 81 CHAPTER 2 4.1 Changes in Income 81 Prices, Costs, and the Gains Changes in Income and Changes in the from Trade 31 Budget Line 81 Changes in Income and Changes in the 2.1 Prices 31 Optimum Point 82 Absolute versus Relative Prices 32 The Engel Curve 84 Some Applications 34 4.2 Changes in Price 85 2.2 Costs, Efficiency, and Gains from Changes in Price and Changes in the Trade 35 Budget Line 85 Costs and Efficiency 35 Changes in Price and Changes in the Optimum Point 86 Specialization and the Gains from Trade 37 The Demand Curve 88 Why People Trade 39 4.3 Income and Substitution Summary 41 -

What Role Does Consumer Sentiment Play in the U.S. Economy?

The economy is mired in recession. Consumer spending is weak, investment in plant and equipment is lethargic, and firms are hesitant to hire unemployed workers, given bleak forecasts of demand for final products. Monetary policy has lowered short-term interest rates and long rates have followed suit, but consumers and businesses resist borrowing. The condi- tions seem ripe for a recovery, but still the economy has not taken off as expected. What is the missing ingredient? Consumer confidence. Once the mood of consumers shifts toward the optimistic, shoppers will buy, firms will hire, and the engine of growth will rev up again. All eyes are on the widely publicized measures of consumer confidence (or consumer sentiment), waiting for the telltale uptick that will propel us into the longed-for expansion. Just as we appear to be headed for a "double-dipper," the mood swing occurs: the indexes of consumer confi- dence register 20-point increases, and the nation surges into a prolonged period of healthy growth. oes the U.S. economy really behave as this fictional account describes? Can a shift in sentiment drive the economy out of D recession and back into good health? Does a lack of consumer confidence drag the economy into recession? What causes large swings in consumer confidence? This article will try to answer these questions and to determine consumer confidence’s role in the workings of the U.S. economy. ]effre9 C. Fuhrer I. What Is Consumer Sentitnent? Senior Econotnist, Federal Reserve Consumer sentiment, or consumer confidence, is both an economic Bank of Boston. -

Demand Composition and the Strength of Recoveries†

Demand Composition and the Strength of Recoveriesy Martin Beraja Christian K. Wolf MIT & NBER MIT & NBER September 17, 2021 Abstract: We argue that recoveries from demand-driven recessions with ex- penditure cuts concentrated in services or non-durables will tend to be weaker than recoveries from recessions more biased towards durables. Intuitively, the smaller the bias towards more durable goods, the less the recovery is buffeted by pent-up demand. We show that, in a standard multi-sector business-cycle model, this prediction holds if and only if, following an aggregate demand shock to all categories of spending (e.g., a monetary shock), expenditure on more durable goods reverts back faster. This testable condition receives ample support in U.S. data. We then use (i) a semi-structural shift-share and (ii) a structural model to quantify this effect of varying demand composition on recovery dynamics, and find it to be large. We also discuss implications for optimal stabilization policy. Keywords: durables, services, demand recessions, pent-up demand, shift-share design, recov- ery dynamics, COVID-19. JEL codes: E32, E52 yEmail: [email protected] and [email protected]. We received helpful comments from George-Marios Angeletos, Gadi Barlevy, Florin Bilbiie, Ricardo Caballero, Lawrence Christiano, Martin Eichenbaum, Fran¸coisGourio, Basile Grassi, Erik Hurst, Greg Kaplan, Andrea Lanteri, Jennifer La'O, Alisdair McKay, Simon Mongey, Ernesto Pasten, Matt Rognlie, Alp Simsek, Ludwig Straub, Silvana Tenreyro, Nicholas Tra- chter, Gianluca Violante, Iv´anWerning, Johannes Wieland (our discussant), Tom Winberry, Nathan Zorzi and seminar participants at various venues, and we thank Isabel Di Tella for outstanding research assistance. -

Indifference Curves

Lecture # 8 – Consumer Behavior: An Introduction to the Concept of Utility I. Utility -- A Description of Preferences • Our goal is to come up with a model that describes consumer behavior. To begin, we need a way to describe preferences. Economists use utility to do this. • Utility is the level of satisfaction that a person gets from consuming a good or undertaking an activity. o It is the relative ranking, not the actual number, that matters. • Marginal utility is the satisfaction obtained from consuming an additional amount of a good. It is the change in total utility resulting from a one-unit change in product. o Marginal utility diminishes (gets smaller) as you consume more of a good (the fifth ice cream cone isn't as desirable as the first). o However, as long as marginal utility is positive, total utility will increase! II. Mapping Preferences -- Indifference Curves • Since economics is about allocating scarce resources -- that is, asking what choices people make when faced with limited resources -- looking at utility for a single good is not enough. We want to compare utility for different combinations of two or more goods. • Our goal is to be able to graph the utility received from a combination of two goods with a two-dimensional diagram. We do this using indifference curves. • An indifference curve represents all combinations of goods that produce the same level of satisfaction to a person. o Along an indifference curve, utility is constant. o Remember that each curve is analogous to a line on a contour map, where each line shows a different elevation. -

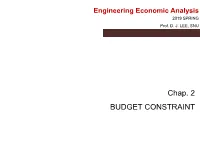

2. Budget Constraint.Pdf

Engineering Economic Analysis 2019 SPRING Prof. D. J. LEE, SNU Chap. 2 BUDGET CONSTRAINT Consumption Choice Sets . A consumption choice set, X, is the collection of all consumption choices available to the consumer. n X = R+ . A consumption bundle, x, containing x1 units of commodity 1, x2 units of commodity 2 and so on up to xn units of commodity n is denoted by the vector xx =(1 ,..., xn ) ∈ X n . Commodity price vector pp =(1 ,..., pn ) ∈R+ 1 Budget Constraints . Q: When is a bundle (x1, … , xn) affordable at prices p1, … , pn? • A: When p1x1 + … + pnxn ≤ m where m is the consumer’s (disposable) income. The consumer’s budget set is the set of all affordable bundles; B(p1, … , pn, m) = { (x1, … , xn) | x1 ≥ 0, … , xn ≥ 0 and p1x1 + … + pnxn ≤ m } . The budget constraint is the upper boundary of the budget set. p1x1 + … + pnxn = m 2 Budget Set and Constraint for Two Commodities x2 Budget constraint is m /p2 p1x1 + p2x2 = m. m /p1 x1 3 Budget Set and Constraint for Two Commodities x2 Budget constraint is m /p2 p1x1 + p2x2 = m. the collection of all affordable bundles. Budget p1x1 + p2x2 ≤ m. Set m /p1 x1 4 Budget Constraint for Three Commodities • If n = 3 x2 p1x1 + p2x2 + p3x3 = m m /p2 m /p3 x3 m /p1 x1 5 Budget Set for Three Commodities x 2 { (x1,x2,x3) | x1 ≥ 0, x2 ≥ 0, x3 ≥ 0 and m /p2 p1x1 + p2x2 + p3x3 ≤ m} m /p3 x3 m /p1 x1 6 Opportunity cost in Budget Constraints x2 p1x1 + p2x2 = m Slope is -p1/p2 a2 Opp. -

Decisions and Games

DECISIONS AND GAMES. PART I 1. Preference and choice 2. Demand theory 3. Uncertainty 4. Intertemporal decision making 5. Behavioral decision theory DECISIONS AND GAMES. PART II 6. Static Games of complete information 7. Dynamic games of complete information 8. Static games of incomplete information 9. Dynamic games of incomplete information 10. Behavioral game theory References Gibbons, R. 1992. Game theory for applied economists. Princeton University Press. Princeton, New Jersey. Varian, H.1992. Microeconomic analysis. Norton & Company. New York. Chapters 7, 8, 9, 10, 11, 19. Camerer, C. , Loewenstein, G. , and Rabin, M. 2004. Advances in Behavioral Economics. Princeton University Press. Mas-Colell, A., Whinston, M., and Green, J. 1995. Microeconomic theory. Oxford University Press. Chapters 1, 2, 3, 4, 6. 1 Two approaches to analyze behavior of decision makers. 1. From an abstract construction generate choices that satisfy rationality restrictions. 2. Directly from choice, ask for some structure to these choices and derive properties. Relation between the two approaches. 2 1. Preference and choice Consider a set of alternatives (mutually exclusives) X and we consider a preference relation on X. Preferences The preference relation “at least as good as” is a binary relation − over the set of alternatives X. Preferences express the ordering between alternatives resulting from the objectives of the decision maker. Properties: Rational Preference Relation (or Weak order, or Complete preorder) if -Completeness, Transitivity (and Reflexivity) A relation is complete if ∀∈x,,yXxy or yx. A relation is transitive if and only if ∀∈x,yz, X, if x≺≺y and y z, then x≺z. 3 Transitiveness is more delicate than completeness. -

The Indifference Curve Analysis - an Alternative Approach Represented by Odes Using Geogebra

The indifference curve analysis - An alternative approach represented by ODEs using GeoGebra Jorge Marques and Nuno Baeta CeBER and CISUC University of Coimbra June 26, 2018, Coimbra, Portugal 7th CADGME - Conference on Digital Tools in Mathematics Education Jorge Marques and Nuno Baeta The indifference curve analysis - An alternative approach represented by ODEs using GeoGebra Outline Summary 1 The neoclassic consumer model in Economics 2 2 Smooth Preferences on R+ Representation by a utility function Representation by the marginal rate of substitution 3 2 Characterization of Preferences Classes on R+ 4 Graphic Representation on GeoGebra Jorge Marques and Nuno Baeta The indifference curve analysis - An alternative approach represented by ODEs using GeoGebra The neoclassic consumer model in Economics Variables: Quantities and Prices N Let R+ = fx = (x1;:::; xN ): xi > 0g be the set of all bundles of N goods Xi , N ≥ 2, and Ω = fp = (p1;:::; pN ): pi > 0g be the set of all unit prices of Xi in the market. Constrained Maximization Problem The consumer is an economic agent who wants to maximize a utility function u(x) subject to the budget constraint pT x ≤ m, where m is their income. In fact, the combination of strict convex preferences with the budget constraint ensures that the ∗ ∗ problem has a unique solution, a bundle of goods x = (xi ) ∗ i such that xi = d (p1;:::; pN ; m). System of Demand Functions In this system quantities are taken as functions of their market prices and income. Jorge Marques and Nuno Baeta The indifference curve analysis - An alternative approach represented by ODEs using GeoGebra The neoclassic consumer model in Economics Economic Theory of Market Behavior However, a utility function has been regarded as unobservable in the sense of being beyond the limits of the economist’s knowledge.