Dormy Inn Hakata Gion)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mitsui Garden Hotel Fukuoka Gion to Open for Business on Thursday

June 18, 2019 For immediate release Mitsui Fudosan Co., Ltd. Mitsui Fudosan Hotel Management Co., Ltd. First Mitsui Garden Hotel in Fukuoka Mitsui Garden Hotel Fukuoka Gion to Open for Business on Thursday, June 27, 2019 A hotel where guests can experience new charm in Fukuoka with its modern arrangements of Hakata culture. Tokyo, Japan, June 18, 2019 – Mitsui Fudosan Co., Ltd., a leading global real estate company headquartered in Tokyo and Mitsui Fudosan Hotel Management Co., Ltd. announced today that Mitsui Garden Hotel Fukuoka Gion (300 guestrooms; 2-8-15, Hakataekimae, Hakata-ku, Fukuoka City, Fukuoka Prefecture) will open for business on Thursday, June 27, 2019. This will be the second facility in the Kyushu area after Mitsui Garden Hotel Kumamoto, and first to debut in Fukuoka Prefecture. Hakata is a bustling town at the center of Kyushu’s political, economic, and cultural landscape. JR Hakata Station serves as a chief station for Fukuoka City and a base for those traveling around Kyushu for leisure. There is a lot of activity around the station, which visitors often use during business trips and other excursions. Mitsui Garden Hotel Fukuoka Gion is only a few minutes away from JR Hakata Station and Gion Station on the Kuko Subway Line, located on the corner of Hakata Ekimae Dori and Gion Odori. It is also within walking distance of the Nakasu and Tenjin areas, making it a convenient and comfortable location to use as a base for leisure and business activities. The hotel was designed under the concept of “HAKATA TSUMUGI: Hakata townhouses that link memories of good old-fashioned towns, people, and culture to the future” so visitors can experience the region’s new charm. -

Fiscal Period Ended December 31, 2018

https://www.midcity-reit.com/en/ th Period INVESTOR PRESENTATION25– Appendix – Fiscal Period ended December 31, 2018 Securities Code 3227 * Fractions of the stated amounts are cut off and those of the ratios and years are rounded off unless otherwise indicated. Therefore, the aggregation of Index the figures stated hereupon are not necessarily identical to the total. 1. ABOUT MCUBS MidCity INVESTMENT CORPORATION 5. PORTFOLIO • Who We Are 4 • Portfolio profitability 39 • History 5 • Portfolio overview (as of the end of Dec. 2018) 40 • Mitsubishi Corp.-UBS Realty Inc. Group (MC-UBS Group) 6 • Portfolio data (as of the end of Dec. 2018) 1 41 • Investment Policy 7 • Portfolio data (as of the end of Dec. 2018) 2 42 • Track Record 8 • Revenue and expenses by property 1 (Fiscal period ended Dec. 31, 2018) 43 • Portfolio Summary 9 • Revenue and expenses by property 2 (Fiscal period ended Dec. 31, 2018) 44 • Office Portfolio: Comparison with other REITs 10 • Appraisal values by property 45 • Industry-leading acquisition capability 11 • Unrealized gain/loss 46 • Asset management with a focus on tenant satisfaction 12 • Portfolio map / Portfolio overview 47-56 • Stable financial base 13 6. FINANCING STRATEGY • ESG-conscious portfolio management 14 • Major financing-related figures and investment corporation bonds 58 2. FINANCIAL HIGHLIGHTS • Financial status 1 59 • Overview of financial results • Financial status 2 60 for the fiscal period ended December 31, 2018 (25th Period) 1 16 • Lender composition (as of the end of Dec. 2018) 61 • Overview of financial results • Outstanding borrowings (as of the end of Dec. 2018) 62 for the fiscal period ended December 31, 2018 (25th Period) 2 17 • Maturity ladder (as of the end of Dec. -

Investor Presentation -Appendix- (Ended Dec. 2017)

rd Period Fiscal Period23 ended December, 2017 * Fractions of the stated amounts are cut off and those of the ratios and years are rounded off unless otherwise indicated. Therefore, the aggregation of the figures Index stated hereupon are not necessarily identical to the total. 1. FINANCIAL HIGHLIGHTS • Portfolio overview - Office in Tokyo area 3 35 • Overview of financial results • Portfolio overview - Office in Osaka area 1 36 for the fiscal period ended December 31, 2017 (23rd Period) 4 • Portfolio overview - Office in Osaka area 2 37 • 23rd Period financial results – Comparison to previous period 5 • Portfolio overview - Office in Osaka, others and TK interest 38 • 23rd Period financial results – Comparison to initial forecasts 6 • Portfolio overview – Other than the office 39 • 23rd Period financial results – • Newly acquired assets 40 Breakdown of change from previous period 7 • Balance sheet 8 5. FINANCING STRATEGY • Income statement 9 • Major financing- related figures and investment corporation bonds 45 2. FORECASTS FOR THE 24TH AND 25TH FISCAL PERIOD • Financial status 46 • Forecasts for the 24th and 25th fiscal period 11 • Lender composition and maturity ladder (as of end of Dec. 2017) 47 • Breakdown of change from previous period 12 • Outstanding borrowings (as of end of Dec. 2017) 48 3. RESULTS FOR THE 23RD FISCAL PERIOD • Lender composition and maturity ladder (Estimate for Mar. 2018) 49 • Occupancy 14 • Outstanding borrowings (Estimate for Mar. 2018) 50 • Portfolio operation 15 6. MARKET ENVIRONMENT • Occupancy by property 16 • Office market data 1 (Tokyo 23 districts) 53 • Revisions and gaps in rents 17 • Office market data 2 (Tokyo 23 districts) 54 • Surveys on tenants’ satisfaction 18 • Office market data 3 (Osaka) 55 • Initiatives in Properties in the Portfolio 19 • Office market data 4 (Osaka) 56 4. -

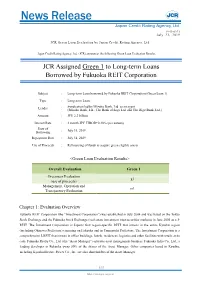

To Long-Term Loan Borrowed by Fukuoka REIT Corporation

19-D-0371 July 23, 2019 JCR Green Loan Evaluation by Japan Credit Rating Agency, Ltd. Japan Credit Rating Agency, Ltd. (JCR) announces the following Green Loan Evaluation Results. JCR Assigned Green 1 to Long-term Loans Borrowed by Fukuoka REIT Corporation Subject : Long-term Loan borrowed by Fukuoka REIT Corporation (Green Loan 1) Type : Long-term Loan Lender : Syndication led by Mizuho Bank, Ltd. as an agent (Mizuho Bank, Ltd., The Bank of Saga Ltd. and The Higo Bank, Ltd.) Amount : JPY 2.2 billion Interest Rate : 3 month JPY TIBOR+0.30% (per annum) Date of Borrowing : July 31, 2019 Repayment Date : July 31, 2029 Use of Proceeds : Refinancing of funds to acquire green eligible assets <Green Loan Evaluation Results> Overall Evaluation Green 1 Greenness Evaluation g1 (use of proceeds) Management, Operation and m1 Transparency Evaluation Chapter 1: Evaluation Overview Fukuoka REIT Corporation (the “Investment Corporation”) was established in July 2004 and was listed on the Tokyo Stock Exchange and the Fukuoka Stock Exchange (real estate investment trust securities markets) in June 2005 as a J- REIT. The Investment Corporation is Japan's first region-specific REIT that invests in the entire Kyushu region (including Okinawa Prefecture) centering on Fukuoka and in Yamaguchi Prefecture. The Investment Corporation is a comprehensive J-REIT that invests in office buildings, hotels, residences, logistics and other facilities with retails at its core. Fukuoka Realty Co., Ltd. (the “Asset Manager”) operates asset management business. Fukuoka Jisho Co., Ltd., a leading developer in Fukuoka owns 50% of the shares of the Asset Manager. Other companies based in Kyushu, including Kyushu Electric Power Co., Inc. -

The 27Th Fiscal Period Analyst Meeting Material Appendix (July 1, 2019 To

th Period INVESTOR PRESENTATION27- Appendix - Fiscal Period ended December 31, 2019 Securities Code 3227 https://www.midcity-reit.com/en/ * Fractions of the stated amounts are cut off and those of the ratios and years are rounded off unless otherwise indicated. Therefore, the aggregation of the figures Index stated hereupon are not necessarily identical to the total. 1. ABOUT MCUBS MidCity Investment Corporation • Who We Are 4 • Growth in existing property NOI 34 • History 5 • Revisions and gaps in rents 35 • The asset management company: • Diversification of tenant contract types 36 Mitsubishi Corp.- UBS Realty Inc. (MC-UBS) 6 • Appraisal value by property 37 • Investment policy 7 • Unrealized gain/loss 38 • Track record 8 • Portfolio data (as of the end of Dec. 2019) 39-40 • Portfolio summary 9 • Revenue and expenses by property • Portfolio comparison with other Office REITs 10 (Fiscal period ended Dec. 31, 2019) 41-42 • Industry-leading acquisition capability 11 • Portfolio map / Portfolio overview 43-53 • Selected investment utilizing MidCity’s advantage 12 • Acquired Properties 55-58 • Asset management with a focus on tenant satisfaction & Stable financial base 13 4. FINANCING STRATEGY • Major financing-related figures and investment corporation bonds 60 • ESG-conscious portfolio management 14 • Financial status 61-62 2. FINANCIAL HIGHLIGHTS & FORECASTS FOR THE 28TH AND 29TH PERIOD • Outstanding borrowings (as of the end of Jan. 2020) 63-64 • Overview of financial results • Lender composition (as of the end of Jan. 2020) 65 for the fiscal period ended Dec. 31, 2019 (27th Period) 16-17 • Maturity ladder (as of the end of Jan. 2020) 66 • 27th Period financial results – Comparison to previous period 18 th 5. -

Investor Presentation -Appendix- (Fiscal Period Ended June 30, 2019)

26 th Period INVESTOR PRESENTATION – Appendix – Fiscal Period ended June 30, 2019 Securities Code 3227 https://www.midcity-reit.com/en/ * Fractions of the stated amounts are cut off and those of the ratios and years are rounded off unless otherwise indicated. Therefore, the aggregation of the figures Index stated hereupon are not necessarily identical to the total. 1. ABOUT MCUBS MidCity Investment Corporation • Revisions and gaps in rents 35 • Who We Are 4 • Diversification of tenant contract types 36 • History 5 • Appraisal value by property 37 • The asset management company: • Unrealized gain/loss 38 Mitsubishi Corp.- UBS Realty Inc. (MC-UBS) 6 • Portfolio data (as of the end of Jun. 2019) 1 39 • Investment policy 7 • Portfolio data (as of the end of Jun. 2019) 2 40 • Track record 8 • Revenue and expenses by property 1 (Fiscal period ended Jun. 30, 2019) 41 • Portfolio summary 9 • Revenue and expenses by property 2 (Fiscal period ended Jun. 30, 2019) 42 • Portfolio comparison with other Office REITs 10 • Portfolio map / Portfolio overview 43-52 • Industry-leading acquisition capability 11 4. FINANCING STRATEGY • Selected investment utilizing MidCity’s advantage 12 • Major financing-related figures and investment corporation bonds 54 • Asset management with a focus on tenant satisfaction • Financial status 1 55 & Stable financial base 13 • Financial status 2 56 • ESG-conscious portfolio management 14 • Lender composition (as of the end of Jul. 2019) 57 2. FINANCIAL HIGHLIGHTS & FORECASTS FOR THE 27TH AND 28TH PERIOD • Outstanding borrowings (as of the end of Jul. 2019) 58 • Overview of financial results • Maturity ladder (as of the end of Jul. -

Mitsui Garden Hotel Fukuoka Gion (300 Rooms) Opening on June 27, 2019 Reservations Available from December 13, 2018

December 13, 2018 For immediate release Mitsui Fudosan Co., Ltd. Mitsui Fudosan Hotel Management Co., Ltd. Establishment of the First Mitsui Garden Hotel in Fukuoka Prefecture Mitsui Garden Hotel Fukuoka Gion (300 Rooms) Opening on June 27, 2019 Reservations available from December 13, 2018 Tokyo, Japan, December 13, 2018 - Mitsui Fudosan Co., Ltd., a leading global real estate company headquartered in Tokyo and Mitsui Fudosan Hotel Management Co., Ltd. announce that they have decided to commence operation of Mitsui Garden Hotel Fukuoka Gion, located at 2-chome Hakataekimae in the Hakata ward of Fukuoka City in Fukuoka Prefecture, on June 27, 2019. Reservations are available starting from Thursday, December 13, 2018. This hotel is seven minutes on foot from JR Hakata Station, and five minutes on foot from Gion Station on the Kuko Subway Line. It is also within walking distance of the Nakasu and Tenjin areas, placing it in a very convenient location for tourism and leisure. The hotel lobby and communal spaces such as the lounge, and guestrooms also have designs that evoke Hakata style, and the facility strives for guests from inside and outside Japan to visit and spend time in Hakata in comfort. Mitsui Fudosan Hotel Management currently operates a total of 25 facilities and 6,545 rooms across the country, with 6,041 rooms in 22 facilities throughout Japan under Mitsui Garden Hotels, its upper middle-class lodging-focused hotel brand, and 504 rooms in 3 facilities under THE CELESTINE HOTELS, its high-class lodging-focused hotel brand. This hotel will be the 27th facility continuing on from the Mitsui Garden Hotel Kanazawa (158 rooms) that will open for business on January 11, 2019, the second facility in the Kyushu area after Mitsui Garden Hotel Kumamoto (225 rooms) in the Chuo ward of Kumamoto City, and the first facility for Fukuoka Prefecture. -

Acquisition of Five Office Assets

Creating peace of mind through honest and committed management. [Provisional Translation Only] This English translation of the original Japanese document is provided solely for information purposes. Should there be any discrepancies between this translation and the Japanese original, the latter shall prevail. April 8, 2016 REIT Issuer Ichigo Office REIT Investment Corporation (8975) 1-1-1 Uchisaiwaicho, Chiyoda-ku, Tokyo Representative: Yoshihiro Takatsuka, Executive Director www.ichigo-office.co.jp/english Asset Management Company Ichigo Real Estate Investment Advisors Co., Ltd. Representative: Wataru Orii, President & Representative Statutory Executive Officer Inquiries: Hiroto Tajitsu, Head of Administration & Statutory Executive Officer Tel: +81-3-3502-4891 Acquisition of Five Office Assets Ichigo Real Estate Investment Advisors Co., Ltd. (IRE), the asset management company of Ichigo Office REIT Investment Corporation (“Ichigo Office REIT”), has decided to acquire five assets (total acquisition price 8,370,000,000 yen). I. Acquisition Summary Total appraisal value: 8,730,000,000 yen, total acquisition price: 8,370,000,000 yen O-72 O-73 O-74 O-75 O-76 Ichigo Shibuya Ichigo Ichigo Nishi Ichigo Hakata Nishiki First Asset Name1 East Building Ningyocho Honmachi Building Building Building Building Asset Type Office Office Office Office Office Date Built October 1985 March 1984 October 1990 April 1989 October 1984 Trust beneficiary Trust beneficiary Trust beneficiary Trust beneficiary Trust beneficiary Legal Form of interest in real interest -

Asset Acquisitions, New Loans, and New Subsidiary Consolidations

Creating peace of mind through honest and committed management. [Provisional Translation Only] This English translation of the original Japanese document is provided solely for information purposes. Should there be any discrepancies between this translation and the Japanese original, the latter shall prevail. July 28, 2015 Ichigo Group Holdings Co., Ltd. (JASDAQ, 2337) Representative: Scott Callon, Chairman and Representative Statutory Executive Officer Inquiries: Takeyuki Yoshimatsu, Senior Statutory Executive Officer Telephone: +81-3-3502-4818 www.ichigo-holdings.co.jp/english Asset Acquisitions, New Loans, and New Subsidiary Consolidations Ichigo Group Holdings (“Ichigo”) decided today to acquire twenty-four office assets, financed primarily via new loans, and the special purpose companies (“SPCs”) created for the acquisitions will become Ichigo’s consolidated subsidiaries. 1. Purpose of the Acquisitions Ichigo is driving greater synergies between its asset management and value-add businesses. In support of full achievement of its Shift Up 2016 Mid-Term Business Plan, via today’s acquisitions Ichigo is acquiring high-quality assets to expand its stable earnings base and further increase its capital efficiency via the growth of its asset management business. In today’s transactions, Ichigo is investing jointly with Ichigo REIT (8975) in two SPCs, Motoazabu Holdings GK Tokumei Kumiai (TK) (“Motoazabu TK”) and Ikenohata Holdings GK Tokumei Kumiai (TK) (“Ikenohata TK”), while it is the sole investor in a third SPC, Kichijoji GK Tokumei Kumiai (TK) (“Kichijoji TK” and collectively, the “TKs”). As described in section 3 below, the TKs are being established today and in the next two days Ichigo will invest in and become the majority investor in all three TKs, at which point all three TKs will become Ichigo’s consolidated subsidiaries. -

Nippon Building Fund, Inc. Sadafumi Abe, Executive Director (TSE Code : 8951) Contact: Asset Management Company Nippon Building Fund Management, Ltd

January 31, 2011 To All Concerned Parties Name of REIT Issuer: Nippon Building Fund, Inc. Sadafumi Abe, Executive Director (TSE Code : 8951) Contact: Asset Management Company Nippon Building Fund Management, Ltd. Koichi Nishiyama, President and CEO Person to Contact: Yasushi Akimoto, General Manager (TEL. +81-3-6259-8681) Notice of Acquisition of Assets (River City M-SQUARE and 4 Other Properties) Nippon Building Fund, Inc. (“NBF”) hereby provides notice of its decision on January 11, 2011 to acquire assets as follows: Description 1. Outline of Acquisition 1) Acquired assets; names of assets; acquisition prices NO. Acquired Name of Assets Acquisition Price Assets (*1) I. Real Property River City M-SQUARE ¥ 13,350,000,000 II. 〃 Nihonbashi Kabuto-cho M-SQUARE ¥ 4,850,000,000 III. 〃 Hakata Gion M-SQUARE ¥ 8,000,000,000 IV. 〃 Gate City Ohsaki (Additional Acquisition) (*2) ¥ 11,650,000,000 V. 〃 Chofu South Gate Bldg. ¥ 9,320,000,000 Total ¥ 47,170,000,000 *1 Miscellaneous acquisition costs, fixed assets tax, city-planning tax and consumption tax etc. are not included in this amount. *2 The sale and purchase price (the total amount of the acquisition price and the reserve for repairs) for the Gate City Ohsaki (additional acquisition) is ¥12 billion. Since the amount of the reserve for repairs as of the anticipated date of transfer is yet to be confirmed, the acquisition price is not fixed at present. Therefore, the anticipated acquisition price for this property is an approximate estimate. Note: This document constitutes a general announcement to the press concerning NBF’s acquisition of assets and 1 is not intended to solicit investment from investors. -

Overview of the 31St Fiscal Period Performance

Security code Overview of the 31st fiscal period performance[8968]September 1st,2019~February 29th,2020 Topics of the 31st fiscal period or later 1 New Acquisition properties [scheduled] 3 Financial statements 7 Business forecasts 9 Portfolio overview 11 Financial strategy 18 Appraisal value 21 Situation of Fukuoka and Kyushu 23 Sustainability 27 Appendix 28 *Regarding rounding of amounts, percentage, and ratios : unless otherwise noted, in these materials, monetary amounts are rounded down to the nearest whole unit, and percentages and ratios are rounded off to one decimal places. These materials may contain future performance, plans, st Overview of the 31 fiscal period performance management targets and strategies. These forward-looking descriptions are based on present assumptions on future events [Security code ]September 1st,2019~February 29th,2020 and trends in the business environment, but such assumptions 8968 may not necessarily be accurate. Actual results may differ mate- rially due to various factors. Neither Fukuoka REIT Corporation nor Fukuoka Realty shall be liable for the accuracy, rationality and completeness of information contained in these materials, whether they were prepared by Fukuoka REIT Corporation or Fukuoka Realty or provided by a third party. These materials have not been prepared to entice investment. When applying to purchase investment units issued by Fukuoka REIT Corporation, do so based on your own judgment and responsibility. Topics of the 31st fiscal period or later Owned properties [The 31st FP] New acquisition properties [The 32nd FP] ◎Retail ◎Two new properties to be acquired in the 32nd fiscal period [total: 4,990 million yen] Canal City Hakata (*1) ■ Fewer tourists from South Korea plus self-restraint on going out and fewer Office building Logistics % Year-on-year comparison of sales 96.5 inbound tourists due to COVID-19 infection since late February impacted sales. -

Call for Exhibitors at the 2019 JET Programme Career Fairs 17 Feb

Council of Local Authorities for International Relations (CLAIR) Looking for globally-minded personnel? No Exhibition Call for Exhibitors at the Fee 2019 JET Programme Career Fairs CLAIR hosts the 2019 JET Programme Career Fairs in order to provide a platform for businesses seeking global personnel to meet internationally-minded JET Programme participants with Japanese language ability and conduct interviews with potential job candidates. Fukuoka 3 Feb. 2019 (Sun.) Approx. 100 participants and 30 exhibitors Venue:Fukuoka Fashion Building 2-10-19 Hakata-ekimae, Hakata-ku, Fukuoka city, Fukuoka prefecture (7-minute walk from JR Hakata station / 1-minute walk from Metro Gion station) Application deadline: 28 Dec. 2018 (Fri.) Venue Osaka 17 Feb. 2019 (Sun.) Approx. 180 participants and 32 exhibitors Venue:Herbis Hall 2-5-25 Umeda, Kita-ku, Osaka city, Osaka prefecture (7-minute walk from JR Osaka Station / 5-minute walk from Hanshin Umeda Station) Application deadline: 28 Dec. 2018 (Fri.) Greater Tokyo Company information booth 1 Mar. 2019 (Fri.) Approx. 400 participants and 70 exhibitors Venue:Tokyo Bay Makuhari hall 2-3 Hibino, Mihama-ku, Chiba city, Chiba prefecture (10-minute walk from JR Kaihinmakuhari Station) Application deadline:18 Jan. 2019 (Fri.) Interview corner 2018 Greater Tokyo/Osaka Career Fair Survey Results (from participating companies) % Were you satisfied 100 Did you meet potential hires YES with the career fair? Satisfied or Very Satisfied at the career fair? 93% Application details Online application form: https://job-haku.com/afterjet/contact/ ※Application form and the Career Fair website will be made available on 1 November, 2018 at 10 am.