Walkup Wake-Up Call: New York © the George Washington University School of Business 2017 3 Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Macerich Names Will Voegele to New Position of Chief Development Officer

Macerich Names Will Voegele to New Position of Chief Development Officer August 8, 2019 SANTA MONICA, Calif., Aug. 8, 2019 /PRNewswire/ -- Macerich (NYSE:MAC), one of the nation's leading owners, operators and developers of exceptional retail properties in top markets, today announced the appointment of Will Voegele to the new position of Executive Vice President, Chief Development Officer. Voegele's responsibilities will include overseeing and facilitating all aspects of mixed-use and master planned project development, assessing opportunities across the portfolio for multi-use potential and driving the creative design process that conceives and realizes exceptional place-making environments where consumers want to live, work, stay and play. He will report to Macerich's President Ed Coppola. As a 35-year veteran of the shopping center industry, Voegele brings to Macerich a broad base of experience managing large-scale retail and mixed-use developments as well as renovation and re-development of commercial and retail assets. Recent projects include Ballston Quarter, Arlington, VA, Short Pump Town Center renovation, Richmond, VA, and Station Square, Pittsburgh, PA. A visionary and passionate development executive, Voegele has extensive experience in the conception, master planning and execution of complex mixed-use developments incorporating retail, entertainment, office, hotel and residential uses; securing complicated entitlements; structuring public- private partnerships; and overall development oversight to ensure adherence to project goals and return on investment objectives. Previously, Voegele served as Senior Vice President, Mixed-Use Development for Brookfield Properties and Senior Vice President, Commercial Development for Forest City Realty Trust. "As we seize opportunities to add even more value to our high-quality portfolio of A-level properties in attractive, largely urban markets – including recapturing well-placed Sears boxes – we are very pleased to welcome Will Voegele to our senior executive team," said Coppola. -

Leading the Way in Life Sciences Innovation

LEADING THE WAY IN LIFE SCIENCES INNOVATION JANUARY 2021 1 LifeSci NYC: Leading the Way in Life Sciences Innovation OUR VISION: HEALTHIER COMMUNITIES, A STRONGER ECONOMY With its deep and diverse talent pool, network of premier academic medical centers, lab space, and access to National Institutes of Health and venture funding, New York City has emerged as a major center of life sciences innovation. What started as a hub of biomedical research, clinical care, and commercial biotech firms on the East Side of Manhattan has evolved to become a citywide ecosystem, with neighborhood-based clusters that each make a distinctive contribution to the city’s growing life sciences sector. 2 LifeSci NYC: Leading the Way in Life Sciences Innovation Now is the time to build on these strengths and invest in the spaces, companies, and talent that will create life-saving cures and treatments, while catalyzing new economic opportunities for the people of this city. Over the next decade, Over 3M square feet of additional life sciences space, the City will nurture the including specialized facilities to prepare early-stage development of a thriving discoveries for commercialization, incubator space for life sciences industry startups, and space for expanding biotech companies by investing in: to continue to grow in NYC 100 new startup companies that will drive the development of small molecules, biologics, vaccines, gene therapies, and cell therapies—addressing high unmet medical needs These investments Thousands of new jobs in an industry where 50 percent will lead to: of jobs do not require a bachelor’s degree Dozens of new cures and treatments to keep New Yorkers safe and healthy 3 LifeSci NYC: Leading the Way in Life Sciences Innovation OUR BUILDING BLOCKS: TALENT, INSTITUTIONS, AND INFRASTRUCTURE New York City is home to a deep and diverse talent pool, premier academic and medical institutions, and the widest and most varied healthcare-delivery infrastructure of any place in the world. -

A Map of Free Meals in Manhattan

washington heights / inwood north of 155 st breakfast lunch dinner ARC XVI Fort Washington m–f 12–1 pm 1 4111 BROADWAY Senior Center $2 ENTER 174th ST (A 175 ST) 2 ARC XVI Inwood Senior Center m–f 8:30– m–f 12–1 p m 84 VERMILYEA AVE (A DYCKMAN ST) 9:30 am $1 $1.50 Church on the Hill Older Adults 3 Luncheon Club 2005 AMSTERDAM AVE m–f 1 p m A map of free meals in Manhattan (C 163 ST AMSTERDAM AVE) $1.50 W 215 ST m–f 9– m–f 12–1:30 washington 4 Dyckman Senior Center heights & 3754 TENTH AVE (1 DYCKMAN ST) 10:30 am 50¢ pm $1 BROADWAY inwood Harry & Jeanette Weinberg m–f, su map key symbols key 5 Senior Center 54 NAGLE AVE 12–1 pm (1 DYCKMAN ST) $1.50 2 TENTH AVE SEAMEN AVE Moriah Older Adult Luncheon m-th 1:15–2 pm All welcome Mobile kitchen Residents only 204 ST 11 — 207 ST 6 f 11:45–12:15 pm Club 90 BENNETT AVE (A 181 ST) $1.50 — 205 ST Brown bag meal Only HIV positive 4 Riverstone Senior Center m–f 12–1 Senior Citizens — 203 ST 7 99 FORT WASHINGTON AVE (1 ,A,C 168 ST) pm $1.50 VERMILYEA SHERMANAVE AVE AVE POST AVE — 201 ST m–f m–f 12–1 pm Must attend Women only 8 STAR Senior Center 650 W 187th ST (1 191 ST) 9 a m $1.50 Under 21 services ELLWOOD ST NINTH NAGLE AVE UBA Mary McLeod Bethune Senior m–f 9 am m–f 12–1 pm 9 Center 1970 AMSTERDAM AVE ( 1 157 ST) 50¢ $1 HIV Positive Kosher meals 5 Bethel Holy Church 10 tu 1–2 pm 12 PM 922 SAINT NICHOLAS AVE (C 155 ST) Women Must call ahead to register The Love Kitchen m–f 4:30– BROADWAY 11 3816 NINTH AVE (1 207 ST) 6:30 pm W 191 ST Residents AVE BENNETT North Presbyterian Church sa 12–2 pm 8 W 189 ST 12 525 W 155th ST (1 157 ST) 6 W 187 ST W 186 ST W 185 ST east harlem W 184 ST 110 st & north, fifth ave–east river breakfast lunch dinner harlem / morningside heights ST AVE NICHOLAS W 183 ST 110 155 Corsi Senior Center m–f 12– st– st; fifth ave–hudson river breakfast lunch dinner 63 W 181 ST 307 E 116th ST ( 6 116 ST) 1 pm $1.50 WADSWORTH AVE WADSWORTH 13 Canaan Senior Service Center m–f W 180 ST W 179 ST James Weldon Johnson Senior m–f 12– 10 LENOX AVE (2 ,3 CENTRAL PARK NO. -

Today's Gowanus Is Tomorrow's Tribeca

Today’s Gowanus Is Tomorrow’s Tribeca Twenty under-the-radar microneighborhoods that may just be the Next Big Thing. • By S.Jhoanna Robledo • Published Apr 3, 2011 In a city that is, to quote the late, great Alistair Cooke, “the biggest collection of villages in the world,” what makes a village take off? What turns a non-neighborhood or a fledgling neighborhood or a forgotten, forlorn neighborhood into a Name Brand neighborhood? Sometimes, it takes just one big arrival—an overhauled cultural space (see: Museum of the Moving Image, Astoria), a signature building (MiMA on Far West 42nd Street), or a Zeitgeist- seizing restaurant (Roberta’s in Bushwick)—to shake a neighborhood from a stupor. Sometimes, as with the High Line, the city steps in, providing much-needed capital to enliven an area’s crumbling infrastructure. Other times, as with the damn-the-Superfund darlings Gowanus and Greenpoint, the shift comes from basic free-market forces: outpriced renters seeking more space for less rent; shopkeepers needing bigger footprints; a demand for affordable places to shake it on a Saturday night. And it’s also true that, sometimes, sleepers just suddenly wake up. (Good morning, Flushing!) Below you’ll find twenty pockets around the city pulsing with the first stirrings, anyway, of rebirth. Think of them as villages in the making. The Next Big Neighborhood: • 1. The Higher Line Because the High Line Is About to Double in Size • 2. Manhattan Valley Because It’s Suburbia With Subways • 3. Far West 42nd Because Despite Its Gawky Name, MiMA Is One Stunning Building • 4. -

Investment Manager Summary

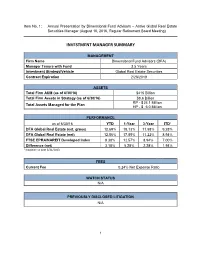

Item No. 1: Annual Presentation by Dimensional Fund Advisors – Active Global Real Estate Securities Manager (August 10, 2016, Regular Retirement Board Meeting) INVESTMENT MANAGER SUMMARY MANAGEMENT Firm Name Dimensional Fund Advisors (DFA) Manager Tenure with Fund 3.5 Years Investment Strategy/Vehicle Global Real Estate Securities Contract Expiration 2/28/2019 ASSETS Total Firm AUM (as of 6/30/16) $415 Billion Total Firm Assets in Strategy (as of 6/30/16) $8.6 Billion RP - $ 24.1 Million Total Assets Managed for the Plan HP - $ 6.0 Million PERFORMANCE as of 6/30/16 YTD 1-Year 3-Year ITD¹ DFA Global Real Estate (est. gross) 12.69% 18.13% 11.58% 9.28% DFA Global Real Estate (net) 12.56% 17.85% 11.22% 8.94% FTSE EPRA/NAREIT Developed Index 9.38% 12.57% 8.94% 7.00% Difference (net) 3.18% 5.28% 2.28% 1.94% ¹ Inception to date 3/31/2013 FEES Current Fee 0.24% Net Expense Ratio WATCH STATUS N/A PREVIOUSLY DISCLOSED LITIGATION N/A 1 Los Angeles Water and Power Employees’ Retirement Plan August 10, 2016 Joseph Chi, CFA, Co-Head of Portfolio Management and Vice President Glenn S. Granz, CFA, Regional Director This information is provided for registered investment advisors and institutional investors, and is not intended for public use. Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission. Consider the investment objectives, risks, and charges and expenses of the Dimensional funds carefully before investing. For this and other information about the Dimensional funds, please read the prospectus carefully before investing. -

Manhattan: City Council, Assembly, and State Senate

Manhattan: City Council, Assembly, and State Senate M O South Riverdale Y S A H O Spencer Estates W L D U P A Y Pelham Bay O R 81 B Y P M 11 HA L 11 78 PE Spuyten Duyvil Marble Hill Pelham Parkway Morris Park Country Club 80 Middletown 13 34 34 NT AV RD MO AM RE DH T Westchester Square FOR E Fordham E Belmont 82 H U T C 33 H B Van Nest I Eastchester Bay R N O S O N N University Heights X R R V V R 14 R Inwood P Y P Y EP CROSS BRONX Tremont Parkchester Unionport 86 P E Tremont 76 RONX E ROSS B Sherman Creek 15 West Farms C P E R E N K C Mount Hope U Castle Hill 10 R B Fort George 72 Bathgate Bruckner Bronx River 36 18 M A J O 79 S R OU Clason Point N D D VIE E 85 W A E V G Claremont Village Soundview A N P E 31 E R Washington Heights 28 E P N BR K TON 77 C ING U ASH R G W B Concourse Harding Park High Bridge 71 16 Morrisania 32 19 Longwood 27 E 161 ST Hunts Point 11 Melrose W 155 ST P E N A D I R E Sugar Hill H 17 S 7 The Hub Hamilton Heights 84 11 27 19 Mott Haven Port Morris 8 22 34 85 V A 70 30 5 Harlem L B S S A L G 9 U H W 125 ST A O East Harlem R D L E D M E La Guardia Airport R R V F R D Y Morningside Heights P E 34 E N O T 35 S S E T 36 I H 16 W 33 Spanish Harlem T 68 8 Steinway CATHEDRAL PY 31 28 34 Ditmars 21 W A K P Astoria Heights S I R 69 Manhattan Valley R O 32 M T 36 T M 22 30 28 E ST B 96 Q W W 96 ST E 11 E 28 T Carnegie Hill N B 13 34 R B E N TO S E 26 IT H 28 11 W 29 12 S 25 13 16 W 86 ST Yorkville Astoria Jackson Heights E Upper West Side H A R L E 39 M N 25 11 R 14 V W 79 ST W 80 ST 15 6 R D Y 25 17 A Upper East Side -

June 2019 Landmarks Resolutions

Carter Booth, Chair Antony Wong, Treasurer Daniel Miller, First Vice Chair Keen Berger, Secretary Susan Kent, Second Vice Chair Erik Coler, Assistant Secretary Bob Gormley, District Manager Community Board No. 2, Manhattan 3 Washington Square Village N EW YORK, NY 10012-1899 www.cb2manhattan.org P: 212-979-2272 F: 212-254-5102 E : [email protected] Greenwich Village v Little Italy v SoHo v NoHo v Hudson Square v Chinatown v Gansevoort Market June 21, 2019 Sarah Carroll, Chair NYC Landmarks Preservation Commission One Centre St., 9th Floor North New York, New York 10007 Dear Chair Carroll: At its Full Board meeting on June 20, 2019, Community Board #2, Manhattan (CB2, Man.) adopted the following resolution: 1. 43 Perry Street. - Application is to replace windows at the primary façade. Whereas: A. The facade was extensively altered prior to designation to a Dutch inspired style with a stained glass window on the ground floor and custom casement windows incorporating distinctive round stained glass elements on the upper floors; and B. The applicant presented evidence that the window with stained glass on the first floor can be restored while the existing casement windows on the upper floors are deteriorated to the extent that they are beyond repair; and C. The existing windows date from the 1948 pre-designation design, with custom made mullions fitted with round architectural stained glass in each section, and they are clearly integral to the design of building and in this respect are historic to the existing facade; and D. The proposal is to replace all of the windows with sliding style windows with considerably wider frames and “snap-in” mullions and is in no respect suitable for this building and the historic neighborhood; now Therefore be it resolved that CB2, Man. -

July 2019 SLA Licensing Resolutions

Carter Booth, Chair Antony Wong, Treasurer Daniel Miller, First Vice Chair Keen Berger, Secretary Susan Kent, Second Vice Chair Erik Coler, Assistant Secretary Bob Gormley, District Manager COMMUNITY BOARD NO. 2, MANHATTAN 3 W ASHINGTON SQUARE V ILLAGE N EW YORK, NY 10012-1899 www.cb2manhattan.org P: 212-979-2272 F: 212-254-5102 E : [email protected] Greenwich Village v Little Italy v SoHo v NoHo v Hudson Square v Chinatown v Gansevoort Market July 23, 2019 Director Licensing Issuance Division NY State Liquor Authority 317 Lenox Avenue New York, New York 10027 Dear Sir/Madam: At its Full Board meeting on July 18, 2019, Community Board #2, Manhattan (CB2, Man.) adopted the following resolution: 1. K&K Grand Corp., d/b/a SoHo Thai, 141 Grand St. 10013 (OP – Restaurant | Corporate Transfer) i. Whereas, applicant appeared before Community Board 2, Manhattan’s SLA Licensing committee to present an application for a corporate change to the existing restaurant wine license (SN 1278344) for their Thai cuisine restaurant located in a M1-5B zoned for-story, mixed-use 1920 building on Grand Street between Lafayette and Crosby Streets (block #233/ lot #12) in the NYC Landmarks Preservation Commission designated SoHo-Cast Iron Historic District; and, ii. Whereas, the interior 1-story premises are 1,350 sq. ft., and has a total of 15 tables with 46 seats and one service bar (no seats); and applicant has Letter of No Objection to use the space as a food and drinking establishment from the NYC Department of Buildings; and, iii. Whereas, the applicant signed and notarized a new stipulations agreement with CB2, Man. -

West Village Little Italy Noho Civic Center Chinatown Hudson Square

Neighborhood Map ¯ Bleecker Street 494 88 1 Bond Street E 2 Street 15 6 Avenue Anthology 95 Minetta Center for 1 Mercer 2 Avenue Green t Fiorello Film e 56 Architecture e Playground M15 t La Guardia r Washington 29 324 Archives Grove Street Father15 Demo t e SBS Statue 26 60 S e Square Extra Place Square a r Morton Street tt t Village Hudson Street Our Lady e 101 313 n S i 1 6 M15 n M 337 31 B 68 of Pompeii Bleecker Street 350 e a Church of d 652 f t Church v 464 o 5 i e Minetta l Barrow Street r l d Street Mercer Saint Luke re 30 S u t Triangle Broadway 28 M20 tr 27 228 Bleecker Street in the Fields e S S Culture 37 71 e Street Thompson t y Street MacDougal 2 336 4 ro Bleecker St Project 100 197 La Guardia Place Guardia La 198 Commerce Street e 231 189 177 163 147 123 113 212 77 73 29 L 53 E 1 Street Cherry 7 Avenue South Greenwich Street653 88 324 26 Lane Bleecker Street Bleecker Street Bleecker Street 14 30 41 Winston Bleecker Street Theatre Carmine Street 316 32 Churchill Avenue of the AmericasLittle Red Bowery 178 162 146 98 68 60 195 196 210 Square 171 Square 642 M20 Downing Street 36 M103 2 Av Playground La Guardia M103 452 Corner 100 Liz Christy Barrow Street 49 Gardens 39 Garden 455 Noho 102 43 278 257 Greenwich 28 M55 M55 296 69 51 Bedford Street M21 West 509 Silver Towers 294 33 Downing Street Chrystie Street 71 637 35 22 William F. -

The Case of New York City's Financial District

INFORMATION TECHNOWGY AND WORLD CITY RESTRUCTURING: THE CASE OF NEW YORK CITY'S FINANCIAL DISTRICT by Travis R. Longcore A thesis submitted to the Faculty of the University of Delaware in partial fulfillment of the requirements for the degree of Honors Bachelor of Arts in Geography May 1993 Copyright 1993 Travis R. Longcore All Rights Reserved INFORMATION TECHNOWGY AND WORLD CITY RESTRUCTURING: THE CASE OF NEW YORK CITY'S FINANCIAL DISTRICT by Travis R. Longcore Approved: Peter W. Rees, Ph.D. Professor in charge of thesis on behalf of the Advisory Committee Approved: Robert Warren, Ph.D. Committee Member from the College of Urban Affairs Approved: Francis X. Tannian, Ph.D. Committee Member from the University Honors Program Approved: Robert F. Brown, Ph.D. Director, University Honors Program "Staccato signals of constant information, A loose affiliation of millionaires and billionaires and baby, These are the days of miracle and wonder. This is a long distance call. " Paul Simon, Graceland iii ACKNOWLEDGEMENTS The author would like to recognize and thank Dr. Peter Rees for his guidance on this project. Without the patient hours of discussion, insightful editorial comments, and firm schedule, this thesis would have never reached completion. The author also thanks the University Honors Program, the Undergraduate Research Program and the Department of Geography at the University of Delaware for their financial support. Many thanks are due to the Water Resources Agency for New Castle County for the use of their automated mapping system. IV TABLE OF CONTENTS LIST OFTABLES .................................... viii LIST OF FIGURES ix ABSTRACT ....................................... .. x Chapter 1 THE CITY IN A WORLD ECONOMY ................... -

CB11 Recommendation

COMMUNITY BOARD ELEVEN BOROUGH OF MANHATTAN 1664 PARK AVENUE NEW YORK, NEW YORK 10035 Diane Collier TEL: (212) 831-8929/30 Chair FAX: (212) 369-3571 Angel D. Mescain District Manager www.cb11m.org April 18, 2017 Marisa Lago Director New York City Department of City Planning 120 Broadway, 31st Floor New York, NY 10271 Re: Land Use Application No. 170269PCM, 170270PCM – M11 Sanitation Garage Relocation On April 18, 2017, Community Board 11 (CB11) held a public hearing and voted on Land Use Application Nos. 170269PCM, 170270PCM, submitted by the New York City Department of Sanitation, the New York City Department of Citywide Administrative Services and the New York City Department of Housing Preservation & Development with respect to a proposed project which would result in the relocation of the Manhattan District 11 Sanitation Garage, Manhattan Lot Cleaning Unit and Headquarters to a site located at 207-17 East 127th Street (Block 1792, Lot 5 and p/o Lot 28) between Second Avenue and Third Avenue and East 127th Street and 128th Street in the Borough of Manhattan. The Manhattan District 11 Sanitation Garage and Manhattan Lot Cleaning Unit and Headquarters are currently located elsewhere in Manhattan Community District 11 (East Harlem). Our board has considered this project over the past few months and has hosted several presentations by the development team. Project Description The City of New York (“City”) Department of Sanitation (“DSNY”) with the Department of Citywide Administrative Services (“DCAS”) proposes to acquire (acquisition terms to be determined), approximately 119,560 square feet (SF) of space comprising (a) an entire building of approximately 91,478 SF, (b) approximately 3,800 SF of outdoor parking space, and (c) approximately 24,282 SF adjacent land on which a new building, comprising of approximately 8,750 SF of space will be constructed by the property owner, at 207-17 East 127th Street (aka 2495 Second Avenue and/or 206-20 East 128th Street), in the Borough of Manhattan, all to be used by DSNY. -

Manhattan 2016 Mid-Year Sales Report by Ariel Property Advisors | Released July 2016

MANHATTan 2016 Mid-Year SaleS REPORT by Ariel Property Advisors | Released July 2016 Join Our Network: e-mail [email protected] or visit arielpa.nyc 212.544.9500 I arielpa.nyc 122 East 42nd Street, Suite 2405, New York NY 10168 MANHATTan 2016 Mid-Year SaleS REPORT Dear Friends, 2016 Mid-Year SaleS REPORT From the continuation of low interest rates to the Brexit, the first half of 2016 has seen some remarkable economic events that have been having various effects on the Manhattan real estate market. Manhattan investment property sales saw a pullback in terms of dollar volume and, in a more pronounced way, transaction volume during 1H16, but several fac- Dollar Volume Transaction Volume Property Volume tors are contributing to a greater sense of stability in the market place. In 1H16, Manhattan saw 304 transactions consisting of 361 properties totaling approxi- $19.3 304 361 mately $19.35 billion in gross consideration in 1H16. The previous six months of 2H15, which saw 345 transactions for 477 properties with an aggregate dollar volume of $22.29 BILLION billion, capped off a banner year that included the $5.5 billion sale of Stuyvesant Town / Pe- 13% decrease 11% decrease 24% decrease ter Cooper Village. By excluding this outlier transaction from the aggregate dollar volume, 1H16 figures represent a 15% increase in total dollar volume compared to 2H15. Moreover, compared compared compared 1H16 dollar volume figures are well above the dollar volume seen in 1H14. to 2H 2015 to 2H 2015 to 2H 2015 Fewer transactions are taking place—the 1H16’s 304 sales is the lowest number of trans- actions to take place since 1H13—but properties that are selling demonstrate that strong demand remains for quality product.