Motor Oil (Hellas) Corinth Refineries S.A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ELLAKTOR Presentation March 5Th, 2020 Table of Contents

ELLAKTOR Presentation March 5th, 2020 Table of contents 1 Executive summary 2 Business Overview 3 Capital Structure 4 9M 2019 Financials 1 1 Executive summary 2 Business Overview 3 Capital Structure 4 9M 2019 Financials 2 Executive Summary ELLAKTOR history 1950s-1990s 1990s-2000s 2000-2009 2010-2018 2018 - forward 1950s: Establishment of 1999: Led domestic 2007: Acquisition of TEB, ELLINIKI construction sector Pantechniki, leading to Industry TECHNODOMIKI and consolidation (Merger of controlling stake in Attiki consolidation AKTOR TEB, Elliniki Odos (59%) Technodomiki & AKTOR) 1996: Signed first 2003: Entry into concession projects environment segment Diversification (Attiki Odos and Rio- 2008: Signed 3 out of 5 of activities Antirrio Bridge) major concession projects awarded in Greece 2004: First international 2012: c. €600m of construction contracts in projects in the Balkans Romania and Kuwait Geographic 2014: €3.2bn Doha metro 2005: Internationalisation diversification project in Qatar of HELECTOR through acquisition of Herhof GmbH 2010-2012: Sale of gold 2018: Sale of Athens Resort assets Casino (€13.5 ml) Focus on core 2014: ELTECH ANEMOS 2018: Increased stake in IPO Attiki Odos by 6.5% competencies 2019: Sold Corporate Headquarters (€25.5 ml) and stake in Elpedison (€ 18 ml) 2015: 1st Waste PPP in July 2018: Newly elected Greece Board post 1st proxy fight in Renewed 2016: Moreas completed Greece opportunity / in full operation July 2019: Group 2017-18 :Olympia Odos rationalization / ELTECH & Maliakos completed ANEMOS absorption 4 The ELLAKTOR group led the construction sector consolidation in Greece H’ (Highest) grade construction companies in 1998 (€m) 7th grade(1) construction companies in 2018 (€m)(2) Thessaliki SA Etep SA Parnon SA Themeli SA Odon & Odostromaton SA Ekter SA INTRAKAT SA Gekat SA Europaiki Techniki SA I.G. -

Annual Report 2007 Design - Production: 2007 2007

NEMESIS S.A. Annual Report 2007 Design - Production: 2007 2007 12A Irodou Attikou str., Annual Report Maroussi 151 24, Athens - GREECE Tel.: (+30) 210 809 4000, Fax: (+30) 210 809 4444 www.moh.gr CMYK CORINTH REFINERIES S.A. Annual Report 2007 TableTable of of contents contents 1 INFORMATION CONCERNING THIS ANNUAL REPORT AND THE COMPANY AUDITORS............................6 2 SHAREHOLDERS’ RIGHTS ..............................................................................................................................8 2.1 General Information ..................................................................................................................................8 2.2 Dividend Taxation......................................................................................................................................9 3 MARKET INFORMATION AND STRUCTURE ................................................................................................10 3.1 Structure of the Oil Refining Market in Greece ..........................................................................................10 3.2 Regulatory Framework ............................................................................................................................11 3.3 Recent Developments in the International Oil Market ................................................................................14 4 COMPANY PROFILE ......................................................................................................................................15 -

Exakm Sa Reference List of Major Project & Supplies 2000 – 2015

EXAKM SA REFERENCE LIST OF MAJOR PROJECT & SUPPLIES 2000 – 2015 Industrial Commercial & Technical Co. CLIENT EQUIPMENT BRAND PROJECT YEAR NEW INTERNATIONAL AIRPORT OF ERGOKAT ATE HYDRANTS ERHARD GmbH ATHENS 2000 “EL. VENIZELOS” NEW INTERNATIONAL AIRPORT OF SAFETY VALVES FOR WATER SUPPLY ERGOKAT ATE BAILEY BIRKETT ATHENS 2000 NETWORK “EL. VENIZELOS” NEW INTERNATIONAL AIRPORT OF J/V ERGOKAT-ELTER-PYRAMIS Co- PENSTOCKS ERHARD GmbH ATHENS 2000 OPERATION “EL. VENIZELOS” BALL VALVES, BUTTERFLY VALVES, EVINOS & MORNOS RIVERS JUNCTION, TERNA SA ERHARD GmbH 2000 CONTROL VALVES TUNEL & DIVERTION GREEK SUGAR INDUSTRY PNEUMATIC CONTROL VALVES SAMSON AG EZA S.A 2000 FISCHER & UNILEVER S.A - ELAIS VARIABLE ARE FLOWMETERS PEIRAOS FACTORY 2000 PORTER – ABB EYATH - SEWAGE CENTRAL J/V ATHENA S.A – X. KONSTANTINIDIS PENSTOCKS ERHARD GmbH TRANSMISSION NETWORK OF 2000 S.A THESSALONIKI FISCHER & ATHENIAN BREWERY S.A ELECTROMAGNETIC FLOWMETERS “IOLI” NATURAL WATER PLANT 2000 PORTER – ABB MUNICIPAL ENTERPRISE OF WATER 122 DISTRICT HEATING CONSUMER SUPPLY AND SEWAGE OF KOZANI EXAKM SA KOZANI DISTRICT HEATING 2000 THERMAL SUBSTATIONS HYDROELECTRIC POWER PLANT OF HYDROENERGIAKI S.A PENSTOCKS ERHARD GmbH 2000 “ANTHOCHORI” EXAKM SA Page 1 of 21 Ave. Kallirrois 39 Tel.: +30 210 9215332, +30 210 9218441, +30 210 9216887 GR-11743 Athens Fax: +30 210 9218761 http://www.exakm.gr Factory & North Greece Branch: Ο.Τ 039Β – Insustrial Area of Sindos, GR-57022 Thessaloniki, Τel. +30 2310 799954, +30 2310 570387 EXAKM SA REFERENCE LIST OF MAJOR PROJECT & SUPPLIES 2000 – 2015 -

Winter in Prague 144 Companies Representing 15 Countries Can Be Selected for Meetings Online

emerging europe conference Winter in Prague 144 companies representing 15 countries can be selected for meetings online Atrium / X5 / Banca Transilvania / Torunlar REIC have recently signed up click here Registration closes on Friday Tuesday to Friday 4 November For more information please contact your WOOD sales representative: 29 November to 2 December 2016 Warsaw +48 222 22 1530 Prague +420 222 096 452 Radisson Blu Alcron Hotel London +44 20 3530 0611 [email protected] Companies by country Bolded confirmed Companies by sector Bolded confirmed Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Biztonsagi Nyomda Nyrt. Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Agora AT&S Magyar Telekom Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka Asseco Poland CA Immobilien MOL Group Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim AT&S Conwert OTP Bank Electrica Cimsa Arcelik Banca Transilvania CME Erste Bank Wizz Air Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Cyfrowy Polsat S.A. Immofinanz Hidroelectrica Dogan Holding Atlantic Grupa BGEO Ciech LiveChat Software PORR Poland Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Pekao Cimsa Luxoft Raiffeisen Bank Agora OMV Petrom Ford Otosan CCC Bank Zachodni WBK Dogus Otomotiv Magyar Telekom RHI Alior Bank Romgaz Garanti Coca-Cola Icecek Bucharest Stock Exchange Ford Otosan O2 Czech Republic Uniqa AmRest SIF-2 Moldova Halkbank DIXY CSOB Grupa Azoty Orange Polska Vienna Insurance Group Asseco Poland Transelectrica Lokman Hekim Eurocash Erste Bank Grupa Kęty OTE Warimpex Bank Millennium Transgaz Migros Ticaret Folli Follie Eurobank HMS Group Turk Telekom Wienerberger Bank Pekao Pegasus Airlines Fortuna Garanti Industrial Milk Company Wirtualna Polska Holding Bank Zachodni WBK Russia Sabanci Holding Gorenje Getin Noble Bank Intercars Croatia CCC DIXY Teknosa Hellenic Petroleum Halkbank Mytilineos Atlantic Grupa Ciech Gazprom Tofas Kernel Hellenic Bank Pegas Nonwovens Podravka Cyfrowy Polsat S.A. -

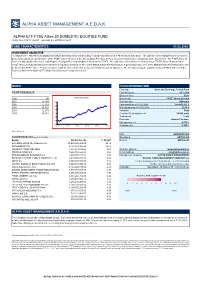

Alpha Asset Management Α.Ε.D.Α.Κ

ALPHA ASSET MANAGEMENT Α.Ε.D.Α.Κ. ALPHA ETF FTSE Athex 20 DOMESTIC EQUITIES FUND HCMC Rule 789/13.12.2007 Gov.Gaz. s.n. 2474/B/31.12.07 FUND CHARACTERISTICS 01.02.2008 INVESTMENT OBJECTIVE The Alpha ETF FTSE Athex 20 DOMESTIC EQUITIES FUND is the first Exchange Traded Fund listed on the Athens Stock Exchange. The objective of the Mutual Fund’s investment policy is to replicate the performance of the FTSE® Athex 20 Index of the Athens Stock Exchange in Euro, by mirror matching the composition of the Benchmark. The FTSE® Athex 20 Index is a big capitalization Index, capturing the 20 largest blue chip companies listed on the ATHEX. The total value of investments in shares of the FTSE® Athex 20 Index and in FTSE® Athex 20 Index derivatives accounts for a regulatory minimum of 95% of the Mutual Fund’s Net Asset Value. A percentage up to 35% of the Mutual Fund’s Net Asset Value may be invested in FTSE® Athex 20 Index derivatives with the aim of achieving the Mutual Fund’s investment objectives. The derivatives may be tradable (such as FTSE® Athex 20 Index futures) and/or non-tradable (OTC Swap Transactions) in a regulated market. INDEX FUND INFORMATION Fund type Domestic Exchange Traded Fund PERFORMANCE First listing date 24.1.2008 Base currency Euro Year (%) FTSE Athex 20 Index Benchmark FTSE® Athex 20 Index 2007 15,79% 3300 Currency risk Minimum 2006 17,73% Fund assets as of 01.02.2008 141.403.221 € 2800 2005 30,47% Net unit price as of 01.02.2008 23,40 € 2004 32,27% 2300 Valuation Daily 2003 35,43% 1800 Creation / Redemption unit 50.000 units 1300 Trading unit 1 unit Dividends Annual - 30 June 800 Management fee 0,275% 300 31/12/02 31/12/03 31/12/04 31/12/05 31/12/06 31/12/07 Custodian fee 0,100% Source: Bloomberg ISIN GRF000013000 COMPOSITION (as of 01.02.2008) Bloomberg AETF20 GA Equity Market Cap (€) % Weight Reuters AETF20.AT NATIONAL BANK OF GREECE S.A. -

Hellenic Equities: a New Start-July 2015

Hellenic Equities: A New Start-July 2015 In view of the imminent Hellenic stock market re-opening sometime in the short term future we attempt to re-value our preferred picks and affirm our investment thesis. It is more than obvious that in such extraordinary circumstances with low visibility and high volatility in the market and financial /fiscal operations, any assumptions regarding valuations fall under certain culprits. At the core of our problem lies the Risk free rate crucial for our model. We have utilized both the normalized scenario of 6.50% R.f. rate and the 10.50% stressed R.f. rate to better evaluate our picks. We are obliged to pinpoint that at 11.00% current 10yr Hellenic Government Bond yield both our scenarios fall short. Our fundamental research indicates as top picks in our Hellenic Equities Universe the following listed stocks: Coca Cola Hellenic (CCH), OTE Hellenic Telecommunications Organization (HTO), Aegean Airlines (ARAIG), Mytilineos Holdings (MYTIL), Metka S.A (METK), Hellenic Organization of Football Prognostics (OPAP), Titan Cement (TITK) and Hellenic Exchanges Group (EXAE). Additionally we have a positive view on Motor Oil, Thrace Plastics, Kri Kri S.A, Thessaloniki Sewage Company and Terna Energy S.A from smaller capitalizations. Coca Cola Hellenic Bottling operates largely in a broad geographical area covering the Balkan markets, Russia, certain parts of Europe and Greece. The Company is headquartered in Switzerland, a relocation offering an improved risk- return profile due to the significantly lower risk premium. We expect Coca Cola Hellenic to preserve its strong Cash Flow ability and regard it a safe and value play on Greek Equities. -

Company Update Strategy to Penetrate New Markets Pays Off

Metka Greece/ Basic Resources Company update Investment Research Reason: Estimates Revision 3 June 2013 Buy Strategy to penetrate new markets pays off Recommendation unchanged Share price: EUR 10.70 Despite the uncertain global economic environment, Metka’s strategy to closing price as of 31/05/2013 penetrate new markets in Africa and Middle East bears fruits, securing Target price: EUR 13.80 new EPC contracts that help replenish backlog. Metka’s attractive from Target Price: EUR 12.70 investment case remains intact due to: a) solid position in a broad region Reuters/Bloomberg MTKr.AT/METTK GA (SE Europe, Middle East, Africa) which is characterized by substantial Daily avg. no. trad. sh. 12 mth 46,695,000 opportunities due to rising demand and high infrastructure needs, b) Daily avg. trad. vol. 12 mth (m) 488,890.88 increasing importance of natural gas as the fuel of choice for thermal Price high 12 mth (EUR) 12.70 power plants, c) strong balance sheet estimating a net cash position of Price low 12 mth (EUR) 5.55 c.EUR 190m by the end of 2013 and c.EUR 260m by the end of 2014. In Abs. perf. 1 mth -7.2% this framework, we raise our target price to EUR 13.80 from EUR 12.70 Abs. perf. 3 mth -12.3% Abs. perf. 12 mth 82.9% previously, reiterating our Buy recommendation. Market capitalisation (EURm) 556 Metka’s backlog currently stands at around EUR 1.0bn, conservatively Current N° of shares (m) 52 excluding from our estimates the second awarded project in Syria with a budget of EUR 678m as opposed to the first project which is in an Free float 43% advanced phase. -

Permanent University Fund Detail Schedules of Investment Securities and Independent Auditors’ Report

PERMANENT UNIVERSITY FUND DETAIL SCHEDULES OF INVESTMENT SECURITIES AND INDEPENDENT AUDITORS’ REPORT August 31, 2014 INDEPENDENT AUDITORS' REPORT ON SUPPLEMENTAL SCHEDULES The Board of Regents of The University of Texas System The Board of Directors of The University of Texas Investment Management Company We have audited the financial statements of the Permanent University Fund (the “PUF”) as of and for the years ended August 31, 2014 and 2013, and have issued our report thereon dated October 31, 2014, which contained an unmodified opinion on those financial statements. Our audits were conducted for the purpose of forming an opinion on the financial statements as a whole. The supplemental schedules consisting of the PUF’s equity securities (Schedule A), preferred stocks (Schedule B), purchased options (Schedule C), debt securities (Schedule D), investment funds (Schedule E), physical commodities (Schedule F), cash and cash equivalents (Schedule G), hedge fund investment funds (Schedule H), and private investment funds (Schedule I) as of August 31, 2014 are presented for the purposes of additional analysis and are not a required part of the financial statements. These schedules are the responsibility of The University of Texas Investment Management Company and were derived from and relate directly to the underlying accounting and other records used to prepare the financial statements. Such schedules have been subjected to the auditing procedures applied in our audits of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. -

Soft Quarter Shadowed by New Projects

GREECE | EQUITY RESEARCH | INDUSTRIALS May 17, 2013 Q1 2013 REVIEW METKA Recommendation BUY Target Price €13.40 Soft quarter shadowed by new projects Prior Target Price €12.70 Closing Price (17/05) €12.50 Q1 2013 review - The EPC contractor reported a 21.5% decline in revenues in the Market Cap (mn) €649.4 first quarter to EUR134mn, reflecting tough comparables, weak contract execution on Greece and the delay in Syria, which had made a significant contribution during Expected Return 1.0% the same period last year. Apart from these expected trends, Turkey-related Expected Dividend (2014e) 6.2% Expected Total Return 7.2% payments came in lower than our expectations and as a result group sales stood 26% lower than our estimates. This does not trigger a downgrade of our 2013e METKA Share Price estimates however; recall that the two Turkish projects are up for completion in 13.00 H1 2013 and we expect that the revenue miss will be reversed in the coming quarter. Adjusting for Turkey, the results were broadly in line with our expectations. On a positive note, the mgt’s special measures in Syria started 11.00 delivering positive results and contract execution has resumed. EBITDA stood at EUR22.9mn, down 17.3% yoy and 24.3% lower than our forecasts reflecting the aforementioned revenue miss but on sustainably strong operating margins, which 9.00 were in line with our forecasts. Although there was no improvement in working capital, METKA reported positive operating cash flows of EUR14.3mn in the quarter compared to an outflow of EUR84.6mn last year. -

24Th National Conference ENERGY & DEVELOPMENT 2019

24th National Conference ENERGY & DEVELOPMENT 2019 Curriculum Vitae of Moderators and Speakers Athens, 21-22 November 2019 2 Boyana Achovski GIE Secretary General, Gas Infrastructure Europe (GIE), Brussels, Belgium Since September 2016, Boyana Achovski serves as Secretary General of Gas Infrastructure Europe (GIE), the European association of gas transmission, gas storage and LNG regasification terminal operators. Prior to her current function, Ms. Achovski held the position of GIE Vice Executive Secretary for a period of 4 years. Before joining GIE, Boyana Achovski worked for Bulgartransgaz, the Bulgarian transmission and storage operator, where she led the Analysis and International Operations Division, managing the company’s undertakings relating to the European regulatory framework and European energy policy. Ms. Achovski graduated in International Economic Affairs, specialized in International Finance and holds a Master's degree in Finance. Boyana Achovski was a Chair of GasNaturally Steering Committee from June 2017 to January 2018 and from July to December 2019. Ass. Prof. Athanasia Alonistioti Associate Professor at the Department of Informatics and Telecommunications of the University of Athens Ms. Athanasia Alonistioti is Associate Professor at the Department of Informatics and Telecommunications of the University of Athens. She has extensive experience in European and National Research Programs, while she has also served as being coordinator and technical manager in several of them. She has participated in more than 30 projects (eg CTS, SS # 7, ACTS RAINBOW, EURESCOM, MOBIVAS, ANWIRE, FP7 E2R, LIAISON, E3, SELFNET, UNIVERSELF, CONSERN, WHERE 2, SmartAgriFood, LIVECITY, METIS, H2020 FISPACE, SPECIFI, FRACTALS, PRIVACY FLAG, Fed4FIRE, 5GINFIRE, 5GCroCo). Her research interests are in the areas of Cognitive Self-managed Networks, Future Internet, Internet of Things, Big Data Analytics. -

Hellenic Cables S.A. "Hellenic Cables Industry S.A."

HELLENIC CABLES S.A. "HELLENIC CABLES INDUSTRY S.A." Report on the Market Value of the transferred assets and liabilities based on the Statement of Financial Position as at 31 December 2015 based on the provisions of article 52 of Law 4172/2013 DFK P AUDIT S.A. Certified Public Accountants and Business Advisors 4 Vas. Sofias & 153 Kifissias Ave., GR-151 24 Marousi Tel.: +30 (210) 7249302, Fax: +30 (210) 7212075 Greek ICPA (SOEL) Reg. No.: 163 Reg. No. in Accounting Standardisation and Auditing Committee (ELTE):031 www.pdaudit.gr HELLENIC CABLES SA Report on the Market Value of the transferred Assets and Liabilities based on the Statement of Financial Position as at 31 December 2015. Table of contents 1 Mission, purpose and extent of project 3 2 Establishment, term and registered office of the Contributor 4 3 Purpose of the Contributor 4 4 Shareholders - Share Capital of the Contributor 5 5 Management - Representation of the Contributor 5 6 Description of the Contributing Industry 5 6.1 Description of the Manufacturing Process per Factory 6 6.2 Description of the Industrial Products Manufactured 10 7 Description of Contributed Part of Commercial Sector 11 8 Approach to project and audit procedures 12 9 Valuation method 13 10 Valuation methodology for the contributed assets and liabilities 14 11 Breakdown of Statement of Financial Position as at 31 December 2015 of the contributed sector (amounts in Euro) 15 11.1 Assets 15 11.2 Liabilities 31 11.3 Equity 37 12 Conclusion 40 13 Details of Acquirer 42 14 Exchange ratio of shares 43 ANNEXES I. -

Annual Report 2018

ANNUAL REPORT 2018 Message from the Chairman 2018 was another year of changes, domestically and globally. For the Greek Economy, the completion of the Third Economic Adjustment Program was a milestone, creating new opportunities and prospects for positive developments in the country. Despite the favorable forecasts, however, challenges remain for the next day to come, as 2019 is an election year. Internationally, major political events have led to the destabilization of several regions globally, which, together with the trade tensions between major economies, have strengthened the feeling of uncertainty. However, in this context, MYTILINEOS has managed, for yet another year, to cope with the challenges and achieve a positive economic performance. In the Metallurgy Business Unit, and in a year of unpredictable turns, the company successfully took advantage of the opportunities that rose from the imposition of US tariffs on the Russian industry. The rapid rise in the price of alumina, which negatively affected almost all aluminium producers, did not affect our company, demonstrating once again the advantage of the fully vertically integrated producer. Part of enhancing the metallurgical sector was the acquisition of 97.87% of EP.AL.ME. SA, a company that operates in the production, processing and trading of metals and especially aluminium alloys and derivative products. The particular investment increases the company’s presence in Greek and international markets, directly boosts its production and extends its activity by recycling aluminium scrap. At the same time, the basic engineering study for a new -game changer - Alumina production plant is rapidly proceeding at our Aghios Nikolaos premises. In the EPC Business Unit, the company continued its successful course undertaking a series of international energy construction projects, while METKA EGN announced some new investment partnerships expanding its activities both in existing and emerging markets.