Hellenic Petroleum 2019 Outlook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2007 Design - Production: 2007 2007

NEMESIS S.A. Annual Report 2007 Design - Production: 2007 2007 12A Irodou Attikou str., Annual Report Maroussi 151 24, Athens - GREECE Tel.: (+30) 210 809 4000, Fax: (+30) 210 809 4444 www.moh.gr CMYK CORINTH REFINERIES S.A. Annual Report 2007 TableTable of of contents contents 1 INFORMATION CONCERNING THIS ANNUAL REPORT AND THE COMPANY AUDITORS............................6 2 SHAREHOLDERS’ RIGHTS ..............................................................................................................................8 2.1 General Information ..................................................................................................................................8 2.2 Dividend Taxation......................................................................................................................................9 3 MARKET INFORMATION AND STRUCTURE ................................................................................................10 3.1 Structure of the Oil Refining Market in Greece ..........................................................................................10 3.2 Regulatory Framework ............................................................................................................................11 3.3 Recent Developments in the International Oil Market ................................................................................14 4 COMPANY PROFILE ......................................................................................................................................15 -

Exakm Sa Reference List of Major Project & Supplies 2000 – 2015

EXAKM SA REFERENCE LIST OF MAJOR PROJECT & SUPPLIES 2000 – 2015 Industrial Commercial & Technical Co. CLIENT EQUIPMENT BRAND PROJECT YEAR NEW INTERNATIONAL AIRPORT OF ERGOKAT ATE HYDRANTS ERHARD GmbH ATHENS 2000 “EL. VENIZELOS” NEW INTERNATIONAL AIRPORT OF SAFETY VALVES FOR WATER SUPPLY ERGOKAT ATE BAILEY BIRKETT ATHENS 2000 NETWORK “EL. VENIZELOS” NEW INTERNATIONAL AIRPORT OF J/V ERGOKAT-ELTER-PYRAMIS Co- PENSTOCKS ERHARD GmbH ATHENS 2000 OPERATION “EL. VENIZELOS” BALL VALVES, BUTTERFLY VALVES, EVINOS & MORNOS RIVERS JUNCTION, TERNA SA ERHARD GmbH 2000 CONTROL VALVES TUNEL & DIVERTION GREEK SUGAR INDUSTRY PNEUMATIC CONTROL VALVES SAMSON AG EZA S.A 2000 FISCHER & UNILEVER S.A - ELAIS VARIABLE ARE FLOWMETERS PEIRAOS FACTORY 2000 PORTER – ABB EYATH - SEWAGE CENTRAL J/V ATHENA S.A – X. KONSTANTINIDIS PENSTOCKS ERHARD GmbH TRANSMISSION NETWORK OF 2000 S.A THESSALONIKI FISCHER & ATHENIAN BREWERY S.A ELECTROMAGNETIC FLOWMETERS “IOLI” NATURAL WATER PLANT 2000 PORTER – ABB MUNICIPAL ENTERPRISE OF WATER 122 DISTRICT HEATING CONSUMER SUPPLY AND SEWAGE OF KOZANI EXAKM SA KOZANI DISTRICT HEATING 2000 THERMAL SUBSTATIONS HYDROELECTRIC POWER PLANT OF HYDROENERGIAKI S.A PENSTOCKS ERHARD GmbH 2000 “ANTHOCHORI” EXAKM SA Page 1 of 21 Ave. Kallirrois 39 Tel.: +30 210 9215332, +30 210 9218441, +30 210 9216887 GR-11743 Athens Fax: +30 210 9218761 http://www.exakm.gr Factory & North Greece Branch: Ο.Τ 039Β – Insustrial Area of Sindos, GR-57022 Thessaloniki, Τel. +30 2310 799954, +30 2310 570387 EXAKM SA REFERENCE LIST OF MAJOR PROJECT & SUPPLIES 2000 – 2015 -

³Privatisation, Employment and Employees´ Nikiforos Manolas

&RQIHUHQFHRQ ³3ULYDWLVDWLRQ(PSOR\PHQWDQG(PSOR\HHV´ 1LNLIRURV0DQRODV (FRQRPLVW 0LQLVWU\RI(FRQRP\DQG)LQDQFH *UHHFH 5HJXODWRU\ 5HIRUPV 6WUXFWXUDO &KDQJHV DQG 3ULYDWLVDWLRQ LQ *UHHFH GXULQJ V 3DSHU VXEPLWWHG EXW QRW SUHVHQWHG ± 2FWREHU $WDN|\ ,VWDQEXO 7XUNH\ 5HJXODWRU\5HIRUPV6WUXFWXUDO&KDQJHVDQG3ULYDWLVDWLRQLQ*UHHFHGXULQJV ,%DFNJURXQG During 90s, for the fist time in post-war history, Greek strategies for economic development shifted markedly reliance on market forces rather than on state-managed growth. In the pre-1974 period Greece’s state-led development strategy based on import substitution and credit allocation produced strong growth (7% with manufacturing on the average at 11.4% annually), combined with low inflation (4%) and small balance of payments deficits (2.1% of GDP) until 1974. From 1974 until 1995 the economy showed a completely different picture. GDP annual growth rate averaged 2%, manufacturing growth slowed to almost zero, annual inflation averaged 18%, and the average external deficit, as a share of GDP, doubled. This performance was much worse than that of its neighbors and the other countries of the European Union (EU). The economic slowdown can be attributed almost completely to two major factors, namely the decline in the share of total investments in GDP, and the decline in the productivity of new investments. In an environment which had led to a downward spiral in economic performance, ultimately resulting in crisis (of slowing growth) and many large private firms that had grown rapidly in -

Winter in Prague 144 Companies Representing 15 Countries Can Be Selected for Meetings Online

emerging europe conference Winter in Prague 144 companies representing 15 countries can be selected for meetings online Atrium / X5 / Banca Transilvania / Torunlar REIC have recently signed up click here Registration closes on Friday Tuesday to Friday 4 November For more information please contact your WOOD sales representative: 29 November to 2 December 2016 Warsaw +48 222 22 1530 Prague +420 222 096 452 Radisson Blu Alcron Hotel London +44 20 3530 0611 [email protected] Companies by country Bolded confirmed Companies by sector Bolded confirmed Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Biztonsagi Nyomda Nyrt. Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Agora AT&S Magyar Telekom Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka Asseco Poland CA Immobilien MOL Group Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim AT&S Conwert OTP Bank Electrica Cimsa Arcelik Banca Transilvania CME Erste Bank Wizz Air Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Cyfrowy Polsat S.A. Immofinanz Hidroelectrica Dogan Holding Atlantic Grupa BGEO Ciech LiveChat Software PORR Poland Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Pekao Cimsa Luxoft Raiffeisen Bank Agora OMV Petrom Ford Otosan CCC Bank Zachodni WBK Dogus Otomotiv Magyar Telekom RHI Alior Bank Romgaz Garanti Coca-Cola Icecek Bucharest Stock Exchange Ford Otosan O2 Czech Republic Uniqa AmRest SIF-2 Moldova Halkbank DIXY CSOB Grupa Azoty Orange Polska Vienna Insurance Group Asseco Poland Transelectrica Lokman Hekim Eurocash Erste Bank Grupa Kęty OTE Warimpex Bank Millennium Transgaz Migros Ticaret Folli Follie Eurobank HMS Group Turk Telekom Wienerberger Bank Pekao Pegasus Airlines Fortuna Garanti Industrial Milk Company Wirtualna Polska Holding Bank Zachodni WBK Russia Sabanci Holding Gorenje Getin Noble Bank Intercars Croatia CCC DIXY Teknosa Hellenic Petroleum Halkbank Mytilineos Atlantic Grupa Ciech Gazprom Tofas Kernel Hellenic Bank Pegas Nonwovens Podravka Cyfrowy Polsat S.A. -

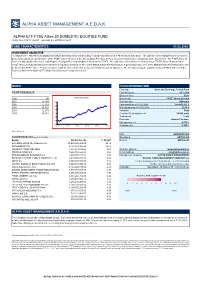

Alpha Asset Management Α.Ε.D.Α.Κ

ALPHA ASSET MANAGEMENT Α.Ε.D.Α.Κ. ALPHA ETF FTSE Athex 20 DOMESTIC EQUITIES FUND HCMC Rule 789/13.12.2007 Gov.Gaz. s.n. 2474/B/31.12.07 FUND CHARACTERISTICS 01.02.2008 INVESTMENT OBJECTIVE The Alpha ETF FTSE Athex 20 DOMESTIC EQUITIES FUND is the first Exchange Traded Fund listed on the Athens Stock Exchange. The objective of the Mutual Fund’s investment policy is to replicate the performance of the FTSE® Athex 20 Index of the Athens Stock Exchange in Euro, by mirror matching the composition of the Benchmark. The FTSE® Athex 20 Index is a big capitalization Index, capturing the 20 largest blue chip companies listed on the ATHEX. The total value of investments in shares of the FTSE® Athex 20 Index and in FTSE® Athex 20 Index derivatives accounts for a regulatory minimum of 95% of the Mutual Fund’s Net Asset Value. A percentage up to 35% of the Mutual Fund’s Net Asset Value may be invested in FTSE® Athex 20 Index derivatives with the aim of achieving the Mutual Fund’s investment objectives. The derivatives may be tradable (such as FTSE® Athex 20 Index futures) and/or non-tradable (OTC Swap Transactions) in a regulated market. INDEX FUND INFORMATION Fund type Domestic Exchange Traded Fund PERFORMANCE First listing date 24.1.2008 Base currency Euro Year (%) FTSE Athex 20 Index Benchmark FTSE® Athex 20 Index 2007 15,79% 3300 Currency risk Minimum 2006 17,73% Fund assets as of 01.02.2008 141.403.221 € 2800 2005 30,47% Net unit price as of 01.02.2008 23,40 € 2004 32,27% 2300 Valuation Daily 2003 35,43% 1800 Creation / Redemption unit 50.000 units 1300 Trading unit 1 unit Dividends Annual - 30 June 800 Management fee 0,275% 300 31/12/02 31/12/03 31/12/04 31/12/05 31/12/06 31/12/07 Custodian fee 0,100% Source: Bloomberg ISIN GRF000013000 COMPOSITION (as of 01.02.2008) Bloomberg AETF20 GA Equity Market Cap (€) % Weight Reuters AETF20.AT NATIONAL BANK OF GREECE S.A. -

Speakers CV Speakers CV

2 Speakers CV Speakers CV Opening Session John Chadjivassiliadis Chairman ΙΕΝΕ Dipl. Mechanical and Electrical Engineer of the NTUA (1960) is expert in the development of the renewable energy sources and sustainable power systems. Worked for the Public Power Corporation (1962-1990) in the department of power generation, he was director of power plants, and project manager in large power plants. From the mid-1970s John was in charge of the development of wind and solar energy projects for power generation with the successful Windpark of Kythnos, the first in Europe (1982) and the biggest hybrid by wind and solar PV. Since 1990, he is consultant engineer in energy, especially in the renewable energy sources, energy efficiency and sustainable development. For many years he served as an expert in evaluating research proposals and programs, coordinator and technical assistant of large research projects for RES integration into the networks within the European Commission research programs. John has been a scientific committee member in a number of European and international conferences, invited lecturer in international events and conferences where he presented over 80 papers. H e is founding Member of the European Wind Energy Association (EWEA, 1982), member of national and EU missions for international cooperation in scientific research and technology, founding Member and Secretary General of IENE, National Representative in the Mirror Group of the European PV Technology Platform, Member of the Scientific Committee of the Hellenic Association of Mechanical and Electrical Engineers, Major in Reserve of the Hellenic Army in the Technical Corp. John is the recipient of the “Prize Aeolus” Award, for his contribution in wind energy development, by the Hellenic Wind Energy Association-member of EWEA (2009), as well as of the “2010 PES Chapter Outstanding Engineer” Award, for his contribution in renewable energy research and development by the ΙΕΕΕ Power & Energy Society, PES Greece Chapter. -

Hellenic Petroleum – a Leading Energy Group in SE Europe

Credit Update June 2014 Contents • Introduction – Group Overview • Strategy update • Industry & market developments • Credit update • Strategic business units (SBUs) • Appendix 1 Group’s Profile • Largest SEE independent downstream Group, with investments in Power & Gas – €10b Turnover with 14 MT of product sales, with strong export orientation (50% exports) – Leading Greek market position covering c. 60- 65% of local wholesale market fuels demand – Regional footprint through subsidiaries; coastal refineries provide supply chain advantage • Completed its strategic investment plan, with positive cash flow impact – A €2bn investment plan with €150-200m of incremental cash flow opportunity at mid-cycle margins; no material capex requirements – Asset portfolio allows upside on recovery of refining margins and Greek market • Successfully implemented a transformation competitiveness improvement plan on Group structure and operational model – Transformation initiatives added c.€270m annual benefits with additional opportunities of €130m over the next 18-24 months • Consistent delivery of strategic targets; improving balance sheet – Achievement of strategic targets, despite Greek crisis & industry “black swans” – Continuous support from local and international relationship banks throughout crisis – Completion of capex cycle allows deleveraging from higher than target gearing – Opportunities for value monetisation (DEPA/DESFA sale process) 2 Complex refining asset base and leading domestic market share; Group positioned to benefit from Greek market -

Asset Development Plan 31 January, 2017

Asset Development Plan 31 January, 2017 Table of Contents 1. Regional Airports ................................................................................................................................................................................................................. 3 2. Hellinikon ............................................................................................................................................................................................................................. 4 3. Afantou, Rhodes .................................................................................................................................................................................................................. 5 4. Hellenic Gas Transmission System Operator (DESFA) ......................................................................................................................................................... 6 5. Piraeus Port Authority (OLP) ................................................................................................................................................................................................ 7 6. Thessaloniki Port Authority S.A. (OLTH) .............................................................................................................................................................................. 8 7. 10 Port Authorities .............................................................................................................................................................................................................. -

Ellaktor Group Presentation De

Group Presentation December 2013 Recent Developments / 9M2013 Financial Highlights The agreements for the re-initiation of the suspended BOT projects of Argean Motorways and Olympia Odos have been submitted for approval to the parliament of the Hellenic Republic - financial close targeted in December 2013 Revenues in 9Μ 2013 reached € 884.5 ml, slightly increased (1.7%) compared to 9M2012, mainly as a result of increased revenues in Construction Operating profit (EBIT) reached € 83.9 ml Profit before tax reached € 42.9 ml, decreased by 13.8% vs 9M 2012 After tax (before minorities) the group reported losses of € 12.0 ml vs profits of € 26.8 ml in 9M 2012, negatively affected by increased deferred taxation of ~ € 25 ml as a result of the corporate tax rate increase from 20% to 26% (mainly impacting Attiki Odos) - no withholding tax on dividend distribution is expected on future dividend inflows from group companies that will have a net positive cash flow effect for the group Total construction backlog stands at ~ € 3.2 bn (incl. ~ € 390 ml of contracts pending signature) Negotiations for the re-initiation of the suspended BOT projects are in their final stages Corporate related Net Debt as of 30/9/2013 reached € 438.3 ml vs € 513.2 ml as of 31/12/2012, mainly due to an increase in cash - refinancing of corporate debt at ELLAKTOR and AKTOR Concessions is at its final stages of documentation and is expected to be signed by year end 2013 9eld0029 2 Key Investment highlights Leading infrastructure player in Greece with an increasing international footprint Significant values from participation in Eldorado Well-balanced diversified Gold / Hellas Gold portfolio of activities Growth prospects in Waste Unrivalled construction Management and knowhow (backlog Renewable Energy c.€3.2bn) Strong expected dividend stream from mature concessions (i.e. -

Public Power Corporation S.A

PUBLIC POWER CORPORATION S.A. Interim Condensed Consolidated and Separate Financial Statements for the three month period from January 1, 2010 to March 31, 2010 in accordance with International Financial Reporting Standards, adopted by the European Union The attached interim condensed consolidated and separate financial statements were approved by Public Power Corporation Board of Directors on May 19, 2010 and they are available in the web site of Public Power Corporation S.A. at www.dei.gr. Public Power Corporation S.A. Registration No 47829/06/Β/00/2 Chalkokondyli 30 - 104 32 Athens This page is left blank intentionally PUBLIC POWER CORPORATION S.A. INTERIM CONDENSED FINANCIAL STATEMENTS (SEPARATE AND CONSOLIDATED) FOR THE THREE MONTH PERIOD ENDED MARCH 31, 2010 CONTENTS Page A1. INTERIM CONDENSED FINANCIAL STATEMENTS ......................................................................... 2 A2. NOTES TO THE INTERIM CONDENSED FINANCIAL STATEMENTS ........................................... 9 1. CORPORATE INFORMATION ............................................................................................................... 10 2. CHANGES IN LEGAL FRAMEWORK ................................................................................................... 10 3. BASIS OF PRESENTATION FOR THE INTERIM CONDENSED FINANCIAL STATEMENTS... 13 4. SEASONALITY OF OPERATIONS ........................................................................................................ 16 5. INVESTMENTS IN SUBSIDIARIES ...................................................................................................... -

Delos Pet Ote Balanced Fund H.C.M.C

DELOS PET OTE BALANCED FUND H.C.M.C. Rule 3/261/26-7-2001 NBG Asset Management MFMC 103-105 Syngrou Avenue 117 45, Athens Greece Risk Profile Tel. +30 210 900 7400 Fax.+30 210 900 7499 www.nbgam.gr The investment objective of the Mutual Fund is the highest possible return, through income and the capital appreciation of its investments. The Mutual Fund invests mainly in a combination of equities, sovereign and corporate fixed income securities, money-market instruments, and derivative instruments. Report Date 31/03/2017 FUND INFORMATION PERFORMANCE MUTUAL FUND Currency EUR 3 Years Cumulative Return (31/03/2014- Fund Size (mm) 8,55 31/03/2017) Launch Date 7/11/2001 0% ISIN GRF000011004 -5% Bloomberg Code DELPOIB GA EQUITY -10% RETURNS -15% Ytd 1year 3year -20% (01/01/2017- (31/03/2016- (31/03/2014- -25% 31/03/2017) 31/03/2017) 31/03/2017) Mutual Fund 2,11% 9,68% -16,09% -30% Until 15/02/2017 the Mutual Fund used the following benchmark: 25% ATHEX Composite Share Price Index, 20% Dj Eurostoxx 50, 20% ΙΒΟΧΧ € CRP TR 1-3 15% Bloomberg/EFFAS Bond Indices Greece Govt All > 1 Yr TR, 20% EONIA Total Return Since 16/02/2017 the Mutual Fund does not use Benchmark. STATISTICAL DATA (3 years rolling) (31/03/2014-31/03/2017) ASSET ALLOCATION Fund Equity Sharpe Ratio -0,61 45,8% Annualised Standard Deviation 13,23% Equity Funds Maximum Monthly Return 6,73% 5,0% Minimum Monthly Return -7,41% Cash / Months with Positive Return 20 Equivalents Months with Negative Return 16 2,6% Top 10 Holdings Gov't Bonds Corporate 23,2% Bonds HELLENIC REPUBLIC 4 3/4 04/17/19 3,3% 23,4% NBGAM ETF ATHEX GEN DOM EQTY 3,1% GE CAPITAL EURO FUNDING 5 3/8 01/16/18 2,4% Bond Portfolio Characteristics TITAN GLOBAL FINANCE PLC 3 1/2 06/17/21 2,4% MOTOR OIL FINANCE PLC 5 1/8 05/15/19 2,4% Duration 4,89 MOTOR OIL FINANCE PLC 3 1/4 04/01/22 2,3% Yield to Maturity 4,50% ALPHA BANK AE 2,3% Years to Maturity 7,14 OPAP SA 2,0% Coupon 3,63% MOTOR OIL (HELLAS) SA 1,9% MYTILINEOS HOLDINGS S.A. -

Energy Greece Sectors in Focus

Energy Greece Sectors in focus April 2020 2 Disclaimer This report, issued by Alpha Bank, is provided for information purposes only. The information it contains has been obtained from sources believed to be reliable but not verified by Alpha Bank and consist an expression of opinion based on available data at a particular date. This report does not constitute an advice or recommendation nor is it an offer or a solicitation of an offer for any kind of transaction and therefore factors such as knowledge, experience, financial situation and investment targets- of each one of the potential or existing clients- have not been taken into consideration and have not been tested for potential taxation of the issuer at the source neither for any other tax consistency arising from participating in them. Furthermore, it does not constitute investment research and therefore it has not been prepared in accordance with the legal requirements regarding the safeguarding of independence of investment research. Alpha Bank has no obligation to review, update, modify or amend this report or to make announcements or notifications in the event that any matter stated herein or any opinion, projection, forecast or estimate set forth herein, changes or is subsequently found to be inaccurate. Eventual predictions related to the evolution of the economic variables and values referred to this report, consist views of Alpha Bank based on the data contained in it. No representation or warranty, express or implied, is made as to the accuracy, completeness or correctness of the information and opinions contained herein, or the suitability thereof for any particular use, and no responsibility or liability whatsoever is accepted by Alpha Bank and its subsidiaries, or by their directors, officers and employees for any direct or indirect damage that may result from the use of this report or the information it contains, in whole or in part.