Fisher's Equation and the Inflation Risk Premium in a Simple

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Deflation and the Fisher Equation

Economic SYNOPSES short essays and reports on the economic issues of the day 2010 ■ Number 27 Deflation and the Fisher Equation William T. Gavin, Vice President and Economist rving Fisher (1867-1947), one of America’s greatest federal funds rate was 2.18 percent and, in the 1980s, it I monetary economists, is famous for many reasons. was a whopping 4.61 percent. One of the most important is the Fisher equation, which states that the nominal interest rate is equal to the real interest rate plus the expected inflation rate. This is a So, according to Irving Fisher, statement about equilibrium in the market for bonds, not one reason to worry about deflation is about the factors that determine these two components. that the federal funds rate is expected Depending on which market rate is used, the expected real return will include a premium for various sources of to be held near zero as the economy risk. For most of post-WWII U.S. history, estimates of this grows out of this recession. risk premium in the federal funds market have been small relative to estimates of the risk-free real interest rate and the expected inflation rate, so they are ignored in this essay. With the federal funds rate near zero since December The chart shows the Fed’s policy rate—the federal funds 2008 and expected to remain there for the next year or two, rate—and the consumer price index (CPI) inflation trend. the Fisher equation has important implications for the The trend is measured as a 25-month centered moving expected inflation rate. -

A Lower Bound on Real Interest Rates by Jesse Aaron Zinn

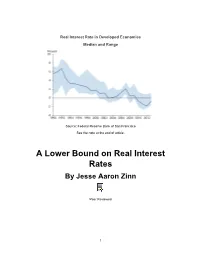

Real Interest Rate in Developed Economies Median and Range Source: Federal Reserve Bank of San Francisco See the note at the end of article. A Lower Bound on Real Interest Rates By Jesse Aaron Zinn Peer Reviewed 1 Jesse Aaron Zinn is an Assistant Professor of Economics in the College of Business at Clayton State University. His research interests include macroeconomics, public finance, and developmental economics. He earned his PhD in Economics at University of California, Santa Barbara. Abstract In this short article, the author demonstrates that real interest rates cannot be lower than -1 (i.e. -100%). He discusses how the textbook approximation to the Fisher equation can lead to the erroneous belief that there is no lower bound on real interest rates. He also speculates that the widespread use of the Fisher equation is why we had yet to realize that a lower bound on real rates exists. This leads him to advocate using and teaching the exact Fisher equation, rather than its approximation. Introduction Negative real interest rates have been common in the United States and other countries since the financial crisis of 2007-8. In fact, Japan has often had negative real interest rates going back to the early 1990s. In some countries, such as Denmark and Switzerland, there have been cases where nominal interest rates have also turned negative, disproving the idea that zero is an impenetrable lower bound on nominal rates. These phenomena have, no doubt, lead many to wonder how low rates can go. The objective of this short piece is to demonstrate the existence of a lower bound on real rates of interest. -

Real Interest Rate and Fisher Equation

6. Real interest rate, Fisher equation, Fisher effect 1. Real interest rate The real interest rate of an economy represents the purchasing power of the economy’s nominal interest rate : it is the nominal rate expressed in terms of goods. That the nominal interest rate between period and period 1 is means that, by lending 1 currency unit in , one gets 1 currency units in 1. That the real interest rate between period and period 1 is means that, by lending 1 unit of goods int , one gets 1 units of goods in 1. Thus, expresses purchasing power: the amount of goods obtained from each unit of good lent. 2. An example on the real interest rate Let “goods” be represented by the CPI basket. There are two periods, 1 and 2. The nominal interest rate between 1 and 2 is 10%. The cost of the CPI basket in 1 is 204 EUR. The cost of the CPI basket in 2 is 220 EUR; see the sketch on the right. With this information, the CPI inflation rate is 220 204 7.84%. 204 If 612 EUR are lent in 1. Then 612 1 612 1 0.10 673.2 EUR are obtained in 2. In 1, the purchasing power of 612 EUR is 612/ 612/204 3 baskets. In 2, the purchasing power of 673.2 EUR is 673.2/ 673.2/220 3.06 baskets. The real interest rate measures the change in purchasing power of the money lent. Specifically, transforms 3 baskets into 3.06 baskets. Thus, satisfies 3 1 3.06, so 0.02 2%. -

IRVING FISHER – Forerunner of Monetarism

PROFILES OF WORLD ECONOMISTS IRVING FISHER – forerunner of monetarism doc. Ing. Ján Iša, DrSc. Irving Fisher (1867 to 1947), who the theory of capital and interest, the theo- J. A. Schumpeter labelled as the greatest ry of index numbers and accounting, the theoretical economist of America, signifi- ”Phillips curve” and economic research cantly contributed to numerous spheres of methodology. economic theory and statistics. Perhaps he Fisher was the first American mathemati- is most known for his contribution to the de- cal economist, entrepreneur, reformer and velopment of the modern quantity theory, lecturer. Irving Fisher was born on 27th February, 1867 in Saugerti- He was appointed a full professor of economics in 1898 and es (New York) and lived in New Haven (Connecticut). Over ti- worked at Yale University actively up until 1920, afterwards me Fisher attended gradually schools in Peace Dale (Rhode Is- devoting his time mainly to writing books (of his 28 books pub- land), New Haven (Connecticut) and Saint Louis (Missouri). lished 18 dealt with economic theory) and a number of various Just at the time when he had finished secondary school and ga- activities outside the university. He taught only on a part-time ined a place at Yale College, his father died, leaving Irving 500 basis and therefore had less of an influence on students and, in dollars for his college education. contrast to other eminent architects of economic science (for At Yale University he studied mathematics, science, sociolo- example J. M. Keynes); he did not create a distinctive economic gy and philosophy. His most eminent teachers were the mathe- school. -

Nber Working Paper Series Searching for Irving Fisher

NBER WORKING PAPER SERIES SEARCHING FOR IRVING FISHER Kris James Mitchener Marc D. Weidenmier Working Paper 15670 http://www.nber.org/papers/w15670 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 January 2010 We thank Michael Bordo, Richard Burdekin, Andy Rose, Eric Swanson, and participants at UC Berkeley, the San Francisco Fed, and the ASSA meetings for comments and suggestions. Mitchener acknowledges the generous financial support of the Hoover Institution while in residence as the W. Glenn Campbell and Rita Ricardo-Campbell National Fellow. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2010 by Kris James Mitchener and Marc D. Weidenmier. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Searching for Irving Fisher Kris James Mitchener and Marc D. Weidenmier NBER Working Paper No. 15670 January 2010 JEL No. E4,G1,N2 ABSTRACT There is a long-standing debate as to whether the Fisher effect operated during the classical gold standard period. We break new ground on this question by developing a market-based measure of general inflation expectations during the gold standard. Since the gold-silver price ratio was widely used to track inflation during the gold standard period, we are able to derive a measure of inflation expectations using the interest-rate differential between Austrian silver and gold perpetuity bonds with identical terms. -

MONEY and BANKING

MONEY and BANKING: ECON 3115 Revised, Fall 2011 Professor Benjamin Russo Chapter 4: Understanding Interest Rates To simplify discussion these notes ignore important economic differences between financial intermediaries and financial markets. Instead, the notes treat the financial system as one big happy family. Outline I) What is the „Present Value‟ of an Asset? How is Present Value Calculated? II) Interest Rates and Yield to Maturity III) Interest Rates versus Rates of Return IV) Interest Rate Risk V) “The” Interest Rate and Economic Efficiency VI) The Real Interest Rate versus the Nominal Interest Rate I) What is the „Present Value‟ of an Asset? How is Present Value Calculated? 1) Present Value (PV) is a fundamental concept in financial economics. For this reason, you need to understand the concept and how to calculate it. Start with the concept. Generally speaking, the PV of an asset is the current value of future income the asset is expected to produce, after the future income is discounted by the "opportunity cost of owning the asset." The opportunity cost of owning an asset is the future income that could have been earned if the owner had bought the next best alternative asset. E.G., suppose Ms. Penny-pincher ranks four different assets with the colorful names Red, Blue, Green, and Fuchsia. Ms. P. ranks Blue highest, and buys only Blue. She ranks Green second highest, but does not buy Green. Thus, Ms. P. foregoes the opportunity to earn income from Green. The foregone Green income is the opportunity cost of owning Blue. 2) The opportunity cost of owning an asset often is called the "time value of money" because it is the value one could have achieved, over time, had "money" been invested differently. -

Chapter 8 - Theories of FX Determination – Part 2 Goal Get a Formula for St

Rauli Susmel FINA 4360 – International Financial Management Dept. of Finance Univ. of Houston Chapter 8 - Theories of FX Determination – Part 2 Goal get a formula for St. St = f( id, if,Id, If,…) Last Lecture Effect of LOOP (arbitrage through trade) on FX Markets. Derive “equilibrium” (i.e., no-trade) St: Absolute PPP: St = Pd / Pf (Rejected, existence of transaction costs, borders a problem) Relative PPP: ef, Id - If (Rejected in the short-run, some long-run support) This Lecture Continue the search for a functional form that explains St. 8.2 International Fisher Effect (IFE) IFE builds on the law of one price, but for financial transactions. Idea: Expected returns to international investors who invest in money markets in their home country should be equal to the expected returns they would get if they invest in foreign money markets once adjusted for currency fluctuations. Exchange rates will be set in such a way that international investors cannot profit from interest rate differentials. The "effective" T-day return on a foreign bank deposit is: rd (f) = (1 + if * T/360) (1 + ef,T) -1. On the other hand, the effective T-day return on a home bank deposit is: rd (d) = id * T/360. Setting rd (d) = rd (f) and solving for ef,T = (St+T/St - 1) we get: S (1 i *T /360) e IFE T t 1 d 1 (IFE). f ,T S (1 i *T /360) t f IFE Using a linear approximation: e f,T (id - if) x T/360. IFE e f,,T represents an expectation –i.e., E[ef,,T]. -

DEVOLUTION of the FISHER EQUATION: Rational Appreciation to Money Illusion*

View metadata, citation and similar papers at core.ac.uk brought to you by CORE GRIPS Policy Information Center provided by InsitutionalDiscussion Repository at the Paper National Graduate : 08-04 Institute for Policy Studies DEVOLUTION OF THE FISHER EQUATION: Rational Appreciation to Money Illusion* James R. Rhodes. June 2008 .Professor of Economics, National Graduate Institute for Policy Studies (GRIPS), 7-22-1 Roppongi, Minato-ku, Tokyo 106-8677 Japan TEL: +81-(0)3-6439-6220 E-mail: [email protected] *The author is indebted to Levis Kochin for providing the original stimulus for this paper and to the late Milton Friedman for sustaining interest. Thanks are also due Joerg Bibow, Yang Ming Chang, Dana Ferrell, Thomas Humphrey, the late Mark Meador, Perry Mehrling, Francisco de A. Nadal-De Simone, Sumimaru Odano, Frank Packer, Kenichi Sakakibara, Kenji Yamamoto, and several anonymous referees for helpful comments on earlier versions of the paper. Supplementary Notes on the Fisher Equations contains elaborations and extensions of material contained in the paper. Supplementary Notes is available from the author. © 2008 by James R. Rhodes. All rights reserved. GRIPS Policy Information Center Discussion Paper : 08-04 DEVOLUTION OF THE FISHER EQUATION: Rational Appreciation to Money Illusion Abstract In Appreciation and Interest Irving Fisher (1896) derived an equation connecting interest rates in any two standards of value. The original Fisher equation (OFE) was expressed in terms of the expected appreciation of money [percent change in E(1/P)] whereas the ubiquitous conventional Fisher equation (CFE) uses expected goods inflation [percent change in E(P)]. Since Jensen‟s inequality implies the non-equivalence of the two equations, the OFE is not subject to standard criticisms of non-rationality leveled against the CFE. -

An Empirical Investigation of the International Fisher Effect

2002:042 SHU BACHELOR’S THESIS An Empirical Investigation of the International Fisher Effect EMIL SUNDQVIST Social Science and Business Administration Programmes ECONOMICS PROGRAMME Department of Business Administration and Social Sciences Division of Economics Supervisor: Stefan Hellmer 2002:042 SHU • ISSN: 1404 – 5508 • ISRN: LTU - SHU - EX - - 02/42 - - SE An Empirical Investigation of the International Fisher Effect EMIL SUNDQVIST Social Science and Business Administration Programme Economics Programme Department of Business Administration and Social Sciences Division of Economics Supervisor: Stefan Hellmer V TABLE OF CONTENTS ABSTRACT I SAMMANFATTNING II LIST OF FIGURES V Chapter 1 INTRODUCTION 5 1.1 Purpose 6 1.2 Method 6 1.3 Scope 7 1.4 Outline 8 Chapter 2 THEORETICAL FRAMEWORK 8 2.1 Purchasing Power Parity 9 2.1.1 Empirical evidence 10 2.2 The Fisher Effect 11 2.2.1 Empirical evidence 14 2.3 The International Fisher Effect 14 2.3.1 Empirical evidence 17 Chapter 3 THE REGRESSION MODEL 17 3.1 The efficient market hypothesis 18 3.2 The regression model 19 3.3 The data 20 Chapter 4 THE REGRESSION RESULTS AND ANALYSIS 22 4.1 The regression results for United States-Sweden 23 4.2 The regression results for United States-Japan 25 4.3 The regression results for United States-United Kingdom 26 4.4 The regression results for United States-Canada 27 V 4.5 The regression results for United States-Germany 29 Chapter 5 CONCLUSIONS 31 REFERENCES 35 V LIST OF FIGURES Figure 2.1 Purchasing Power Parity 6 Figure 2.2 The Fisher Effect 9 Figure 2.3 -

Do Expected Shifts in Inflation Affect Estimates of the Long-Run Fisher Relation? Author(S): Martin D

American Finance Association Do Expected Shifts in Inflation Affect Estimates of the Long-Run Fisher Relation? Author(s): Martin D. D. Evans and Karen K. Lewis Source: The Journal of Finance, Vol. 50, No. 1 (Mar., 1995), pp. 225-253 Published by: Wiley for the American Finance Association Stable URL: http://www.jstor.org/stable/2329244 . Accessed: 08/10/2013 16:26 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. Wiley and American Finance Association are collaborating with JSTOR to digitize, preserve and extend access to The Journal of Finance. http://www.jstor.org This content downloaded from 128.91.113.15 on Tue, 8 Oct 2013 16:26:34 PM All use subject to JSTOR Terms and Conditions THE JOURNAL OF FINANCE * VOL. L, NO. 1 * MARCH 1995 Do Expected Shifts in Inflation Affect Estimates of the Long-Run Fisher Relation? MARTIN D. D. EVANS and KAREN K. LEWIS* ABSTRACT Recent empirical studies suggest that nominal interest rates and expected inflation do not move together one-for-one in the long run, a finding at odds with many theoretical models. This article shows that these results can be deceptive when the process followed by inflation shifts infrequently. -

Irving Fisher, the UIP Puzzle And

Irving Fisher and the UIP Puzzle Rachel A.J. Campbell Maastricht University and Tilburg University Faculty of Economics and Business Administration, Maastricht University, P.O. Box 616, 6200 MD Maastricht, The Netherlands, tel. +31 43 388-4827, e-mail: [email protected]. Kees G. Koedijk Tilburg University and CEPR Department of Economics, Tilburg University, P.O. Box 90153, 5000 LE Tilburg, The Netherlands, tel. +31 13 466-2915, e-mail: [email protected]. James R. Lothian (corresponding author) Fordham University Graduate School of Business, Fordham University, 113 West 60th Street, New York, NY 10023, USA, tel. +1 212 636-6147, e-mail: [email protected] ; [email protected] . Ronald J. Mahieu Tilburg University Department of Econometrics & Operations ResearchFinancial Management, Tilburg University, P.O. Box 90153, 5000 LE Tilburg, The Netherlands, tel. +31 13 466 8752, e-mail: [email protected]. February 2009 JEL Classification: F31, B19 Keywords: Exchange rates, forward discount bias, international parities, expectation errors, Irving Fisher. _________________ We would like to thank Richard Ballie, Menzie Chinn, John Cochrane, John Devereux, Hans DeWachter, Martin D.D. Evans, Paul de Grauwe, Franz Palm, Yusif Simaan, Daniel Thornton, Mathijs Van Dijk, Christian Wolff, Jun Yang and to seminar participants at Fordham University, Trinity College Dublin and University College Cork for helpful comments. Abstract In this paper we empirically verify much of the seminal work by Irving Fisher on uncovered interest parity, which he conducted over a century ago. Like Fisher, we find that the departures from UIP are connected to individual episodes in which errors surrounding exchange-rate expectations are persistent, but eventually transitory. -

Basics of Financial Mathematics

MINISTRY OF EDUCATION AND SCIENCE OF THE RUSSIAN FEDERATION Federal State-Funded Educational Institution of Higher Vocational Education «National Research Tomsk Polytechnic University» Department of Higher Mathematics and Mathematical Physics BASICS OF FINANCIAL MATHEMATICS A study guide 2012 BASICS OF FINANCIAL MATHEMATICS Author A. A. Mitsel. The study guide describes the basic notions of the quantitative analysis of financial transactions and methods of evaluating the yield of commercial contracts, investment projects, risk-free securities and optimal portfolio of risk-laden securities. The study guide is designed for students with the major 231300 Applied Mathematics, 230700 Application Informatics, and master’s program students with the major 140400 Power Engineering and Electrical Engineering. CONTENTS Introduction Chapter 1. Accumulation and discounting 1.1. Time factor in quantitative analysis of financial transactions 1.2. Interest and interest rates 1.3. Accumulation with simple ınterest 1.4. Compound interest 1.5. Nominal and effective interest rates 1.6. Determining the loan duration and interest rates 1.7. The notion of discounting 1.8. Inflation accounting at interest accumulation 1.9. Continuous accumulation and discounting (continuous interest) 1.10. Simple and compound interest rate equivalency 1.11. Change of contract terms 1.12. Discounting and accumulation at a discount rate 1.13. Comparison of accumulation methods 1.14. Comparing discounting methods Questions for self-test Chapter 2. Payment, annuity streams 2.1. Basic definitions 2.2. The accumulated sum of the annual annuity 2.3. Accumulated sum of annual annuity with interest calculation m times a year 2.4. Accumulated sum of p – due annuity 2.5.