IRVING FISHER – Forerunner of Monetarism

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Debt-Deflation Theory of Great Depressions by Irving Fisher

THE DEBT-DEFLATION THEORY OF GREAT DEPRESSIONS BY IRVING FISHER INTRODUCTORY IN Booms and Depressions, I have developed, theoretically and sta- tistically, what may be called a debt-deflation theory of great depres- sions. In the preface, I stated that the results "seem largely new," I spoke thus cautiously because of my unfamiliarity with the vast literature on the subject. Since the book was published its special con- clusions have been widely accepted and, so far as I know, no one has yet found them anticipated by previous writers, though several, in- cluding myself, have zealously sought to find such anticipations. Two of the best-read authorities in this field assure me that those conclu- sions are, in the words of one of them, "both new and important." Partly to specify what some of these special conclusions are which are believed to be new and partly to fit them into the conclusions of other students in this field, I am offering this paper as embodying, in brief, my present "creed" on the whole subject of so-called "cycle theory." My "creed" consists of 49 "articles" some of which are old and some new. I say "creed" because, for brevity, it is purposely ex- pressed dogmatically and without proof. But it is not a creed in the sense that my faith in it does not rest on evidence and that I am not ready to modify it on presentation of new evidence. On the contrary, it is quite tentative. It may serve as a challenge to others and as raw material to help them work out a better product. -

Deflation and the Fisher Equation

Economic SYNOPSES short essays and reports on the economic issues of the day 2010 ■ Number 27 Deflation and the Fisher Equation William T. Gavin, Vice President and Economist rving Fisher (1867-1947), one of America’s greatest federal funds rate was 2.18 percent and, in the 1980s, it I monetary economists, is famous for many reasons. was a whopping 4.61 percent. One of the most important is the Fisher equation, which states that the nominal interest rate is equal to the real interest rate plus the expected inflation rate. This is a So, according to Irving Fisher, statement about equilibrium in the market for bonds, not one reason to worry about deflation is about the factors that determine these two components. that the federal funds rate is expected Depending on which market rate is used, the expected real return will include a premium for various sources of to be held near zero as the economy risk. For most of post-WWII U.S. history, estimates of this grows out of this recession. risk premium in the federal funds market have been small relative to estimates of the risk-free real interest rate and the expected inflation rate, so they are ignored in this essay. With the federal funds rate near zero since December The chart shows the Fed’s policy rate—the federal funds 2008 and expected to remain there for the next year or two, rate—and the consumer price index (CPI) inflation trend. the Fisher equation has important implications for the The trend is measured as a 25-month centered moving expected inflation rate. -

Interest Rates and Expected Inflation: a Selective Summary of Recent Research

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Explorations in Economic Research, Volume 3, number 3 Volume Author/Editor: NBER Volume Publisher: NBER Volume URL: http://www.nber.org/books/sarg76-1 Publication Date: 1976 Chapter Title: Interest Rates and Expected Inflation: A Selective Summary of Recent Research Chapter Author: Thomas J. Sargent Chapter URL: http://www.nber.org/chapters/c9082 Chapter pages in book: (p. 1 - 23) 1 THOMAS J. SARGENT University of Minnesota Interest Rates and Expected Inflation: A Selective Summary of Recent Research ABSTRACT: This paper summarizes the macroeconomics underlying Irving Fisher's theory about tile impact of expected inflation on nomi nal interest rates. Two sets of restrictions on a standard macroeconomic model are considered, each of which is sufficient to iniplv Fisher's theory. The first is a set of restrictions on the slopes of the IS and LM curves, while the second is a restriction on the way expectations are formed. Selected recent empirical work is also reviewed, and its implications for the effect of inflation on interest rates and other macroeconomic issues are discussed. INTRODUCTION This article is designed to pull together and summarize recent work by a few others and myself on the relationship between nominal interest rates and expected inflation.' The topic has received much attention in recent years, no doubt as a consequence of the high inflation rates and high interest rates experienced by Western economies since the mid-1960s. NOTE: In this paper I Summarize the results of research 1 conducted as part of the National Bureaus study of the effects of inflation, for which financing has been provided by a grait from the American life Insurance Association Heiptul coinrnents on earlier eriiins of 'his p,irx'r serv marIe ti PhillipCagan arid l)y the mnibrirs Ut the stall reading Committee: Michael R. -

American Economic Association

American Economic Association /LIH&\FOH,QGLYLGXDO7KULIWDQGWKH:HDOWKRI1DWLRQV $XWKRU V )UDQFR0RGLJOLDQL 6RXUFH7KH$PHULFDQ(FRQRPLF5HYLHZ9RO1R -XQ SS 3XEOLVKHGE\$PHULFDQ(FRQRPLF$VVRFLDWLRQ 6WDEOH85/http://www.jstor.org/stable/1813352 $FFHVVHG Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/action/showPublisher?publisherCode=aea. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. American Economic Association is collaborating with JSTOR to digitize, preserve and extend access to The American Economic Review. http://www.jstor.org Life Cycle, IndividualThrift, and the Wealth of Nations By FRANCO MODIGLIANI* This paper provides a review of the theory Yet, there was a brief but influential inter- of the determinants of individual and na- val in the course of which, under the impact tional thrift that has come to be known as of the Great Depression, and of the interpre- the Life Cycle Hypothesis (LCH) of saving. -

Macroeconomic Dynamics at the Cowles Commission from the 1930S to the 1950S

MACROECONOMIC DYNAMICS AT THE COWLES COMMISSION FROM THE 1930S TO THE 1950S By Robert W. Dimand May 2019 COWLES FOUNDATION DISCUSSION PAPER NO. 2195 COWLES FOUNDATION FOR RESEARCH IN ECONOMICS YALE UNIVERSITY Box 208281 New Haven, Connecticut 06520-8281 http://cowles.yale.edu/ Macroeconomic Dynamics at the Cowles Commission from the 1930s to the 1950s Robert W. Dimand Department of Economics Brock University 1812 Sir Isaac Brock Way St. Catharines, Ontario L2S 3A1 Canada Telephone: 1-905-688-5550 x. 3125 Fax: 1-905-688-6388 E-mail: [email protected] Keywords: macroeconomic dynamics, Cowles Commission, business cycles, Lawrence R. Klein, Tjalling C. Koopmans Abstract: This paper explores the development of dynamic modelling of macroeconomic fluctuations at the Cowles Commission from Roos, Dynamic Economics (Cowles Monograph No. 1, 1934) and Davis, Analysis of Economic Time Series (Cowles Monograph No. 6, 1941) to Koopmans, ed., Statistical Inference in Dynamic Economic Models (Cowles Monograph No. 10, 1950) and Klein’s Economic Fluctuations in the United States, 1921-1941 (Cowles Monograph No. 11, 1950), emphasizing the emergence of a distinctive Cowles Commission approach to structural modelling of macroeconomic fluctuations influenced by Cowles Commission work on structural estimation of simulation equations models, as advanced by Haavelmo (“A Probability Approach to Econometrics,” Cowles Commission Paper No. 4, 1944) and in Cowles Monographs Nos. 10 and 14. This paper is part of a larger project, a history of the Cowles Commission and Foundation commissioned by the Cowles Foundation for Research in Economics at Yale University. Presented at the Association Charles Gide workshop “Macroeconomics: Dynamic Histories. When Statics is no longer Enough,” Colmar, May 16-19, 2019. -

Texte Intégral

Working Paper History as heresy: unlearning the lessons of economic orthodoxy O'SULLIVAN, Mary Abstract In spring 2020, in the face of the covid-19 pandemic, central bankers in rich countries made unprecedented liquidity injections to stave off an economic crisis. Such radical action by central banks gained legitimacy during the 2008-2009 global financial crisis and enjoys strong support from prominent economists and economic historians. Their certainty reflects a remarkable agreement on a specific interpretation of the Great Depression of the 1930s in the United States, an interpretation developed by Milton Friedman and Anna Schwartz in A Monetary History of the United States (1963). In this article, I explore the origins, the influence and the limits of A Monetary History’s interpretation for the insights it offers on the relationship between theory and history in the study of economic life. I show how historical research has been mobilised to show the value of heretical ideas in order to challenge economic orthodoxies. Friedman and Schwartz understood the heretical potential of historical research and exploited it in A Monetary History to question dominant interpretations of the Great Depression in their time. Now that [...] Reference O'SULLIVAN, Mary. History as heresy: unlearning the lessons of economic orthodoxy. Geneva : Paul Bairoch Institute of Economic History, 2021, 38 p. Available at: http://archive-ouverte.unige.ch/unige:150852 Disclaimer: layout of this document may differ from the published version. 1 / 1 FACULTÉ DES SCIENCES DE LA SOCIÉTÉ Paul Bairoch Institute of Economic History Economic History Working Papers | No. 3/2021 History as Heresy: Unlearning the Lessons of Economic Orthodoxy The Tawney Memorial Lecture 2021 Mary O’Sullivan Paul Bairoch Institute of Economic History, University of Geneva, UniMail, bd du Pont-d'Arve 40, CH- 1211 Genève 4. -

5. Monetary Policy and Monetary Reform: Irving Fisher’S Contributions to Monetary Macroeconomics

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Loef, Hans E.; Monissen, Hans G. Working Paper Monetary policy and monetary reform: Irving Fisher's contributions to monetary macroeconomics W.E.P. - Würzburg Economic Papers, No. 11 Provided in Cooperation with: University of Würzburg, Chair for Monetary Policy and International Economics Suggested Citation: Loef, Hans E.; Monissen, Hans G. (1999) : Monetary policy and monetary reform: Irving Fisher's contributions to monetary macroeconomics, W.E.P. - Würzburg Economic Papers, No. 11, University of Würzburg, Department of Economics, Würzburg This Version is available at: http://hdl.handle.net/10419/48451 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu W. E. P. Würzburg Economic Papers Nr. -

A Classical View of the Business Cycle

NBER WORKING PAPER SERIES A CLASSICAL VIEW OF THE BUSINESS CYCLE Michael T. Belongia Peter N. Ireland Working Paper 26056 http://www.nber.org/papers/w26056 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 July 2019 We are especially grateful to David Laidler for his encouragement during the development of this paper and to John Taylor, Kenneth West, two referees, and seminar participants at the Federal Reserve Bank of Atlanta for helpful comments on previous drafts. All errors that remain are our own. Neither of us received any external support for, or has any financial interest that relates to, the research described in this paper. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2019 by Michael T. Belongia and Peter N. Ireland. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. A Classical View of the Business Cycle Michael T. Belongia and Peter N. Ireland NBER Working Paper No. 26056 July 2019 JEL No. B12,E31,E32,E41,E43,E52 ABSTRACT In the 1920s, Irving Fisher extended his previous work on the Quantity Theory to describe, through an early version of the Phillips Curve, how changes in the money stock could be associated with cyclical movements in output, employment, and inflation. -

The Fisher Relation in the Great Depression and the Great Recession*

The Fisher Relation in the Great Depression and the Great Recession* by David Laidler Abstract. The Fisher relation played a very different role in debates surrounding the Great Depression and the more recent Great Recession. This paper explores some of these differences, and suggests an explanation for them derived from a sketch of the idea’s evolution between the two events, thus providing a brief case study of the interaction of economic ideas and economic events that is a central feature.of the History of Economic Thought. JEL Classifications: B22, B26, E31, E32, E43. Key words: Interest rates, nominal vs. real, Inflation, deflation, expectations, depression, recession, Keynesian economics, monetarism, monetary policy. *This essay builds upon a section of an earlier and longer paper: “Two Crises, Two Ideas and One Question” (EPRI Working Paper 2012-4) and incorporates material from it. Correspondence and discussion with Michael Belongia, Lars Christensen, Tim Congdon, Peter Howitt, Thomas Humphrey, Douglas Irwin Richard Lipsey Perry Mehrling, Edward Nelson and Michael Parkin are gratefully acknowledged The so-called Fisher relation plays a central part in today's work-horse models of monetary policy and it often finds a place in general discussion of such issues far beyond the boundaries of the academic literature. It had been making appearances in monetary debates long before the Great Depression began, indeed long before Irving Fisher himself discussed it with such skill and thoroughness in (1896) that his name became firmly and perpetually attached to it.1 Even so, this idea’s specific place in macroeconomics has changed considerably over the years. -

Extensions to Notes on Macroeconomics Thomas J. Sargent July 1976 Working Paper

1 Extensions to Notes on Macroeconomics Thomas J. Sargent July 1976 Working Paper #: 64 Rsch. File #: 299.1 Not for Distribution The views expressed herein are solely those of the author and do not necessarily represent the views of the Federal Reserve Bank of Minneapolis or the Federal Reserve System. r- -r 1 4 Extensions to Notes on Macroeconomics by Thomas Sargent July 1976 __ Contents I. In Defense of Keynesian Analyses that "Ignore" the Government's Budget Constraint II. Linear Least Squares Projection (Regressions) The Orthogonality Condition Recursive Projection The Signal Extraction Problem The Term Structure of Interest Rates III. Notes on the Consumption Function The Cross Section Data The Time Series Simulating the Model: Response to an Unexpected Change in Income Response to a Change in the Trend Rate of Growth of Income Response to a Random Tax Credit Compatability of Friedman's Model with the Time Series Regressions Testing the Model IV, The Phillips Curve V. Investment Under Uncertainty VI. Optimal Monetary Policy Optimal Control with Ad Hoc Expectations An Example The Information Variable Problem Optimal Control Under Rational Expectations Which View Does the Evidence Favor? Should the Monetary Authority Use Interest or Money as Its Instrument? In Defense of Keynesian Analyses That "Ignore" the Government's Budget Constraint Following the appearance of Carl Christ's article, it has been common to hear the textbook Keynesian model criticized for ignoring the fact that the government has a budget constraint. Christ and others have claimed that various Keynesian multiplier formulas are mistaken because they ignore the government's budget constraint. -

The Fisher Relation in the Great Depression and the Great Recession

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Laidler, David Working Paper The Fisher Relation in the Great Depression and the Great Recession EPRI Working Paper, No. 2013-2 Provided in Cooperation with: Economic Policy Research Institute (EPRI), Department of Economics, University of Western Ontario Suggested Citation: Laidler, David (2013) : The Fisher Relation in the Great Depression and the Great Recession, EPRI Working Paper, No. 2013-2, The University of Western Ontario, Economic Policy Research Institute (EPRI), London (Ontario) This Version is available at: http://hdl.handle.net/10419/70277 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen -

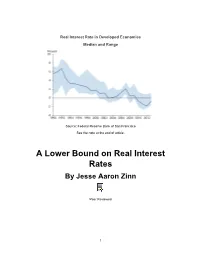

A Lower Bound on Real Interest Rates by Jesse Aaron Zinn

Real Interest Rate in Developed Economies Median and Range Source: Federal Reserve Bank of San Francisco See the note at the end of article. A Lower Bound on Real Interest Rates By Jesse Aaron Zinn Peer Reviewed 1 Jesse Aaron Zinn is an Assistant Professor of Economics in the College of Business at Clayton State University. His research interests include macroeconomics, public finance, and developmental economics. He earned his PhD in Economics at University of California, Santa Barbara. Abstract In this short article, the author demonstrates that real interest rates cannot be lower than -1 (i.e. -100%). He discusses how the textbook approximation to the Fisher equation can lead to the erroneous belief that there is no lower bound on real interest rates. He also speculates that the widespread use of the Fisher equation is why we had yet to realize that a lower bound on real rates exists. This leads him to advocate using and teaching the exact Fisher equation, rather than its approximation. Introduction Negative real interest rates have been common in the United States and other countries since the financial crisis of 2007-8. In fact, Japan has often had negative real interest rates going back to the early 1990s. In some countries, such as Denmark and Switzerland, there have been cases where nominal interest rates have also turned negative, disproving the idea that zero is an impenetrable lower bound on nominal rates. These phenomena have, no doubt, lead many to wonder how low rates can go. The objective of this short piece is to demonstrate the existence of a lower bound on real rates of interest.