FHA Title II Programs: 203(B) Mortgage Insurance Program

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Down Payment and Closing Cost Assistance

STATE HOUSING FINANCE AGENCIES Down Payment and Closing Cost Assistance OVERVIEW STRUCTURE For many low- and moderate-income people, the The structure of down payment assistance programs most significant barrier to homeownership is the down varies by state with some programs offering fully payment and closing costs associated with getting a amortizing, repayable second mortgages, while other mortgage loan. For that reason, most HFAs offer some programs offer deferred payment and/or forgivable form of down payment and closing cost assistance second mortgages, and still other programs offer grant (DPA) to eligible low- and moderate-income home- funds with no repayment requirement. buyers in their states. The vast majority of HFA down payment assistance programs must be used in combi DPA SECOND MORTGAGES (AMORTIZING) nation with a first-lien mortgage product offered by the A second mortgage loan is subordinate to the first HFA. A few states offer stand-alone down payment and mortgage and is used to cover down payment and closing cost assistance that borrowers can combine closing costs. It is repayable over a given term. The with any non-HFA eligible mortgage product. Some interest rates and terms of the loans vary by state. DPA programs are targeted toward specific popula In some programs, the interest rate on the second tions, such as first-time homebuyers, active military mortgage matches that of the first mortgage. Other personnel and veterans, or teachers. Others offer programs offer more deeply subsidized rates on their assistance for any homebuyer who meets the income second mortgage down payment assistance. Some and purchase price limitations of their programs. -

Commercial Mortgage Loans

STRATEGY INSIGHTS MAY 2014 Commercial Mortgage Loans: A Mature Asset Offering Yield Potential and IG Credit Quality by Jack Maher, Managing Director, Head of Private Real Estate Mark Hopkins, CFA, Vice President, Senior Research Analyst Commercial mortgage loans (CMLs) have emerged as a desirable option within a well-diversified fixed income portfolio for their ability to provide incremental yield while maintaining the portfolio’s credit quality. CMLs are privately negotiated debt instruments and do not carry risk ratings commonly associated with public bonds. However, our paper attempts to document that CMLs generally available to institutional investors have a credit profile similar to that of an A-rated corporate bond, while also historically providing an additional 100 bps in yield over A-rated industrials. CMLs differ from public securities such as corporate bonds in the types of protections they offer investors, most notably the mortgage itself, a benefit that affords lenders significant leverage in the relationship with borrowers. The mortgage is backed by a hard, tangible asset – a property – that helps lenders see very clearly the collateral behind their investment. The mortgage, along with other protections, has helped generate historical recovery from defaulted CMLs that is significantly higher than recovery from defaulted corporate bonds. The private CML market also provides greater flexibility for lenders and borrowers to structure mortgages that meet specific needs such as maturity, loan amount, interest terms and amortization. Real estate as an asset class has become more popular among institutional investors such as pension funds, insurance companies, open-end funds and foreign investors. These investors, along with public real estate investment trusts (REITs), generally invest in higher quality properties with lower leverage. -

The Real Estate Marketplace Glossary: How to Talk the Talk

Federal Trade Commission ftc.gov The Real Estate Marketplace Glossary: How to Talk the Talk Buying a home can be exciting. It also can be somewhat daunting, even if you’ve done it before. You will deal with mortgage options, credit reports, loan applications, contracts, points, appraisals, change orders, inspections, warranties, walk-throughs, settlement sheets, escrow accounts, recording fees, insurance, taxes...the list goes on. No doubt you will hear and see words and terms you’ve never heard before. Just what do they all mean? The Federal Trade Commission, the agency that promotes competition and protects consumers, has prepared this glossary to help you better understand the terms commonly used in the real estate and mortgage marketplace. A Annual Percentage Rate (APR): The cost of Appraisal: A professional analysis used a loan or other financing as an annual rate. to estimate the value of the property. This The APR includes the interest rate, points, includes examples of sales of similar prop- broker fees and certain other credit charges erties. a borrower is required to pay. Appraiser: A professional who conducts an Annuity: An amount paid yearly or at other analysis of the property, including examples regular intervals, often at a guaranteed of sales of similar properties in order to de- minimum amount. Also, a type of insurance velop an estimate of the value of the prop- policy in which the policy holder makes erty. The analysis is called an “appraisal.” payments for a fixed period or until a stated age, and then receives annuity payments Appreciation: An increase in the market from the insurance company. -

Private Mortgage Insurer Eligibility Requirements (Pmiers)

Private Mortgage Insurer Eligibility Requirements September 27, 2018 Contents Chapter Section Page Foreword Introduction 3 Effective Date 3 Amendments and Waivers 3 Defined Terms 3 Introduction 100 PMIERs Must be Met at All Times 4 101 Compliance with Laws 4 102 Applicable NAIC Regulations 5 103 Ownership/Corporate Governance 5 Application 200 Application Criteria 6 201 Application Submission 6 202 Application Fee/Other Costs 6 203 Newly-Approved Insurer Requirements 7 Business Requirements 300 Scope of Business 8 301 Organization 8 302 Policies, Procedures, Practices 8 303 Rebates, Commissions, Charges, and Compensating Balances 8 304 Separation of Responsibilities 8 305 Master Policies 9 306 Settlements and Changes to Freddie Mac’s Rights 9 307 Diversification Policies 9 308 Claims Processing 10 309 Loss Mitigation 11 310 Lender and Servicer Guidelines 11 311 Policies of Insurance 12 312 Insurance Data Reconciliation 12 313 Business Continuity Planning 12 314 Document Retention 12 Policy Underwriting 400 Overview 13 401 Evaluation of Loan Eligibility and Borrower Credit-worthiness 13 402 Property Valuation 13 403 Delegated Underwriting 14 404 Use of Automated Tools 14 405 Independent Validation for Early Rescission Relief and Credible 15 Evidence Quality Control 500 Quality Control Program 16 501 Discretionary Reviews 17 502 Post-Closing Review 18 503 Post-Closing QC Loan Sample Selection and Defect Rates 19 504 QC Reporting 20 505 Corrective Actions 21 506 Internal Audit 21 Lender Approval & 600 Lender Approval 22 Monitoring 601 Lender -

Your Step-By-Step Mortgage Guide

Your Step-by-Step Mortgage Guide From Application to Closing Table of Contents In this Guide, you will learn about one of the most important steps in the homebuying process — obtaining a mortgage. The materials in this Guide will take you from application to closing and they’ll even address the first months of homeownership to show you the kinds of things you need to do to keep your home. Knowing what to expect will give you the confidence you need to make the best decisions about your home purchase. 1. Overview of the Mortgage Process ...................................................................Page 1 2. Understanding the People and Their Services ...................................................Page 3 3. What You Should Know About Your Mortgage Loan Application .......................Page 5 4. Understanding Your Costs Through Estimates, Disclosures and More ...............Page 8 5. What You Should Know About Your Closing .....................................................Page 11 6. Owning and Keeping Your Home ......................................................................Page 13 7. Glossary of Mortgage Terms .............................................................................Page 15 Your Step-by-Step Mortgage Guide your financial readiness. Or you can contact a Freddie Mac 1. Overview of the Borrower Help Center or Network which are trusted non- profit intermediaries with HUD-certified counselors on staff Mortgage Process that offer prepurchase homebuyer education as well as financial literacy using tools such as the Freddie Mac CreditSmart® curriculum to help achieve successful and Taking the Right Steps sustainable homeownership. Visit http://myhome.fred- diemac.com/resources/borrowerhelpcenters.html for a to Buy Your New Home directory and more information on their services. Next, Buying a home is an exciting experience, but it can be talk to a loan officer to review your income and expenses, one of the most challenging if you don’t understand which can be used to determine the type and amount of the mortgage process. -

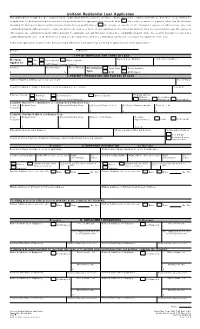

Sample Mortgage Application (PDF)

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower" or "Co-Borrower," as applicable. Co-Borrower information must also be provided (and the appropriate box checked) when the income or assets of a person other than the Borrower (including the Borrower's spouse) will be used as a basis for loan qualification or the income or assets of the Borrower's spouse or other person who has community property rights pursuant to state law will not be used as a basis for loan qualification, but his or her liabilities must be considered because the spouse or other person has community property rights pursuant to applicable law and Borrower resides in a community property state, the security property is located in a community property state, or the Borrower is relying on other property located in a community property state as a basis for repayment of the loan. If this is an application for joint credit, Borrower and Co-Borrower each agree that we intend to apply for joint credit (sign below): Borrower Co-Borrower I. TYPE OF MORTGAGE AND TERMS OF LOAN Agency Case Number Lender Case Number Mortgage VA Conventional Other (explain): Applied for: FHA USDA/Rural Housing Service Amount Interest Rate No. of Months Amortization Fixed Rate Other (explain): $%Type: GPM ARM (type): II. PROPERTY INFORMATION AND PURPOSE OF LOAN Subject Property Address (street, city, state & ZIP) No. of Units Legal Description of Subject Property (attach description if necessary) Year Built Purpose of Loan Purchase Construction Other (explain): Property will be: Primary Secondary Refinance Construction-Permanent Residence Residence Investment Complete this line if construction or construction-permanent loan. -

321 Part 213—Cooperative Housing Mortgage

Office of Assistant Secretary for Housing, HUD § 213.251 but not limited to the following organi- COOPERATIVE MANAGEMENT HOUSING zations: local management agents, INSURANCE AND DISTRIBUTIVE SHARES local management associations and 213.275 Nature of the Cooperative Manage- management agents with centralized ment Housing Insurance Fund. facilities. Owners of multiple projects 213.276 Allocation of Cooperative Manage- may centralize the electronic trans- ment Housing Insurance Fund income or losses. mission function. However, owners 213.277 Right and liability under the Coop- that contract out or centralize the erative Management Housing Insurance electronic transmission function are Fund. required to retain the ability to mon- 213.278 Distribution of distributive share. itor the day-to-day operations of the 213.279 Maximum amount of distributive share. project at the project site and be able 213.280 Finality of determination. to demonstrate that ability to the rel- evant HUD field office. Subpart C—Individual Properties Released From Project Mortgage; Expiring Program [58 FR 61022, Nov. 19, 1993, as amended at 59 FR 43475, Aug. 24, 1994] 213.501 Savings clause. AUTHORITY: 12 U.S.C. 1715b, 1715e; 42 U.S.C. PART 213—COOPERATIVE 3535(d). HOUSING MORTGAGE INSURANCE SOURCE: 36 FR 24553, Dec. 22, 1971, unless otherwise noted. Subpart A—Eligibility Requirements— Projects Subpart A—Eligibility Sec. Requirements—Projects 213.1 Eligibility requirements. § 213.1 Eligibility requirements. Subpart B—Contract Rights and The eligibility requirements set forth Obligations—Projects in 24 CFR part 200, subpart A, apply to multifamily project mortgages insured 213.251 Cross-reference. under section 213 of the National Hous- 213.252 Definitions. -

FICO Mortgage Credit Risk Managers Handbook

FICO Mortgage Credit Risk Manager’s Best Practices Handbook Craig Focardi Senior Research Director Consumer Lending, TowerGroup September 2009 Executive Summary The mortgage credit and liquidity crisis has triggered a downward spiral of job losses, declining home prices, and rising mortgage delinquencies and foreclosures. The residential mortgage lending industry faces intense pressures. Mortgage servicers must better manage the rising tide of defaults and return financial institutions to profitability while responding quickly to increased internal, regulatory, and investor reporting requirements. These circumstances have moved management of mortgage credit risk from backstage to center stage. The risk management function cuts across the loan origination, collections, and portfolio risk management departments and is now a focus in mortgage servicers’ strategic planning, financial management, and lending operations. The imperative for strategic focus on credit risk management as well as information technology (IT) resource allocation to this function may seem obvious today. However, as recently as June 2007, mortgage lenders continued to originate subprime and other risky mortgages while investing little in new mortgage collections and infrastructure, technology, and training for mortgage portfolio management. Moreover, survey results presented in this Handbook reveal that although many mortgage servicers have increased mortgage collections and loss mitigation staffing, few servicers have invested sufficiently in data management, predictive analytics, scoring and reporting technology to identify the borrowers most at risk, implement appropriate treatments for different customer segments, and reduce mortgage re-defaults and foreclosures. The content of this Handbook is based on a survey that FICO, a leader in decision management, analytics, and scoring, commissioned from TowerGroup, a leading research and advisory firm focusing on the strategic application of technology in financial services. -

Coinsurance 4330.4

COINSURANCE 4330.4 ___________________________________________________________________________ CHAPTER 5: COINSURED MORTGAGES ___________________________________________________________________________ 5-1 GENERAL. A. Claims on loans which were originated under the coinsurance * provisions of Section 244 of the National Housing Act, 12USC 1715Z-9 and are still within the period of coinsurance must * be filed in accordance with the provisions of this Chapter, unless the mortgage has been accepted by HUD for assignment. Under the coinsurance program the mortgagee does not convey the property to HUD in exchange for insurance benefits. After acquiring the property by foreclosure or deed-in-lieu of foreclosure, the mortgagee sells the property for the best price obtainable. The unpaid principal balance of the mortgage is reduced by the purchase price in computing insurance benefits. If the property is not sold within 6 months after acquisition, the unpaid principal balance is reduced by the appraised value of the property. HUD and the mortgagee share any loss arising out of the mortgage transaction. The lender exposure will be 10% of the actual loss subject to a "stop loss" of one percent of the total face amount of coinsured loans originated by the lender in same calendar year. B. HUD maintains a Coinsurance Reserve Account for each mortgagee by calendar year. A percentage of the annual mortgage insurance premium is credited, and the mortgagee's share of the loss is debited, to this account. C. Claims for insurance benefits under the coinsurance program may be filed only by an approved coinsuring mortgagee (See 24 CFR 204.5). During the coinsurance period servicing functions must be performed by an approved coinsuring mortgagee. -

Va Form 29-8636, Veterans Mortgage Life Insurance Statement

VETERANS MORTGAGE LIFE INSURANCE INSTRUCTIONS - PLEASE READ THE INSTRUCTIONS BEFORE COMPLETING THE ATTACHED VA FORM 29-8636, VETERANS MORTGAGE LIFE INSURANCE STATEMENT. INACCURATE INFORMATION MAY RESULT IN YOUR NOT BEING INSURED FOR THE FULL AMOUNT OF YOUR ENTITLEMENT. GENERAL DESCRIPTION OF COVERAGE Veterans Mortgage Life Insurance (VMLI) is designed to provide financial protection to cover an eligible veteran's outstanding home mortgage in the event of his/her death. This mortgage insurance program is administered by the Department of Veterans Affairs. The insurance is available only to disabled veterans, who, because of their disabilities, have received a Specially Adapted Housing Grant or a Special Housing Adaptation Grant from the Department of Veterans Affairs. Coverage for this insurance cannot be issued after age 69. MAXIMUM AMOUNT OF COVERAGE The maximum amount of VMLI allowed is $200,000. Veterans may select their level of coverage up to the maximum allowed by law, or their current mortgage balance, whichever is less. The amount payable at the time of death is computed according to the schedule of mortgage payments and does not include any amount arising from delinquent payments. The money is paid only to the mortgage holder (mortgage company, bank, etc.) THE MORTGAGE The mortgage is the mortgage secured on a specially adapted or modified residence purchased or remodeled in part with a grant from the Department of Veterans Affairs. If you had VMLI on a housing unit and you sold or otherwise disposed of that housing unit, you may obtain VMLI coverage for a mortgage loan on another eligible housing unit. SPECIAL PROVISIONS The housing unit which is security for the mortgage loan must be used by you as your residence. -

1 I. Introduction Interest Rates, Financial Leverage, and Asset Values Are

I. Introduction Interest rates, financial leverage, and asset values are among the most important variables in the economy. Many economists, policy makers, and investors believe that these variables may affect each other; therefore, manipulation of some variables may cause desired changes in the others. While interest rates are traditionally the variable that the Federal Reserve monitors and tries to influence, research on the recent financial crisis highlights the importance of financial leverage in the economy (see, e.g. Geanakoplos (2009), Acharya and Viswanathan (2011), among others). Recognizing this, Federal Reserve researchers are investigating whether changing requirements for mortgages’ loan-to-value ratios based on the economic environment could improve financial stability.1 The effectiveness of such policies would depend on how the loan to value ratios and property values exactly interact with each other, as well as whether and how they are endogenously determined. For example, if the two variables are only endogenously correlated and do not affect each other, policies that tries to manipulate the loan to value ratios to affect property values would have little effect. A natural starting point to understand the interactions between the loan to value ratios and property values is to understand their long-run equilibrium relationship. However, the existing literature is virtually silent on this very important issue. 1 See the speech by Ben S. Bernanke at the Annual Meeting of the American Economic Association at Philadelphia: http://www.federalreserve.gov/newsevents/speech/bernanke20140103a.htm. 1 This paper develops a very simple theoretical model in which commercial real estate mortgage interest rates, leverage, and property values are jointly determined. -

Suzanne Hutchinson Mortgage Insurance Companies of America

-" May 29, 2002 Financial Crimes Enforcement Network P.o. Box 39 Mortgage Vienna, VA 22183 Insurance Companies Re: Section 352 AMLP Regulations of America Dear Sir or Madam: This letter, on behalf of the Mortgage Suzanne C. Hutchinson Executive Vice President Insurance Companies of America ("MICA"), a trade association that represents the interests of private mortgage insurers throughout the United States, is in response to the Interim Final Rule published in the Federal Register (67 Fed. Reg. 21110) on April 29, 2002. The Interim Final Rule temporarily exempts certain financial institutions, including insurance companies, from the requirement that they establish anti-money laundering programs under the Bank Secrecy Act ("BSA"), 31 U.S.C., 18 U.S.C. § 5318(h) (1). This provision was added to the BSA by Section 352 of the USA PATRIOT Act. For the reasons discussed below, when expected regulations requiring compliance programs for insurance companies are issued, we respectfully request that private mortgage insurance companies be excluded from the definition of insurance and, consequently, not be required to establish and maintain.ananti-moneylaunderingprograms. The Rule states that: Treasury and FinCEN have not had the opportunity to identify the nature and scope of the money laundering or terrorist financing risks associated with [the exempt] businesses. The extension of the anti-money laundering program requirement to all the remaining financial institutions, most of which have never been subject to federal financial regulation, raises many significant practical and policy issues. An inadequate understanding of the affected 72715thSt., N.W. 12th Floor Washington,D.C.20005 (202)393-5566 Fax (202)393-5557 ..,,..,.""0 .-".