Second Supplement Dated 29 June 2017 to the Base Prospectus Dated 18 November 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Not to Be Published Or Distributed in the United States, Australia, Canada and Japan

NOT TO BE PUBLISHED OR DISTRIBUTED IN THE UNITED STATES, AUSTRALIA, CANADA AND JAPAN Italgas: 1 billion euros dual-tranche fixed rate bond issue successfully completed Milan, 5 February 2021 ! Today Italgas SpA (rating BBB+ by "#$%&' ())* +, -../,012 successfully priced a new dual tranche bond issue, due February 2028 and February 2033, both at fixed rate and for an amount of 500 million euros each, annual coupon of 0% and 0.5% respectively, under its EMTN Programme (Euro Medium Term Notes) established in 2016 and renewed by resolution of the Board of Directors on October 5, 2020. The transaction has gathered almost 3.4 billion euros of demand from a high quality and geographically diversified investor base. In particular, the 12-year tranche represents the corporate bond with the lowest coupon issued so far in Italy on that maturity. Taking advantage from favorable market conditions, the Company carried on its process of cost of debt optimization and refinancing risk reduction, further extending the average duration of the bond portfolio. Joint Bookrunners of the placement, restricted to institutional investors only, were BNP Paribas, J.P. Morgan Securities plc, Unicredit Bank AG, Intesa Sanpaolo S.p.A., Crédit Agricole CIB, Goldman Sachs International, Mediobanca S.p.A and Morgan Stanley. The bond will be listed on the Luxembourg Stock Exchange and the proceeds will be partially used to repurchase part of the two bonds maturing in 2022 and in 2024 subject to the tender offers launched this morning. Details of the two tranches are as -

Acquisition of Italgas and Stogit

SNAM RETE GAS HALF YEAR REPORT AT 30 JUNE 2009 / ACQUISITION OF ITALGAS AND STOGIT Acquisition of Italgas and Stogit On 30 June 2009, the acquisition of the entire share capital Gas of a consideration of € 4,509 million 1, including € of Italgas S.p.A. and Stogit S.p.A., the major players in the 2,922 million for Italgas and € 1,587 million for Stogit. The Italian natural gas distribution and storage sectors, respec- difference compared to the price agreed when signing the tively, from Eni was carried out with payment by Snam Rete acquisition contracts of € 148 million and € 63 million for (1) This consideration is subject to possible future adjustments for both acquisitions, which were not considered when determining the price given the objective difficulty in making forecasts based on the currently available information. Disclosures about the price adjustment mechanisms are given in note 21 “Guarantees, commitments and risks” to the condensed interim consolidated financial statements. 4 SNAM RETE GAS HALF YEAR REPORT AT 30 JUNE 2009 / ACQUISITION OF ITALGAS AND STOGIT Italgas and Stogit, respectively, is due to contractually pro- directors of Snam Rete Gas S.p.A. in its meeting of 23 vided-for price adjustment mechanisms which consider, March 2009 when the board resolved to execute the proxy, inter alia , the acquirees’ final net financial position, the given to it by the shareholders in their extraordinary meet- 2008 dividends distributed by Italgas and Stogit to Eni ing of 17 March 2009, to increase share capital in one or S.p.A. and the financial expense accrued from the date more instalments for a maximum of € 3,500 million, when the transaction became effective for financial pur- including the premium, by issuing ordinary shares against poses (1 January 2009) to the date of its execution (30 consideration with a nominal amount of € 1 and regular June 2009). -

An Analysis of the Level of Qualitative Efficiency for the Equity Research Reports in the Italian Financial Market

http://ijba.sciedupress.com International Journal of Business Administration Vol. 9, No. 2; 2018 An Analysis of the Level of Qualitative Efficiency for the Equity Research Reports in the Italian Financial Market Paola Fandella1 1 Università Cattolica del Sacro Cuore, Italy Correspondence: Paola Fandella, Università Cattolica del Sacro Cuore, Italy. Received: January 15, 2018 Accepted: February 6, 2018 Online Published: February 8, 2018 doi:10.5430/ijba.v9n2p21 URL: https://doi.org/10.5430/ijba.v9n2p21 Abstract Corporate reports issued by various financial intermediaries play a major role in investment decisions. For this reason, it is particularly interesting to understand the accuracy of the forecasts, by carrying out an empirical analysis of the "equity research" system in Italy, identifying structural features, degree of reliability and incidence in the market. The choice of the analysis of the efficiency level information on the Italian market proposes to assess the interest of equity research of a niche market (339 listed companies in 2017) but with characteristics of potential growth such as having been acquired by LSEGroup in 2007, the 6th stock-exchange group at international level for the number of listed companies and the 4th for capitalization. The analysis was carried out on the reports issued on companies belonging to the Ftse Mib stock index during a period of 5 years. It aims to analyse the composition of the equity research system in Italy as well as the analysts' ability to properly evaluate the stocks' fair price, so as to test their degree of reliability and detect possible anomalies in recommendations to the investors. -

Of the Ftse-Mib Companies

DEPARTMENT OF BUSINESS AND MANAGEMENT DEPARTMENT OF ECONOMICS AND FINANCE MASTER’S DEGREE IN CORPORATE FINANCE INTERLOCKING DIRECTORATES IN ITALY: SOCIAL NETWORK ANALYSIS OF THE FTSE-MIB COMPANIES SUPERVISOR CANDIDATE Prof. Saverio Bozzolan Guido Biagio Sallemi SUPERVISOR Prof. Riccardo Tiscini ACADEMIC YEAR 2018-19 1 2 CONTENTS 1. Introduction ................................................................................................................................... 5 2. The interlocking literature ............................................................................................................ 9 2.1. Theory behind the interlocking directorates .......................................................................... 9 2.2. Relevant cases and findings in SNA Literature................................................................... 11 3. Methodological Section .............................................................................................................. 15 3.1. Social network Analysis ...................................................................................................... 15 3.2. Basic Graphs Taxonomy ..................................................................................................... 16 3.3. Vertex Degree and related metrics ...................................................................................... 19 3.4. Centrality measures ............................................................................................................. 20 3.5. Network Cohesion -

Chapter 8: Italy

COMPETITION LAWS OUTSIDE THE UNITED STATES FIRST SUPPLEMENT CHAPTER 8: ITALY Mario Siragusa Matteo Berretta Saverio Valentino Principal Co-authors Matteo Bay Principal Reviewer Reprinted by permission of the American Bar Association. © 2005 ABA. ISBN: 1-59031-325-9 This volume should be officially cited as: ABA Section of Antitrust Law, Competition Laws Outside the United States, First Supplement (2005) Italy-3 CONTENTS I. INTRODUCTION ..............................................................................................5 A. Overview of Applicable Statutes and Landmark Cases ........................5 B. Overview of Enforcement Agencies and Their Jurisdiction..................6 C. Existence and Practical Availability of Private Rights of Action....................................................................................................8 II. OVERVIEW .....................................................................................................9 A. Application of Relevant Economic Doctrines.......................................9 1. Use of Specific Economic Analyses..............................................9 III. SUBSTANTIVE LAW ......................................................................................10 A. Horizontal Agreements and Practices .................................................10 1. Concept of Undertaking ..............................................................10 2. Agreements, Decisions, and Concerted Practices .......................11 (a) Concerted Practices ...........................................................11 -

Cdp Italy Report Climate Insights Among Italian Businesses and Local Governments

DISCLOSURE INSIGHT ACTION CDP ITALY REPORT CLIMATE INSIGHTS AMONG ITALIAN BUSINESSES AND LOCAL GOVERNMENTS DECEMBER 2019 With the kind support of DECEMBER 2019 CONTENTS 04 FOREWORD FROM THE ITALIAN MINISTRY FOR THE ENVIRONMENT, LAND AND SEA 05 WHY CDP? 05 THE COLLABORATION WITH THE ITALIAN GOVERNMENT 07 REPORT KEY FINDINGS 08 ANALYSIS OF CDP CITIES, STATES AND REGIONS DATA 2018 14 ANALYSIS OF CDP CORPORATE DATA 2018 18 CASE STUDY: SYNERGIES BETWEEN THE PUBLIC AND THE PRIVATE SECTOR 20 FINANCIAL MARKET TRENDS 23 APPENDIX: LIST OF RESPONDING COMPANIES, CITIES AND REGIONS Important Notice The contents of this report may be used by anyone providing acknowledgement is given to CDP Europe (CDP). This does not represent a license to repackage or resell any of the data reported to CDP or the contributing authors and presented in this report. If you intend to repackage or resell any of the contents of this report, you need to obtain express permission from CDP before doing so. CDP has prepared the data and analysis in this report based on responses to the CDP 2018 and CDP 2019 information request. No representation or warranty (express or implied) is given by CDP as to the accuracy or completeness of the information and opinions contained in this report. You should not act upon the information contained in this publication without obtaining specific professional advice. To the extent permitted by law, CDP does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this report or for any decision based on it. -

Credit Market Opportunities Date and Time of Production

Credit Strategy 3 September 2020: 19:14 CET Credit Market Opportunities Date and time of production Tactical View on Credit Markets Italy/Bi-Weekly Report After the negative performance recorded in 1H20, we believe that a moderate Index price performance spread tightening trend could occur in 2H20 for Italian IG Non-Financial corporate % Value -1W -1M bonds, as they are supported by the ECB’s heightened monetary stimulus amid IG ASW 89 -2.2 -11.9 HY OAS 398 -1.5 -8.1 resilient fundamentals, on average. Amid dovish monetary policies, investors’ hunt for Crossover 5Y 305 -5.5 -18.7 yield could also support the highest-rated HY names. However, careful credit selection Europe 5Y 50 -7.1 -17.0 will remain key in the HY segment, due to the more pronounced vulnerability of their % Value -1W -1M fundamentals to a deteriorating economic outlook. In the Italian bank bond sector, Euro Stoxx 50 3,338 -0.6 5.1 FTSE MIB 19,858 -1.4 4.0 we see as supportive factors the ECB’s comprehensive package of monetary stimulus * IG = Corporate IG. Source: Bloomberg and the large number of measures that have been adopted by regulators as well as Report priced at market close on day prior to the Italian fiscal packages and the forthcoming EU stimulus package of grants and issue (except where otherwise indicated). loans. However, the Italian macroeconomic scenario remains challenging, and we expect volatility to persist. ML IG Eur Corp. vs Itraxx Main (bps) Corporate (ASW) Investment Recommendations 220 170 In the corporate Investment Grade segment, we recommend the following switches: 120 1) buying IGIM 1 5/8 2027 bond and selling IGIM 1 2031 bond, expecting a widening of the ASW spread gap (currently 9bps); 2) buying EXOIM 2 1/4 04/30 bond and selling 70 EXOIM 1 3/4 10/34 bond, expecting an inversion of the current ASW gap; 3) buying 20 EXOIM 2 1/4 04/30 bond and selling EXOIM 1 3/4 01/28 bond, expecting a reduction of 01.10 07.13 01.17 07.20 the current ASW gap (60.7bps). -

Introduction of “Split Payment” Regulations for RCC Service Invoices

Market Notice 11 August 2017 MN_61/2017 Introduction of “Split Payment” regulations for RCC service invoices For the attention of: Intermediaries Priority: High Re: Invoicing of RCC charges Dear Client, Please note that following the publication of the Ministry of Economy and Finance Decree of 13 July 2017 in Official Gazette No. 171 of 24 July 2017, which amends the implementing regulations for the splitting of payments for VAT purposes (Article 17-ter, Presidential Decree No. 633/1972) in invoices payable as of 1 July 2017, the RCC fees invoicing application for issuer companies included in the list of listed companies in the FTSE MIB Index published by the Ministry of Economy and Finance (link) must be adapted to the new provisions. The Monte Titoli application is currently in the process of modification and therefore data indicated in the invoicing documentation issued by intermediaries to the issuers concerned (see the list below) in the period 1 July - 10 August is not consistent with the instructions in the Decree. Pending the adaption of the application, and in order to avoid issuing incorrect documents, the invoice request function has been temporarily suspended exclusively for sums due from Issuers to which the aforementioned Decree applies. It should be recalled that the RCC application allows the recovery of sums in suspension without time limits. Monte Titoli shall promptly inform clients by means of Market Notice when the application has been adapted. 1 Market Notice 11 August 2017 MN_61/2017 We apologise for this temporary inconvenience. Our operating offices are available for any clarifications or operating requirements. -

Transition Effects from the Initial Adoption of IFRS 9 by Italian and German Blue Chip Companies

Journal of Modern Accounting and Auditing, November 2020, Vol. 16, No.11, 467-483 doi: 10.17265/1548-6583/2020.11.001 D DAVID PUBLISHING Transition Effects from the Initial Adoption of IFRS 9 by Italian and German Blue Chip Companies Knut Henkel University of Applied Sciences, Emden/Leer, Emden, Germany Marvin Bürger NORD/LB Norddeutsche Landesbank - Girozentrale -, Hanover, Germany For the financial years from 2018, the new standard for accounting of financial instruments, IFRS 9, was applicable for the first time. Various questions arose in connection with the transition. For example, how high would the resulting transition effect be on equity? Another aspect related to the question of the extent to which the fair value measurement (through profit or loss) would increase. It is also of interest whether the previously presented IFRS 9 changes are classifiable as being material. Through the analysis of the financial statements of FTSE MIB and DAX 30 companies that were prepared for the first time in accordance with IFRS 9 in the year 2018, answers are given in this article to the aforementioned questions and a comparison is made regarding the extent to which national differences or commonalities existed. In the overall view of the absolute change in equity, for the FTSE MIB companies, a mean value of € - 3.03 million was calculated and for the DAX 30 companies, € - 34.29 million. The equity ratio (median), however, only declined marginally in percentage points with the FTSE MIB companies (-0.07), as well as with the DAX 30 companies (-0.02). With regard to the migration of financial assets, it has been shown that the accounting and measurement of more than 90% of financial assets of the FTSE MIB and DAX 30 companies have not changed. -

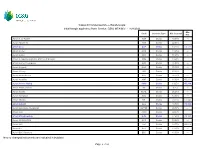

Cassa Di Compensazione E Garanzia Spa Initial Margin Applied to Share Section GEM, MTA/MIV - 16/8/2021 Min

Cassa di Compensazione e Garanzia spa Initial Margin applied to Share Section GEM, MTA/MIV - 16/8/2021 Min. Code Contract Type Mar. Interval Mar. Azioni A. S. ROMA ASR Stocks 49.00% --- Azioni Abitare IN ABT Stocks 22.00% --- Azioni Acea ACE Stocks 13.25% €0.122 Azioni Acotel ACO Stocks 41.25% --- Azioni Aedes AED Stocks 51.25% --- Azioni Aeroporto Guglielmo Marconi di Bologna ADB Stocks 18.25% --- Azioni Alerion Cleanpower ARN Stocks 25.00% --- Azioni Algowatt ALW Stocks 30.75% --- Azioni Alkemy ALK Stocks 25.00% --- Azioni Ambienthesis ATH Stocks 26.75% --- Azioni Amplifon AMP Stocks 13.00% €0.260 Azioni Anima Holding ANIM Stocks 19.25% €0.038 Azioni Antares Vision AV Stocks 9.25% --- Azioni Aquafil ECNL Stocks 26.25% --- Azioni Ascopiave ASC Stocks 13.00% --- Azioni Atlantia ATL Stocks 23.75% €0.146 Azioni Autogrill AGL Stocks 33.50% €0.082 Azioni Autostrade Meridionali AUTME Stocks 26.50% --- Azioni Avio AVIO Stocks 22.50% --- Azioni Azimut Holding AZM Stocks 17.50% €0.182 Azioni ACSM AGAM ACS Stocks 19.00% --- Azioni A2A A2A Stocks 14.75% €0.012 Azioni B.F. BFG Stocks 13.50% --- Azioni B&C Speakers BEC Stocks 13.00% --- New or changed instruments are indicated in boldface Page 1 of 16 Cassa di Compensazione e Garanzia spa Initial Margin applied to Share Section GEM, MTA/MIV - 16/8/2021 Min. Code Contract Type Mar. Interval Mar. Azioni Banca Carige CRG Stocks 97.50% --- Azioni Banca Carige Rnc CRGR Stocks 96.50% --- Azioni Banca Farmafactoring BFF Stocks 17.25% --- Azioni Banca Finnat BFE Stocks 16.75% --- Azioni Banca Generali BGN -

Annual Accounts and Reports As at 30 June 2020 Translation from the Italian Original Which Remains the Definitive Version CONTENTS

LIMITED COMPANY SHARE CAPITAL € 443,616,723.50 HEAD OFFICE: PIAZZETTA ENRICO CUCCIA 1, MILAN, ITALY REGISTERED AS A BANK. PARENT COMPANY OF THE MEDIOBANCA BANKING GROUP. REGISTERED AS A BANKING GROUP Annual Accounts and Reports as at 30 June 2020 www.mediobanca.com translation from the Italian original which remains the definitive version CONTENTS Consolidated accounts Review of operations Mediobanca Group 7 Declaration by head of company financial reporting 79 External auditors' report 83 Consolidated financial statements 95 Notes to the accounts 105 Part A - Accounting policies 108 Part B - Notes to the consolidated balance sheet 162 Part C - Notes to the consolidated profit and loss account 219 Part D - Comprehensive consolidated profit and loss account 238 Part E - Information on risks and related hedging policies 239 Part F - Information on consolidated capital 338 Part G - Combination involving Group companies or business units 346 Part H - Related party disclosure 347 Part I - Share-based payment schemes 349 Part L - Segment reporting 353 Part M - Disclosure on leasing 357 *** Annexes Consolidated financial statements 362 *** Other documents Glossary 369 www.mediobanca.com translation from the Italian original which remains the definitive version Contents 3 CONSOLIDATED ACCOUNTS REVIEW OF OPERATIONS MEDIOBANCA GROUP REVIEW OF GROUP OPERATIONS The twelve months under review reflect the unprecedented shock caused by the Covid-19 epidemic, which caused the leading global economies to stall rapidly and enter recession. Stock markets lost more than 30% in March 2020 compared to the start of the year, before gradually recovering by-end June. The most recent estimates for 2020 suggest global GDP will fall on average by 6.5%, Eurozone GDP by 9.2%, and Italian GDP by 11.6%, with the expectation that growth could resume from as early as 2021, but uncertainty over when end- 2019 levels will be recovered. -

The Italgas Shareholder

THE ITALGAS SHAREHOLDER HOW TO BECOME A SHAREHOLDER, TO STAY INFORMED, AND TO PLAY AN ACTIVE ROLE IN THE COMPANY How to become a shareholder, to stay informed, and to play an active role in the Company DEAR SHAREHOLDERS, This Guide will give you an overview of Italgas in the Company’s events through voting at the activities, strategies and performance. It also Shareholders’ Meeting. includes comprehensive data on Italgas shares The Guide selects a range of important issues, but and stock-market metrics. The final pages of the it is not all-inclusive: we recommend that you visit document offer practical information on how the corporate web site (www.italgas.it) and contact Italgas shareholders can actively exercise their the Investor Relations Department to gain a better role: how to get information, invest and monitor knowledge and understanding of Italgas, and to share performance; lastly, how to participate remain regularly updated about the Company. INDEX Business, strategies and performance 3 Italgas key figures 4 Italgas profile INDEX 5 Governance 6 Strategic levers 7 Strategic achievements Italgas and the Stock Exchange 8 Italgas on the Stock Exchange 9 Shareholding structure 10 Shareholders’ returns Being an Italgas’ shareholder 11 How to invest 12 Participating in the Shareholders’ Meeting 13 Keeping up to date and getting involved THE ITALGAS SHAREHOLDER THE ITALGAS 2021 14 Glossary 15 Useful sources 2 ITALGAS KEY FIGURES Italgas Group Municipalities under concession Consolidated companies Subsidiaries (data as of 31 December