Autel-Maxitpms-Ts508-Eu-Mx-Sensor-V5.4X-Coverage-List.Pdf (438K)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2017

(a joint stock company Incorporated in the People's Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 Annual Report 2017 * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the content set out in this annual report is true, accurate and complete and does not contain any false representations, misleading statements or material omissions, and jointly and severally take legal liability for its contents. II. All the directors of the Company attended the Board meeting. III. Deloitte Touche Tohmatsu Certified Public Accountants LLP has issued the standard audited report for the Company without qualified opinion. The financial information in the annual report was prepared in accordance with China Accounting Standards for Business Enterprises and the relevant laws and regulations. IV. Wei Jian Jun, person-in-charge of the Company, Li Feng Zhen, person-in-charge of the accounting affairs and Lu Cai Juan, person-in-charge of the accounting department (head of the accounting department), declare that they warrant the truthfulness, accuracy and completeness of the financial report in this annual report. V. Proposal of profit distribution or capitalization of capital reserve during the Reporting Period reviewed by the Board As audited by Deloitte Touche Tohmatsu Certified Public Accountants LLP, the net profit of the Group and net profit attributable to shareholders of the Company in 2017 amounted to RMB5,043,386.53 and RMB5,027,297,997.74 respectively. The Company proposed to declare a cash dividend of RMB1,551,635,730.00 (representing RMB0.17 per share) (tax inclusive) to the shareholders of the Company for the year ended 31 December 2017. -

A80-Toothlearn-Xtooleshop.PDF (249K)

Tooth learn Function List Software Version: 5.22 Automaker method Model Engine/Type Year Chery By System Delphi electronic control system 1.5L(477F) Chery By System Delphi Electronic Control 1.6L(481F) Chery By System Delphiel ectroni ccontrol system 1.6L(451F) Chery By System Delphi 473 system Chery By System Delphi CNG engine Chery By System Liuji 465 Electronic Control System Chery By Type Type1(Delphie OBD) Chery By Type Type2 Chery By model Fengyun2 Series Delphi Electric Control System 1.5L(477F) Chery By model Cowin/Cowin2 Delphi Electronic Control System Chery By model Cowin/Cowin2 Delphi CNG engine Chery By model Cowin1 Delphi 473 EFI Chery By model Cowin3 Delphi CNG engine Chery By model Cowin5 Delphi Electronic Control Chery By model A1 Delphi 473 system Chery By model A5 Delphi CNG engine Chery By model E5 Chery By model Sonoftheeast Delphi Electronic Control System Chery By model QQ3 Liuji 465 Electronic Control System Chery By model QQ6 Delphi 473 system Chery By model Tiggo/Tiggo3 Delphi Electric Control2.0L/2.4L(4G63/4G64) Chery By model Tiggo/Tiggo3 Delphi Electronic Control1.6L(481F) Kairui By model Excellent Q22B Type1 Kairui By model Excellent Q22B Type2 Kairui By model ViewSonic Q21 Type1 Kairui By model ViewSonic Q21 Type2 Kairui By model YouSheng Q21D Type1 Kairui By model YouSheng Q21D Type2 Kairui By model elegant S22 Type1 Kairui By model elegant S122 Type2 Kairui By model elegant 2 Type1 Kairui By model elegant 2 Type2 Kairui By model QQ3 series Type1 Kairui By model QQ3 series Type2 Kairui By model K50 AUTO -

GREAT WALL MOTOR COMPANY LIMITED (A Joint Stock Company Incorporated in the People’S Republic of China with Limited Liability) (Stock Code: 2333)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. 長 城 汽 車 股 份 有 限 公 司 * GREAT WALL MOTOR COMPANY LIMITED (a joint stock company incorporated in the People’s Republic of China with limited liability) (Stock Code: 2333) ANNOUNCEMENT OF AUDITED ANNUAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2019 The board of directors (the “Board”) of Great Wall Motor Company Limited (the “Company”) is pleased to announce the audited results of the Company and its subsidiaries for the year ended 31 December 2019. This announcement, containing the full text of the 2019 Annual Report of the Company, is prepared with reference to the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to preliminary announcements of Annual Results. The Company’s 2019 Annual Report will be available for viewing on the websites of The Stock Exchange of Hong Kong Limited at www.hkexnews.hk and of the Company at www.gwm.com.cn. Printed version of the Company’s 2019 Annual Report will also be delivered to the Company’s shareholders. By order of the Board Great Wall Motor Company Limited Xu Hui Company Secretary IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the contents of this annual report are true, accurate and complete and do not contain any false representations, misleading statements or material omissions, and jointly and severally take legal liability for its contents. -

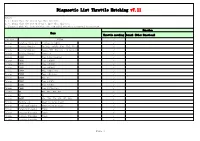

Throttle Matching V7.11

Disgnostic List Throttle Matching v7.11 Remark: 1.√: means that the system has this function 2. -: means that the system doesn't have this function 3. Compared with the last version, the new added function is marked in red font Function Menu Throttle matching Remark (Other Functions) Demo mode NISSAN √ Chinese Dongfeng Yueda KIA Sportage R (2013) √ Chinese Beijing Hyundai Yuedong, SONATA, I30, IX35, Viena √ Chinese Beijing Hyundai Sonata YFC, Elantra, new Santa Fe √ Chinese Beijing Hyundai Sonata 9 √ Chinese CHERY Type 1(Continental) √ Chinese CHERY Type 2(DIAS) √ Chinese CHERY Type 3(DIAS) √ Chinese CHERY Type 4(DIAS) √ Chinese CHERY Type 5(Marelli) √ Chinese CHERY Type 6(Delphi) √ Chinese CHERY Type 7 √ Chinese CHERY Type 8(UMC) √ Chinese CHERY Type 9(UMC) √ Chinese CHERY Type 10(Troitec) √ Chinese MG MG3、MG5、MG6、MG7 √ Chinese MG GS √ Chinese ROEWE 350, 550, 750, 950, W5, BP12 √ Chinese Haixing car Adaptive value reset √ Chinese Dongfeng Fengshen Adaptive value reset √ Chinese Dongfeng Fengshen Type2 √ Chinese Dongfeng Fengshen Type3 √ Chinese Dongfeng Fengshen Type4 √ Chinese Dongfeng Fengshen √ Page 1 Disgnostic List Throttle Matching v7.11 Remark: 1.√: means that the system has this function 2. -: means that the system doesn't have this function 3. Compared with the last version, the new added function is marked in red font Function Menu Throttle matching Remark (Other Functions) Chinese SOUEAST LingYue V3, Xiwang, LingYue V5/V6 √ LangLang, Langyue, A01, Chinese ZOTYE √ Z500(4A91T) Chinese TJFAW √ Chinese Riich, Rely √ Chinese ZXAUTO -

2017 Interim Report

(a joint stock company incorporated in the People’s Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 Interim Report 2017 2017 Interim Report * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the information in this interim report is true, accurate and complete and does not contain any false representations, misleading statements or material omissions, and jointly and severally take legal liability for its contents. II. All the directors of the Company attended the Board meeting. III. This interim report has not been audited. The financial information in this interim report was prepared in accordance with China Accounting Standards for Business Enterprises and the relevant laws and regulations. IV. Wei Jian Jun, person-in-charge of the Company, Li Feng Zhen, person-in-charge of the accounting affairs and Lu Cai Juan, person-in-charge of the accounting department (head of the accounting department), declare that they warrant the truthfulness, accuracy and completeness of the financial report in this interim report. V. Proposal of profit distribution or capitalization of capital reserve during the Reporting Period approved by the Board None VI. Risks relating to forward-looking statements Applicable Not applicable Forward-looking statements, such as plans for the future described in this interim report do not constitute an actual commitment of the Company to investors. Investors should be aware of the relevant investment risks. VII. Was there any non-operational appropriation of the Company’s funds by its controlling shareholders and related parties? No VIII. -

Annual Report

(a joint stock company incorporated in the People's Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 2 019 ANNUAL REPORT * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the contents of this annual report are true, accurate and complete and do not contain any false representations, misleading statements or material omissions, and jointly and severally take legal liability for its contents. II. All the directors of the Company attended the Board meeting. III. Deloitte Touche Tohmatsu Certified Public Accountants LLP has issued the standard audited report for the Company without qualified opinion. The financial information in the annual report was prepared in accordance with China Accounting Standards for Business Enterprises and the relevant laws and regulations. IV. Wei Jian Jun, person-in-charge of the Company, Liu Yu Xin, person-in-charge of the accounting affairs and Lu Cai Juan, person-in-charge of the accounting department (head of the accounting department), declare that they warrant the truthfulness, accuracy and completeness of the financial report in this annual report. V. Proposal of profit distribution or capitalization of capital reserve during the Reporting Period reviewed by the Board As audited by Deloitte Touche Tohmatsu Certified Public Accountants LLP, the net profit of the Group and net profit attributable to shareholders of the Company in 2019 amounted to RMB4,530,732,870.30 and RMB4,496,874,893.92 respectively. The Company proposed to declare a cash dividend of RMB2,281,817,250.00, (representing RMB0.25 per share) (tax inclusive) to the shareholders of the Company for the year ended 31 December 2019. -

Annual Report * for Identification Purpose Only IMPORTANT NOTICE I

(a joint stock company incorporated in the People’s Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 2015 Annual Report * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the information in this annual report is true, accurate and complete and does not contain any false representations, misleading statements or material omissions, and jointly and severally take responsibility for its contents. II. Director(s) absent from the Board meeting Position of the Name of the director(s) Reasons for being director(s) absent absent from absent from from the Board meeting the Board meeting the Board meeting Representative Independent director Liang Shang Shang Work commitment Lu Chuang (Independent non-executive director) III. Deloitte Touche Tohmatsu Certified Public Accountants LLP (auditor of the Company) has issued the standard audited report for the Company without qualified opinion. The financial information in the annual report was prepared in accordance with China Accounting Standards for Business Enterprises and the relevant laws and regulations. IV. Wei Jian Jun, person-in-charge of the Company, Li Feng Zhen, person-in-charge of the accounting affairs and Lu Cai Juan, person-in-charge of the accounting department (head of the accounting department), declare that they warrant the truthfulness, accuracy and completeness of the financial report in this annual report. V. Proposal -

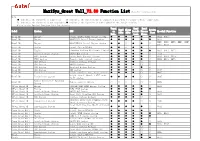

Model System ECU Versi on Info. Read Dtcs Clear Dtcs Read

MaxiSys_Great Wall_V3.80 Function List(Note:For reference only) Note: ● indicates the function is supported. ※ indicates the function may be supported according to actual vehicle conditions. ○ indicates the function is not available.● indicates the function is newly added to the latest version. Refer to the Special Function List for details. Versi Read Read Read Clear Active Model System ECU on DataSt Freeze Special Function DTCs DTCs Test Info. ream Frame Haval H3 Engine Delphi MT20U2_EOBD engine system ● ● ● ● ● ● 0012 0015 Haval H3 Engine BOSCH V50 Diesel Engine System ● ● ● ● ● ● 0011 0001 0002 0003 0004 0005 Haval H3 Engine BOSCH-EDC16 Diesel Engine System ● ● ○ ● ● ○ 0006 0027 Haval H3 Engine Delphi System(MT20U) ● ● ○ ● ● ○ Haval H3 Engine Liaoning Xinfeng Electronic Control ● ● ● ● ● ● 0021 0011 0015 Haval H3 Antilock Brake System BOSCHSystem ABS System ● ● ● ● ● ○ 0013 Haval H3 VECU System Delphi Body Control System ● ● ● ● ● ○ 0030 0018 0019 Haval H3 VECU System Tongzhi body control system ● ● ● ● ● ○ 0030 0029 007A Haval H3 SRS System Jinzhou Jinheng Airbags ● ● ● ● ○ ○ Haval H3 SRS System BOSCH Airbags ● ● ● ● ○ ○ Haval H3 SRS System Mainland Airbag System ● ● ● ○ ● ○ Haval H3 SRS System TRW airbag ● ● ● ● ○ ○ 0030 Haval H3 Immobilizer System Delphi gasoline anti-theft system ● ● ● ● ○ ○ 0025 Delphi diesel (Bosch 2.8TC) anti- Haval H3 Immobilizer System ● ● ● ● ○ ○ 0025 theft system Remote Controller Matching Haval H3 Remote control system ○ ○ ○ ○ ○ ○ 0078 System GWPeri,Haval M1 Engine GW413EF UAES EOBD Engine System ● ● ● -

Launch CRP909 IMMO Vehicle List.Pdf

IMMO V10.60 Diagnostics List(Note:For reference only) Make Model Year CL 2007-2014 CSX 2007-2014 EL 2007-2014 MDX 2007-2014 ACURA RDX 2007-2014 RSX 2007-2014 TL 2008-2014 TSX 2007-2014 AUDI AUDI Up to 2008 Remote control 163-M CLASS 1997-2005 system 169-A CLASS 2005-2007 176-A CLASS As of 2007 245-B CLASS As of 2005 246-B CLASS As of 2007 203-C CLASS 2000-2007 203-CLC CLASS As of 2008 204-C CLASS As of 2007 216-CL CLASS As of 2006 117-CLA CLASS As of 2012 209-CLK CLASS As of 2004 218-CLS CLASS As of 2007 219-CLS CLASS 2004-2006 207-E CLASS As of 2007 211-E CLASS 2002-2009 212-E CLASS As of 2009 Disable key MERCEDES-BENZ 463-G CLASS Up to 2013 164-GL CLASS As of 2004 166-GL CLASS As of 2013 156-GLA CLASS As of 2013 204-GLK CLASS As of 2007 292-GLE/M CLASS As of 2013 163-M CLASS 1997-2005 164-M CLASS 2005-2011 166-M CLASS As of 2010 251-R CLASS As of 2004 220-S CLASS 1998-2005 221-S CLASS As of 2006 171-SLK CLASS 2004-2011 172-SLK CLASS As of 2011 197-SLS CLASS As of 2007 MERCEDES-BENZ IMMO V10.60 Diagnostics List(Note:For reference only) Make Model Year 204-CCLASS As of 2007 Tailgate control 212-ECLASS As of 2009 system X204-GLKCLASS As of 2007 1 SERIES 2003-2015 2 SERIES 2013-2015 3 SERIES 2004-2015 4 SERIES 2013-2015 5 SERIES 2004-2015 BMW 6 SERIES 2004-2015 7 SERIES 2002-2015 I SERIES 2013-2015 X SERIES 2007-2015 Z SERIES 2003-2015 BORGWARD BORGWARD Up to 2016 MINI MINI 2004-2015 200 As of 2011 300 2005-2014 300C 2005-2014 300M 1999-2007 ASPEN 2007-2009 CONCORDE 300 1998-2004 GRAND VOYAGER As of 2004 CHRYSLER LHS 1999-2001 NEON 2000-2002 -

Annual Report 2016 2016 Annual Report

(a joint stock company incorporated in the People’s Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 Annual Report 2016 2016 Annual Report * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the information in this annual report is true, accurate and complete and does not contain any false representations, misleading statements or material omissions, and jointly and severally take legal liability for its contents. II. Director(s) absent from the Board meeting Position of the Name of the Reasons for director(s) absent director(s) absent being absent from the Board meeting from the Board meeting from the Board meeting Representative Independent director Lu Chuang Work commitment Ma Li Hui III. Deloitte Touche Tohmatsu Certified Public Accountants LLP (auditor of the Company) has issued the standard audited report for the Company without qualified opinion. The financial information in the annual report was prepared in accordance with China Accounting Standards for Business Enterprises and the relevant laws and regulations. IV. Wei Jian Jun, person-in-charge of the Company, Li Feng Zhen, person-in-charge of the accounting affairs and Lu Cai Juan, person-in-charge of the accounting department (head of the accounting department), declare that they warrant the truthfulness, accuracy and completeness of the financial report in this annual report. V. Proposal of profit distribution or capitalization of capital reserve during the Reporting Period approved by the Board As audited by Deloitte Touche Tohmatsu Certified Public Accountants LLP, the net profit of the Company and net profit attributable to shareholders of the Company in 2016 amounted to RMB10,553,954,644.48 and RMB10,551,158,884.21 respectively. -

IMMO Diagnostics List

IMMO Diagnostics List (Note:For reference only) make model year system function subfunction ACURA CL 2007-2014 -- IMMO ACURA CSX 2007-2014 -- IMMO ACURA EL 2007-2014 -- IMMO ACURA MDX 2007-2014 -- IMMO ACURA RDX 2007-2014 -- IMMO ACURA RSX 2007-2014 -- IMMO ACURA TL 2008-2014 -- IMMO ACURA TSX 2007-2014 -- IMMO AUDI AUDI Up to 2008 -- IMMO MERCEDES- BENZ(Remote control 163-M CLASS 1997-2005 -- IMMO system) MERCEDES- 169-A CLASS 2005-2007 -- IMMO BENZ(Disable key) MERCEDES- 176-A CLASS As of 2007 -- IMMO BENZ(Disable key) MERCEDES- 245-B CLASS As of 2005 -- IMMO BENZ(Disable key) MERCEDES- 246-B CLASS As of 2007 -- IMMO BENZ(Disable key) MERCEDES- 203-C CLASS 2000-2007 -- IMMO BENZ(Disable key) MERCEDES- 203-CLC CLASS As of 2008 -- IMMO BENZ(Disable key) MERCEDES- 204-C CLASS As of 2007 -- IMMO BENZ(Disable key) MERCEDES- 216-CL CLASS As of 2006 -- IMMO BENZ(Disable key) MERCEDES- 117-CLA CLASS As of 2012 -- IMMO BENZ(Disable key) MERCEDES- 209-CLK CLASS As of 2004 -- IMMO BENZ(Disable key) MERCEDES- 218-CLS CLASS As of 2007 -- IMMO BENZ(Disable key) MERCEDES- 219-CLS CLASS 2004-2006 -- IMMO BENZ(Disable key) MERCEDES- 207-E CLASS As of 2007 -- IMMO BENZ(Disable key) MERCEDES- 211-E CLASS 2002-2009 -- IMMO BENZ(Disable key) MERCEDES- 212-E CLASS As of 2009 -- IMMO BENZ(Disable key) make model year system function subfunction MERCEDES- 463-G CLASS Up to 2013 -- IMMO BENZ(Disable key) MERCEDES- 164-GL CLASS As of 2004 -- IMMO BENZ(Disable key) MERCEDES- 166-GL CLASS As of 2013 -- IMMO BENZ(Disable key) MERCEDES- 156-GLA CLASS As of 2013 -

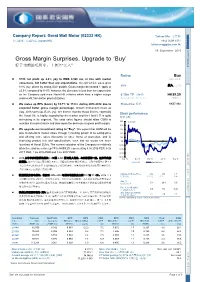

Gross Margin Surprises, Upgrade to 'Buy'

Company Report: Great Wall Motor (02333 HK) Toliver Ma 马守彰 公司报告:长城汽车 (02333 HK) +852 2509 5317 [email protected] 国泰君安研究 19 September 2016 Gross Margin Surprises, Upgrade to ‘Buy’ 好于预期的毛利率,上调至“买入” GTJA Research GTJA Rating: Buy 1H16 net profit up 4.4% yoy to RMB 4,926 mn, in line with market Upgraded consensus, but better than our expectations. Overall vehicle sales grew 评级: 买入 (上调) 8.8% yoy, driven by strong SUV growth. Gross margin decreased 1.1ppts to 23.9% compared to 1H15; however, the decrease is less than our expectation as the Company sold more Haval H6 vehicles which have a higher margin 6-18m TP 目标价: HK$9.29 and benefit from better plant utilization. Revised from 原目标价: HK$7.14 We revise up EPS (basic) by 15.7% to 17.0% during 2016-2018 due to Share price 股价: HK$7.960 expected better gross margin percentage. Growth momentum intact as Aug. 2016 sales up 25.4% yoy. We believe that the Haval Series, especially Stock performance the Haval H6, is highly regarded by the market and the Haval H7 is quite 股价表现 welcoming in its segment. The solid sales figures should allow GWM to 50.0 % of return maintain its market share and slow down the decrease in gross profit margin. 40.0 We upgrade our investment rating to “Buy”. We expect that GWM will be 30.0 able to defend its market share through 1) limiting growth of its selling price 20.0 and offering more sales discounts or other forms of promotion, and 2) 10.0 improving product mix and specifications, such that we would see more 0.0 launches of Haval SUVs.