The Sale of London Transport's Bus Operating Companies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

English Counties

ENGLISH COUNTIES See also the Links section for additional web sites for many areas UPDATED 23/09/21 Please email any comments regarding this page to: [email protected] TRAVELINE SITES FOR ENGLAND GB National Traveline: www.traveline.info More-detailed local options: Traveline for Greater London: www.tfl.gov.uk Traveline for the North East: https://websites.durham.gov.uk/traveline/traveline- plan-your-journey.html Traveline for the South West: www.travelinesw.com Traveline for the West & East Midlands: www.travelinemidlands.co.uk Black enquiry line numbers indicate a full timetable service; red numbers imply the facility is only for general information, including requesting timetables. Please note that all details shown regarding timetables, maps or other publicity, refer only to PRINTED material and not to any other publications that a county or council might be showing on its web site. ENGLAND BEDFORDSHIRE BEDFORD Borough Council No publications Public Transport Team, Transport Operations Borough Hall, Cauldwell Street, Bedford MK42 9AP Tel: 01234 228337 Fax: 01234 228720 Email: [email protected] www.bedford.gov.uk/transport_and_streets/public_transport.aspx COUNTY ENQUIRY LINE: 01234 228337 (0800-1730 M-Th; 0800-1700 FO) PRINCIPAL OPERATORS & ENQUIRY LINES: Grant Palmer (01525 719719); Stagecoach East (01234 220030); Uno (01707 255764) CENTRAL BEDFORDSHIRE Council No publications Public Transport, Priory House, Monks Walk Chicksands, Shefford SG17 5TQ Tel: 0300 3008078 Fax: 01234 228720 Email: [email protected] -

Operators Route Contracts

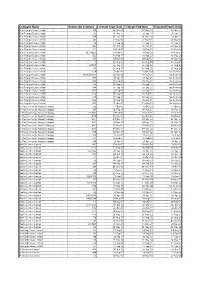

Company Name Routes On Contract Contract Start Date Contract End Date Extended Expiry Date Blue Triangle Buses Limited 300 06-Mar-10 07-Dec-18 03-Mar-17 Blue Triangle Buses Limited 193 01-Oct-11 28-Sep-18 28-Sep-18 Blue Triangle Buses Limited 364 01-Nov-14 01-Nov-19 29-Oct-21 Blue Triangle Buses Limited 147 07-May-16 07-May-21 05-May-23 Blue Triangle Buses Limited 376 17-Sep-16 17-Sep-21 15-Sep-23 Blue Triangle Buses Limited 346 01-Oct-16 01-Oct-21 29-Sep-23 Blue Triangle Buses Limited EL3 18-Feb-17 18-Feb-22 16-Feb-24 Blue Triangle Buses Limited EL1/NEL1 18-Feb-17 18-Feb-22 16-Feb-24 Blue Triangle Buses Limited EL2 18-Feb-17 18-Feb-22 16-Feb-24 Blue Triangle Buses Limited 101 04-Mar-17 04-Mar-22 01-Mar-24 Blue Triangle Buses Limited 5 26-Aug-17 26-Aug-22 23-Aug-24 Blue Triangle Buses Limited 15/N15 26-Aug-17 26-Aug-22 23-Aug-24 Blue Triangle Buses Limited 115 26-Aug-17 26-Aug-22 23-Aug-24 Blue Triangle Buses Limited 674 17-Oct-15 16-Oct-20 See footnote Blue Triangle Buses Limited 649/650/651 02-Jan-16 01-Jan-21 See footnote Blue Triangle Buses Limited 687 30-Apr-16 30-Apr-21 See footnote Blue Triangle Buses Limited 608 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 646 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 648 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 652 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 656 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 679 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 686 03-Sep-16 03-Sep-21 See footnote -

London and the South East of England: 15 July 2016

OFFICE OF THE TRAFFIC COMMISSIONER (LONDON AND THE SOUTH EAST OF ENGLAND) NOTICES AND PROCEEDINGS PUBLICATION NUMBER: 2359 PUBLICATION DATE: 15 July 2016 OBJECTION DEADLINE DATE: 05 August 2016 Correspondence should be addressed to: Office of the Traffic Commissioner (London and the South East of England) Hillcrest House 386 Harehills Lane Leeds LS9 6NF Telephone: 0300 123 9000 Fax: 0113 249 8142 Website: www.gov.uk/traffic-commissioners The public counter at the above office is open from 9.30am to 4pm Monday to Friday The next edition of Notices and Proceedings will be published on: 29/07/2016 Publication Price £3.50 (post free) This publication can be viewed by visiting our website at the above address. It is also available, free of charge, via e-mail. To use this service please send an e-mail with your details to: [email protected] Remember to keep your bus registrations up to date - check yours on https://www.gov.uk/manage-commercial-vehicle-operator-licence-online NOTICES AND PROCEEDINGS Important Information All correspondence relating to public inquiries should be sent to: Office of the Traffic Commissioner (London and the South East of England) Ivy House 3 Ivy Terrace Eastbourne BN21 4QT The public counter at the Eastbourne office is open for the receipt of documents between 9.30am and 4pm Monday Friday. There is no facility to make payments of any sort at the counter. General Notes Layout and presentation – Entries in each section (other than in section 5) are listed in alphabetical order. Each entry is prefaced by a reference number, which should be quoted in all correspondence or enquiries. -

The Go-Ahead Group Plc Annual Report and Accounts 2019 1 Stable Cash Generative

Annual Report and Accounts for the year ended 29 June 2019 Taking care of every journey Taking care of every journey Regional bus Regional bus market share (%) We run fully owned commercial bus businesses through our eight bus operations in the UK. Our 8,550 people and 3,055 buses provide Stagecoach: 26% excellent services for our customers in towns and cities on the south FirstGroup: 21% coast of England, in north east England, East Yorkshire and East Anglia Arriva: 14% as well as in vibrant cities like Brighton, Oxford and Manchester. Go-Ahead’s bus customers are the most satisfied in the UK; recently Go-Ahead: 11% achieving our highest customer satisfaction score of 92%. One of our National Express: 7% key strengths in this market is our devolved operating model through Others: 21% which our experienced management teams deliver customer focused strategies in their local areas. We are proud of the role we play in improving the health and wellbeing of our communities through reducing carbon 2621+14+11+7+21L emissions with cleaner buses and taking cars off the road. London & International bus London bus market share (%) In London, we operate tendered bus contracts for Transport for London (TfL), running around 157 routes out of 16 depots. TfL specify the routes Go-Ahead: 23% and service frequency with the Mayor of London setting fares. Contracts Metroline: 18% are tendered for five years with a possible two year extension, based on Arriva: 18% performance against punctuality targets. In addition to earning revenue Stagecoach: 13% for the mileage we operate, we have the opportunity to earn Quality Incentive Contract bonuses if we meet these targets. -

Operations Review

OPERATIONS REVIEW SINGAPORE PUBLIC TRANSPORT SERVICES (BUS & RAIL) • TAXI AUTOMOTIVE ENGINEERING SERVICES • INSPECTION & TESTING SERVICES DRIVING CENTRE • CAR RENTAL & LEASING • INSURANCE BROKING SERVICES OUTDOOR ADVERTISING Public Transport Services The inaugural On-Demand Public Bus ComfortDelGro Corporation Limited is Services trial, where SBS Transit operated a leading provider of land transport and five bus routes – three in the Joo Koon area related services in Singapore. and two in the Marina-Downtown area – for 2.26 the LTA ended in June 2019. Conducted REVENUE Scheduled Bus during off-peak hours on weekdays, (S$BILLION) SBS Transit Ltd entered into its fourth year commuters could book a ride with an app of operating under the Bus Contracting and request to be picked up and dropped Model (BCM) in 2019, where the provision off at any bus stop within the defined areas. of bus services and the corresponding It was concluded by the LTA that such bus standards are all determined by the Land services were not cost-effective due to Transport Authority (LTA). Under this model, the high technology costs required in the Government retains the fare revenue scaling up. and owns all infrastructure and operating assets such as depots and buses. A major highlight in 2019 was SBS Transit’s active involvement in the three-month long 17,358 Bus routes in Singapore are bundled into public trial of driverless buses on Sentosa TOTAL OPERATING 14 bus packages. Of these, SBS Transit Island with ST Engineering. Operated as an FLEET SIZE operated nine. During the year, it continued on-demand service, visitors on the island to be the biggest public bus operator with could book a shuttle ride on any of the a market share of 61.1%. -

Key to Maps for Details in Central London See Overleaf

S 1 N B C 712.724 M S 2 O 9 Maldon Manor Station, The Manor Drive, Worcester Park, Dorchester Road, North Cheam, London Road, Windsor Avenue, H A C 242.C1.C2 M H 310.311 W1† 614 S 298 308.312 610 66.103.175 D 9 757 to D NE R R 2 E Cuffley 381 3 R E R A A 8 N LEY 4 1 A 5 .39 FF H U . 364 5.248 . A L N 12 A CU IL D 1 T A E P C1.C3.C4 6 621 N 615 A 3 A 380.880 L 191 W8 W10 247.294.296 O 8 - * Luton Airport E Cranborne Road . L T H 8 Stayton Road, Sutton, Cedar Road, Langley Park Road, Lind Road, Westmead Road, Carshalton, Carshalton Beeches, D R 2 9 O 1 R Breach Barns A R D Colney D * L T N 2 84 N C1 K B81 Y . O 2 648.N15 4 N S3 R 6 TI 242 I 8 E . E 0 84.302 A 365.375.575 S . A 797 D *T C T 2 S S C1 W9 O O L M B 298 B Industrial 3 RD C 382 9 . E N 7 6 G Y R . 8 CH 880 G * S S 1 T I U Street E . R R 242 211.212† 6 4 8 602 A U O R C Belmont, Royal Marsden Hospital, Sutton Hospital (Mon-Sat except evenings). Quality Line M O O O 4 398 H R 169 R T H S Shenleybury B 0 E 242 F . -

Capital Space Ltd Land South of Coldharbour Road, Gravesend

Capital Space Ltd Land South of Coldharbour Road, Gravesend Transport Assessment July 2016 Gravesham Borough Council Contents 1 INTRODUCTION .................................................................................................. 1 2 SITE AND LOCAL AREA ........................................................................................ 2 Site Location ....................................................................................................... 2 Local Road Network ............................................................................................ 2 Public Transport .................................................................................................. 3 3 POLICY ................................................................................................................ 4 National Planning Policy Framework .................................................................. 4 Supplementary Planning Guidance SPG 4 Kent Vehicle Parking Standards (July 2006) ................................................................................................................... 4 Gravesham Local Plan Core Strategy (September 2014) ................................... 5 4 BASELINE CONDITIONS ..................................................................................... 6 Existing Traffic Conditions .................................................................................. 6 5 PROPOSED DEVELOPMENT ................................................................................. 7 Overview -

Anticipated Acquisition by London and South Eastern Railway, a Wholly Owned Subsidiary of Govia Limited, of the Integrated Kent Rail Franchise

Anticipated acquisition by London and South Eastern Railway, a wholly owned subsidiary of Govia Limited, of the Integrated Kent Rail Franchise The OFT's decision on reference under section 33(1) given on 28 March 2006. Full text of decision published 4 April 2006. PARTIES 1. Govia Limited (Govia) is a rail franchise holding company. It was formed as a joint venture between The Go-Ahead Group Plc (Go-Ahead) and Keolis (UK) Limited (a subsidiary of Keolis SA), which have shareholdings in Govia of 65 per cent and 35 per cent respectively. Govia will acquire the Integrated Kent Rail Franchise through its wholly owned subsidiary, London and South Eastern Railway (LSER). 2. The Integrated Kent Rail Franchise (IKF) will include passenger rail services on the network currently operated by South Eastern Trains (SET), a subsidiary of the Strategic Rail Authority (SRA). IKF is a commuter network serving several areas around the South East of England, parts of Greater London and several London termini. IKF will also include new domestic high-speed services from London St Pancras, making use of the Channel Tunnel Rail Link. SET's turnover for the year ended 31 March 2005 was £443.3 million. TRANSACTION 3. Govia (through LSER) was named the preferred bidder for IKF on 30 November 2005. IKF is due to commence on 1 April 2006 and will run for six years, although the contract allows for an extension of two years if performance targets are met. Alternatively, in the event of a delay to the start of the new high speed services using the Channel Tunnel Rail Link, the franchise may be extended by two years. -

Tfl Corporate Archive Top 20 Records

LT000605/005 - Description of the New Administrative Offices of the Underground Group of Companies By the late 1920s, the Underground Electric Railways Companies of London Ltd was anxious to house all of its ‘head office’ staff in one new purpose-built office block on the site of the old Metropolitan District Railway offices above St James’s Park station. The plans developed by Adams, Holden and Pearson, the architects commissioned by the Group, were radical: • 55 Broadway would be the tallest office building in London; • there would be a cruciform design - in place of the customary hollow rectangle format – which would offer staff more natural daylight in wings projecting from a central core housing lifts, staircases and essential services; and • Contemporary artists would be invited to sculpt decorative features directly onto the stone facade. As detailed in this reprint of a 1929 brochure about the building, 55 Broadway was constructed between 1927 and 1929. 700 reinforced concrete piles sunk to an average depth of 40 feet below basement level support the building. Nineteen load-bearing steel girders span the railway, and special insulation was used to reduce vibration from the trains. Above ground, the building was constructed around a steel girder skeleton and faced with 78,000 cubic feet of high quality Portland stone. The building has a bold appearance, enhanced by progressive stepping back above the sixth, eighth and ninth floors – giving an uneven pyramid effect. The clock tower, 174 feet high, has a similar stepped back effect. Granite for the ground floor came from Norway whilst the Travertine marble used in the interior came from Italy. -

Cambridge University Library Map Department Collection of Plans of Towns in England, Wales, Scotland, Isle of Man and Channel Islands Classmark = Maps.TPE

Cambridge University Library Map Department collection of plans of towns in England, Wales, Scotland, Isle of Man and Channel Islands Classmark = Maps.TPE. followed by town name and date, the ID is also useful * Indicates that the item is filed in the Outsize sequence Abbots Bromley Staffordshire ID Date Pub Code Notes/Part 1076 2001 Abbots Bromley Parish Council Sm,G Abbots Langley Hertfordshire ID Date Pub Code Notes/Part 1693 1971 ? T Aberdeen ID Date Pub Code Notes/Part 4811 1960 ca. Bartholomew - Town plan T, E 1260 1988 Aberdeen Tourist Board T 1222 1994 ca. Footprints - The Pint Sized Guide T [Aberdeen pub guide.] 461 1996 Bartholomew - Streetfinder Map 658 1997 Bartholomew - Streetfinder Atlas 664 1997 Bartholomew - Streetfinder Colour Ma 654 1998 Collins - Streetfinder Atlas 629 1998 ca. Collins - Streetfinder Map Westhill, Elrick 905 1999 Hallewell Sm,GB,Walk Aberdeen on foot 628 1999 ca. Nicolson Westhill, Elrick 1307 2001 ca. Nicolson - Street Guide T 1316 2003 Collins - Streetfinder T 02 February 2021 Page 1 of 296 3293 2004 Cityscape Maps T,S,Transport,P Transport,Shopping, Guide map and 3048 2005 Nicolson - Street Atlas 3820 2010 ca. Nicolson T & Bieldside, Bridge of Don, Bucksbur 4974 2016 Nicolson Digital - Street map, 1:14,000 T Aberdour ID Date Pub Code Notes/Part 2944 2005 ca. Fife Tourist Board T, G Aberfan ID Date Pub Code Notes/Part 393 1997 ca. Manderley Sm Treharris, Troedyrhiw, Merthyr Vale Aberfeldy ID Date Pub Code Notes/Part 1659 1956 Scottish Field Studies Association T Abergavenny Monmouthshire ID Date Pub Code Notes/Part 395 1996 ca. -

Historic Fleetlists.Xlsx

Fife Scottish Omnibuses Limited (trading as Stagecoach in Fife) Fleet 2001… 40th Anniversary Fleet strength 294 (25 less than 1996 and back to 1991 level) After being a constant since the fleet was formed in 1961 the last Leyland single deckers are withdrawn 30 low floor 'Loliner' branded buses are now in service at Cowdenbeath and Dunfermline A return to operating Scottish Citylink services has brought a number of toilet fitted coaches back into the fleet Over 50 former London double deckers have arrived to replace older vehicles from the 1970s Stagecoach Express coach fleet has grown to over 40 vehicles, including articulated coaches Livery notes; A new group livery for Stagecoach UK operations is introduced. Retaining white, orange, red and blue in a new design From 2000 Fife, Stagecoach Perth and Bluebird Buses in Aberdeen are being managed by common management albeit remaining as separate companies * LF next to a fleet number indicates it is low floor/wheelchair accessible ** Seating code shows a bus, dual purpose or coach (starts with a B, DP or C) followed by number of seats and then F (for front entranced) a 't' at the end means toilet fitted *** Double decker seating is shown 'H' followed by the upper deck seating/lower deck seating and then the door code (F for front entranced). Open top vehicles start 'O' MINIBUSES (Total 20) 2001 Fleet Depot Registration Chassis Vehicle Seats** Year Notes Number* Alloc Number Type Type New 16 K F234NLS Mercedes Benz 609D Mercedes Benz DP18F 1988 ex Alisons in 2000 17 K M317RSO Mercedes Benz -

We Are Committed to Improving Our Practices to Combat Slavery And

We are committed to improving our practices Our supply chains include: to combat slavery and human trafficking. Our UK business has in excess of 1,000 ORGANISATION'S STRUCTURE suppliers who provide a range of products and services including capital equipment, We are a bus operating company. We are a professional services, facilities, maintenance part of the ComfortDelGro Group ("Group"), repair & operating and support services and our ultimate parent company is the totalling nearly £200 million per year in spend. ComfortDelGro Corporation which has its Whilst all the Tier 1 suppliers are based in the head office in Singapore. The Group has over UK there are a handful whose operations and 24,000 employees worldwide and operates in Tier 2 supply chains are also performed outside seven countries. The Group has a global annual the UK. turnover of S$3.81billion. OUR POLICIES ON SLAVERY AND OUR BUSINESS HUMAN TRAFFICKING This statement covers all of the activities of We are committed to ensuring that there is no Braddell Limited. Metroline Limited is the most modern slavery or human trafficking in our substantial part of our business operating and supply chains or in any part of our business. is responsible for almost 20% of the London Our Procurement Policy and Supplier Code of bus market through our subsidiaries, Metroline Conduct reflects our commitment to acting Travel Limited and Metroline West Limited. ethically and with integrity in all our business Our parent company itself is responsible for relationships and to implementing and operating a bus refurbishment centre. Braddell enforcing effective 'systems and controls to also has an interest in operating express coach ensure slavery and human trafficking is not services in the Republic of Ireland through a taking place anywhere in our supply chains.