Virtual Analyst Event

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S. and Worldwide September 2020 Contents Acknowledgements ....................................................................................................................................... 2 Executive Summary ...................................................................................................................................... 3 Drivers of Global Electric Vehicle Growth – Global Goals to Phase out Internal Combustion Engines ..... 6 Policy Drivers of U.S. Electric Vehicle Growth ........................................................................................... 8 Manufacturer Commitments ....................................................................................................................... 10 Job Creation ................................................................................................................................................ 13 Charging Network Investments .................................................................................................................. 15 Commercial Fleet Electrification Commitments ........................................................................................ 17 Sales Forecast.............................................................................................................................................. 19 Battery Pack Cost Projections and EV Price Parity ................................................................................... -

ELECTRIC VEHICLES MARKET IS POWERING up an Industry Snapshot

Investment and Company Research Opportunity Research INDUSTRY SNAPSHOT July 2, 2020 ELECTRIC VEHICLES MARKET IS POWERING UP An Industry Snapshot Featured Companies: Tesla (NASDAQ - TSLA); Nikola (NASDAQ – NKLA); Workhorse Group (NASDAQ – WKHS); Alternet Systems (OTC – ALYI) www.goldmanresearch.com Copyright © Goldman Small Cap Research, 2020 Page 1 of 8 Investment and Company Research Opportunity Research INDUSTRY SNAPSHOT OUR THESIS: As of this writing, shares of Tesla (NASDAQ – TSLA), the undisputed bellwether stock for the electric vehicle market trades at $1121 per share. At current prices, the market cap is over $207 billion, representing over 5 estimated 2021 sales and a whopping 98x next year’s EPS. In many investors’ minds, where Tesla goes, so goes the industry segment, especially as it relates to the capital markets. While TSLA is the industry’s most important company, it is the exact mid-point of 2020, not 2016, and therefore is not the only pubco in the space. In fact, some under the radar firms with exposure to the space offer major upside that may rival TSLA, with varying risk profiles and share prices. Instead of making the case for the industry and its constituents in the lithium, fuel cell, and other segments, we have elected to focus on the vehicle producers, where we believe the greatest attention and upside exist. THE EV MARKET: A BRIEF HISTORY We began writing about the EV market in 2015/2016 and while going over our old reports and blogs, we came across some striking information. In 2016, Bloomberg New Energy Finance (now billed as Bloomberg NEF) projected that by 2040, EV passenger sales will reach 41 million units. -

Advanced Technology Equipment Manufacturers*

Advanced Technology Equipment Manufacturers* Revised 04/21/2020 On-Road (Medium/Heavy Duty, Terminal Tractors) OEM Model Technology Vocations GVWR Type Altec Industries, Inc Altec 12E8 JEMS ePTO ePTO ePTO, Utility > 33,000, 26,001 - 33,000 New Altec Industries, Inc Altec JEMS 1820 and 18E20 ePTO ePTO ePTO, Utility > 33,000, 26,001 - 33,000 New Altec Industries, Inc Altec JEMS 4E4 with 3.6 kWh Battery ePTO ePTO, Utility 16,001-19,500, 19,501-26,000 New Altec Industries, Inc Altec JEMS 6E6 with 3.6 kWh Battery ePTO ePTO, Utility 16,001-19,500, 19,501-26,000 New Autocar Autocar 4x2 and 6x4 Xpeditor with Cummins-Westport ISX12N Engine Near-Zero Engine Truck > 33,001 New Autocar Autocar 4x2 and 6x4 Xpeditor with Cummins-Westport L9N Engine Near-Zero Engine Refuse > 33,001 New Blue Bird Blue Bird Electric Powered All American School Bus Zero Emission Bus, School Bus > 30,000 New Blue Bird Blue Bird Electric Powered Vision School Bus 4x2 Configuration Zero Emission Bus, School Bus > 30,000 New BYD Motors BYD 8Y Electric Yard Tractor Zero Emission Terminal Truck 81,000 New BYD Motors BYD C10 45' All-Electric Coach Bus Zero Emission Bus 49,604 New BYD Motors BYD C10MS 45' All-Electric Double-Decker Coach Bus Zero Emission Transit Bus 45' New BYD Motors BYD C6 23' All-Electric Coach Bus Zero Emission Bus 18,331 New BYD Motors BYD K11 60' Articulated All-Electric Transit Bus Zero Emission Bus 65,036 New BYD Motors BYD K7M 30' All-Electric Transit Bus Zero Emission Bus, Transit Bus 30' New BYD Motors BYD K9 40' All-Electric Transit Bus Zero Emission -

DIAMONDPEAK HOLDINGS CORP. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported): September 17, 2020 DIAMONDPEAK HOLDINGS CORP. (Exact name of registrant as specified in its charter) Delaware 001-38821 83-2533239 (State or other jurisdiction (Commission (IRS Employer of incorporation) File Number) Identification No.) 40 W 57th Street, 29th Floor New York, New York 10019 (Address of principal executive offices, including zip code) Registrant’s telephone number, including area code: (212) 716-2000 N/A (Former name or former address, if changed since last report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☒ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Units, each consisting of one share of Class A common stock, DPHCU The Nasdaq Stock Market LLC $0.0001 par value, and one-third of one Warrant Class A common stock, par value $0.0001 per share DPHC The Nasdaq Stock Market LLC Warrants to purchase Class A common stock DPHCW The Nasdaq Stock Market LLC Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). -

11 Electric Vehicle Stocks to Buy for 2021

INVESTOR PLACE 11 ELECTRIC VEHICLE STOCKS TO BUY FOR 2021 LUKE LANGO How to turn the electric disruption of transportation into your million-dollar opportunity When it comes to identifying next-generation breakthrough investments that could rise 100%, 200%, 500%, or more, I always come back to one saying. Where there’s disruption, there’s opportunity. Case-in-point: The internet. Throughout the 1990s, the emergence of the internet rapidly disrupted how people across the globe worked, communicated, and played. For many, it was a scary time. Change is never easy. For many more, it was an exciting time, as the internet was unlocking a new world of possibilities. But… for investors… it was an opportunity. Specifically, it was a once-in-a-decade opportunity to invest early in emerging titans of the internet industry. Like Amazon (AMZN)… when it was a $438 million company in 1997… It’s a $1.6 TRILLION company today – representing a whopping 365,000% return. That means a mere $1,000 investment in Amazon in 1997 would be worth more than $3.6 million today. 2 Luke Lango’s Hypergrowth Investing Need I say more? Where there’s disruption, there’s opportunity – and the bigger the disruption, the bigger the opportunity. Right now, we are on the cusp of an enormous disruption. This disruption will fundamentally and entirely change the world’s multi-trillion-dollar transportation work. In its wake, it will create new hundred-billion-dollar titans of the auto industry – most of whom are just tiny companies today. What disruption am I talking about specifically? The shift toward electric vehicles. -

Burleson & Company, LLC Form 13F-HR Filed 2021-05-12

SECURITIES AND EXCHANGE COMMISSION FORM 13F-HR Initial quarterly Form 13F holdings report filed by institutional managers Filing Date: 2021-05-12 | Period of Report: 2021-03-31 SEC Accession No. 0001104659-21-064935 (HTML Version on secdatabase.com) FILER Burleson & Company, LLC Mailing Address Business Address 201 1ST STREET, SUITE 204 201 1ST STREET, SUITE 204 CIK:1733510| IRS No.: 201160877 | State of Incorp.:CA | Fiscal Year End: 1231 PETALUMA CA 94952 PETALUMA CA 94952 Type: 13F-HR | Act: 34 | File No.: 028-18696 | Film No.: 21913955 (707) 283-0520 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE OMB Number: 3235-0006 COMMISSION Expires: July 31, 2015 Washington, D.C. 20549 Estimated average burden hours per response: 23.8 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: 03-31-2021 Check here if Amendment: ☐ Amendment Number: This Amendment (Check only one.): ☐ is a restatement. ☐ adds new holdings entries. Institutional Investment Manager Filing this Report: Name: Burleson & Company, LLC Address: 201 1st Street, Suite 204 Petaluma, CA 94952 Form 13F File Number: 028-18696 The institutional investment manager filing this report and the person by whom it is signed hereby represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: James Burleson Title: Principal and Chief Compliance Officer Phone: 707-283-0520 Signature, Place, and Date of Signing: /s/ James Burleson Petaluma, CALIFORNIA 05-12-2021 [Signature] [City, State] [Date] Report Type (Check only one.): ☒ 13F HOLDINGS REPORT. -

GM Sells Shuttered Ohio Assembly Plant to Electric Vehicle Startup by David Welch November 7, 2019, 3:10 PM EST

Hyperdrive GM Sells Shuttered Ohio Assembly Plant to Electric Vehicle Startup By David Welch November 7, 2019, 3:10 PM EST Lordstown Motors is still raising money for its plug-in pickup CEO Steve Burns says he hopes to start production in late 2020 rally-goers from selling their homes because of all the jobs he would bring back to the area. Democrats seized on the development as a symbol of unfulfilled promises made to voters in a key battleground state. Trump was so eager to endorse GM’s discussions to sell the Lordstown plant that he preempted the announcement of the talks in May by the largest U.S. automaker and Workhorse. But both companies are on shaky financial footing, with Workhorse totaling just $6,000 of revenue during its latest quarter. American flags fly in front of the GM plant in Lordstown, Ohio, in March. The automaker has sold the factory to Lordstown Motors. Lordstown Motors Corp., the electric-truck startup formed specifically to save a shuttered Ohio car factory, has acquired the highly politicized plant from General Motors Co. The acquisition that the two companies announced Thursday ends an era that began when GM opened the complex in 1966. The factory’s fate was largely sealed when the United Auto Workers union was unable to convince GM to keep it in the fold as part of a new labor contact ratified late last month. With the plant acquisition out of the way, Steve Burns, who Terms of the deal aren’t being disclosed. Workhorse Group used to lead Workhorse and is now chief executive officer Inc., which is affiliated with Lordstown Motors but doesn’t of Lordstown Motors, is turning his attention to phase two: share any ownership, soared 27% to close at $3.13 in New seeking cash to convert the Lordstown plant from making York trading. -

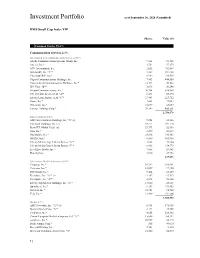

DWS Small Cap Index VIP

Investment Portfolio as of September 30, 2020 (Unaudited) DWS Small Cap Index VIP ______________________Shares Value ($) Common Stocks 98.6% Communication Services 2.3% Diversified Telecommunication Services 0.8% Alaska Communications Systems Group, Inc. 9,664 19,328 Anterix, Inc.* 1,751 57,275 ATN International, Inc. 2,052 102,887 Bandwidth, Inc. "A"* 3,387 591,268 Cincinnati Bell, Inc.* 8,969 134,535 Cogent Communications Holdings, Inc. 7,403 444,550 Consolidated Communications Holdings, Inc.* 12,394 70,522 IDT Corp. "B"* 3,076 20,240 Iridium Communications, Inc.* 20,284 518,865 Liberty Latin America Ltd. "A"* 8,472 69,894 Liberty Latin America Ltd. "C"* 27,483 223,712 Ooma, Inc.* 3,608 47,084 Orbcomm, Inc.* 12,899 43,857 Vonage Holdings Corp.* 39,742 _________406,561 2,750,578 Entertainment 0.2% AMC Entertainment Holdings, Inc. "A" (a) 9,254 43,586 Cinemark Holdings, Inc. (a) 19,171 191,710 Eros STX Global Corp* (a) 23,773 52,538 Gaia, Inc.* 2,099 20,633 Glu Mobile, Inc.* 24,816 190,463 IMAX Corp.* 8,860 105,966 Liberty Media Corp.-Liberty Braves "A"* 1,868 39,004 Liberty Media Corp.-Liberty Braves "C"* 6,415 134,779 LiveXLive Media, Inc.* 7,885 20,462 Marcus Corp. 3,616 _________27,952 827,093 Interactive Media & Services 0.4% Cargurus, Inc.* 14,792 319,951 Cars.com, Inc.* 12,057 97,420 DHI Group, Inc.* 9,464 21,389 Eventbrite, Inc. "A"* (a) 11,367 123,332 EverQuote, Inc. "A"* 2,494 96,368 Liberty TripAdvisor Holdings, Inc. -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Workhorse Group, INC--The Small Cincinnati Company “Delivering” in the Electric Vehicle Race

June 2020 Will Brown Adam Eagleston CEO and Managing Partner CIO Workhorse Group, INC--The Small Cincinnati Company “Delivering” in the Electric Vehicle Race It is rare to find a company at the intersection of two major trends; it’s even more unusual that it is in your hometown. However, that is the case with the aptly named Workhorse Group, Inc. (ticker: WKHS) headquartered in Loveland, OH. Formidable Asset Management (“FAM”) recently established a position; following are the key pieces of our investment thesis: • Established technology and infrastructure • Marquee customers • Undervalued investments Overview Workhorse manufactures electric vehicles (both land-based and aerial), predominantly for use in deliveries (think Amazon, UPS, or the U.S. Postal Service). Despite its presence in this attractive niche, valuable intellectual property, and potentially transformative strategic partnerships, the company trades at a significant discount to our estimate of its intrinsic value. Established technology and infrastructure The company builds more than electric vehicles; it has developed an integrated platform to offer clients a holistic delivery solution that includes cost efficient ground vehicles, telematics to optimize deliveries, and unmanned aerial systems (UASs) for last mile delivery. In the company’s opinion, it is a first mover with a two-to-three year head start over its competitors, which is critically important. Once established, it is very difficult to displace an incumbent within the context of a vehicle fleet, especially one that is integrated. The company has seven (7) granted and four (4) pending patents. As we’ll see later, some of Workhorse’s core electric vehicle intellectual property is currently being licensed. -

Gm's Closed Lordstown Factory Spawns a Wave of Industrial Migrants

GM’S CLOSED LORDSTOWN FACTORY SPAWNS A WAVE OF INDUSTRIAL MIGRANTS Workers leave their families behind in Ohio in search of good pay and benefits in other states. By Michael Phillips and Nora Naughton November 29, 2020 On Zach Sherry’s first day of work at the General Motors Co. factory in Bedford, Ind., trainers gave a safety presentation that included an image of a cartoon hand spurting blood from the ring finger. The overt message was straightforward: Rings can get caught in the machinery, so don’t wear them on the job. The symbolism wasn’t lost on the 48-year-old Mr. Sherry, who had transferred to the Indiana facility after losing his previous job at the GM plant in Lordstown, Ohio, that shut down last year. The transfer meant leaving his family behind one state away. “You just took me 450 miles from my home and you’re telling me to take my wedding ring off,” he says. Mr. Sherry is one of a cadre of Lordstown workers turned middle-aged industrial migrants, venturing out alone in search of good pay and benefits. Itinerant work has long been common in manufacturing, including people moving around the country for fracking jobs. Auto workers haven’t been immune to chasing their livelihoods across state lines, either. When GM and Chrysler LLC. closed plants as part of their bankruptcy restructurings a decade ago, workers were moved to the factories that survived. The workers in Lordstown, many of whom are multigenerational GM employees, never planned to be among them. The plant was an example of American manufacturing might when it opened in 1966, churning out Chevrolet Impalas, Bel Airs and Caprices. -

United States Securities and Exchange Commission Form

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of report (Date of earliest event reported): June 17, 2021 LORDSTOWN MOTORS CORP. (Exact name of registrant as specified in its charter) Delaware 001-38821 83-2533239 (State or other Jurisdiction (Commission (IRS Employer of Incorporation) File Number) Identification No.) 2300 Hallock Young Road Lordstown, Ohio 44481 (Address of principal executive offices and Zip Code) (234) 285-4001 (Registrant’s telephone number, including area code) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Trading Name of each exchange Title of each class Symbol(s) on which registered Class A common stock, par value $0.0001 per share RIDE The Nasdaq Stock Market LLC Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).