Automotive Industry Outlook: Staying Ahead of the Curve in a Rapidly Changing Landscape March 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Enel Green Power, Sharp and Stmicroelectronics Sign Agreement for the Largest Photovoltaic-Panel Manufacturing Plant in Italy

Enel Green Power, Sharp and STMicroelectronics Sign Agreement for the Largest Photovoltaic-Panel Manufacturing Plant in Italy January 4, 2010 3:04 AM ET Enel Green Power, Sharp and STMicroelectronics join forces to produce innovative thin-film photovoltaic panels. The plant, located in Catania, Italy, is expected to have initial production capacity of 160 MW per year and is targeted to grow to 480 MW over the next years. In addition, Enel Green Power and Sharp will jointly develop solar farms focusing on the Mediterranean area, with a total installed capacity at a level of 500 MW, by the end of 2016. Geneva, January 4, 2010 – Today, Enel Green Power, Sharp and STMicroelectronics signed an agreement for the manufacture of triple-junction thin-film photovoltaic panels in Italy. At the same time, Enel Green Power and Sharp signed a further agreement to jointly develop solar farms. Today's agreement regarding the photovoltaic panel factory follows the Memorandum of Understanding signed in May 2008 by Enel Green Power and Sharp. STMicroelectronics has joined this strategic partnership. This agreement marks the first time that three global technology and industrial powerhouses have joined together in an equal partnership to contribute their unique value-add to the solar industry. It brings together Enel Green Power, with its international market development and project management know-how; Sharp, and its exclusive triple-junction thin-film technology, which will be operational in the mother plant in Sakai, Japan as of spring 2010; and STMicroelectronics, with its manufacturing capacity, skills and resources in highly advanced, hi-tech sectors such as microelectronics. -

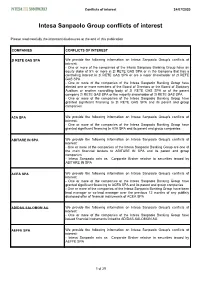

Intesa Sanpaolo Group Conflicts of Interest

Conflicts of interest 24/07/2020 Intesa Sanpaolo Group conflicts of interest Please read carefully the important disclosures at the end of this publication COMPANIES CONFLICTS OF INTEREST 2I RETE GAS SPA We provide the following information on Intesa Sanpaolo Group's conflicts of interest: - One or more of the companies of the Intesa Sanpaolo Banking Group have an equity stake of 5% or more in 2I RETE GAS SPA or in the Company that has a controlling interest in 2I RETE GAS SPA or are a major shareholder of 2I RETE GAS SPA - One or more of the companies of the Intesa Sanpaolo Banking Group have elected one or more members of the Board of Directors or the Board of Statutory Auditors or another controlling body of 2I RETE GAS SPA or of the parent company 2I RETE GAS SPA or the majority shareholder of 2I RETE GAS SPA - One or more of the companies of the Intesa Sanpaolo Banking Group have granted significant financing to 2I RETE GAS SPA and its parent and group companies A2A SPA We provide the following information on Intesa Sanpaolo Group's conflicts of interest: - One or more of the companies of the Intesa Sanpaolo Banking Group have granted significant financing to A2A SPA and its parent and group companies ABITARE IN SPA We provide the following information on Intesa Sanpaolo Group's conflicts of interest: - One or more of the companies of the Intesa Sanpaolo Banking Group are one of the main financial lenders to ABITARE IN SPA and its parent and group companies - Intesa Sanpaolo acts as Corporate Broker relative to securities issued -

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S. and Worldwide September 2020 Contents Acknowledgements ....................................................................................................................................... 2 Executive Summary ...................................................................................................................................... 3 Drivers of Global Electric Vehicle Growth – Global Goals to Phase out Internal Combustion Engines ..... 6 Policy Drivers of U.S. Electric Vehicle Growth ........................................................................................... 8 Manufacturer Commitments ....................................................................................................................... 10 Job Creation ................................................................................................................................................ 13 Charging Network Investments .................................................................................................................. 15 Commercial Fleet Electrification Commitments ........................................................................................ 17 Sales Forecast.............................................................................................................................................. 19 Battery Pack Cost Projections and EV Price Parity ................................................................................... -

TEA6422 TEA6422D TEA6422DT Stmicroelectronics Datasheet

TEA6422 BUS-CONTROLLED AUDIO MATRIX ■ 6 Stereo Inputs ■ 3 Stereo Ouputs ■ Gain Control 0 dB/Mute for each Output ■ Cascadable (2 different addresses) ■ Serial Bus Controlled ■ Very Low Noise ■ Very Low Distorsion SHRINK DIP24 ■ Fully ESD Protected (Shrink Plastic Package) ■ Wide Audio Dynamic Range ( 3 V ) RMS ORDER CODE: TEA6422 DESCRIPTION The TEA6422 switches 6 stereo audio inputs on 3 stereo outputs. All the switching possibilities are changed through the I2C BUS. SO28 (Plastic Monopackage) ORDER CODE: TEA6422D Figure 1. PIN CONNECTIONS SO28 SDIP24 GND 1 28 SDA GND 1 24 SDA CAPACITANCE 2 27 SCL 2 23 CAPACITANCE SCL VS 3 26 ADDR VS 3 22 ADDR L1 4 25 R1 L1 4 21 R1 L2 5 24 R2 L2 5 20 R2 L3 6 23 R3 L3 6 19 R3 NC 7 22 NC L4 7 18 R4 NC 8 21 NC L5 8 17 R5 L4 9 20 R4 L6 9 16 R6 L5 10 19 R5 LOUT1 10 15 ROUT3 L6 11 18 R6 ROUT1 11 14 LOUT3 LOUT1 12 17 ROUT3 LOUT2 12 13 ROUT2 ROUT1 13 16 LOUT3 LOUT2 14 15 ROUT2 September 2003 1/10 1 TEA6422 BLOCK DIAGRAM RIGHT INPUTS GAIN = 0 dB RIGHT OUTPUTS VS SDA C SUPPLY BUS DECODER SCL GND ADDR LEFT OUTPUTS GAIN = 0 dB LEFT INPUTS ABSOLUTE MAXIMUM RATINGS Symbol Parameter Value Unit VCC Supply Voltage 12 V o Toper Operating Temperature 0, + 70 C o Tstg Storage Temperature - 20, + 150 C THERMAL DATA Symbol Parameter Value Unit SDIP24 75 oC/W R (j-a) Junction - ambient Thermal Resistance th SO28 75 oC/W 2/10 1 TEA6422 ELECTRICAL CHARACTERISTICS o Ω Ω TA = 25 C, VS = 9 V, RL = 10 k , RG = 600 , f = 1 kHz (unless otherwise specified) Symbol Parameter Test Conditions Min. -

4133-6266-6020.6 EMTN PROGRAMME PROSPECTUS This

EMTN PROGRAMME PROSPECTUS This document constitutes two base prospectuses: (i) the base prospectus of TIM S.p.A. and (ii) the base prospectus of Telecom Italia Finance S.A. (together, the EMTN Programme Prospectus). TIM S.p.A. (incorporated with limited liability under the laws of the Republic of Italy) TELECOM ITALIA FINANCE S.A. (incorporated with limited liability under the laws of the Grand-Duchy of Luxembourg) €20,000,000,000 Euro Medium Term Note Programme unconditionally and irrevocably guaranteed in respect of Notes issued by Telecom Italia Finance S.A. by TIM S.p.A. (incorporated with limited liability under the laws of the Republic of Italy) Under this €20,000,000,000 Euro Medium Term Note Programme (the Programme), TIM S.p.A. (TIM) and Telecom Italia Finance S.A. (TI Finance and, together with TIM in its capacity as an issuer, the Issuers and each an Issuer) may from time to time issue notes (the Notes) denominated in any currency agreed with the relevant Dealer (as defined below). Payment of all amounts owing in respect of the Notes issued by TI Finance will be unconditionally and irrevocably guaranteed by TIM (in such capacity, the Guarantor). The maximum aggregate nominal amount of all Notes from time to time outstanding under the Programme will not exceed €20,000,000,000 (or its equivalent in other currencies calculated as described in the Programme Agreement), subject to increase as described herein. The Notes may be issued on a continuing basis to one or more of the Dealers specified under “Overview of the Programme” and any additional Dealer appointed under the Programme from time to time by the Issuers (each a Dealer and, together, the Dealers), which appointment may be for a specific issue or on an ongoing basis. -

World's Smallest Micro-Mirror Scanning Technology From

Press release Communiqué de presse Comunicato stampa 新闻稿 / 新聞稿 プレスリリース 보도자료 T4264D World’s Smallest Micro-Mirror Scanning Technology from STMicroelectronics Chosen for Intel® RealSense™ High-Resolution LiDAR Depth Camera L515 Power-efficient, hi-res LiDAR camera capturing millions of depth points per second suits a wide range of Industrial and Computing use cases Geneva, March 8, 2021 – STMicroelectronics (NYSE: STM), a global semiconductor leader serving customers across the spectrum of electronics applications, has developed a tiny MEMS mirror with Intel enabling spatial scanning of an environment. Intel developed a LiDAR system based on this micro-mirror, providing high-resolution scanning for industrial applications such as robotic arms for bin picking, volumetric measurements, logistics, and 3D scanning. Built into the Intel RealSense LiDAR1 Camera L515, the small dimensions of the ST micro-mirror contribute to the LiDAR camera’s hockey-puck size (61mm diameter x 26mm height). The micro-mirror enables continuous laser scanning across the entire field of view. In combination with a custom photodiode sensor, the RealSense LiDAR Camera L515 renders a 3D depth map of the entire scene. “With 30 frames per second and a field-of-view of 70° by 55°, ST’s 2nd-generation micro-mirror continues to set the bar for 3D scanning and detection applications,” said Benedetto Vigna, President Analog, MEMS and Sensors Group, STMicroelectronics. “Continuing the long-term supply relationship for micro-mirrors with Intel demonstrates our never-ending efforts to leverage our long-lasting leadership in MEMS to meet the demanding technical and supply needs of our customers.” The L515 leverages the scanning capabilities of ST’s MEMS to deliver high-resolution depth with no interpolated pixels, the ability to control the field of view, and provides close to zero pixel blur driven by the low 50nS exposure time. -

Burleson & Company, LLC Form 13F-HR Filed 2021-05-12

SECURITIES AND EXCHANGE COMMISSION FORM 13F-HR Initial quarterly Form 13F holdings report filed by institutional managers Filing Date: 2021-05-12 | Period of Report: 2021-03-31 SEC Accession No. 0001104659-21-064935 (HTML Version on secdatabase.com) FILER Burleson & Company, LLC Mailing Address Business Address 201 1ST STREET, SUITE 204 201 1ST STREET, SUITE 204 CIK:1733510| IRS No.: 201160877 | State of Incorp.:CA | Fiscal Year End: 1231 PETALUMA CA 94952 PETALUMA CA 94952 Type: 13F-HR | Act: 34 | File No.: 028-18696 | Film No.: 21913955 (707) 283-0520 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE OMB Number: 3235-0006 COMMISSION Expires: July 31, 2015 Washington, D.C. 20549 Estimated average burden hours per response: 23.8 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: 03-31-2021 Check here if Amendment: ☐ Amendment Number: This Amendment (Check only one.): ☐ is a restatement. ☐ adds new holdings entries. Institutional Investment Manager Filing this Report: Name: Burleson & Company, LLC Address: 201 1st Street, Suite 204 Petaluma, CA 94952 Form 13F File Number: 028-18696 The institutional investment manager filing this report and the person by whom it is signed hereby represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: James Burleson Title: Principal and Chief Compliance Officer Phone: 707-283-0520 Signature, Place, and Date of Signing: /s/ James Burleson Petaluma, CALIFORNIA 05-12-2021 [Signature] [City, State] [Date] Report Type (Check only one.): ☒ 13F HOLDINGS REPORT. -

GM Sells Shuttered Ohio Assembly Plant to Electric Vehicle Startup by David Welch November 7, 2019, 3:10 PM EST

Hyperdrive GM Sells Shuttered Ohio Assembly Plant to Electric Vehicle Startup By David Welch November 7, 2019, 3:10 PM EST Lordstown Motors is still raising money for its plug-in pickup CEO Steve Burns says he hopes to start production in late 2020 rally-goers from selling their homes because of all the jobs he would bring back to the area. Democrats seized on the development as a symbol of unfulfilled promises made to voters in a key battleground state. Trump was so eager to endorse GM’s discussions to sell the Lordstown plant that he preempted the announcement of the talks in May by the largest U.S. automaker and Workhorse. But both companies are on shaky financial footing, with Workhorse totaling just $6,000 of revenue during its latest quarter. American flags fly in front of the GM plant in Lordstown, Ohio, in March. The automaker has sold the factory to Lordstown Motors. Lordstown Motors Corp., the electric-truck startup formed specifically to save a shuttered Ohio car factory, has acquired the highly politicized plant from General Motors Co. The acquisition that the two companies announced Thursday ends an era that began when GM opened the complex in 1966. The factory’s fate was largely sealed when the United Auto Workers union was unable to convince GM to keep it in the fold as part of a new labor contact ratified late last month. With the plant acquisition out of the way, Steve Burns, who Terms of the deal aren’t being disclosed. Workhorse Group used to lead Workhorse and is now chief executive officer Inc., which is affiliated with Lordstown Motors but doesn’t of Lordstown Motors, is turning his attention to phase two: share any ownership, soared 27% to close at $3.13 in New seeking cash to convert the Lordstown plant from making York trading. -

John Hancock Disciplined Value International Fund A: JDIBX C: JDICX I: JDVIX R2: JDISX R4: JDITX R6: JDIUX

All data is as of June 30, 2021 Q2 - 2021 International equity fund Quarterly commentary John Hancock Disciplined Value International Fund A: JDIBX C: JDICX I: JDVIX R2: JDISX R4: JDITX R6: JDIUX Objective Use for Morningstar category Long-term growth of capital Core international holding Foreign Large Value Quarterly commentary Highlights The fund beneited from strong stock selection in the communication International equities rallied in the second quarter, helping the fund’s services sector, where SK Telecom Co., Ltd. was a top performer ater its benchmark—the MSCI EAFE Index—achieve a series of all-time highs management announced a plan to split the company in two to recognize before it peaked in mid-June. value. The fund also outperformed in energy, due largely to a rally in shares The fund delivered a positive return, but it trailed the index. of Cenovus Energy, Inc., IMI PLC, and Hitachi Corp. All three companies Given the underperformance of the value style relative to growth, the were top contributors for the quarter, as was a zero weighting in the fund’s value-driven strategy was a headwind to results compared with the Japanese company Sotbank Group Corp. broad-based benchmark. Market review and outlook Portfolio changes International stocks performed well in the past three months as economic We increased the fund’s weightings in industrials and healthcare while data continued to improve as the gradual rollout of vaccines fostered a reducing its allocation to information technology. The changes were all resumption of normal business conditions. Broad measures of consumer stock speciic, and the structure of the portfolio didn’t change materially. -

Euro Stoxx® Residual Momentum Premium Index

EURO STOXX® RESIDUAL MOMENTUM PREMIUM INDEX Components1 Company Supersector Country Weight (%) EUROFINS SCIENTIFIC null null 3.37 SARTORIUS STEDIM BIOTECH null null 3.20 EDP RENOVAVEIS null null 2.97 HELLOFRESH AG null null 2.21 SIEMENS GAMESA null null 2.21 SARTORIUS PREF. null null 2.16 KESKO null null 2.07 DEUTSCHE POST null null 1.89 CORBION null null 1.81 BRENNTAG null null 1.80 SIGNIFY null null 1.75 ZALANDO null null 1.68 SEB null null 1.56 LVMH MOET HENNESSY null null 1.52 BOLLORE null null 1.48 INTERPUMP GRP null null 1.45 SIEMENS null null 1.44 CAP GEMINI null null 1.41 RATIONAL null null 1.41 BMW null null 1.40 BANCO BPM null null 1.37 FUCHS PETROLUB PREF null null 1.30 SOITEC null null 1.27 SAINT GOBAIN null null 1.25 PUBLICIS GRP null null 1.23 MICHELIN null null 1.22 UNIBAIL-RODAMCO-WESTFIELD null null 1.20 WARTSILA null null 1.15 CAIXABANK null null 1.13 STELLANTIS null null 1.12 CNH Industrial NV null null 1.12 SOLVAY null null 1.11 BCO BILBAO VIZCAYA ARGENTARIA null null 1.09 PROSIEBENSAT.1 MEDIA null null 1.08 NOKIAN RENKAAT null null 1.08 COVESTRO null null 1.06 DEUTSCHE BANK null null 1.02 INFINEON TECHNOLOGIES null null 1.02 DAIMLER null null 1.02 STMICROELECTRONICS null null 1.02 CONTINENTAL null null 1.01 REXEL null null 0.99 FLUTTER ENTERTAINMENT null null 0.99 AALBERTS null null 0.99 COMMERZBANK null null 0.95 RYANAIR null null 0.94 HEIDELBERGCEMENT null null 0.93 BASF null null 0.93 ASML HLDG null null 0.93 SPIE null null 0.90 ING GRP null null 0.90 ELIS null null 0.89 HERMES INTERNATIONAL null null 0.88 ASM -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Gm's Closed Lordstown Factory Spawns a Wave of Industrial Migrants

GM’S CLOSED LORDSTOWN FACTORY SPAWNS A WAVE OF INDUSTRIAL MIGRANTS Workers leave their families behind in Ohio in search of good pay and benefits in other states. By Michael Phillips and Nora Naughton November 29, 2020 On Zach Sherry’s first day of work at the General Motors Co. factory in Bedford, Ind., trainers gave a safety presentation that included an image of a cartoon hand spurting blood from the ring finger. The overt message was straightforward: Rings can get caught in the machinery, so don’t wear them on the job. The symbolism wasn’t lost on the 48-year-old Mr. Sherry, who had transferred to the Indiana facility after losing his previous job at the GM plant in Lordstown, Ohio, that shut down last year. The transfer meant leaving his family behind one state away. “You just took me 450 miles from my home and you’re telling me to take my wedding ring off,” he says. Mr. Sherry is one of a cadre of Lordstown workers turned middle-aged industrial migrants, venturing out alone in search of good pay and benefits. Itinerant work has long been common in manufacturing, including people moving around the country for fracking jobs. Auto workers haven’t been immune to chasing their livelihoods across state lines, either. When GM and Chrysler LLC. closed plants as part of their bankruptcy restructurings a decade ago, workers were moved to the factories that survived. The workers in Lordstown, many of whom are multigenerational GM employees, never planned to be among them. The plant was an example of American manufacturing might when it opened in 1966, churning out Chevrolet Impalas, Bel Airs and Caprices.