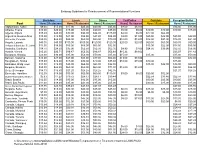

Quarterly Forecast

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Manama Connects Issue No

THE E-NEWSLETTER OF THE EMBASSY OF MALAYSIA IN BAHRAIN MANAMA CONNECTS ISSUE NO. 14 – APRIL TO JUNE 2020 MALAWAKIL MANAMA EID-UL-FITR 1441/2020 CELEBRATION Muslims around the world celebrated Eid-ul Fitr this year in a new normal including us in Manama, Kingdom of Bahrain. However, the celebration of Eid-ul Fitr on 24 May 2020 at Malaysia House was still full of happiness with lots of delicious special Raya dishes enjoyed by Embassy’s staff and families only. It started with photo session, brunch and ended with takbir led by Ambassador Agus Salim bin Yusof. Prior to that, the Ambassador sent his Eid-ul Fitr message by email to all Malaysian Muslims in Bahrain. On 28 May 2020, the fifth day of Syawal, the Embassy of Malaysia celebrated the Eid-ul Fitr with the Embassy’s staff. Colorful Malaysian traditional wear of batik, songket and baju melayu were worn by all officers and staff. The gathering was also to celebrate birthdays of staff who were born in the month of May and June. [TypeMANAMA here] CONNECTS [Type here] ISSUE 14: APRIL – JUNE[Type 2020 here] Courtesy Visit by New Ambassador Courtesy Visit by New Ambassador of Bangladesh to the Kingdom of of the Republic of Korea to the Bahrain Kingdom of Bahrain On 11 June 2020, Ambassador Agus Salim bin On 25 June 2020, Ambassador Agus Salim bin Yusof received in the Embassy, His Excellency Yusof received His Excellency Chung Hae Muhammad Nazrul Islam, Ambassador of Kwan, Ambassador of the Republic of Korea to Bangladesh to the Kingdom of Bahrain. -

Manama, Capital of Bahrain (Population: 1.4 Million) Dubai

FMM-SMF Joint Business Mission Bahrain & United Arab Emirates November 24-30, 2018 (Up to 50% FUNDING under Malaysia-Singapore Third Country Business Development Fund for two (2) representatives from each company ) Manama, Capital of Bahrain (Population: 1.4 million) Malaysia has been exporting halal products such as agricultural produce, batik, ceramics, clothing, cosmetics, frozen foods and wood products to Bahrain In 2017, Bahrain imported from Malaysia RM456 million worth of products including wood products (mainly sawn wood, wood fiberboard, and plywood), foodstuff and glazed ceramics Although a small island-nation, Bahrain’s geostrategic location and strong ties with Saudi Arabia . and other G.C.C. members position it as a “gateway to the Gulf” and the wider Arab world Dubai, Capital of United Arab Emirates (Population: 9.54 million) Dubai is the trading hub of the Middle East, Asia and Africa UAE is one of the top export destination in the West Asia region for Malaysia Malaysia exported RM12 billion worth of products and services to UAE including palm oil & palm oil-based products, E&E products, jewellery, metal, machinery and equipment Other products with potential market in UAE are food & beverages, furniture, building materials, telecommunication equipment, construction & related services, healthcare, ICT related services. Mission Highlights Visit to BIG 5, the largest building construction show in the Middle East Business matching meetings arranged by MATRADE, Bahrain Chamber of Commerce & Industry and Dubai Chamber -

Reservations Contact Detail

Reservations Contact Detail Name Richard Vangunster Position Assistant Revenue Manager Telephone +973-663-16666 Fax +973-663-16667 Email [email protected] & [email protected] 1. Cash, or other guaranteed form of payment 2. Credit card (We accept all major credit cards) 3. Electronic Funds Transfer to following hotel account Building 65, Road 4003, Block 340, Juffair, Kingdom of Bahrain Tel: +973-663-16666 Fax: +973-160-00098 wyndhamgardenmanama.com THE HARD FACTS MADE EASY Everything you need to know about your Wyndham Garden Manama JASHAN CAFE MOSAIC TRATTORIA DINING AND ENTERTAINMENT GETTING THERE Wyndham Garden Manama features world-class speciality dining and Directions from Bahrain International Airport entertainment options, that’s sure to deliver the finest experience in Distance: 10 Minutes the very heart of the city. Directions: Exit from Airport at the first roundabout, take road No. 2403 • Jashan - Savour the authentic taste of Indian cuisine with a wide to Arad highway and drive towards Khalifa Al Khabeer highway going variety of traditional Indian recipes reflecting the diversity towards Muharraq. Take Shaikh Hamad Causeway that goes towards of India. Manama. Enter left at Al Fateh highway and drive for 3 kms. Enter left • Café Mosaic - This international all day dining outlet is perfect again into Awal Avenue. At Al Fateh Grand Mosque signal, take the first for a business lunch or relaxed dining with friends and family. The right toward Shabab Avenue, then take right again at the end of Shabab restaurant offers a wide selection of delightful dishes prepared at live cooking stations. Avenue; followed by the second left on Road 4005. -

Embassy Guidelines for Reimbursement of Representational Functions

Embassy Guidelines for Reimbursement of Representational Functions Breakfast Lunch Dinner Tea/Coffee Cocktails Reception/Buffet Post Home Restaurant Home Restaurant Home Restaurant Home Restaurant Home Restaurant Home Restaurant Afghanistan, Kabul $9.00 $15.00 $17.00 $25.00 $20.00 $35.00 $8.00 $12.00 $14.00 $15.00 Albania, Tirana $10.00 $20.00 $15.00 $30.00 $20.00 $35.00 $5.00 $5.00 $10.00 $10.00 $10.00 $15.00 Algeria, Algiers $18.00 $40.00 $30.00 $90.00 $44.00 $125.00 $4.00 $6.00 $22.00 $64.00 Argentina, Buenos Aires $15.00 $18.50 $47.00 $54.00 $47.00 $54.00 $8.00 $11.00 $25.00 $42.00 $25.00 $42.00 Armenia, Yerevan $20.00 $22.00 $25.00 $60.00 $40.00 $70.00 $10.00 $12.00 $16.00 $21.00 $16.00 $21.00 Angola, Luanda $40.00 $40.00 $100.00 $100.00 $120.00 $120.00 $20.00 $20.00 $60.00 $60.00 $60.00 $50.00 Antigua & Barduda, St. Johns $11.00 $18.00 $45.00 $66.00 $63.00 $92.00 $15.00 $22.00 $34.00 $45.00 Australia, Canberra $14.70 $24.50 $35.00 $52.50 $52.50 $62.30 $4.90 $7.00 $24.50 $39.90 $52.50 $56.00 Austria, Vienna $15.26 $20.71 $46.87 $56.56 $46.87 $56.68 $15.26 $19.62 $25.07 $41.42 Bahamas, Nassau $20.00 $30.00 $35.00 $50.00 $70.00 $85.00 $15.00 $15.00 $15.00 $50.00 Bahrain, Manama $13.00 $27.00 $27.00 $53.00 $37.00 $66.00 $13.00 $19.00 $19.00 $32.00 Bangladesh, Dhaka $15.00 $20.00 $15.00 $30.00 $20.00 $35.00 $10.00 $15.00 $10.00 $15.00 Barbados, Bridgetown $11.00 $18.00 $45.00 $66.00 $63.00 $92.00 $15.00 $22.00 $34.00 $50.00 Belguim, Brussels $28.00 $28.00 $60.00 $60.00 $60.00 $71.00 $12.00 $12.00 $24.00 $24.00 Belize,Belmopan $14.10 -

4.617: Balancing Globalism and Regionalism: the Heart of Doha Project

SPRING 2009 DEPARTMENT OF ARCHITECTURE 4.617: Balancing Globalism and Regionalism: The Heart of Doha Project Instructor: Nasser Rabbat Prerequisite: Permission of Instructor Wednesday from 2 to 5 in Room 5-216 Prerequisite: Permission of instructor Submit two paragraph statement of intent to Nasser Rabbat, via email <[email protected]>, by Jan. 20th. Enrollment limited to 10 In the last two decades, the Arabian Gulf experienced an extraordinary urban boom fueled by a global economy looking for new, profitable outlets and an accumulated oil wealth seeking easy and safe invest- ments at home. The combined capital found its ideal prospect in developing gargantuan business parks and malls, luxury housing and hotels, and touristic, cultural, and entertainment complexes. Architecture at once assumed the role of branding instrument and spectacular wrapping for these new lavish enterprises, which swiftly sprang up in cities like Dubai, Doha, Abu Dhabi, Sharjah, Manama, Riyadh, and Kuwait. Yet, not all recent architecture in the Gulf readily fits what Joseph Rykwert matter-of-factly calls the “Emirate Style,” a style whose extravagant flights of fancy seem to depend only on the unbridled imagination of the designers and the willingness of their patrons to bankroll those fantasies. Various large-scale projects are trying to reverse the trend by judiciously using the vast financial resources available to produce quality design that tackles some of the most urgent social, cultural, and environmental issues facing those countries today. These urban and architectural experiments, like Masdar City in Abu Dhabi, the Heart of Doha in Qatar, and KAUST Campus in Jeddah, Saudi Arabia, hailed as design tours de force, have yet to be studied from a his- torical and sociocultural perspective. -

Oman - Today’S Spotlight, Tomorrow’S Destination

Oman - Today’s Spotlight, Tomorrow’s Destination Hala Matar Choufany, Consulting & Valuation Analyst Elie Younes, Associate Director HVS INTERNATIONAL LONDON 14 Hallam Street London, W1W 6JG +44 20 7878-7738 +44 20 7436-3386 (Fax) June 2005 New York San Francisco Boulder Denver Miami Dallas Chicago Washington, D.C. Weston, CT Phoenix Mt. Lakes, NJ Vancouver Toronto London Madrid New Delhi Singapore Hong Kong Sydney São Paulo Buenos Aires Newport, RI HVS International Oman – Today’s Spotlight, Tomorrow’s Destination 1 Oman – Today’s Spotlight, Tomorrow’s Destination By Hala Matar Choufany and Elie Younes, HVS International Many industry colleagues consider the Middle East hotel markets, and notably the GCC region, to have similar characteristics and dynamics; but is this really the case? While most GCC markets are similar in terms of their oil-based economies, and the insignificant quantity of natural resources that would support and stimulate a large amount of international leisure visitation, some destinations are just different. In spring 2005, we visited Oman to advise on the multibillion dollar Blue City development near Muscat. What we saw on our trip confirmed our views. The Middle East is once again proving to be resilient to the international and regional shocks affecting tourism worldwide. Destinations like Bahrain, Doha, Dubai and Egypt have recently achieved record levels of visitation and Oman seems to be following a similar trend. In this article, we shed some light on Oman, a newly emerging market with significant opportunities at all levels. The reader should note that we have paid most attention to Muscat, the Omani capital, in our assessment and analysis. -

November 2020 List of Participants 1 Afghanistan

NOVEMBER 2020 LIST OF PARTICIPANTS AFGHANISTAN ALGERIA Mr. Ajmal Ahmady Mr. Loumi Chaâbane Governor Subdirector of Statistics Afghanistan Central Bank MOF, General Tax Directorate Pashtonistan Watt Cité Malki-Ben Aknoun Kabul 1001 Algiers 16000 AFGHANISTAN ALGERIA Mr. Mustafa Sameh Mrs. Kendil Fatma Zohra Manager, Financial Stability Section On-site Supervisor Da Afghanistan Bank Banking Supervision & Inspection Dept. Pashtonistan Watt Bank of Algeria Kabul 1001 38 Ave. Franklin Roosevelt AFGHANISTAN Algiers 16000 ALGERIA Mr. Gul Mohammad Noori Ms. Fatma Zohra Dahmani Deputy Manager, Financial Stability Inspector, Off Site Supervision Dept . Da Afghanistan Bank Bank of Algeria Pashtonistan Watt 38, avenue Franklin Roosevelt Kabul 1001 Alger 16000 AFGHANISTAN ALGERIA ALBANIA ARMENIA Mr. Deniz Deralla Ms. Mariam Yeghiazaryan Director of Supervision Dept. Head of Banking System Regulation Division Bank of Albania Central Bank of Armenia Sheshi Skënderbej No. 1 Vazgen Sargsyan 6 Tirana 1001 Yerevan ALBANIA ARMENIA 0010 ALGERIA AUSTRALIA Ms. Sara Kennouche Mr. Wayne Byres Directorate General of Politics and Provision Chair Finance Ministries Australian Prudential Regulation Authority Ahmed Francis bldg. Level 12, 1 Martin Place Ben aknoun -Algiers Sydney 2000 ALGERIA AUSTRALIA 1 NOVEMBER 2020 LIST OF PARTICIPANTS AUSTRIA BAHRAIN Mr. Eduard Mueller Mr. Nabeel Juma Executive Director Superintendent, Financial Institutions Financial Market Authority Austria Regulatory Policy Otto Wagner Platz 5 Central Bank of Bahrain Vienna 1090 King Faisal Highway, Diplomatic Area, Block 317, AUSTRIA Road 1702, Building 96 Manama BAHRAIN Mrs. Katharina Muther-Pradler Head of Department of Integrated Supervision Ms. Reema Mandeel Financial Market Authority Austria Superintendent, Regulatory Policy Otto Wagner Platz 5 Central Bank of Bahrain Vienna 1090 King Faisal Highway, Diplomatic Area, Block 317, AUSTRIA Road 1702, Building 96 Manama BAHRAIN Dr. -

GCC Most Prominent Decisions

SLOVAKIA GCC most prominent decisions COLOMBIA Doha hosts the 35th summit 1980 1 st session The council confirmed that stability in the Gulf is linked to peace in the May 1981 - Abu Dhabi Middle -East, Palestine in particular 2 nd session The council signed the first 210 Nov. 1981 - Riyadh economic agreement aimed at abolishing million barriers between member countries 3 d session The establishment of Gulf Investment Foundation, with a capital of US$ 2 1982 - Manama billion 4 th session The council discussed political 1983 - Doha links and coordinating defense affairs between member States 5 th session The council approved the framework which organizes ownership right for 1984 - Kuwait citizens in member States 6 th session The council approved the 1985 - Muscat strategic vision of defense cooperation between member States 7 th session The council cooperation and coordination in security and communication 1986 - Abu Dhabi fields 8 th session The council approved oil lending 1987 - Riyadh system between members and set negotiation mechanisms with international economic groups 9 th session Allowing GCC citizens to own stocks in shareholding firms 1988 - Manama 10 th session The council discussed situation 1989 - Muscat in occupied Arab territories and the Palestinian Intifada fallouts 1990 11 th session The council discussed The 1990 - Doha Iraqi aggression on Kuwait, its gravity and threat to member States security 12 th session The council called on Iraq to 1991 - Kuwait release prisoners of war, demarcate borders and pay indemnities 13 th -

United States Postal Service Request for Information Air Transportation Services

RFI-Warzone-19 United States Postal Service Request for Information Air Transportation Services Air Transportation and Ancillary Services in the Warzone Region Scope and Objectives In accordance with the Postal Service’s Supplying Principles and Practices, the United States Postal Service (USPS or Postal Service) is issuing this Request for Information (RFI) to identify potential suppliers that are interested in and capable of providing a total air transportation and logistics solution for processing, transporting and delivering military mail to and from various combat destinations in Afghanistan, Bahrain and Kuwait. The Department of Defense (DoD) and USPS require reliable, secure end-to-end air transportation and logistics services. USPS operations at the Chicago International Service Center (ISC), Chicago, IL (ORD) and New Jersey Network Distribution Center (NDC), Jersey City, NJ (EWR) sort mail for tendering to end destinations. The processed mail is tendered to the supplier at the processing plant in ORD, or at the supplier’s warehouse facility at JFK for transport to end destination. The current transportation model consists of the Supplier consolidating mail within the United States and transporting it to the International Hub, in Manama, Bahrain (BAH) where the mail is sorted and segregated for transport to its final destination. The International Hub supports the processing and handling of military mail into and out of the combat zone. The supplier may utilize other approved transportation models which include: transporting mail from airports in EWR or New York (JFK) to the International Hub, or transporting mail from the supplier’s Hub to transfer locations in Brussels, Belgium (BRU) or Leipzig, Germany (LEJ), and then on to the International Hub or directly to the final destination. -

The Near & Middle East

The Near & Middle East Maggs Bros. Ltd. 48 Bedford Square London WC1B 3DR Telephone: +44 (0)20 7493 7160 Email: [email protected] © Maggs Bros Ltd 2020 THE ARABIAN PENINSULA A Handsome Portrait 1 [BAHRAIN]. Signed photograph of the Emir of Bahrain, Isa bin Salman Al Khalifa. Original silver gelatin photograph, measuring 820 by 139mm, signed in dark blue ink. A few light creases to bottom left corner, stamp of State of Bahrain, Ministry of Information and ms. caption in pencil to reverse. With an official State of Bahrain, Ministry of Information envelope, dated 1973. [Manama], Ministry of Information, [1973]. £500 A handsome photographic portrait of Isa bin Salman Al Khalifa (1931-1999), who was the first Emir of Bahrain, ruling for thirty- eight years. 1 With descriptions of Kuwait and Qatar its chief town, Doha, and its ruler, Sheikh Abdullah bin Jassim Al Thani (1880-1957). The Sheikh is described as “a rich and 2 GENERAL STAFF, INDIA. Field Notes. Mesopotamia. powerful chief, who has a following of about 2,000 fighting men.” February 1915. Catalogue No. M. 3. (p.179). He is also said to be “friendly toward the British … [and] would no doubt be glad to be rid of the Turks.” (p.180). The last First edition, one of 500 copies. With a folding heliozincographed comment proved to be somewhat prescient, as the Sheikh forced map of “Lower Mesopotamia”, dated 1914. Original limp tan the Ottomans to abandon their garrison in Doha on the 19th of buckram with wrap-around fastening tie, covers a little stained August 1915, just 6 months after this manual was prepared. -

Quarterly Forecast

MENA HOTELS QUARTERLY REVIEW Q2 | 2020 2 CONTENTS 3 Colliers Quarterly Update QUARTER | 2 2020 MENA QUARTER 4 Kingdom of Saudi Arabia Riyadh Jeddah MENA Quarterly Review | Colliers International International | Colliers Quarterly Review MENA Dammam/Khobar Makkah Madinah 5 United Arab Emirates Dubai Abu Dhabi Sharjah Ras Al Khaimah Fujairah 6 Egypt Cairo Alexandria Sharm El Sheikh Hurghada 7 Kuwait City, Kuwait 7 Manama, Bahrain 7 Muscat, Oman 7 Amman, Jordan 3 QUARTER | 2 2020 MENA QUARTER MENA Quarterly Review | Colliers International International | Colliers Quarterly Review MENA COLLIERS QUARTERLY UPDATE WTTC LAUNCHES SAFETY STAMPS FOR GLOBAL TRAVEL DESTINATIONS World Travel & Tourism Council (WTTC) issued safe travel protocols to standardize health and safety measures across hospitality and tourism sectors. The protocol was launched in May and includes several measures for social distancing, use of PPE and removal of extra items in hotels. Destinations in the MENA region which have received these Stamps are Tunisia, Jordan, Egypt, Dubai & RAK. NEW SAFETY CERTIFICATION FOR ABU DHABI HOTELS Abu Dhabi’s Department of Culture and Tourism have rolled out a new certification – “Go Safe Certification”, for hotels and attractions which are able to achieve high health and safety standards. The certification is intended to re-establish the confidence among the tourists to travel to the emirate ahead of its plan to reopen. W Abu Dhabi, was the first hotel to be Go Safe certified. LIMITED NUMBER OF PILGRIMS ALLOWED FOR HAJJ THIS YEAR The Ministry of Hajj and Umrah in KSA have announced that this year due to COVID-19, limited number of pilgrims will be able to perform Hajj. -

ATFM TF/3 & FWC2022 TF/3 International Civil Aviation

ATFM TF/3 & FWC2022 TF/3 International Civil Aviation Organization MIDANPIRG Air Traffic Flow Management Task Force and MIDANPIRG FIFA World Cup 2022 Task Force Third Meetings (ATFM TF/3 & FWC2022 TF/3) (Amman, Jordan, 12 – 14 January 2020) LSIT OF PARTICIPANTS 13 January 2020 NAME TITLE STATES BAHRAIN Mr. Abdulla Hassan Al Qadhi Chief Aeronautical Information Management & Airspace Planning Bahrain Civil Aviation Affairs P.O. Box 586 Manama - KINGDOM OF BAHRAIN Mr. Rashid Saleh Joben Chief Standards, Licensing & Development Bahrain Civil Aviation Affairs P.O. Box 586 Manama - KINGDOM OF BAHRAIN EGYPT Mr. Amr Ibrahim Abdel Latiff Ibrahim ATS Inspector Egyptian Civil Aviation Authority (ECAA) Cairo Airport Road Cairo - EGYPT INDIA Mr. Hasrat Ali Khan Assistant Manager (ATM-ATFM) CHQ, Airports Authority of India Rajiv Gandhi Bhawan, Safdarjung Airport New Delhi – 110003 - INDIA Mr. Jiji Punamadathu Alex Executive Director (Air Traffic Flow Management) CHQ, Airports Authority of India Rajiv Gandhi Bhawan, Safdarjung Airport New Delhi – 110003 - INDIA - 2 - NAME TITLE Mr. Manjunath K. Nelli Joint General Manager (ATM) CHQ, Airports Authority of India Rajiv Gandhi Bhawan, Safdarjung Airport New Delhi – 110003 - INDIA IRAQ Mr. Ammar Ahmed Taqi Flow Management Officer General Company for Air Navigation Services (GCANS) Baghdad Airport 10020 Baghdad - IRAQ Mr. Cucu dan Operations Manager General Company for Air Navigation Services (GCANS) Ms. Daniah Hashim Hasan ATFM Unit Manager General Company for Air Navigation Services (GCANS) Baghdad Airport 10020 Baghdad - IRAQ Mr. Erwin Obergruber MBA General Company for Air Navigation Services (GCANS) Al-Burhan Center, Baghdad Airport 10023 Baghdad - IRAQ Mr. Mahmood Hashim Muttashar Operations Manager General Company for Air Navigation Services (GCANS) Baghdad Airport 10020 Baghdad - IRAQ JORDAN Mr.