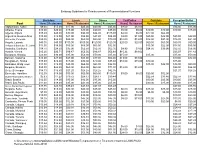

Quarterly Forecast

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bali E Singapore

[email protected] /www.anywhereviaggi.it ANYWHERE VIAGGI SRL VIA ROMA 47 10025 PINO TORINESE TEL.011-840528/840582 KUALA LUMPUR + REDANG DAL 08 AL 23 AGOSTO 2020 01 GIORNO 08/08/2020 MALPENSA/ MUSCAT Orario consigliato di arrivo all’aeroporto di MALPENSA alle ore 19.05 al banco OMAN AIR per le operazioni d’imbarco. Ore 22.05 partenza con volo WY144 per MUSCAT. 02 GIORNO 09/08/2020 MUSCAT/ KUALA LUMPUR Arrivo a MUSCAT alle ore 06.40. Coincidenza con volo WY823 delle ore 09.05 per KUALA LUMPUR. Arrivo a Kuala Lumpur alle ore 20.10. Trasferimento con incaricato presso LE APPLE BOUTIQUE HOTEL KLCC 4**** o similare, in pernottamento e prima colazione. 03-04 GIORNO 10-11/08/2020 KUALA LUMPUR Prima colazione. Giornata a disposizione per la visita libera della città. Cena libera. Pernottamento a Kuala Lumpur. 05 GIORNO 12/08/2020 (colazione) KUALA LUMPUR /KUALA TERRENGANU /REDANG Prima colazione, trasferimento con incaricato in aeroporto e decollo con volo MH delle ore 10.05 per KUALA TERRENGANU con arrivo alle ore 11.10. Da qui trasferimento con incaricato al porto di SHABANDAR. Traghetto per REDANG e sistemazione presso CORAL REDANG ISLAND RESORT, camera standard in pensione completa. DAL 06 AL 14 GIORNO DAL 13 AL 21/08/2020 REDANG Pensione completa al resort. Giornate libere da dedicare ad attività balneari o a visite ed escursioni facoltative. 15 GIORNO 22/08/2020 REDANG /KUALA TERRENGANU /KUALA LUMPUR /MUSCAT Prima colazione e rilascio della camera entro ore 12.00. Partenza con traghetto per SHAHBANDAR. Arrivo e trasferimento con incaricato all’aeroporto di KUALA TERENGGANU. -

Muscat Escape “Transfer Through Muscat to Shangri La..”

OMAN Muscat Escape “Transfer through Muscat to Shangri La..” When you arrive into Muscat Airport, head through immigration, baggage collection and Customs and proceed to the arrivals hall where you will be met by your driver. You are privately chauffeured to the Shangri La Bar Al jissah resort in Muscat. You will be collected on your return back to Muscat Airport up to 3 hours prior to your departure flight. Jumeirah Mosque “Home of the Founding Father – Abu Dhabi City Tour” 09:00 – 16:00 Tour - From Muscat we drive towards Quariyat and then along the coast towards Sur Our first stop is at the Bimmah sinkhole, here you can sit with your feet in the water and have the little fish eat away at all those nasty bits. Not for the Ticklish! We have time to swim and jump of the rocks on the other side Further along the coast just before the quaint village of Tiwi is Wadi Shab. This is still a very beautiful Wadi but it was devastated when a cyclone called Gonu hit in 2007 and its beauty was not enhanced by the construction of a road bridge across the entrance. It is about an hour’s walk to the Swimming Pools but be sure to have some decent trekking shoes in fact two pairs of shoes are advisable one for trekking and the other for swimming and a bit of rock climbing. Bring some water (particularly in summer) and do not bring any valuables unless you have a waterproof case 17:00 – 19:00 Sunset Dhow Cruise - leave the Marina Bandar al Rowdha and cruise along the coast taking in the views of Muscat Harbour the sultan’s Palace and the Forts of Al Jalali and Al Mirani. -

Prometric Combined Site List

Prometric Combined Site List Site Name City State ZipCode Country BUENOS AIRES ARGENTINA LAB.1 Buenos Aires ARGENTINA 1006 ARGENTINA YEREVAN, ARMENIA YEREVAN ARMENIA 0019 ARMENIA Parkus Technologies PTY LTD Parramatta New South Wales 2150 Australia SYDNEY, AUSTRALIA Sydney NEW SOUTH WALES 2000 NSW AUSTRALIA MELBOURNE, AUSTRALIA Melbourne VICTORIA 3000 VIC AUSTRALIA PERTH, AUSTRALIA PERTH WESTERN AUSTRALIA 6155 WA AUSTRALIA VIENNA, AUSTRIA Vienna AUSTRIA A-1180 AUSTRIA MANAMA, BAHRAIN Manama BAHRAIN 319 BAHRAIN DHAKA, BANGLADESH #8815 DHAKA BANGLADESH 1213 BANGLADESH BRUSSELS, BELGIUM BRUSSELS BELGIUM 1210 BELGIUM Bermuda College Paget Bermuda PG04 Bermuda La Paz - Universidad Real La Paz BOLIVIA BOLIVIA GABORONE, BOTSWANA GABORONE BOTSWANA 0000 BOTSWANA Physique Tranformations Gaborone Southeast 0 Botswana BRASILIA, BRAZIL Brasilia DISTRITO FEDERAL 70673-150 BRAZIL BELO HORIZONTE, BRAZIL Belo Horizonte MINAS GERAIS 31140-540 BRAZIL BELO HORIZONTE, BRAZIL Belo Horizonte MINAS GERAIS 30160-011 BRAZIL CURITIBA, BRAZIL Curitiba PARANA 80060-205 BRAZIL RECIFE, BRAZIL Recife PERNAMBUCO 52020-220 BRAZIL RIO DE JANEIRO, BRAZIL Rio de Janeiro RIO DE JANEIRO 22050-001 BRAZIL SAO PAULO, BRAZIL Sao Paulo SAO PAULO 05690-000 BRAZIL SOFIA LAB 1, BULGARIA SOFIA BULGARIA 1000 SOFIA BULGARIA Bow Valley College Calgary ALBERTA T2G 0G5 Canada Calgary - MacLeod Trail S Calgary ALBERTA T2H0M2 CANADA SAIT Testing Centre Calgary ALBERTA T2M 0L4 Canada Edmonton AB Edmonton ALBERTA T5T 2E3 CANADA NorQuest College Edmonton ALBERTA T5J 1L6 Canada Vancouver Island University Nanaimo BRITISH COLUMBIA V9R 5S5 Canada Vancouver - Melville St. Vancouver BRITISH COLUMBIA V6E 3W1 CANADA Winnipeg - Henderson Highway Winnipeg MANITOBA R2G 3Z7 CANADA Academy of Learning - Winnipeg North Winnipeg MB R2W 5J5 Canada Memorial University of Newfoundland St. -

ORANGE MUSCAT Hartwick Vineyard — Mokelumne River

MARCH 2020 | VOLUME 15 | ISSUE 3 MARCH WINE OF THE MONTH ORANGE MUSCAT Hartwick Vineyard — Mokelumne River Orange Muscat has an evocative name that hints not at the wine’s color or flavor, but at bright and refreshing citrus aromatics. SMALL LOT ALL ABOUT CULTIVATION AROMATICS While plantings of Orange Muscat are rela- Mokelumne River boasts a Mediterranean cli- tively small, parts of California are known for mate with hot, sunny days mitigated by nights prominent cultivation. This balanced, off-dry influenced by the Sacramento–San Joaquin white wine originates from the meticulously River Delta, which brings cool Pacific Ocean maintained Hartwick Vineyard in the Moke- air from the San Francisco Bay. This environ- lumne River growing area, a sub-appellation ment results in outstanding development of of Lodi which lies northeast of San Francisco. plush flavors and out-of-this-world aromat- This vineyard was planted in the 1990s and ics, which you’ll experience when you put your sits near a beautifully shaded river area, an en- nose in the glass and breathe the intensity of chanting growing site. orange blossoms, lemon, and lime candy. The spot is known for its distinctive sandy A sip of this wine is rich and just-a-touch loam soil, which promotes deep roots and fruit sweet, with a long finish packed with florals concentration. It’s perfect for Orange Muscat, and Granny Smith apple. The viscous mouth- a relatively obscure grape that is a cross be- feel makes Orange Muscat a unique treat to tween Muscat Blanc à Petits Grains (one of savor with a plate of mild cheeses. -

Manama Connects Issue No

THE E-NEWSLETTER OF THE EMBASSY OF MALAYSIA IN BAHRAIN MANAMA CONNECTS ISSUE NO. 14 – APRIL TO JUNE 2020 MALAWAKIL MANAMA EID-UL-FITR 1441/2020 CELEBRATION Muslims around the world celebrated Eid-ul Fitr this year in a new normal including us in Manama, Kingdom of Bahrain. However, the celebration of Eid-ul Fitr on 24 May 2020 at Malaysia House was still full of happiness with lots of delicious special Raya dishes enjoyed by Embassy’s staff and families only. It started with photo session, brunch and ended with takbir led by Ambassador Agus Salim bin Yusof. Prior to that, the Ambassador sent his Eid-ul Fitr message by email to all Malaysian Muslims in Bahrain. On 28 May 2020, the fifth day of Syawal, the Embassy of Malaysia celebrated the Eid-ul Fitr with the Embassy’s staff. Colorful Malaysian traditional wear of batik, songket and baju melayu were worn by all officers and staff. The gathering was also to celebrate birthdays of staff who were born in the month of May and June. [TypeMANAMA here] CONNECTS [Type here] ISSUE 14: APRIL – JUNE[Type 2020 here] Courtesy Visit by New Ambassador Courtesy Visit by New Ambassador of Bangladesh to the Kingdom of of the Republic of Korea to the Bahrain Kingdom of Bahrain On 11 June 2020, Ambassador Agus Salim bin On 25 June 2020, Ambassador Agus Salim bin Yusof received in the Embassy, His Excellency Yusof received His Excellency Chung Hae Muhammad Nazrul Islam, Ambassador of Kwan, Ambassador of the Republic of Korea to Bangladesh to the Kingdom of Bahrain. -

Manama, Capital of Bahrain (Population: 1.4 Million) Dubai

FMM-SMF Joint Business Mission Bahrain & United Arab Emirates November 24-30, 2018 (Up to 50% FUNDING under Malaysia-Singapore Third Country Business Development Fund for two (2) representatives from each company ) Manama, Capital of Bahrain (Population: 1.4 million) Malaysia has been exporting halal products such as agricultural produce, batik, ceramics, clothing, cosmetics, frozen foods and wood products to Bahrain In 2017, Bahrain imported from Malaysia RM456 million worth of products including wood products (mainly sawn wood, wood fiberboard, and plywood), foodstuff and glazed ceramics Although a small island-nation, Bahrain’s geostrategic location and strong ties with Saudi Arabia . and other G.C.C. members position it as a “gateway to the Gulf” and the wider Arab world Dubai, Capital of United Arab Emirates (Population: 9.54 million) Dubai is the trading hub of the Middle East, Asia and Africa UAE is one of the top export destination in the West Asia region for Malaysia Malaysia exported RM12 billion worth of products and services to UAE including palm oil & palm oil-based products, E&E products, jewellery, metal, machinery and equipment Other products with potential market in UAE are food & beverages, furniture, building materials, telecommunication equipment, construction & related services, healthcare, ICT related services. Mission Highlights Visit to BIG 5, the largest building construction show in the Middle East Business matching meetings arranged by MATRADE, Bahrain Chamber of Commerce & Industry and Dubai Chamber -

CIS 2018 Middle East Tour Summary

CIS 2018 Middle East Tour Summary Tour Director: Molly Witt, University of Vermont Assistant Tour Director: Jordan England, University of California, Davis TOUR OVERVIEW • Available to institutions from all regions • Visits 6 countries total (Jordan, Egypt, Qatar, Bahrain, Oman, UAE) • Ends with an optional add-on in Beirut, Lebanon • Includes visits to a diverse group of local and international schools • Ample networking opportunities CITIES & SCHOOLS VISITED CITY DAYS SCHOOL(S) VISITED STUDENTS MET Dubai, UAE 4 • GEMS Dubai American Academy 340 • American School of Dubai • GEMS World Academy • Al-Mizhar American Academy • Al Mawakeb School • Universal American School Abu Dhabi, 1 • American Community School of Abu Dhabi 30 UAE Muscat, Oman 1 • Muscat International School 370 • The American International School of Muscat (TAISM) • American British Academy Doha, Qatar 1 • American School of Doha 190 • ACS Doha International School • Doha British School Manama, 1 • Bahrain Bayan School 185 Bahrain • Naseem International School • British School of Bahrain Amman, 2 • American Community School 469 Jordan • Amman Academy • Amman Baccalaureate School • King’s Academy • Modern American School • Mashrek International School • Modern Montessori School • The International Academy - Amman Cairo, Egypt 2 • El Alsson 510 • American International School – West • Cairo American College • Hayah International School • Modern English School Cairo • American International School - East Beirut, 2 • College Notre Dame de Jamhour 395 Lebanon • Wellspring Learning -

Reservations Contact Detail

Reservations Contact Detail Name Richard Vangunster Position Assistant Revenue Manager Telephone +973-663-16666 Fax +973-663-16667 Email [email protected] & [email protected] 1. Cash, or other guaranteed form of payment 2. Credit card (We accept all major credit cards) 3. Electronic Funds Transfer to following hotel account Building 65, Road 4003, Block 340, Juffair, Kingdom of Bahrain Tel: +973-663-16666 Fax: +973-160-00098 wyndhamgardenmanama.com THE HARD FACTS MADE EASY Everything you need to know about your Wyndham Garden Manama JASHAN CAFE MOSAIC TRATTORIA DINING AND ENTERTAINMENT GETTING THERE Wyndham Garden Manama features world-class speciality dining and Directions from Bahrain International Airport entertainment options, that’s sure to deliver the finest experience in Distance: 10 Minutes the very heart of the city. Directions: Exit from Airport at the first roundabout, take road No. 2403 • Jashan - Savour the authentic taste of Indian cuisine with a wide to Arad highway and drive towards Khalifa Al Khabeer highway going variety of traditional Indian recipes reflecting the diversity towards Muharraq. Take Shaikh Hamad Causeway that goes towards of India. Manama. Enter left at Al Fateh highway and drive for 3 kms. Enter left • Café Mosaic - This international all day dining outlet is perfect again into Awal Avenue. At Al Fateh Grand Mosque signal, take the first for a business lunch or relaxed dining with friends and family. The right toward Shabab Avenue, then take right again at the end of Shabab restaurant offers a wide selection of delightful dishes prepared at live cooking stations. Avenue; followed by the second left on Road 4005. -

Embassy Guidelines for Reimbursement of Representational Functions

Embassy Guidelines for Reimbursement of Representational Functions Breakfast Lunch Dinner Tea/Coffee Cocktails Reception/Buffet Post Home Restaurant Home Restaurant Home Restaurant Home Restaurant Home Restaurant Home Restaurant Afghanistan, Kabul $9.00 $15.00 $17.00 $25.00 $20.00 $35.00 $8.00 $12.00 $14.00 $15.00 Albania, Tirana $10.00 $20.00 $15.00 $30.00 $20.00 $35.00 $5.00 $5.00 $10.00 $10.00 $10.00 $15.00 Algeria, Algiers $18.00 $40.00 $30.00 $90.00 $44.00 $125.00 $4.00 $6.00 $22.00 $64.00 Argentina, Buenos Aires $15.00 $18.50 $47.00 $54.00 $47.00 $54.00 $8.00 $11.00 $25.00 $42.00 $25.00 $42.00 Armenia, Yerevan $20.00 $22.00 $25.00 $60.00 $40.00 $70.00 $10.00 $12.00 $16.00 $21.00 $16.00 $21.00 Angola, Luanda $40.00 $40.00 $100.00 $100.00 $120.00 $120.00 $20.00 $20.00 $60.00 $60.00 $60.00 $50.00 Antigua & Barduda, St. Johns $11.00 $18.00 $45.00 $66.00 $63.00 $92.00 $15.00 $22.00 $34.00 $45.00 Australia, Canberra $14.70 $24.50 $35.00 $52.50 $52.50 $62.30 $4.90 $7.00 $24.50 $39.90 $52.50 $56.00 Austria, Vienna $15.26 $20.71 $46.87 $56.56 $46.87 $56.68 $15.26 $19.62 $25.07 $41.42 Bahamas, Nassau $20.00 $30.00 $35.00 $50.00 $70.00 $85.00 $15.00 $15.00 $15.00 $50.00 Bahrain, Manama $13.00 $27.00 $27.00 $53.00 $37.00 $66.00 $13.00 $19.00 $19.00 $32.00 Bangladesh, Dhaka $15.00 $20.00 $15.00 $30.00 $20.00 $35.00 $10.00 $15.00 $10.00 $15.00 Barbados, Bridgetown $11.00 $18.00 $45.00 $66.00 $63.00 $92.00 $15.00 $22.00 $34.00 $50.00 Belguim, Brussels $28.00 $28.00 $60.00 $60.00 $60.00 $71.00 $12.00 $12.00 $24.00 $24.00 Belize,Belmopan $14.10 -

4.617: Balancing Globalism and Regionalism: the Heart of Doha Project

SPRING 2009 DEPARTMENT OF ARCHITECTURE 4.617: Balancing Globalism and Regionalism: The Heart of Doha Project Instructor: Nasser Rabbat Prerequisite: Permission of Instructor Wednesday from 2 to 5 in Room 5-216 Prerequisite: Permission of instructor Submit two paragraph statement of intent to Nasser Rabbat, via email <[email protected]>, by Jan. 20th. Enrollment limited to 10 In the last two decades, the Arabian Gulf experienced an extraordinary urban boom fueled by a global economy looking for new, profitable outlets and an accumulated oil wealth seeking easy and safe invest- ments at home. The combined capital found its ideal prospect in developing gargantuan business parks and malls, luxury housing and hotels, and touristic, cultural, and entertainment complexes. Architecture at once assumed the role of branding instrument and spectacular wrapping for these new lavish enterprises, which swiftly sprang up in cities like Dubai, Doha, Abu Dhabi, Sharjah, Manama, Riyadh, and Kuwait. Yet, not all recent architecture in the Gulf readily fits what Joseph Rykwert matter-of-factly calls the “Emirate Style,” a style whose extravagant flights of fancy seem to depend only on the unbridled imagination of the designers and the willingness of their patrons to bankroll those fantasies. Various large-scale projects are trying to reverse the trend by judiciously using the vast financial resources available to produce quality design that tackles some of the most urgent social, cultural, and environmental issues facing those countries today. These urban and architectural experiments, like Masdar City in Abu Dhabi, the Heart of Doha in Qatar, and KAUST Campus in Jeddah, Saudi Arabia, hailed as design tours de force, have yet to be studied from a his- torical and sociocultural perspective. -

Coronavirus - BEY/MCT/AUH Customer Guidelines

Coronavirus - BEY/MCT/AUH Customer Guidelines Answer Id 8170 | Updated 26/03/2020 01.08 PM (GMT) Summary The following guidelines have been published to assist any customer affected by the Coronavirus cancellations for Beirut (BEY), Muscat (MCT) and Abu Dhabi (AUH). More information You do not need to add any keywords or endorsements unless they have been mentioned below. Advice for British Airways-125 ticketed customers whose BA flight is now CANCELLED Rebook onto British Airways Airports affected To/From BEY (Beirut) MCT (Muscat) AUH (Abu Dhabi) Tickets issued by 18 March 2020 Ticket travel dates Up to and including 30 April 2020 Rebooking Allowance Use all options from standard customer guidelines and Principal Coronovirus guideline – Update 1 Rebooking Allowance for BEY orRebook onto Qatar Airlines (QR) between Beirut (BEY)/Muscat MCT (MCT) and Doha (DOH) or v.v. between 29 March and 30 April 2020 Rebook into the lowest available class in the same cabin Must add OS QR INVOL REROUTE DUE BA CANX PER BA/QR AGREEMENT Add OS QR customer contact number Use the lowest class available Only available on QR services BEY-DOH-BEY or MCT-DOH-MCT No Redemptions Then book a connecting BA or QR operating service between DOH and LHR v.v. Rebook into the same class as original or the lowest available class in the same cabin Rebooking Allowance for AUH Rebook onto Etihad Airways (EY) between Abu Dhabi (AUH) and London (LHR) or v.v. between 01 and 30 April 2020 Rebook into the lowest available from the following booking classes First – R/A/F Business -

Oman - Today’S Spotlight, Tomorrow’S Destination

Oman - Today’s Spotlight, Tomorrow’s Destination Hala Matar Choufany, Consulting & Valuation Analyst Elie Younes, Associate Director HVS INTERNATIONAL LONDON 14 Hallam Street London, W1W 6JG +44 20 7878-7738 +44 20 7436-3386 (Fax) June 2005 New York San Francisco Boulder Denver Miami Dallas Chicago Washington, D.C. Weston, CT Phoenix Mt. Lakes, NJ Vancouver Toronto London Madrid New Delhi Singapore Hong Kong Sydney São Paulo Buenos Aires Newport, RI HVS International Oman – Today’s Spotlight, Tomorrow’s Destination 1 Oman – Today’s Spotlight, Tomorrow’s Destination By Hala Matar Choufany and Elie Younes, HVS International Many industry colleagues consider the Middle East hotel markets, and notably the GCC region, to have similar characteristics and dynamics; but is this really the case? While most GCC markets are similar in terms of their oil-based economies, and the insignificant quantity of natural resources that would support and stimulate a large amount of international leisure visitation, some destinations are just different. In spring 2005, we visited Oman to advise on the multibillion dollar Blue City development near Muscat. What we saw on our trip confirmed our views. The Middle East is once again proving to be resilient to the international and regional shocks affecting tourism worldwide. Destinations like Bahrain, Doha, Dubai and Egypt have recently achieved record levels of visitation and Oman seems to be following a similar trend. In this article, we shed some light on Oman, a newly emerging market with significant opportunities at all levels. The reader should note that we have paid most attention to Muscat, the Omani capital, in our assessment and analysis.