Property Valuation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Landscape Analysis of Geographical Names in Hubei Province, China

Entropy 2014, 16, 6313-6337; doi:10.3390/e16126313 OPEN ACCESS entropy ISSN 1099-4300 www.mdpi.com/journal/entropy Article Landscape Analysis of Geographical Names in Hubei Province, China Xixi Chen 1, Tao Hu 1, Fu Ren 1,2,*, Deng Chen 1, Lan Li 1 and Nan Gao 1 1 School of Resource and Environment Science, Wuhan University, Luoyu Road 129, Wuhan 430079, China; E-Mails: [email protected] (X.C.); [email protected] (T.H.); [email protected] (D.C.); [email protected] (L.L.); [email protected] (N.G.) 2 Key Laboratory of Geographical Information System, Ministry of Education, Wuhan University, Luoyu Road 129, Wuhan 430079, China * Author to whom correspondence should be addressed; E-Mail: [email protected]; Tel: +86-27-87664557; Fax: +86-27-68778893. External Editor: Hwa-Lung Yu Received: 20 July 2014; in revised form: 31 October 2014 / Accepted: 26 November 2014 / Published: 1 December 2014 Abstract: Hubei Province is the hub of communications in central China, which directly determines its strategic position in the country’s development. Additionally, Hubei Province is well-known for its diverse landforms, including mountains, hills, mounds and plains. This area is called “The Province of Thousand Lakes” due to the abundance of water resources. Geographical names are exclusive names given to physical or anthropogenic geographic entities at specific spatial locations and are important signs by which humans understand natural and human activities. In this study, geographic information systems (GIS) technology is adopted to establish a geodatabase of geographical names with particular characteristics in Hubei Province and extract certain geomorphologic and environmental factors. -

Download Article

Advances in Economics, Business and Management Research, volume 70 International Conference on Economy, Management and Entrepreneurship(ICOEME 2018) Research on the Path of Deep Fusion and Integration Development of Wuhan and Ezhou Lijiang Zhao Chengxiu Teng School of Public Administration School of Public Administration Zhongnan University of Economics and Law Zhongnan University of Economics and Law Wuhan, China 430073 Wuhan, China 430073 Abstract—The integration development of Wuhan and urban integration of Wuhan and Hubei, rely on and Ezhou is a strategic task in Hubei Province. It is of great undertake Wuhan. Ezhou City takes the initiative to revise significance to enhance the primacy of provincial capital, form the overall urban and rural plan. Ezhou’s transportation a new pattern of productivity allocation, drive the development infrastructure is connected to the traffic artery of Wuhan in of provincial economy and upgrade the competitiveness of an all-around and three-dimensional way. At present, there provincial-level administrative regions. This paper discusses are 3 interconnected expressways including Shanghai- the path of deep integration development of Wuhan and Ezhou Chengdu expressway, Wuhan-Ezhou expressway and from the aspects of history, geography, politics and economy, Wugang expressway. In terms of market access, Wuhan East and puts forward some suggestions on relevant management Lake Development Zone and Ezhou Gedian Development principles and policies. Zone try out market access cooperation, and enterprises Keywords—urban regional cooperation; integration registered in Ezhou can be named with “Wuhan”. development; path III. THE SPACE FOR IMPROVEMENT IN THE INTEGRATION I. INTRODUCTION DEVELOPMENT OF WUHAN AND EZHOU Exploring the path of leapfrog development in inland The degree of integration development of Wuhan and areas is a common issue for the vast areas (that is to say, 500 Ezhou is lower than that of central urban area of Wuhan, and kilometers from the coastline) of China’s hinterland. -

A Simple Model to Assess Wuhan Lock-Down Effect and Region Efforts

A simple model to assess Wuhan lock-down effect and region efforts during COVID-19 epidemic in China Mainland Zheming Yuan#, Yi Xiao#, Zhijun Dai, Jianjun Huang & Yuan Chen* Hunan Engineering & Technology Research Centre for Agricultural Big Data Analysis & Decision-making, Hunan Agricultural University, Changsha, Hunan, 410128, China. #These authors contributed equally to this work. * Correspondence and requests for materials should be addressed to Y.C. (email: [email protected]) (Submitted: 29 February 2020 – Published online: 2 March 2020) DISCLAIMER This paper was submitted to the Bulletin of the World Health Organization and was posted to the COVID-19 open site, according to the protocol for public health emergencies for international concern as described in Vasee Moorthy et al. (http://dx.doi.org/10.2471/BLT.20.251561). The information herein is available for unrestricted use, distribution and reproduction in any medium, provided that the original work is properly cited as indicated by the Creative Commons Attribution 3.0 Intergovernmental Organizations licence (CC BY IGO 3.0). RECOMMENDED CITATION Yuan Z, Xiao Y, Dai Z, Huang J & Chen Y. A simple model to assess Wuhan lock-down effect and region efforts during COVID-19 epidemic in China Mainland [Preprint]. Bull World Health Organ. E-pub: 02 March 2020. doi: http://dx.doi.org/10.2471/BLT.20.254045 Abstract: Since COVID-19 emerged in early December, 2019 in Wuhan and swept across China Mainland, a series of large-scale public health interventions, especially Wuhan lock-down combined with nationwide traffic restrictions and Stay At Home Movement, have been taken by the government to control the epidemic. -

The Development Value and Utilization Strategy of the Local Culture Education Resources in Hubei Prov

International Conference on Management, Computer and Education Informatization (MCEI 2015) The Development Value and Utilization Strategy of the Local Culture Education Resources In Hubei Prov Yanli Wang Abstract—Hubei Province is one of the birthplaces of Chinese course is rich in Hubei region culture style, light Chinese civilization, it has a number of distinctive local and blooming of national culture. characteristics of local culture. The culture does not only show the Chinese language literature in bright light, but also II. LOCAL CULTURE EDUCATION IDEA AND BASIS contains a great spirit of the Chinese nation. College course China has a vast territory, and has formed a unique of China plays an important role in mother tongue cultural resources in the long-term historical and cultural education, quality education, which undertakes the task of development. Local culture refers to the culture which is humanistic education, teaching, the establishment of composed of different groups of people. It is a cultural “Chinese language” concept, Hubei local folk culture, environment that individual or group in the course of regional culture and education resources of local culture by development can influence the formation of its perception, combing the integration after the introduction of the thinking, value and so on. The modern education theory language classroom, the effective development and holds that the cultural resources are the necessary utilization value of Hubei local education cultural resources conditions for the education. In some areas of local culture in University Chinese teaching. Strategy research and providing specific historical background and living space utilization of resources of Chinese native culture develops at for human, often with an invisible force constraints the the University of education value. -

Mapping the Accessibility of Medical Facilities of Wuhan During the COVID-19 Pandemic

International Journal of Geo-Information Article Mapping the Accessibility of Medical Facilities of Wuhan during the COVID-19 Pandemic Zhenqi Zhou 1, Zhen Xu 1,* , Anqi Liu 1, Shuang Zhou 1, Lan Mu 2 and Xuan Zhang 2 1 Department of Landscape Architecture, College of Landscape Architecture, Nanjing Forestry University, Nanjing 210037, China; [email protected] (Z.Z.); [email protected] (A.L.); [email protected] (S.Z.) 2 Department of Geography, University of Georgia, Athens, GA 30602, USA; [email protected] (L.M.); [email protected] (X.Z.) * Correspondence: [email protected] Abstract: In December 2019, the coronavirus disease 2019 (COVID-19) pandemic attacked Wuhan, China. The city government soon strictly locked down the city, implemented a hierarchical diagnosis and treatment system, and took a series of unprecedented pharmaceutical and non-pharmaceutical measures. The residents’ access to the medical resources and the consequently potential demand– supply tension may determine effective diagnosis and treatment, for which travel distance and time are key indicators. Using the Application Programming Interface (API) of Baidu Map, we estimated the travel distance and time from communities to the medical facilities capable of treating COVID-19 patients, and we identified the service areas of those facilities as well. The results showed significant differences in service areas and potential loading across medical facilities. The accessibility of medical facilities in the peripheral areas was inferior to those in the central areas; there was spatial inequality of medical resources within and across districts; the amount of community healthcare Citation: Zhou, Z.; Xu, Z.; Liu, A.; Zhou, S.; Mu, L.; Zhang, X. -

Present Status, Driving Forces and Pattern Optimization of Territory in Hubei Province, China Tingke Wu, Man Yuan

World Academy of Science, Engineering and Technology International Journal of Environmental and Ecological Engineering Vol:13, No:5, 2019 Present Status, Driving Forces and Pattern Optimization of Territory in Hubei Province, China Tingke Wu, Man Yuan market failure [4]. In fact, spatial planning system of China is Abstract—“National Territorial Planning (2016-2030)” was not perfect. It is a crucial problem that land resources have been issued by the State Council of China in 2017. As an important unordered and decentralized developed and overexploited so initiative of putting it into effect, territorial planning at provincial level that ecological space and agricultural space are seriously makes overall arrangement of territorial development, resources and squeezed. In this regard, territorial planning makes crucial environment protection, comprehensive renovation and security system construction. Hubei province, as the pivot of the “Rise of attempt to realize the "Multi-Plan Integration" mode and Central China” national strategy, is now confronted with great contributes to spatial planning system reform. It is also opportunities and challenges in territorial development, protection, conducive to improving land use regulation and enhancing and renovation. Territorial spatial pattern experiences long time territorial spatial governance ability. evolution, influenced by multiple internal and external driving forces. Territorial spatial pattern is the result of land use conversion It is not clear what are the main causes of its formation and what are for a long period. Land use change, as the significant effective ways of optimizing it. By analyzing land use data in 2016, this paper reveals present status of territory in Hubei. Combined with manifestation of human activities’ impact on natural economic and social data and construction information, driving forces ecosystems, has always been a specific field of global climate of territorial spatial pattern are then analyzed. -

Chinacoalchem

ChinaCoalChem Monthly Report Issue May. 2019 Copyright 2019 All Rights Reserved. ChinaCoalChem Issue May. 2019 Table of Contents Insight China ................................................................................................................... 4 To analyze the competitive advantages of various material routes for fuel ethanol from six dimensions .............................................................................................................. 4 Could fuel ethanol meet the demand of 10MT in 2020? 6MTA total capacity is closely promoted ....................................................................................................................... 6 Development of China's polybutene industry ............................................................... 7 Policies & Markets ......................................................................................................... 9 Comprehensive Analysis of the Latest Policy Trends in Fuel Ethanol and Ethanol Gasoline ........................................................................................................................ 9 Companies & Projects ................................................................................................... 9 Baofeng Energy Succeeded in SEC A-Stock Listing ................................................... 9 BG Ordos Started Field Construction of 4bnm3/a SNG Project ................................ 10 Datang Duolun Project Created New Monthly Methanol Output Record in Apr ........ 10 Danhua to Acquire & -

Study on Intangible Cultural Heritage Brands from the Perspective Of

International Conference on Education Technology, Management and Humanities Science (ETMHS 2015) Study on Intangible Cultural Heritage Brands from the Perspective of Ecological Protection Haimeng Li School of music, Hubei Normal University, Huangshi, 435002, China Keywords: ecological protection, intangible cultural heritage, brands Abstract: China has abundant intangible cultural heritage resources. However, economic development brings pressure to ecological environment, changes of which have direct influence on the protection of intangible cultural heritage. At current stage, due to lack of strong consciousness of intangible cultural heritage protection in many regions in China, a part of intangible cultural heritage is in imminent danger. Establishment of intangible cultural heritage brands means inheritance and development of intangible cultural heritage, and is also a way of intangible cultural heritage protection. This paper mainly studies on intangible cultural heritage brands from the perspective of ecological protection with an example of protection of intangible cultural heritage in Southeastern Hubei Province. As intangible cultural heritage has tourism value, various countries begin to attach importance to tourism development of intangible cultural heritage. However, unreasonable development is caused for many factors, which cannot inherit or develop intangible cultural heritage but lead to frequent problems in its protection. Establishment of intangible cultural heritage brands is an important way of intangible cultural development -

Here You Can Taste Wuhan Featured Food

Contents Basic Mandarin Chinese Words and Phrases............................................... 2 Useful Sayings....................................................................................... 2 In Restaurants....................................................................................... 3 Numbers................................................................................................3 Dinning and cafes..........................................................................................5 Eating Out in Wuhan.............................................................................5 List of Restaurants and Food Streets (sort by distance).......................6 4 Places Where You Can Taste Wuhan Featured Food.........................7 Restaurants and cafes in Walking Distance........................................11 1 Basic Mandarin Chinese Words and Phrases Useful Sayings nǐ hǎo Hello 你 好 knee how zài jiàn Goodbye 再 见 zi gee’en xiè xiè Thank You 谢 谢! sheh sheh bú yòng le, xiè xiè No, thanks. 不 用 了,谢 谢 boo yong la, sheh sheh bú yòng xiè You are welcome. 不 用 谢 boo yong sheh wǒ jiào… My name is… 我 叫… wore jeow… shì Yes 是 shr bú shì No 不 是 boo shr hǎo Good 好 how bù hǎo Bad 不 好 boo how duì bù qǐ Excuse Me 对 不 起 dway boo chee wǒ tīng bù dǒng I do not understand 我 听 不 懂 wore ting boo dong duō shǎo qián How much? 多 少 钱? dor sheow chen Where is the xǐ shǒu jiān zài nǎ lǐ See-sow-jian zai na-lee washroom? 洗 手 间 在 哪 里 2 In Restaurants In China, many people call a male waiter as handsome guy and a female waitress as beautiful girl. It is also common to call “fú wù yuan” for waiters of both genders. cài dān Menu 菜 单 tsai dan shuài gē Waiter(Handsome) 帅 哥 shuai ge měi nǚ Waitress(Beautiful) 美 女 may nyu fú wù yuán Waiter/Waitress 服 务 员 fu woo yuan wǒ xiǎng yào zhè ge 我 I would like this. -

Are China's Water Resources for Agriculture Sustainable? Evidence from Hubei Province

sustainability Article Are China’s Water Resources for Agriculture Sustainable? Evidence from Hubei Province Hao Jin and Shuai Huang * School of Public Economics and Administration, Shanghai University of Finance and Economics, Shanghai 200433, China; [email protected] * Correspondence: [email protected]; Tel.: +86-21-65903686 Abstract: We assessed the sustainability of agricultural water resources in Hubei Province, a typical agricultural province in central China, for a decade (2008–2018). Since traditional evaluation models often consider only the distance between the evaluation point and the positive or negative ideal solution, we introduce gray correlation analysis and construct a new sustainability evaluation model. Our research results show that only one city had excellent sustainable development capacity of agricultural water resources, and the evaluation value of eight cities fluctuated by around 0.5 (the median of the evaluation result), while the sustainable development capacity of agricultural water resources in other cities was relatively poor. Our findings not only reflect the differences in the natural conditions of water resources among various cities in Hubei, but also the impact of the cities’ policies to ensure efficient agricultural water use for sustainable development. The indicators and methods Citation: Jin, H.; Huang, S. Are in this research are not difficult to obtain in most countries and regions of the world. Therefore, the China’s Water Resources for indicator system we have established by this research could be used to study the sustainability of Agriculture Sustainable? Evidence agricultural water resources in other countries, regions, or cities. from Hubei Province. Sustainability 2021, 13, 3510. https://doi.org/ Keywords: water resources; agricultural water resources; sustainability; gray correlation analysis; 10.3390/su13063510 evaluation model Academic Editors: Daniela Malcangio, Alan Cuthbertson, Juan 1. -

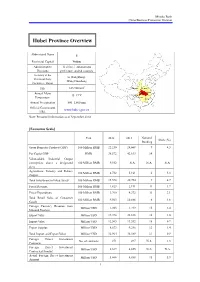

Hubei Province Overview

Mizuho Bank China Business Promotion Division Hubei Province Overview Abbreviated Name E Provincial Capital Wuhan Administrative 12 cities, 1 autonomous Divisions prefecture, and 64 counties Secretary of the Li Hongzhong; Provincial Party Wang Guosheng Committee; Mayor 2 Size 185,900 km Shaanxi Henan Annual Mean Hubei Anhui 15–17°C Chongqing Temperature Hunan Jiangxi Annual Precipitation 800–1,600 mm Official Government www.hubei.gov.cn URL Note: Personnel information as of September 2014 [Economic Scale] Unit 2012 2013 National Share (%) Ranking Gross Domestic Product (GDP) 100 Million RMB 22,250 24,668 9 4.3 Per Capita GDP RMB 38,572 42,613 14 - Value-added Industrial Output (enterprises above a designated 100 Million RMB 9,552 N.A. N.A. N.A. size) Agriculture, Forestry and Fishery 100 Million RMB 4,732 5,161 6 5.3 Output Total Investment in Fixed Assets 100 Million RMB 15,578 20,754 9 4.7 Fiscal Revenue 100 Million RMB 1,823 2,191 11 1.7 Fiscal Expenditure 100 Million RMB 3,760 4,372 11 3.1 Total Retail Sales of Consumer 100 Million RMB 9,563 10,886 6 4.6 Goods Foreign Currency Revenue from Million USD 1,203 1,219 15 2.4 Inbound Tourism Export Value Million USD 19,398 22,838 16 1.0 Import Value Million USD 12,565 13,552 18 0.7 Export Surplus Million USD 6,833 9,286 12 1.4 Total Import and Export Value Million USD 31,964 36,389 17 0.9 Foreign Direct Investment No. -

Xiaokun Li 李小坤 and Jianwei Lu 鲁剑巍

13th IPI-CAU-ISSAS International Symposium Soil K supplying capacity and crops responses to K fertilizer in rice-oilseed rape rotation system 稻-油轮作体系土壤供钾能力及作物对钾肥的响应 Xiaokun Li 李小坤 and Jianwei Lu 鲁剑巍 Huazhong Agricultural University 华中农业大学 Kunming, Nov. 7, 2019 Main producing area of rice Rice: one of the most important food crops in China Main production area: Northeast, Middle and lower reaches of the Yangtze River, Southwest, South China Main producing area of oilseed rape Oilseed rape: the largest oil crop in the planting area Main production area: Yangtze River Basin (YRB) Rice-oilseed rape rotation Yangtze River Basin Important role: Ensuring grain and edible oil security 1 Temporal changes of soil K supplying capacity 20-30 years ago, • K deficiency in rice and oilseed rape was very common in the Yangtze River basin • Why? Lower soil K supplying capacity YRB From 1990s to 2000s, average soil available K was changed from 71.5 to 84.3 mg L−1 and from 68.8 to 82.7 mg L−1, for SE and SW (YRB), respectively. (He, et al., 2015) Reason 1: crops harvest took away mass K Yielding two crops a year Rootzone 0-20cm 0-40cm 0-60cm Aboveground biomass 9525 kg/hm2 for oilseed rape; 16606 kg/hm2 for rice K uptakes 206 kg/hm2 for oilseed rape; 232 kg/hm2 for rice 朱芸等,植物营养与肥料学报,2019 Especially for Straw: moved away for another use • As fuel like firewood • As livestock feed, bed down the livestock (used for livestock) • Used for compost fertilizer... Reason 2: almost no K addition Rice Oilseed rape Rice percentage of <50 kg/ha: 55% Oilseed rape almost no K addition (张卫峰等,2018) Potash played an important role in rice-oilseed rape rotation system 20-30 years ago.