Philips Annual Report 2004 1 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

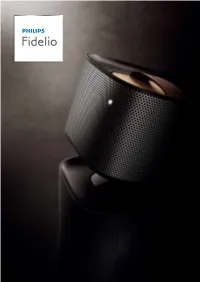

The Fidelio Wireless Hi-Fi Speaker Range Feature

Contents Obsessed with sound Philips sound heritage 05 Defining sound since the 1920s The radio goes global 06 A legend of the recording industry Obsessed with sound 08 The birth of portable audio 09 The CD revolution Pioneering connected audio 11 Fidelio heralds a new era Philips holds a special place within the world of Philips competencies audio. An admired innovator, Philips has defined 14 Fidelio sound 15 Golden Ears the standards of what we hear and how we 17 Design and acoustic engineering 18 Sound and acoustics innovation engineers experience it, bringing to consumers numerous 20 Product designers ground-breaking products such as portable Philips Fidelio 25 Headphones radio, compact cassette and recorder, compact M1BT S2 disc, and wireless Hi-Fi. With the launch of Philips 30 Portable speakers P9X premium Fidelio range, our obsession with sound 35 Docking speakers SoundSphere continues. Primo 40 Wireless Hi-Fi 44 Audio systems As we near a centenary in audio innovation, Sound towers 48 Home cinema sound we share our philosophy and introduce you E5 SoundSphere DesignLine to the people behind it. Join us on our sound SoundHub journey - Philips’ quest to improve and enhance The journey continues the listening experience of music lovers, offering them the most authentic sound possible: just as the artist intended. 2 3 Philips sound heritage Speech by Dutch Queen Wihelmina and Princess Juliana via a Philips short-wave Anton Philips, co-founder of Royal Philips N.V., with the one millionth radio set sold transmitter, 1927. in 1932. Defining sound since the 1920s The radio goes global For almost a century, Philips has pioneered audio innovations Philips’ next major innovation, introduced in 1927, was the that have transformed the way the world enjoys sound. -

Business-Driven IT Transformation at Royal Philips

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by AIS Electronic Library (AISeL) Business-Driven IT Transformation at Royal Philips Business-Driven IT Transformation at Royal Philips: Shedding Light on (Un)Rewarded Complexity Teaching Case Martin Mocker Eric van Heck MIT Erasmus University Center for Information Systems Rotterdam School of Management Research, and Burgemeester Oudlaan 50, Reutlingen University Rotterdam 3062PA, Netherlands ESB Business School [email protected] Alteburgstr. 150, 72762 Reutlingen Germany martin.mocker@reutlingen- university.de Abstract In 2013, Royal Philips was two years into a daunting transformation. Following declining financial performance, CEO Frans van Houten aimed to turn the Dutch icon into a “high-performing company” by 2017. This case study examines the challenges of the business-driven IT transformation at Royal Philips, a diversified technology company. The case discusses three crucial issues. First, the case reflects on Philips’ aim at creating value from combining locally relevant products and services while also leveraging its global scale and scope. Rewarded and unrewarded business complexity is analyzed. Second, the case identifies the need to design and align multiple elements of an enterprise (organizational, cultural, technical) to balance local responsiveness with global scale. Third, the case explains the role of IT (as an asset instead of a liability) in Philips’ transformation and discusses the new IT landscape with its digital platforms, and the new practices to create effective business-IT partnerships. Keywords: Organizational transformation, IS platform, enterprise architecture, IT governance, global business processes, process standards, agile software development Thirty Sixth International Conference on Information Systems, Fort Worth 2015 1 Business-Driven IT Transformation at Royal Philips Introduction In late 2013, Royal Philips was two years into a daunting transformation. -

Smart TV Sí Que Supone Un Gran Salto Tecnológico Importante

INSTITUTO POLITECNICO NACIONAL ESCUELA SUPERIOR DE COMERCIO Y ADMINISTRACIÓN SANTO TOMÁS SEMINARIO: “APLICACIONES DE LA PSICOLOGÍA AL TRABAJO EN MERCADOTECNIA EN FUNCIÓN DE TENDENCIAS GLOBALES DE COMPORTAMIENTO DEL CONSUMIDOR” TRABAJO FINAL “ESTRATEGIAS PARA LA CONSOLIDACION DE LA IMAGEN DE MARCA DE HISENSE S. DE R.L. DE C.V; EN EL MERCADO DE PANTALLAS EN MEXICO” QUE PARA OBTENER EL TÍTULO DE CONTADOR PÚBLICO PRESENTAN: FLORA CUEVAS CRUZ ROGELIO GARCES PANTALEON LICENCIADO EN RELACIONES COMERCIALES PRESENTAN: KAREN ARELI CABRERA ISLAS JORGE IGNACIO ESQUIVEL SOLIS JESSICA MERITH GARCIA ZÁRATE CONDUCTOR: LIC. MARÍA ELENA MORALES PEÑALOZA CIUDAD DE MÉXICO FEBRERO 2016 INSTITUTO POLITÉCNICO NACIONAL CARTA DE CESIÓN DE DERECHOS En la Cuidad de México, D.F., el día 15 del mes de Febrero del año 2016 los que suscriben: Flora Cuevas Cruz Rogelio Garcés Pantaleón Karen Areli Cabrera Islas Jorge Ignacio Esquivel Solís Jessica Merith García Zarate Pasantes de las(s) Licenciatura(s) 1. Contador Público 2. Relaciones Comerciales Manifiestan ser autores intelectuales del presente trabajo final, bajo la dirección de María Elena Morales Peñaloza y ceden los derechos totales del trabajo final Estrategias para la Consolidación de la Imagen de Marca de Hisense S. de R.L. de C.V. en el Mercado de Pantallas en México al Instituto Politécnico Nacional para su difusión con finales académicos y de investigación para ser consultado en texto completo en la Biblioteca Digital y en formato impreso en el Catalogo Colectivo del Sistema Institucional de Bibliotecas y Servicios de información de IPN. Los usuarios de la información no deben reproducir el contenido textual, graficas o datos del trabajo sin el permiso del autor y/o director del trabajo. -

Digital Pathology: the Dutch Perspective

Digital pathology: The Dutch perspective Paul J van Diest, MD, PhD Professor and Head, Department of Pathology University Medical Center Utrecht PO Box 85500, 3508 GA Utrecht The Netherlands [email protected] Professor of Oncology Johns Hopkins Oncology Center Baltimore, MD, USA Notice of Faculty Disclosure In accordance with ACCME guidelines, any individual in a position to influence and/or control the content of this ASCP CME activity has disclosed all relevant financial relationships within the past 12 months with commercial interests that provide products and/or services related to the content of this CME activity. The individual below has responded that he/she has no relevant financial relationship(s) with commercial interest(s) to disclose: Paul J. van Diest, MD, PhD Disclosures • member of advisory boards of Roche, Sectra, Philips (unpaid) • client of Hamamatsu, Sectra, Visiopharm, Leica, Aurora, Philips (paying heavily) • test scanners from Philips and Roche (no contract, no fee) • joint research projects with Philips UMCU Why The Netherlands? • “bunch-a-crazy dudes” • innovation is our middle name • not bound by too many rules and EU-FDA • strong believe in advantages in digital pathology Advantages of digital pathology • no more case assembly in the lab efficacy • quicker diagnostics efficacy • easy and more accurate measurements and counting patient safety/efficacy • better overview of tissue present patient safety • flagging missing slides patient safety • tracking viewing patient safety • automatic linking of images/reporting/LMS -

Nokia 3220 Phone at a Glance

UserGuide_test 1/26/04 1:04 PM Page 1 Thank you for purchasing your new Nokia phone. We’re here for you! www.nokiahowto.com Learn how to use your new Nokia phone. www.nokia.com/us Get answers to your questions. Register your phone’s limited warranty so we can better serve your needs! Nokia Inc. 7725 Woodland Center Boulevard, Suite 150, Tampa FL 33614 . Phone: 1.888.NOKIA.2U (1.888.665.4228) Fax: 1.813.249.9619 . Text Telephone/Telecommunication Device User Guide for the Deaf (TTY/TDD) Users: 1.800.24.NOKIA (1.800.246.6542) PRINTED IN CANADA Nokia 3220 phone at a glance Power key Earpiece Display screen Left Right selection key selection key Call key End key Scroll key Keypad Bottom of phone Back of phone Pop-Port Camera lens Charger port connector Microphone Nokia 3220 User Guide iCopyright © 2004 Nokia •QUICK GUIDE Action Description Make a call Enter a phone number, and press the Call key. Answer a call Press the Call key, or select Answer. Answer call during call Press the Call key. End a call Press the End key. Decline a call Press the End key to send the call to voice mail. Mute a call Select Mute during a call. Redial Press the Talk key twice. Adjust call volume Press the Scroll left and Scroll right keys during a call. Use in-call menu Select Options during a call. Save name and number Enter a number. Select Options > Save. Enter a name. Select OK. Use 1-touch dialing Press and hold a key (2–8). -

Royal Philips First Quarter 2016 Results Information Booklet

Royal Philips First Quarter 2016 Results Information booklet April 25th, 2016 1 Important information Forward-looking statements This document and the related oral presentation, including responses to questions following the presentation, contain certain forward-looking statements with respect to the financial condition, results of operations and business of Philips and certain of the plans and objectives of Philips with respect to these items. Examples of forward-looking statements include statements made about our strategy, estimates of sales growth, future EBITA and future developments in our organic business. By their nature, these statements involve risk and uncertainty because they relate to future events and circumstances and there are many factors that could cause actual results and developments to differ materially from those expressed or implied by these statements. These factors include, but are not limited to, domestic and global economic and business conditions, developments within the euro zone, the successful implementation of our strategy and our ability to realize the benefits of this strategy, our ability to develop and market new products, changes in legislation, legal claims, changes in exchange and interest rates, changes in tax rates, pension costs and actuarial assumptions, raw materials and employee costs, our ability to identify and complete successful acquisitions and to integrate those acquisitions into our business, our ability to successfully exit certain businesses or restructure our operations, the rate of technological changes, political, economic and other developments in countries where Philips operates, industry consolidation and competition. As a result, Philips’ actual future results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. -

a CCOEC 266 Amtners 26

USOO891848OB2 (12) United States Patent (10) Patent No.: US 8,918,480 B2 Qureshey et al. (45) Date of Patent: Dec. 23, 2014 (54) METHOD, SYSTEM, AND DEVICE FOR THE (56) References Cited DISTRIBUTION OF INTERNET RADO CONTENT U.S. PATENT DOCUMENTS (75) Inventors: Safi Qureshey, Santa Ana, CA (US); S3. A 's Stille Daniel D. Sheppard, Brea, CA (US) WW-1 (Continued) (73) Assignee: Black Hills Media, LLC, Wilmington, DE (US) FOREIGN PATENT DOCUMENTS (*) Notice: Subject to any disclaimer, the term of this E. 8:303 E; patent is extended or adjusted under 35 U.S.C. 154(b) by 847 days. (Continued) OTHER PUBLICATIONS (21) Appl. No.: 11/697,833 "A Music Revolution ... SoundServer” imerge, 2 pages. (22) Filed: Apr. 9, 2007 (Continued) (65) Prior Publication Data Primary Examiner — Duyen Doan (57) ABSTRACT US 2007/O18OO63 A1 Aug. 2, 2007 A network-enabled audio device that provides a display device that allows the user to select playlists of music much Related U.S. Application Data like a jukebox is disclosed. The user can compose playlists (63) Continuation of application No. 11/563,227, filed on from disk files, CD’s, Internet streaming audio broadcasts, Nov. 27, 2006 Pat. N s O45 953 hi hi online music sites, and other audio Sources. The user can also OV. Z. f. , now Fal. No. S.U4),932, Which 1S a select a desired Web broadcast from a list of available Web (Continued) broadcasts. In addition, the user can play standard audio CDs and MP3 encoded CD’s and have access to local AM/FM (51) Int. -

Corporate Restructuring in the Asian Electronics Market: Insights from Philips and Panasonic

Munich Personal RePEc Archive Corporate Restructuring in the Asian electronics market: Insights from Philips and Panasonic Reddy, Kotapati Srinivasa 2016 Online at https://mpra.ub.uni-muenchen.de/73663/ MPRA Paper No. 73663, posted 15 Sep 2016 10:39 UTC Corporate Restructuring in the Asian electronics market: Insights from Philips and Panasonic Kotapati Srinivasa Reddy Working version: 2016 1 Corporate Restructuring in the Asian electronics market: Insights from Philips and Panasonic Disguised Case and Teaching Note: Download from the Emerald Emerging Markets Case Studies Reddy, K.S., Agrawal, R., & Nangia, V. K. (2012). Drop-offs in the Asian electronics market: unloading Bolipps and Canssonic. Emerald Emerging Markets Case Studies, 2(8), 1-12. ABSTRACT (DON’T CITE THIS WORKING VERSION) Subject area of the Case: Business Policy and Strategy – Sell-off and Joint venture Student level and proposed courses: Graduation and Post Graduation (BBA, MBA and other management degrees). It includes lessons on Strategic Management and Multinational Business Environment. Brief overview of the Case: The surge in Asian electronics business becomes a global platform for international vendors and customers. Conversely, Chinese and Korean firms have become the foremost manufacturing & fabrication nucleus for electronic supplies in the world. This is also a roaring example of success from Asian developing nations. This case presents the fortune of Asian rivals in the electronics business that made Philips and Panasonic to redesign and reform their global tactics for long-term sustainable occurrence in the emerging economies market. Further, it also discusses the reasons behind their current mode of business and post deal issues. Expected learning outcomes: This case describes a way to impart the managerial and leadership strategies from the regular business operations happening in and around the world. -

ENERGY STAR Consumer Audio/Video Product List

ENERGY STAR Consumer Audio/Video Product List List Posted on July 15, 2010 *Includes All ENERGY STAR Qualified Models Submitted to EPA, Including Models that Are Not Available in the U.S. and Models that May No Longer Be Available in the Market Organization Name Brand Name Model Name Model Number Product Name Watts in Standby Altec Lansing, LLC Altec Lansing inMotion Compact iMT320 Powered Speaker 0.045 Audio Partnership PLC Cambridge Audio azur 550A Stereo Amplifier 0.75 Compact Disc Audio Partnership PLC Cambridge Audio azur 550C Player/Changer 0.82 Audio Partnership PLC Cambridge Audio azur 650A Stereo Amplifier 0.75 Audio Partnership PLC Cambridge Audio azur 650BD DVD Product 0.77 Compact Disc Audio Partnership PLC Cambridge Audio azur 650C Player/Changer 0.81 Audio Partnership PLC Cambridge Audio azur 650R Receiver 0.9 Audio Partnership PLC Cambridge Audio azur 650T Tuner 0.9 Audio Partnership PLC MordauntShort Aviano 7 Powered Speaker 0.42 Audio Partnership PLC MordauntShort Aviano 9 Powered Speaker 0.45 Audio Research Corp. Audio Research DS450 DS450 Stereo Amplifier 0.05 Audio Research Corp. Audio Research DSi200 DSi200 Stereo Amplifier 0.9 iPod CD USB Shelf Beautiful Enterprise Co., Ltd. INSIGNIA System NSES6113 Micro Systems 0.828 Best Buy Corp. Exclusive Insignia Blu Ray Brands Insignia DVD Player NSBRDVD DVD Product .51 Best Buy Corp. Exclusive Compact Disc Brands Insignia NSB3112 NSB3112 Player/Changer 0.8 Best Buy Corp. Exclusive Compact Disc Brands Insignia NSB4111 NSB4111 Player/Changer 0.8 Best Buy Corp. Exclusive Compact Disc Brands Insignia NSB4113 NSB4113 Player/Changer 0.29 Best Buy Corp. -

Nokia 3220 User Guide in French

Manuel d'utilisation du Nokia 3220 9233114 Édition 3 DÉCLARATION DE CONFORMITÉ Nous, NOKIA CORPORATION, déclarons sous notre seule responsabilité la conformité du produit RH-37 aux dispositions de la directive européenne 1999/5/CE. La déclaration de conformité peut être consultée à l'adresse suivante : http://www.nokia.com/phones/declaration_of_conformity/. Copyright © 2005 Nokia. Tous droits réservés. Le symbole de la poubelle sur roues barrée d’une croix signifie que ce produit doit faire l’objet d’une collecte sélective en fin de vie au sein de l’Union européenne. Cette mesure s’applique non seulement à votre appareil mais également à tout autre accessoire marqué de ce symbole. Ne jetez pas ces produits dans les ordures ménagères non sujettes au tri sélectif. La reproduction, le transfert, la distribution ou le stockage d'une partie ou de la totalité du contenu de ce document, sous quelque forme que ce soit, sans l'autorisation écrite préalable de Nokia est interdite. Nokia, Nokia Connecting People, Xpress-on et Pop-Port sont des marques commerciales ou des marques déposées de Nokia Corporation. Les autres noms de produits et de sociétés mentionnés dans ce document peuvent être des marques commerciales ou des noms de marques de leurs détenteurs respectifs. Nokia tune est une marque sonore de Nokia Corporation. Licence américaine Nº 5818437 et autres brevets en instance. Dictionnaire T9 Copyright (C) 1997-2005. Tegic Communications, Inc. Tous droits réservés. Comprend le logiciel de cryptographie ou de protocole de sécurité RSA BSAFE de RSA Security. Java est une marque commerciale de Sun Microsystems, Inc. -

Philips 2017 Annual Report

Investor Relations 15.1 In 2017, a dividend of EUR 0.80 per common share was Exchange rate (based on the “Noon Buying Rate”) EUR per USD paid in cash or shares, at the option of the shareholder. 2013 - 2017 For 48.3% of the shares, the shareholders elected for a period end average high low share dividend, resulting in the issue of 11,264,163 new 2013 0.7257 0.7532 0.7828 0.7238 common shares, leading to a 1.2% dilution. EUR 384 2014 0.8264 0.7533 0.8264 0.7180 million was paid in cash. See also section 3.5, Proposed 2015 0.9209 0.9018 0.9502 0.8323 distribution to shareholders, of this Annual Report. 2016 0.9477 0.9037 0.9639 0.8684 2017 0.8318 0.8867 0.9601 0.8305 ex-dividend date record date payment date Exchange rate per month (based on the “Noon Buying Euronext Rate”) EUR per USD Amsterdam May 7, 2018 May 8, 2018 June 6, 2018 2017 - 2018 New York highest rate lowest rate Stock Exchange May 7, 2018 May 8, 2018 June 6, 2018 August, 2017 0.8545 0.8316 September, 2017 0.8513 0.8305 October, 2017 0.8636 0.8441 Philips Group November, 2017 0.8638 0.8378 Dividend and dividend yield per common share 2008 - 2018 December, 2017 0.8529 0.8318 January, 2018 0.8388 0.8008 5.1% 4.6% 3.4% 3.3% 3.8% 3.3% 3.4% 2.4% 3.0% 2.8% 2.5% Yield in %1) Unless otherwise stated, for the convenience of the 2) 0.80 0.80 0.80 0.80 0.80 Dividend per reader, the translations of euros into US dollars 0.75 0.75 0.75 0.70 0.70 0.70 share in EUR appearing in this section have been made based on the closing rate on December 31, 2017 (USD 1 = EUR 0.8365). -

A Diagnostic X-Ray Tube with Spiral-Groove Bearings

Philips Tech. Rev. 44, No. 11/12, 357-363, Nov. 1989 357 A diagnostic X-ray tube with spiral-groove bearings E. A. Muijderman, C. D. Roelandse, A. Vetter and P. Schreiber The technological development of a product usually advances in a series of small steps. But not always - one example is the change from fixed to rotating anodes in diagnostic X-ray tubes in about 1930. This was a development in which Philips played a leading part, largely because of the work of Albert Bouwers'". Since then there has been a steady stream of small improvements in diagnostic X-ray tubes, mostly because problems with limited bearing life and inadequate cooling of the anode have led designers to make modifications. It now looks as though there has been another great leap forward in solving these problems: spiral groove anode bearings lubricated by liquid metal. Introduetion A diagnostic X-ray tube has to deliver a large So that the anode can rotate it must be provided amount of radiation from the smallest possible area with bearings and driven by an electric motor, which of the anode, the 'point focus', in a time of several has to be an induction motor. The anode, the bearings milliseconds to several seconds [11. The quantity of and the rotor of the induction motor are located radiation must be large enough for a sufficient num- inside the evacuated tube. The bearings therefore ber of electrons to be released at the input screen of an have to meet a number of rather special requirements. X-ray intensifier tube [21, or to produce sufficient The lubricant for the bearings must not contaminate blackening in an X-ray-sensitive film after develop- the vacuum of the tube, the bearings must be able to ment.