Survey of Large-Scale Office Building Supply in Tokyo's 23 Wards 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

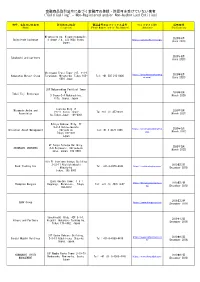

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) Miyakojima-ku, Higashinodamachi, 2020年6月 SwissTrade Exchange 4-chōme−7−4, 534-0024 Osaka, https://swisstrade.exchange/ (June 2020) Japan 2020年6月 Takahashi and partners (June 2020) Shiroyama Trust Tower 21F, 4-3-1 https://www.hamamatsumerg 2020年6月 Hamamatsu Merger Group Toranomon, Minato-ku, Tokyo 105- Tel: +81 505 213 0406 er.com/ (June 2020) 0001 Japan 28F Nakanoshima Festival Tower W. 2020年3月 Tokai Fuji Brokerage 3 Chome-2-4 Nakanoshima. (March 2020) Kita. Osaka. Japan Toshida Bldg 7F Miyamoto Asuka and 2020年3月 1-6-11 Ginza, Chuo- Tel:+81 (3) 45720321 Associates (March 2021) ku,Tokyo,Japan. 104-0061 Hibiya Kokusai Bldg, 7F 2-2-3 Uchisaiwaicho https://universalassetmgmt.c 2020年3月 Universal Asset Management Chiyoda-ku Tel:+81 3 4578 1998 om/ (March 2022) Tokyo 100-0011 Japan 9F Tokyu Yotsuya Building, 2020年3月 SHINBASHI VENTURES 6-6 Kojimachi, Chiyoda-ku (March 2023) Tokyo, Japan, 102-0083 9th Fl Onarimon Odakyu Building 3-23-11 Nishishinbashi 2019年12月 Rock Trading Inc Tel: +81-3-4579-0344 https://rocktradinginc.com/ Minato-ku (December 2019) Tokyo, 105-0003 Izumi Garden Tower, 1-6-1 https://thompsonmergers.co 2019年12月 Thompson Mergers Roppongi, Minato-ku, Tokyo, Tel: +81 (3) 4578 0657 m/ (December 2019) 106-6012 2019年12月 SBAV Group https://www.sbavgroup.com (December 2019) Sunshine60 Bldg. 42F 3-1-1, 2019年12月 Hikaro and Partners Higashi-ikebukuro Toshima-ku, (December 2019) Tokyo 170-6042, Japan 31F Osaka Kokusai Building, https://www.smhpartners.co 2019年12月 Sendai Mubuki Holdings 2-3-13 Azuchi-cho, Chuo-ku, Tel: +81-6-4560-4410 m/ (December 2019) Osaka, Japan. -

Unifying Rail Transportation and Disaster Resilience in Tokyo

University of Arkansas, Fayetteville ScholarWorks@UARK Architecture Undergraduate Honors Theses Architecture 5-2020 The Yamanote Loop: Unifying Rail Transportation and Disaster Resilience in Tokyo Mackenzie Wade Follow this and additional works at: https://scholarworks.uark.edu/archuht Part of the Urban, Community and Regional Planning Commons Citation Wade, M. (2020). The Yamanote Loop: Unifying Rail Transportation and Disaster Resilience in Tokyo. Architecture Undergraduate Honors Theses Retrieved from https://scholarworks.uark.edu/archuht/41 This Thesis is brought to you for free and open access by the Architecture at ScholarWorks@UARK. It has been accepted for inclusion in Architecture Undergraduate Honors Theses by an authorized administrator of ScholarWorks@UARK. For more information, please contact [email protected]. The Yamanote Loop: Unifying Rail Transportation and Disaster Resilience in Tokyo by Mackenzie T. Wade A capstone submitted to the University of Arkansas in partial fulfillment of the requirements of the Honors Program of the Department of Architecture in the Fay Jones School of Architecture + Design Department of Architecture Fay Jones School of Architecture + Design University of Arkansas May 2020 Capstone Committee: Dr. Noah Billig, Department of Landscape Architecture Dr. Kim Sexton, Department of Architecture Jim Coffman, Department of Landscape Architecture © 2020 by Mackenzie Wade All rights reserved. ACKNOWLEDGEMENTS I would like to acknowledge my honors committee, Dr. Noah Billig, Dr. Kim Sexton, and Professor Jim Coffman for both their interest and incredible guidance throughout this project. This capstone is dedicated to my family, Grammy, Mom, Dad, Kathy, Alyx, and Sam, for their unwavering love and support, and to my beloved grandfather, who is dearly missed. -

(English Version of School Brochure) Japanese Preschool & Elementary

Japanese Children’s Society, Inc. (English version of school brochure) Japanese Preschool & Elementary School Contents I. Preschool Curriculum -------------------------------------------------------------- 3 II. Elementary School Curriculum ----------------------------------------------------- 6 III. Campus and Classrooms ---------------------------------------------------------- 10 IV. Bus Service ----------------------------------------------------------------------- 10 V. Directions --------------------------------------------------------------------------10 School Song Written by Shinichiro Sako Composed by Shoichiro Sako Translated by Toshikatsu Konishi 1. A blue sky is broadening over the earth, The mighty Hudson River is flowing into the bay, Like a young tree growing up healthily and quickly, All of us extend our hands And grow strong and big, in our school 2. On the bright windows filled with light, Reflecting smiling faces with enjoyment, Like small birds singing amicably All of us live in harmony Encourage and train with each other, in our school 3. In the city where a large number of people gather together from all over the world In search of freedom and dreaming of a future Like the Stature of Liberty uplifting a torch All of us are afire with high hopes, And build the joy of peace, in our school, in our school 1 Japanese Children’s Society, Inc. Mission Statement 1. To give Japanese preschool and elementary aged children a broad, rich education. 2. To shape and nurture their social and intellectual development. 3. To provide support and education in first language acquisition to preschool and elementary aged students. 4. To provide a cosmopolitan educational experience to students. Our belief is that our students must have a comprehensive knowledge and understanding of the Japanese language and culture in order to survive in today’s world. -

Tokyo Sightseeing Route

Mitsubishi UUenoeno ZZoooo Naationaltional Muuseumseum ooff B1B1 R1R1 Marunouchiarunouchi Bldg. Weesternstern Arrtt Mitsubishiitsubishi Buildinguilding B1B1 R1R1 Marunouchi Assakusaakusa Bldg. Gyoko St. Gyoko R4R4 Haanakawadonakawado Tokyo station, a 6-minute walk from the bus Weekends and holidays only Sky Hop Bus stop, is a terminal station with a rich history KITTE of more than 100 years. The “Marunouchi R2R2 Uenoeno Stationtation Seenso-jinso-ji Ekisha” has been designated an Important ● Marunouchi South Exit Cultural Property, and was restored to its UenoUeno Sta.Sta. JR Tokyo Sta. Tokyo Sightseeing original grandeur in 2012. Kaaminarimonminarimon NakamiseSt. AASAHISAHI BBEEREER R3R3 TTOKYOOKYO SSKYTREEKYTREE Sttationation Ueenono Ammeyokoeyoko R2R2 Uenoeno Stationtation JR R2R2 Heeadad Ofccee Weekends and holidays only Ueno Sta. Route Map Showa St. R5R5 Ueenono MMatsuzakayaatsuzakaya There are many attractions at Ueno Park, ● Exit 8 *It is not a HOP BUS (Open deck Bus). including the Tokyo National Museum, as Yuushimashima Teenmangunmangu The shuttle bus services are available for the Sky Hop Bus ticket. well as the National Museum of Western Art. OkachimachiOkachimachi SSta.ta. Nearby is also the popular Yanesen area. It’s Akkihabaraihabara a great spot to walk around old streets while trying out various snacks. Marui Sooccerccer Muuseumseum Exit 4 ● R6R6 (Suuehirochoehirocho) Sumida River Ouurr Shhuttleuttle Buuss Seervicervice HibiyaLine Sta. Ueno Weekday 10:00-20:00 A Marunouchiarunouchi Shuttlehuttle Weekend/Holiday 8:00-20:00 ↑Mukojima R3R3 TOKYOTOKYO SSKYTREEKYTREE TOKYO SKYTREE Sta. Edo St. 4 Front Exit ● Metropolitan Expressway Stationtation TOKYO SKYTREE Kaandanda Shhrinerine 5 Akkihabaraihabara At Solamachi, which also serves as TOKYO Town Asakusa/TOKYO SKYTREE Course 1010 9 8 7 6 SKYTREE’s entrance, you can go shopping R3R3 1111 on the first floor’s Japanese-style “Station RedRed (1 trip 90 min./every 35 min.) Imperial coursecourse Theater Street.” Also don’t miss the fourth floor Weekday Asakusa St. -

Major Projects

Major Projects November 2012 www.mitsuifudosan.co.jp/english Project Map (Central Tokyo) 33 13 28 12 19 7 8 26 1 27 6 5 2 9 4 32 17 11 31 10 23 3 14 15 22 24 21 30 20 16 25 29 18 Map data ©2012 Google, ZENRIN Existing Projects New Projects 1. Nihonbashi Mitsui Tower 13. Garden Air Tower 25. DiverCity Tokyo 2. Nihonbashi 1-Chome Building 14. Tokyo Midtown 26. Nihonbashi Honcho 2-Chome Project (COREDO Nihonbashi) 15. Shiodome City Center 27. Nihonbashi Muromachi East District 3. Ginza Mitsui Building 16. Celestine Shiba Mitsui Building Development Projects 4. Yaesu Mitsui Building 17. Akasaka Biz Tower 28. Iidabashi Station West Gate Project 5. GranTokyo North Tower 18. Gate City Osaki 29. Kita-Shinagawa 5-Chome Area 1 6. Sumitomo Mitsui Banking Corporation Redevelopment Project 19. Shinjuku Mitsui Building Head Office Building 30. Toyosu 2-, 3-Chome Area2 Project 20. Toyosu Center Building 7. Otemachi 1-Chome Mitsui Building 31. Hibiya Mitsui Building/ Sanshin Building 21. Toyosu Center Bu ilding Annex 8. Otemachi PAL Building Reconstruction Project 22. Toyosu ON Building 9. Marunouchi Mitsui Building 32. Nihonbashi 2-Chome Project (AreaC) 23. Kojun Building 10. Kasumigaseki Building 7. Otemachi 1-Chome Mitsui Building 24. Urban Dock LaLaport TOYOSU 11. Shin-Kasumigaseki Building 33. Ikebukuro Square 12. Jinbo-cho Mitsui Building Black: Office Buildings Red: Retail Facilities 1 Existing Projects Office Buildings (Owned) Chuo-ku Minato-ku Facility Nihonbashi Ginza Mitsui Yaesu Mitsui Nihonbashi 1- Tokyo Midtown name Mitsui Tower Chome Building -

Daiba Park to Monzen- 36 (No.3 Battery) Nakacho No.6 Battery Odaiba- Kaihin-Koen Tokyo Bay Daiba

Rainbow Bridge Waterbus (Odaiba-Kaihin-Koen) Daiba Park to Monzen- 36 (No.3 Battery) Nakacho No.6 battery Odaiba- Kaihin-Koen Tokyo bay Daiba Merpolitan Expressway Shiokaze Park Wangan line Metropolitan Expressway No.1 Museum of Maritime Science Waterbus Daiba Park (Fune-no-Kagakukan) Administrator ■ Tokyo Waterfront Group ●Location Daiba 1-chome, Minato Ward ●Contact Information Shiokaze Park Administration Office tel: 03-5500-0385 (1-2 Higashi-Yashio, Shinagawa-ku 135-0092) ●Transport 12-minute walk from Odaiba-Kaihin-Koen on Yurikamome (Shinbashi to Toyosu), 15-minute walk from Tokyo Teleport (Rinkai line) Water-bus: About 50-minute ride from Ryogoku or Kasai-Rinkai-Koen on Tokyo Mizube Cruising Line (tel: 03-5608-8869). Water-bus: 20-minute walk from Odaiba-Kaihin-Koen (20-minute ride from Hinode Pier on Tokyo Water Cruise)(tel: 0120-977-311). Daiba When the US fleet led by Commodore Perry arrived in Uraga in 1853 during the Bakumatsu (the end of Tokugawa shogunate), the shogunate No. 6 battery On the north side resides the remnants of the port made with stone. government did not have large ships to protect Edo from the attacks of foreign ships. More than the general citizenry, it was the shogunate that It can be viewed by climbing the bank of Daiba Park (the No. 3 battery). was surprised by the arrival of Perry’s back ships. It didn’t have any large ships to protect Edo from foreign at tack. So, the construction of daiba, or artillery batteries, was conceived. Of the 11 originally planned, only six were actually built off the shore of Shinagawa. -

Non-Existing Governmental Bodies)

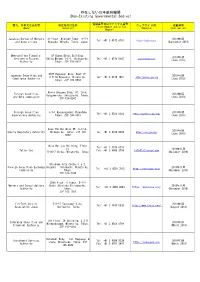

存在しない日本政府機関 (Non-Existing Governmental Bodies) 電話番号又はファックス番号 商号、名称又は氏名等 所在地又は住所 ウェブサイトURL 掲載時期 (Phone Number and/or Fax (Name) (Location) (Website) (Publication) Number) Japanese Bureau of Mergers 31 floor, Midtown Tower, 9-7-1 2019年9月 Tel: +81 3 4572 0701 https://japbma.org/ and Acquisitions Akasaka, Minato, Tokyo, Japan (September 2019) Metropolitan Financial 8F Humax Ebisu Building, 2019年6月 Services & Futures Ebisu Minami 1-1-1, Shibuya-ku, Tel: +81 3 4579 5647 www.mfinsfa.com (June 2019) Authority Tokyo, ZIP 150-0022 STEP Roppongi Bldg. West 1F, Japanese Securities and 2019年6月 6-8-10 Roppongi, Minato-ku, Tel: +81 3 4510 7897 http://jaseca-gov.org Compliance Authority (June 2019) Tokyo, ZIP 106-0032 World Udagawa Bldg. 6F, 36-6, Foreign Securities 2019年6月 Udagawa-cho, Shibuya-ku, Tokyo, and Bond commission (June 2019) ZIP 150-0042 Foreign Securities 3-7-1 Kasumigaseki,Chiyodaku 2019年6月 Tel: +81 3 4520 8922 https://www.fssa-gov.org/ Supervisory Authority Tokyo, ZIP 100-0013 (June 2019) Axes 7th Building 6F, 3-17-4, 2019年6月 Equity Regulatory Authority Shibuya-ku, Tokyo, ZIP 150- Tel: +81 3 4520 8934 https://era-gov.org/ (June 2019) 0002 Mita Belljyu Building, Floor Tel: +81 3 4579 0731 24, 2018年11月 Tatler Cox Fax: +81 3 6800 2769 [email protected] 5-36-7 Shiba, Minato-ku, Tokyo (November 2018) Shiodome City Center 1-5-2, Foreign Securities Exchange Higashi - Shinbashi, Minato-ku, 2018年11月 Tel: +81 3 4510 7815 http://fsec-gov.org/ Commission Tokyo, (November 2018) ZIP 105-7140 29th floor, C tower, 3-7-1 Mergers and Consolidations Nishi -

Bridge Architecture in Japan

International Journal of the Physical Sciences Vol. 6(17), pp. 4302-4310, 2 September, 2011 Available online at http://www.academicjournals.org/IJPS DOI: 10.5897/IJPS11.072 ISSN 1992 - 1950 ©2011 Academic Journals Full Length Research Paper Bridge architecture in Japan Hamed Niroumand1*, M. F. M. Zain2 and Maslina Jamil1 1Department of Architecture, Faculty of Engineering, National University of Malaysia (UKM), Malaysia. 2Deputy Dean, Faculty of Engineering, National University of Malaysia (UKM), Malaysia. Accepted 27 June, 2011 A bridge is a structure built to span physical obstacle such as a body of water, city, or road, for the purpose of providing passage over the obstacle. Bridges are a unique offshoot of architecture and possess their own associated terms, components and styles. This paper presents the second part of Japanese bridges by investigating architectural aspects of its design. Limited usable land in heavily populated areas of Japan has often necessitated the design of unique bridge approaches. One of such design is the spiral viaduct bridge approach. When this design is used, care is taken to make the structures aesthetically appealing. An important reason for the bridge construction will lead into a critical study of bridge aesthetics and structural design. According to the configuration of frameworks, bridges may be described as arched, girdered and cable stayed or suspension. Refereeing to Japanese bridges, those most frequently provided cable stayed in the construction of bridges are important factor in architecture and bridges aesthetic. This paper presents a brief history of bridge design in Japan, and then discusses the influence of technical factors on Japan bridges design. -

Survey of Large-Scale Office Building Supply in Tokyo's 23 Wards 2014

Survey of Large-scale Oce Building Supply in Tokyo’s 23 wards 2014 June 3,2014 Since 1986, Mori Trust Co., Ltd. (Head Oce: Minato-ku, Tokyo) has surveyed trends in the supply of large-scale oce buildings containing total oce space of 10,000 square meters or more within Tokyo’s 23 wards , based on various published materials, eld surveys, and interviews. The results of the most recent surveys(including the survey of mid-scale oce buildings) are presented below.In the calculation of total oce oor area, where the survey deals with multi-purpose buildings—buildings coupled with stores, living quarters or residences, hotels, etc.—only the oor area purely for oce use is taken into consideration. [Survey Date: December 2013] The supply is expected to remain near past averages Main Results of This Survey 1.Supply of large-scale oce buildings In 2013, Tokyo’s 23 wards saw the supply fall to 660,000 square meters, a signicant decline from the average for the past 20 years.The supply in 2014 is expected to be 930,000 square meters, approximately 15% lower than the past average. Annual projections for 2015-17 are at least one million square meters, similar to the past average. 2.Supply trends by area Supply in central Tokyo is expected to further increase during the 2014-17 timeframe: Some 70% of this space will be located in Tokyo’s three central wards. Some 30% of the overall supply is expected to be located in Chiyoda Ward, a consistent leader, followed by Minato Ward, whose share is projected to rise dramatically to more than 20%. -

Ministry of the Environment

List of Public Service Corporations under the Jurisdiction of the Ministry of the Environment ●Public Service Corporations (selected) (As of April 2001) Name of the corporation Address of the main office Telephone number <Under supervision of the Minister’s Secretariat> Environmental Information Center 8F, Office Toranomon1Bldg., 1-5-8 Toranomon, Minato-ku, Tokyo 105-0001 03-3595-3992 Earth, Water and Green Foundation 6F, Nishi-shinbashi YK Bldg., 1-17-4 Nishi-shinbashi, Minato-ku, Tokyo 105-0003 03-3503-7743 <Under supervision of the Waste Management and Recycling Department> Ecological Life and Culture Organization (ELCO) 6F, Sunrise Yamanishi Bldg., 1-20-10 Nishi-shinbashi, Minato-ku, Tokyo 105-0003 03-5511-7331 Japan Environmental Sanitation Center 10-6 Yotsuya-kamicho, Kawasaki-ku, Kawasaki-shi, Kanagawa Prefecture 210-0828 044-288-4896 The National Federation of 4F, Daini-AB Bldg., 3-1-17 Roppongi, Minato-ku, Tokyo 106-0032 03-3224-0811 Industrial Waste Management Associations Japan Industrial Waste Technology Center 2F, Nihonbashi Koa Bldg., 2-8-4 Nihonbashi-horidomecho, Chuo-ku, Tokyo 103-0012 03-3668-6511 Japan Industrial Waste Management Foundation Sakura Shinbashi Bldg., 2-6-1 Shinbashi, Minato-ku, Tokyo 105-0004 03-3500-0271 All Japan Private Sewerage Treatment Association 7F, Tokyo Yofuku Kaikan, 13 Ichigaya-hachimancho, Shinjuku-ku, Tokyo 162-0844 03-3267-9757 Japan Education Center of Environmental Sanitation 2-23-3 Kikukawa, Sumida-ku, Tokyo 130-0024 03-3635-4880 Waste Water Treatment Equipment Engineer Center Kojimachi 4-chome Bldg., 4-3 Kojimachi, Chiyoda-ku, Tokyo 102-0083 03-3237-6591 Japan Sewage Works Association 1F, Nihon Bldg., 2-6-2 Otemachi, Chiyoda-ku, Tokyo 100-0004 03-5200-0811 Japan Waste Management Association 7F, IPB Ochanomizu, 3-3-11 Hongo, Bunkyo-ku, Tokyo 113-0033 03-5804-6281 Japan Sewage Treatment Plant Operation and 5F, Sakura Bldg., 1-3-3 Uchikanda, Chiyoda-ku, Tokyo 101-0047 03-5281-9291 Maintenance Association, INC. -

Download Hotel's Digital Brochure

Good location with a 4 minute walk from Karasumori Exit in Shimbashi Station on the JR lines, a 3 minute by train from Tokyo Station, a 2 minute by train from Hamamatsucho Station. Customers using the Shinkansen or an airplane are also very convenient. It is perfect for business and leisure. This hotel accepts cashless payment. Please use a credit card or QR code payment system for payments of charges. * Image for illustrative purposes. ROOM EQUIPMENTS / AMENITY * Women's amenity kit is offered at the lobby. * Mobile charger is lent at the front desk. Women's amenity kit * Image for illustrative purposes. NUMBERS OF GUEST ROOMS : 220 Double Numbers Room Type Room size(㎡) Bed size(mm) of rooms Floor Single 12.7 1200 56 3~16 Superior Single 13.3 1200 69 3~16 Double 13.7 1400 94 3~16 Universal 18.7 1200 1 3 COFFEE ROOM Renoir BREAKFAST 【Restaurant Renoir (2nd floor)】 OPEN HOURS : 7:00~12:00PM(L.O.11:30) NUMBERS OF SEATS : 70 MENU : A light breakfast of sandwiches and drinks is available. We offer Renoir original blend coffee, made with Ethiopian Mocha. PRICE : 840 yen (tax included) ABOUT THE HOTEL ADDRESS : 4-10-2 , Shinbashi, Minato-ku Tokyo 105-0004 TEL : (+81)3-6695-0203 FAX : (+81)3-6695-0223 CHECK-IN/OUT : 15:00/11:00 AVAILABLE PAYMENT : VISA・MASTER・JCB・AMEX・DINERS・DISCOVER・UnionPay METHODS LINE Pay・PayPay・d barai・au PAY・Rpay・ALIPAY・WeChatPay *This hotel accepts cashless payment. E-MAIL : [email protected] URL : https://fresa-inn.jp/en/shinbashi-karasumoriguchi/ ACCESS : A 4 minute walk from the Karasumori Exit in Shimbashi Station on the JR Lines LOCATION *Estimated travel time is based on Google map. -

Experience and Track Record in Marunouchi

Otemachi Park Building, 1-1, Otemachi 1-chome, Chiyoda-ku, Tokyo 100-8133, Japan TEL +81-3-3287-5200 http://www.mec.co.jp/ Experience and Track Record in Marunouchi 1890 The construction of the area’s first modern office Building, Mitsubishi 1900 1890s – 1950s Ichigokan, was completed in 1894. Soon after, three-story redbrick office First Phase of Buildings began springing up, resulting in the area becoming known as the 1910 “London Block.” Development Following the opening of Tokyo Station in 1914, the area was further 1890s developed as a business center. American-style large reinforced concrete 1920 Dawning of a Full-Scale Buildings lined the streets. Along with the more functional look, the area Starting from Business Center Development was renamed the “New York Block.” Scratch 1940 Purchase of Marunouchi Land and Vision of a Major Business Center 1950 As Japan entered an era of heightened economic growth, there was a sharp 1960 1960s – 1980s increase in demand for office space. Through the Marunouchi remodeling plan that began in 1959, the area was rebuilt with large-scale office buildings, providing a considerable supply of highly integrated office space. 1970 Second Phase of Sixteen such buildings were constructed, increasing the total available floor Development space by more than five times. In addition, Naka-dori Avenue, stretching 1980 An Abundance of Large-Capacity from north to south through the Marunouchi area, was widened from 13 Office Buildings Reflecting a meters to 21 meters. The 1980s marked the appearance of high-rise buildings more than 100 The history of Tokyo’s Marunouchi 1990 Period of Rapid Economic Growth meters tall in the area.