Survey of Large-Scale Office Building Supply in Tokyo's 23 Wards 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

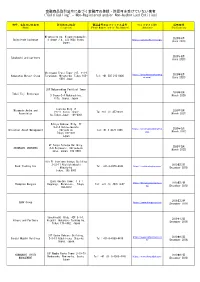

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) Miyakojima-ku, Higashinodamachi, 2020年6月 SwissTrade Exchange 4-chōme−7−4, 534-0024 Osaka, https://swisstrade.exchange/ (June 2020) Japan 2020年6月 Takahashi and partners (June 2020) Shiroyama Trust Tower 21F, 4-3-1 https://www.hamamatsumerg 2020年6月 Hamamatsu Merger Group Toranomon, Minato-ku, Tokyo 105- Tel: +81 505 213 0406 er.com/ (June 2020) 0001 Japan 28F Nakanoshima Festival Tower W. 2020年3月 Tokai Fuji Brokerage 3 Chome-2-4 Nakanoshima. (March 2020) Kita. Osaka. Japan Toshida Bldg 7F Miyamoto Asuka and 2020年3月 1-6-11 Ginza, Chuo- Tel:+81 (3) 45720321 Associates (March 2021) ku,Tokyo,Japan. 104-0061 Hibiya Kokusai Bldg, 7F 2-2-3 Uchisaiwaicho https://universalassetmgmt.c 2020年3月 Universal Asset Management Chiyoda-ku Tel:+81 3 4578 1998 om/ (March 2022) Tokyo 100-0011 Japan 9F Tokyu Yotsuya Building, 2020年3月 SHINBASHI VENTURES 6-6 Kojimachi, Chiyoda-ku (March 2023) Tokyo, Japan, 102-0083 9th Fl Onarimon Odakyu Building 3-23-11 Nishishinbashi 2019年12月 Rock Trading Inc Tel: +81-3-4579-0344 https://rocktradinginc.com/ Minato-ku (December 2019) Tokyo, 105-0003 Izumi Garden Tower, 1-6-1 https://thompsonmergers.co 2019年12月 Thompson Mergers Roppongi, Minato-ku, Tokyo, Tel: +81 (3) 4578 0657 m/ (December 2019) 106-6012 2019年12月 SBAV Group https://www.sbavgroup.com (December 2019) Sunshine60 Bldg. 42F 3-1-1, 2019年12月 Hikaro and Partners Higashi-ikebukuro Toshima-ku, (December 2019) Tokyo 170-6042, Japan 31F Osaka Kokusai Building, https://www.smhpartners.co 2019年12月 Sendai Mubuki Holdings 2-3-13 Azuchi-cho, Chuo-ku, Tel: +81-6-4560-4410 m/ (December 2019) Osaka, Japan. -

Tokyo Sightseeing Route

Mitsubishi UUenoeno ZZoooo Naationaltional Muuseumseum ooff B1B1 R1R1 Marunouchiarunouchi Bldg. Weesternstern Arrtt Mitsubishiitsubishi Buildinguilding B1B1 R1R1 Marunouchi Assakusaakusa Bldg. Gyoko St. Gyoko R4R4 Haanakawadonakawado Tokyo station, a 6-minute walk from the bus Weekends and holidays only Sky Hop Bus stop, is a terminal station with a rich history KITTE of more than 100 years. The “Marunouchi R2R2 Uenoeno Stationtation Seenso-jinso-ji Ekisha” has been designated an Important ● Marunouchi South Exit Cultural Property, and was restored to its UenoUeno Sta.Sta. JR Tokyo Sta. Tokyo Sightseeing original grandeur in 2012. Kaaminarimonminarimon NakamiseSt. AASAHISAHI BBEEREER R3R3 TTOKYOOKYO SSKYTREEKYTREE Sttationation Ueenono Ammeyokoeyoko R2R2 Uenoeno Stationtation JR R2R2 Heeadad Ofccee Weekends and holidays only Ueno Sta. Route Map Showa St. R5R5 Ueenono MMatsuzakayaatsuzakaya There are many attractions at Ueno Park, ● Exit 8 *It is not a HOP BUS (Open deck Bus). including the Tokyo National Museum, as Yuushimashima Teenmangunmangu The shuttle bus services are available for the Sky Hop Bus ticket. well as the National Museum of Western Art. OkachimachiOkachimachi SSta.ta. Nearby is also the popular Yanesen area. It’s Akkihabaraihabara a great spot to walk around old streets while trying out various snacks. Marui Sooccerccer Muuseumseum Exit 4 ● R6R6 (Suuehirochoehirocho) Sumida River Ouurr Shhuttleuttle Buuss Seervicervice HibiyaLine Sta. Ueno Weekday 10:00-20:00 A Marunouchiarunouchi Shuttlehuttle Weekend/Holiday 8:00-20:00 ↑Mukojima R3R3 TOKYOTOKYO SSKYTREEKYTREE TOKYO SKYTREE Sta. Edo St. 4 Front Exit ● Metropolitan Expressway Stationtation TOKYO SKYTREE Kaandanda Shhrinerine 5 Akkihabaraihabara At Solamachi, which also serves as TOKYO Town Asakusa/TOKYO SKYTREE Course 1010 9 8 7 6 SKYTREE’s entrance, you can go shopping R3R3 1111 on the first floor’s Japanese-style “Station RedRed (1 trip 90 min./every 35 min.) Imperial coursecourse Theater Street.” Also don’t miss the fourth floor Weekday Asakusa St. -

Major Projects

Major Projects November 2012 www.mitsuifudosan.co.jp/english Project Map (Central Tokyo) 33 13 28 12 19 7 8 26 1 27 6 5 2 9 4 32 17 11 31 10 23 3 14 15 22 24 21 30 20 16 25 29 18 Map data ©2012 Google, ZENRIN Existing Projects New Projects 1. Nihonbashi Mitsui Tower 13. Garden Air Tower 25. DiverCity Tokyo 2. Nihonbashi 1-Chome Building 14. Tokyo Midtown 26. Nihonbashi Honcho 2-Chome Project (COREDO Nihonbashi) 15. Shiodome City Center 27. Nihonbashi Muromachi East District 3. Ginza Mitsui Building 16. Celestine Shiba Mitsui Building Development Projects 4. Yaesu Mitsui Building 17. Akasaka Biz Tower 28. Iidabashi Station West Gate Project 5. GranTokyo North Tower 18. Gate City Osaki 29. Kita-Shinagawa 5-Chome Area 1 6. Sumitomo Mitsui Banking Corporation Redevelopment Project 19. Shinjuku Mitsui Building Head Office Building 30. Toyosu 2-, 3-Chome Area2 Project 20. Toyosu Center Building 7. Otemachi 1-Chome Mitsui Building 31. Hibiya Mitsui Building/ Sanshin Building 21. Toyosu Center Bu ilding Annex 8. Otemachi PAL Building Reconstruction Project 22. Toyosu ON Building 9. Marunouchi Mitsui Building 32. Nihonbashi 2-Chome Project (AreaC) 23. Kojun Building 10. Kasumigaseki Building 7. Otemachi 1-Chome Mitsui Building 24. Urban Dock LaLaport TOYOSU 11. Shin-Kasumigaseki Building 33. Ikebukuro Square 12. Jinbo-cho Mitsui Building Black: Office Buildings Red: Retail Facilities 1 Existing Projects Office Buildings (Owned) Chuo-ku Minato-ku Facility Nihonbashi Ginza Mitsui Yaesu Mitsui Nihonbashi 1- Tokyo Midtown name Mitsui Tower Chome Building -

Experience and Track Record in Marunouchi

Otemachi Park Building, 1-1, Otemachi 1-chome, Chiyoda-ku, Tokyo 100-8133, Japan TEL +81-3-3287-5200 http://www.mec.co.jp/ Experience and Track Record in Marunouchi 1890 The construction of the area’s first modern office Building, Mitsubishi 1900 1890s – 1950s Ichigokan, was completed in 1894. Soon after, three-story redbrick office First Phase of Buildings began springing up, resulting in the area becoming known as the 1910 “London Block.” Development Following the opening of Tokyo Station in 1914, the area was further 1890s developed as a business center. American-style large reinforced concrete 1920 Dawning of a Full-Scale Buildings lined the streets. Along with the more functional look, the area Starting from Business Center Development was renamed the “New York Block.” Scratch 1940 Purchase of Marunouchi Land and Vision of a Major Business Center 1950 As Japan entered an era of heightened economic growth, there was a sharp 1960 1960s – 1980s increase in demand for office space. Through the Marunouchi remodeling plan that began in 1959, the area was rebuilt with large-scale office buildings, providing a considerable supply of highly integrated office space. 1970 Second Phase of Sixteen such buildings were constructed, increasing the total available floor Development space by more than five times. In addition, Naka-dori Avenue, stretching 1980 An Abundance of Large-Capacity from north to south through the Marunouchi area, was widened from 13 Office Buildings Reflecting a meters to 21 meters. The 1980s marked the appearance of high-rise buildings more than 100 The history of Tokyo’s Marunouchi 1990 Period of Rapid Economic Growth meters tall in the area. -

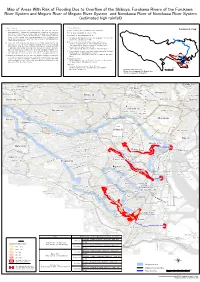

Map of Areas with Risk of Flooding Due to Overflow of the Shibuya

Map of Areas With Risk of Flooding Due to Overflow of the Shibuya, Furukawa Rivers of the Furukawa River System and Meguro River of Meguro River System and Nomikawa River of Nomikawa River System (estimated high rainfall) 1. About this map 2. Basic information Location map (1) Pursuant to the provisions of the Flood Control Act, this map shows the (1) Map created by the Tokyo Metropolitan Government areas expected to flood and anticipated depth of inundation that can occur (2) Risk areas designated on June 27, 2019 when there is the level of rainfall used as a basis for flood control measures for sections subject to flood warnings of the Shibuya, Furukawa (3) Released as TMG announcement No.162 Rivers of the Furukawa River System and Meguro River of Meguro River (4) Designation made based on Article 14, paragraph 2 of the Flood System and those subject to water-level notification of the Nomikawa River Control Act (Act No.193 of 1949) of Nomikawa River System. (5) River subject to flood warnings covered by this map (2) This river flood risk map uses a simulation to show inundation that can Shibuya, Furukawa Rivers of the Furukawa River System occur due to overflow of the Shibuya, Furukawa Rivers of the Furukawa Sumida River (The flood warning section is shown in the table below.) River System and Meguro River of Meguro River System and Nomikawa River Meguro River of Meguro River System of Nomikawa River System resulting from the level of rainfall used as a (The flood warning section is shown in the table below.) basis for flood control measures with an annual exceedance probability of 1 percent. -

Mitsui Fudosan Completed the Construction of Toyosu Bayside

To prevent further spread of COVID-19, the scaled-up opening of Mitsui Shopping Park Urban Dock LaLaport Toyosu (Toyosu Bayside Cross Tower) has been postponed. The alter schedule will be announced on its official website at a later date. March 31, 2020 For immediate release Mitsui Fudosan Co., Ltd. Located in the Toyosu Bayside Cross Area Large-Scale Development Linked Directly to Toyosu Station Mitsui Fudosan Completed the Construction of Toyosu Bayside Cross Tower Tokyo, Japan, March 31, 2020—Mitsui Fudosan Co., Ltd., a leading global real estate company headquartered in Tokyo, announced that today it completed the construction of Toyosu Bayside Cross Tower, which will form the core of the Toyosu Bayside Cross advanced in the Toyosu 2-Chome Station Area with cooperation from the owner of the project site, IHI Corporation. Toyosu Bayside Cross is part of the large-scale development in Toyosu 2-chome and 3-chome that started in the 1980s. In collaboration with IHI, Mitsui Fudosan has built the Toyosu Park Bridge to adjacent Toyosu Park and established a pedestrian deck directly linking to Mitsui Shopping Park Urban Dock LaLaport TOYOSU 1 (LaLaport TOYOSU 1), further realizing a horizontal, mixed-use facility by forming a network with the surrounding area and making it easier to get around. Toyosu Bayside Cross Tower, which was completed today, will meet the wide ranging needs of diverse people; it is a mixed-use development including an office zone equipped with state-of-the-art functions, a retail zone with a rich variety of shops, a hotel capable of serving guests ranging from business people to tourists and an energy center supporting safety and security. -

Urawa Saitama- Shintoshin

Outline of timetable beyond normal train operation(The Olympic games period) The contents are under consideration and may be sbujects to change. As of 22 Jan. 2020 1.Train lines around venue(Timetable at stasions around venue) ・Venues outside JR Yamanote Line, in where games will finish after 11pm. <Reference> Current Last Extention Last Train Service period/Departure Sta./Frequency after normal train service Venue Train line Departure Sta. Arrival Sta. Train Time ※ Musashino 0:30am Shinjuku Everyday/Takahata-fudo Sta./- 0:13 I Forest Sport Keio Line Tobitakyu Plaza for more 0:46 1:40am Keio-hachioji Everyday/ Shinjuku Sta./- (Bound for Takahata- Ⅱ Fudo Sta.) details, Tokyo Metro 1:50am Ikebukuro Everyday/ Shin-kiba Sta./- refer to 0:14 IIII Toyosu Yurakucho Line [2. Other 1:30am Shin-kiba Everyday/ Ikebukuro Sta./- 0:33 Ⅱ train lines]. 1:10am Osaki Everyday/ Shin-kiba Sta./- 23:58 Ⅲ Ariake Arena Rinkai Line Kokusai-tenjijo / Shinonome 1:50am Shin-kiba Everyday/ Osaki Sta./- 0:00 IIII 0:50am Shimbashi Everyday/ Toyosu Sta./- 23:55 Ⅱ Yurikamome Shin-toyosu 1:20am Toyosu Everyday/ Shimbashi Sta./- 0:19 Ⅲ Aomi Urban 1:20am Osaki Everyday/ Shin-kiba Sta./- 0:00 Ⅲ Rinkai Line Tokyo Teleport Sports Park 1:40am Shin-kiba Everyday/ Osaki Sta./- 23:57 IIII 0:30am Ikebukuro Everyday/Omiya Sta./ 25 min 23:49 Ⅱ JR Saikyo Line Kita-Yono 1:40am Omiya Everyday/Shinjuku Sta./ 30 min 0:35 Ⅲ JR Keihin-Tohoku 1:30am Akabane Everyday/Omiya Sta./ 20 min 0:33 Ⅱ Saitama Super Line Arena Saitama- 2:10am Omiya Everyday/Ofuna Sta./ 20 min 1:14 Ⅱ JR Takasaki Line -

Survey of Large-Scale Office Building Supply in Tokyo's 23 Wards 2018

Survey of Large-Scale Office Building Supply in Tokyo’s 23 Wards 2018 April 25, 2018 Mori Trust Co., Ltd., (Head Office: Minato-ku, Tokyo) has surveyed supply trends for large-scale office buildings with total office space of 10,000 square meters or more in Tokyo’s 23 wards since 1986 and for mid-size office buildings with total office space of 5,000 square meters to less than 10,000 square meters since 2013, based on various published materials, field surveys, and interviews. The results of the most recent survey are presented below. In calculating total office floor area, where the survey deals with multipurpose buildings—buildings that also contain retail space, residential space, or hotels—the calculation includes only the floor area set aside solely for office use. [Survey Date: December 2017] Supply to increase in 2018–2020 and decline subsequently —Supply in 2021–2022 to be half the past average or lower— Main Results of This Survey 1. Supply of large-scale office buildings Supply of large-scale office space in 2017 in Tokyo’s 23 wards was 0.76 million square meters, falling short of the past 20-year average of 1.05 million square meters. Supply is projected to be 1.47 million square meters in 2018, 1 million square meters in 2019, and 1.73 million square meters in 2020. The last would mark the third-highest level in the past 20 years. A subsequent downturn is anticipated for the two years from 2021, as supply dips significantly below the past average. 2. -

Survey of Large Office Building Supply in the 23 Wards of Tokyo '07 Extremely Low Supply of Large-Scale Office Buildings

Survey of Large Office Building Supply in the 23 wards of Tokyo '07 April 4, 2007 We, Mori Trust Co., Ltd. (Head Office: Minato-ku, Tokyo), have since 1986 undertaken continuous field surveys and interviews concerning the implementation of plans for large-scale office building projects (total floor area: ten thousand square meters) within the 23 wards of Tokyo. Results of the most recent surveys and analysis are presented below. Where the survey considers multi-purpose buildings—buildings coupled with stores, residences, hotels, etc.—only the area purely for office use is assessed. [Survey Date: December 2006] Extremely Low Supply of Large-scale Office Buildings Until 2010 Main Results of This Survey 㪈㪅㩷Trends in Supply Volume: Average annual supply for 2007–2010 of 760,000 square meters, half the 2003–2006 level of 1.46 million square meters Since the supply boom of 2003, as a result of numerous very large-scale developments (on former JNR land, for example), the average annual supply for 2003–2006 reached 1.46 million square meters. As the majority of these developments were completed in 2006, average annual supply for 2007–2010 is predicted to drop to approximately half of that for 2003–2006, i.e., to 760,000 square meters. 㪉㪅㩷Trends in Supply Location: Supply in Chiyoda Ward for 2007–2010 stands out at 40% or more, with a distinct focus on the area around Tokyo Station. Moreover, active development of medium- and small-sized buildings is seen in the significantly integrated office-space area surrounding the business center. Looking at the supply area for 2007–2010, Chiyoda Ward stands out, accounting for 42% of total supply. -

Fabuleux Tokyo

Index 21_21 Design Sight 32 Dentsu 31 Diète nationale 33 A Drum Museum 26 Ad Museum 31 E Aida, Mitsuo 29 Akagi-jinja 44 Ebisu 41 Akasaka 31 Édifice Sompo Japan 8 Akihabara 46 Edo, ancien château d’ 27 Armani 30 Edo-Tôkyô Museum 45 Asahi 26 Étang de Shinobazu 24 Asakusa 25 Expo Nitten 32 Avenue Jizo dori 47 Avenue Kappabashi-dori 26 F Avenue Omotesandô 18 Fleuve Meguro 41 Avenue Takeshita 17 Fleuve Sumida 26, 35 Ayoama 17 Fuji TV 36 B Fukagawa Edo Museum 46 Brasserie française Paul Bocuse 32 G Bunkamura 16 Gare de Shinjuku 10 Bunkyô Civic Center 45 Gare de Tôkyô 29 C Ginza 30 Ginza Place 30 Café 1894 29 Golden-Gai 12 Capsule hotels 16 Caretta Shiodome 31 H Cathédrale Sainte-Marie de Tôkyô 39 Hanami 27 Cat Street 19 Harajuku 17 Center Gai 15 Hara Museum of Contemporary Art 41 Chien Hachikô 14 Heiseikan 20 Cimetière d’Aoyama 18 Hermès 30 Cimetière de Yanaka 24 Higashi Gyoen 27 Croisière 35 Hikarie 15 D Honkan 20 Horyuji 20 Daikanransha 37 Hôtel Park Hyatt 8 Daikanyama T-Site 41 Hôzô-mon 25 Daykanyama 41 Humax Pavilion 15 http://www.guidesulysse.com/catalogue/FicheProduit.aspx?isbn=9782765872658 I Miraikan 36 Mitsubishi Ichigokan Museum 29 Idemitsu Museum of Arts 28 Mitsui Memorial Museum 29 Ikebukuro 38 Mitsukoshi 30 Institute for Nature Study 42 Mode Gakuen Cocoon Tower 8 Intermediatheque 29 Mori Art Museum 31 Isetan 10 MOT 46 Ito Yokado 12 Musée Artizon 29 J Musée de sculptures Asakura Chôsokan 24 Jardin botanique Koishikawa Shokubut- Musée de Shitamachi 24 suen 45 Musée des sabres japonais 45 Jardin des pivoines 23 Musée Nezu 18 Jardin -

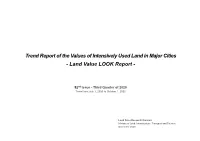

Land Value LOOK Report

Trend Report of the Values of Intensively Used Land in Major Cities - Land Value LOOK Report - 52nd Issue - Third Quarter of 2020 Trend from July 1, 2020 to October 1, 2020 Land Price Research Division Ministry of Land, Infrastructure, Transport and Tourism November 2020 Survey Outline 1. Survey objective To clarify those land value trends of intensively used districts in major cities on a quarterly basis, which tend to indicate property market trends leadingly. 2. Matters to be surveyed Licensed Real Property Appraisers (LRPAs) collect information on the real property markets of the surveyed districts, and estimate land value trends by using real property appraisal approaches to value. The results are to be aggregated by the Ministry of Land, Infrastructure, Transport and Tourism. 3. Surveyed districts Those districts in three major metropolitan areas (Tokyo, Osaka and Nagoya areas) and other major cities, land price trends of which are particularly important in the real property market. A total of 100 districts, including 43 districts in Tokyo area, 25 districts in Osaka area, 9 districts in Nagoya area, and 23 districts in other major cities, are surveyed. (See the attached sheet for the outlines of the districts.). Residential districts comprise of districts intensively used for high-rise apartments, etc. (32 districts). Commercial districts comprise of districts where shops and/or offices are intensively concentrated (68 districts). ※1. Tokyo Area = Saitama, Chiba, Tokyo, and Kanagawa Prefectures; Osaka Area = Kyoto, Osaka, Hyogo, -

Readings of the Third Fukushima Prefecture Environmental Radiation Monitoring in Mesh Survey (Definite Values)

Revised Readings of the Third Fukushima Prefecture Environmental Radiation Monitoring in Mesh Survey (Definite Values) May 21, 2012 Local Nuclear Emergency Response Headquarters (Radioactivity Team) Disaster Provision Main Office of Fukushima Pref. (Nuclear Power Team) The results of air dose rate monitoring based on “The Third Fukushima Prefecture Environmental Radioactivity Monitoring in Mesh Survey Action Plan,” issued on February 20, 2012, are as follows. 1 Monitoring Outline (1) Monitoring Date From Tuesday, February 21 to Friday, March 9, 2012 (2) Number of Monitoring Locations 2,675 locations (Locations monitored in the previous survey: 2,776) 2 Monitoring Results (1) Monitoring Results for this Report (Unit: μSv/h) Readings Readings Monitoring in the in the Segment Maximum value Minimum value locations second first survey survey 2.8 0.06 Date City/Ryozen Town Fukushima City/ 0.13 0.16 Kenpoku 379 Kamioguni Chabatake Tsuchiyuonsen Town Inokura to to (Reading in the previous Near the entrance of Skyline 4.3 4.4 survey of this location:3.0) Prefectural Road 30 1.0 Koriyama City/Daishin 2-chome (Reading in the previous survey of this location:1.0) 0.05 0.08 0.12 Kenchu 914 Miharu Town/Tomizawa Koriyama City/Banyushinden to to Sekita Ienomae 1.4 2.6 Near the starting point of Prefectural Road 119 (Reading in the previous survey of this location:1.1) 0.67 Shirakawa City/ 0.07 0.10 0.12 Kennan 277 Taishinkumado Kaketsuka Yamatsuri Town/Kamiseki to to (Reading in the previous Godo 1.2 1.8 survey of this location:1.2) 0.30 Aizumisato Town/Shimohori