Office Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Espersonespersonesperson 808 Travis Street & 815 Walker Avenue • Houston, Texas

THETHETHE ESPERSONESPERSONESPERSON 808 TRAVIS STREET & 815 WALKER AVENUE • HOUSTON, TEXAS EXECUTIVE SUMMARY THETHETHE ESPERSONESPERSONESPERSON 808 TRAVIS STREET & 815 WALKER AVENUE • HOUSTON, TEXAS HFF, as the exclusive representative of the owner, is pleased to offer for sale a 100% fee simple interest in Esperson (the “Property”), a 19 and 27-story, 599,107 square foot office building located in Houston’s central business district. Constructed in 1927 and 1941 respectively, Esperson is the only iconic structure of Italian Renaissance in Houston’s most densified employment center. The property is currently 62% leased with 4 years remaining average lease term and is situated on 1.447 acres, a full city block. Located at the intersection of Rusk and Walker Street, Esperson has direct access to Houston’s METRO Rail and 7.5 mile underground tunnel system. Over the last 36 months, ownership invested nearly $9 million in non-leasing capital, positioning the asset at the top of its competitive set. Today, considerable value creation is achievable through rolling current in-place rents to market and through the lease up of the remaining 226,561 square feet of vacant space. Redeveloping and expanding Houston’s CBD infrastructure – realized through rebuilt streets – highways, new mass transit and enhanced public utilities coupled with new office, multi-family, and retail projects have transformed Houston’s core into a vibrant, modern 24/7 environment for people to live, work and play. Esperson offers investors prestige, history, quality, abundant amenities, and a prime location in Houston’s largest employment center. INVESTMENT SALES H. DAN MILLER, CCIM, SIOR Senior Managing Director Tel: (713) 852-3576 [email protected] MARTIN T. -

Downtown Development Project List

DOWNTOWN DEVELOPMENT This list provides details on all public and private sector construction projects in Downtown Houston since 1995. Costs are estimated or otherwise not available. Under Construction Harris County Jury Assembly Plaza Reconstruction of the plaza and pavilion including relocation of electrical vault. Address 1210 Congress St. Developer Harris County Estimated cost $11.3 million Est. completion 3Q 2021 Website Harris County Clerk McKee City Living 4‐story, 120‐unit affordable‐workforce housing. Address 626 McKee St. Developer Gulf Coast Housing Partnership Estimated cost $29.9 million Est. completion 4Q 2021 Website McKee City Living UHD Student Wellness & Success 72,000 SF student fitness and recreation facility. Address 315 N Main St. Developer University of Houston Downtown Estimated cost $38 million Est. completion 2Q 2022 Website UHD Student Wellness & Success Center JPMorgan Chase & Co. Tower Reframing and renovations of the first and second floor lobbies, tunnel access and the exterior plaza. Address 600 Travis St. Developer Hines Estimated cost $2 million Est. completion 3Q 2021 Website JPMorgan Chase & Co Tower Frost Town Brewing Reframing and 9,100 SF brewing and taproom serving locally inspired beers Address 600 Travis St. Developer Hines Estimated cost $2.58 million Est. completion 3Q 2021 Website Frost Town Brewing Moxy Hotel by Marriott Redevelopment of the historic office building at 412 Main St. into a 13‐story, 119‐room hotel. Address 412 Main St. Developer InnJoy Hospitality Estimated cost $4.4 million P Est. completion 2Q 2022 Website Moxy Marriott Hotel V = Estimated using the Harris County Appriasal Distict public valuation data, January 2019 P = Estimated using the City of Houston's permitting and licensing data Updated 07/01/2021 Harris County Criminal Justice Center Improvement and flood damage mitigation of the basement and first floor. -

Center for Public History

Volume 8 • Number 2 • spriNg 2011 CENTER FOR PUBLIC HISTORY Oil and the Soul of Houston ast fall the Jung Center They measured success not in oil wells discovered, but in L sponsored a series of lectures the dignity of jobs well done, the strength of their families, and called “Energy and the Soul of the high school and even college graduations of their children. Houston.” My friend Beth Rob- They did not, of course, create philanthropic foundations, but ertson persuaded me that I had they did support their churches, unions, fraternal organiza- tions, and above all, their local schools. They contributed their something to say about energy, if own time and energies to the sort of things that built sturdy not Houston’s soul. We agreed to communities. As a boy, the ones that mattered most to me share the stage. were the great youth-league baseball fields our dads built and She reflected on the life of maintained. With their sweat they changed vacant lots into her grandfather, the wildcatter fields of dreams, where they coached us in the nuances of a Hugh Roy Cullen. I followed with thoughts about the life game they loved and in the work ethic needed later in life to of my father, petrochemical plant worker Woodrow Wilson move a step beyond the refineries. Pratt. Together we speculated on how our region’s soul—or My family was part of the mass migration to the facto- at least its spirit—had been shaped by its famous wildcat- ries on the Gulf Coast from East Texas, South Louisiana, ters’ quest for oil and the quest for upward mobility by the the Valley, northern Mexico, and other places too numerous hundreds of thousands of anonymous workers who migrat- to name. -

Major Lease Transactions Downtown Houston

MAJOR LEASE TRANSACTIONS DOWNTOWN HOUSTON This is a comprehensive list of publicly available leases in Downtown Houston, including new‐to‐Downtown, expansions and renewals. Year Company Type To From Square Feet 512,845 Enterprise Plaza 2020 Enterprise Products Partners Renewal (incl. 2019 (1100 Louisiana) expansion: 22,301) 2020 JP Morgan Chase New/Relocation 600 Travis 1111 Fannin 253,230 2020 EP Energy Relocation/Sublease 601 Travis 1001 Louisiana 62,261 5 Houston Center 2020 Venture Global LNG Renewal/Expansion 58,514 (1401 McKinney) (Expansion: 29,257 2020 Summit Midstream Partners, LP New to Downtown/Sublease 910 Louisiana The Woodlands 48,632 LyondellBasell Tower 2020 Mitsubishi International Corporation Renewal 45,838 (1221 McKinney) 2020 Indigo Minerals Renewal 600 Travis 45,125 Pennzoil Place – North Tower 2020 Cheniere Energy Expansion 33,127 (700 Milam) Texas Tower Wells Fargo Plaza 2020 DLA Piper Relocation/Expansion 31,843 (845 Texas) (1000 Louisiana) (Expansion: 6,836) Bank of America Tower 2020 Waste Management Expansion 31,750 (800 Capitol) USA: Office of the Comptroller and Fulbright Tower 2020 Renewal 27,223 Office of the Currency (1301 McKinney) 2020 Riviera Resources Relocation 717 Texas 600 Travis 27,114 One Allen Center 2020 TPC Group Renewal 24,803 (500 Dallas) Source: Central Houston, Inc. Updated 09-30--2020. 1 Year Company Type To From Square Feet Fulbright Tower 2020 AXIP Energy Services Renewal 24,657 (1301 McKinney) 2020 Chevron Expansion 1600 Smith 23,699 2020 Plains All American Refining, L.P. Expansion Three Allen Center (333 Clay) 23,172 2020 Momentum Midstream Renewal 600 Travis 22,575 2020 Lone Star Legal Aid Renewal 500 Jefferson 20,020 2020 Squire Patton Boggs Renewal 600 Travis 15,641 2 Houston Center 2020 USA: Office of the Comptroller Renewal 14,624 (909 Fannin) 2020 Rockcliff Energy, LLC Renewal 1301 McKinney 14,403 2020 Enbridge, Inc. -

Iconic Tower — Transformed for Today Rebuilding the Tenant Experience from the Ground Up

Iconic Tower — Transformed for Today Rebuilding the tenant experience from the ground up —————— —————— This landmark tower has been transformed A new freestanding restaurant with an engaging into a modern, sustainable, innovation hub to outdoor space will be ideal for activities; a new food support Houston’s leading creative companies — hall-style café on the ground level offers healthy designed to meet or exceed the demands and convenient menu options; new common-areas of a changing workforce, today and tomorrow. include a comfortable lobby lounge ideal for coffee, —————— connecting or disconnecting; plus access to a spa- Meticulously maintained and operated since styled fitness center featuring health and wellness this iconic property was first commissioned as activities for group or self-paced programs. a global corporate headquarters by a leading —————— energy company. 5555 San Felipe is owner-operated and —————— maintained with an eco-friendly and sustainable With a focus on helping modern organizations approach. Our award-winning project is LEED Gold inspire talent, every aspect of the renovation certified and participates in various campaigns delivers a more perfect balance between hospitality for recycling, conservation and green-building and workspace — from the arrival experience, to operations. At every level, our tenants and their three levels of new and enhanced amenities. satisfaction come first. Transformation —————— Everything your team needs to thrive M-M Properties set a vision of rebuilding the tenant experience from the ground up. There are new modern finishes, three full floors of curated amenities and light-filled spaces. There will also be a new, freestanding signature restaurant. 5555 San Felipe is an inspired and FREESTANDING RESTAURANT – ACTIVITY LAWN collaborative office environment — the destination workplace — for today’s valuable employees. -

Downtown Houston Development Continues Despite Covid-19

MEDIA CONTACTS Angie Bertinot / Central Houston [email protected] / 713-650-3022 Whitney Radley / The CKP Group [email protected] / 832-930-4065 x 106 FOR IMMEDIATE RELEASE JANUARY 19, 2021 DOWNTOWN HOUSTON DEVELOPMENT CONTINUES DESPITE COVID-19 More than $1.9 billion in construction projects currently underway with more on the horizon HOUSTON, TX — While the Greater Houston Area begins to recover from the COVID-19 pandemic, Downtown Houston has shown its trademark resilience and grit in the face of the unexpected. Over the past year, office employees have adapted to working from home, hospitality groups have rolled out new services options and staycations, residential properties have adopted technology to conduct virtual space tours and the construction sector has continued grow. More than $1.9 billion in construction projects are currently underway in Downtown Houston, an area defined by IH-45 to the west and south, Highway 59 to the east and IH-10 to the north. “In recent years, Downtown Houston has transitioned from a central business district to a prime destination to live, work, play and stay,” said Bob Eury, president and CEO of the Houston Downtown Management District. “While the pandemic has resulted in some set- backs, we’re seeing confidence in the market: businesses and office employees have adapted to the new normal with agility, developers are leveraging the opportunity to maximize construction across all sectors and the area remains a culinary and cultural destination for Houstonians and visitors.” Office Projects Downtown Houston remains a dynamic business center with a workforce of approximately 158,000 employees and more than 51 million square feet of office space. -

Houstonhouston

RealReal EstateEstate MarketMarket OverviewOverview HoustonHouston Jennifer S. Cowley Assistant Research Scientist Texas A&M University July 2001 © 2001, Real Estate Center. All rights reserved. RealReal EstateEstate MarketMarket OverviewOverview HoustonHouston Contents 2 Note Population 6 Employment 9 Job Market 10 Major Industries 11 Business Climate 13 Public Facilities 14 Transportation and Infrastructure Issues 16 Urban Growth Patterns Map 1. Growth Areas Education 18 Housing 23 Multifamily 25 Map 2. Multifamily Building Permits 26 Manufactured Housing Seniors Housing 27 Retail Market 29 Map 3. Retail Building Permits 30 Office Market Map 4. Office Building Permits 33 Industrial Market Map 5. Industrial Building Permits 35 Conclusion RealReal EstateEstate MarketMarket OverviewOverview HoustonHouston Jennifer S. Cowley Assistant Research Scientist Aldine Jersey Village US Hwy 59 US Hwy 290 Interstate 45 Sheldon US Hwy 90 Spring Valley Channelview Interstate 10 Piney Point Village Houston Galena Park Bellaire US Hwy 59 Deer Park Loop 610 Pasadena US Hwy 90 Stafford Sugar Land Beltway 8 Brookside Village Area Cities and Towns Counties Land Area of Houston MSA Baytown La Porte Chambers 5,995 square miles Bellaire Missouri City Fort Bend Conroe Pasadena Harris Population Density (2000) Liberty Deer Park Richmond 697 people per square mile Galena Park Rosenberg Montgomery Houston Stafford Waller Humble Sugar Land Katy West University Place ouston, a vibrant metropolitan City Business Journals. The city had a growing rapidly. In 2000, Houston was community, is Texas’ largest population of 44,633 in 1900, growing ranked the most popular U.S. city for Hcity. Houston was the fastest to almost two million in 2000. More employee relocations according to a growing city in the United States in the than four million people live in the study by Cendant Mobility. -

Houston's Office Market Weakens Over the Quarter and Braces Itself Moving

Research & Forecast Report HOUSTON | OFFICE Q1 2020 Houston’s office market weakens over the quarter and braces itself moving forward amid $20 oil Lisa Bridges Director of Market Research | Houston Commentary by Patrick Duffy MCR Market Indicators Annual Quarterly Quarterly Colliers generally uses this space to discuss the trends we see Relative to prior period Change Change Forecast* in market data and in conversations we have with our clients, prospects and friendly competitors. We take that data and attempt VACANCY to project activity going forward. The bulk of the first quarter was, NET ABSORPTION for all practical purposes, pre-COVID. Net “move-in” data, as well as new leases signed, were likely unimpacted for Q1 based on the DELIVERIES virus or only marginally impacted. Our industry has a lead time of UNDER CONSTRUCTION at least 4-6 months before a lease is signed or space made ready for occupancy. The real impact of this COVID crisis will not present *Projected in the data until later in Q2. Inertia will carry us for a few more weeks. The world is focused on the COVID driven economic slowdown. Houston has two issues to watch – COVID and a collapse in oil prices. The oil issue is driven by Saudi Arabia and Russia failing to reach an agreement on production and by the severe decline of oil and gas demand driven by the COVID shutdown. Oil has been Summary Statistics Houston Office Market Q1 2019 Q4 2019 Q1 2020 in the low 20’s since the collision of these two events. The Energy Information Administration is projecting that supply will continue to Vacancy Rate 19.4% 19.8% 20.0% outpace demand for the balance of this year by approximately 10MM barrels per day. -

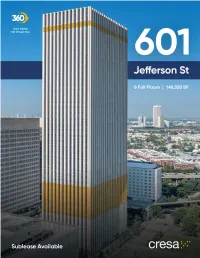

Click Above for Virtual Tour Sublease 601 Jefferson St

Click Above For Virtual Tour Sublease 601 Jefferson St Long-Term Sublease With the remaining term running through June 2030, enjoy peace of mind and long-term savings by locking in below market rents for years to come. Plug & Play Opportunity All floors are fully furnished and ready for occupancy, including Haworth cubicles and office furniture, as well as completely outfitted conference and break rooms. Up To Nearly 150,000 Total SF Available Great Panoramic Views of Downtown DIRTT Walls Quickly tailor your space to your business’ needs Available For Immediate Occupancy by reconfiguring the installed DIRTT Wall offices and conference rooms. Contact Broker For Rate Information For More Information Gary Lawless | 713.491.6307 | [email protected] Samuel Heiber | 202.783.3889 | [email protected] Sublease At-A-Glance Jefferson Towers 6 360+ At Cullen Center Floors Available Building Conference Center Capacity Tunnel Connectivity 88 Enjoy access via skywalk to 1600 Smith St to Houston‘s famed downtown tunnel system offering a wide range of (Very Walkable) retail and dining options all while remaining under protection Walk Score from any inclement weather on the surface level. On-site food court, Frost Bank, Amazon Locker and full-service post office. 1.50/1,000 Thru June 2030 Parking Ratio 25,000 SF Approximate Typical Floor Plate Long-term sublease opportunity 150K SF Building Security Up to nearly 150,000 SF available in total, A robust on-site with more than 123,000 SF contiguous. Great Access security system, including key card 601 Jefferson provides convenient access in and elevators, helps out of downtown via I-10, I-45 and Hwy 59, as well as manage and control Click the icon to the right to get a by Metro‘s bus and light rail transit services. -

1010 Lamar for Lease Houston, Texas

OFFICE SPACE 1010 LAMAR FOR LEASE HOUSTON, TEXAS » 5% Broker Incentive for 3,000 RSF or more with a 5-Year Lease* » $25.00 per RSF tenant improvement allowance for 5+ year lease* » Up to 6 months unreserved abated parking on a 5-year lease term* * NEW LEASES ONLY FOR LEASING INFORMATION, CONTACT: COURTNEY BUCKOUT MIKE MARTIN 713.209.5959 713.209.5710 [email protected] [email protected] 1010 LAMAR HOUSTON, TEXAS BUILDING AMENITIES & FEATURES • 19-story office building located in the • Conveniently located, with easy Houston CBD access to Discovery Green and other neighboring amenities • Million dollar elevator modernization - Phase One delivery - March 2017 • Tunnel access • New 24/7 garage access control system • Across the street from the Metro Rail • New Common area upgrades • Card key access system • 2:1000; Attached parking garage • On-site management • 702 RSF - 3,000 RSF spec suites • On-site courtesy guard • Adjacent to GreenStreet is a 570,000 • 6,900 SF fully-networked auditorium/ square foot mixed-use destination conference facility featuring three-city blocks of premier shopping, dining and entertainment destinations AVAILABLE SPACE SUITE SQ. FT. SUITE SQ. FT. 670 3,310 1111 6,482 750 3,525 1200 2,831- 14,328 840 702 1300 6,016 910 1,144 1450 1,821- 14,314 950 3,623 1520 1,386 1000 5,161 1610 4,830 1005 2,561 T-30 6,065 1010 LAMAR HOUSTON, TEXAS 1010 LAMAR HOUSTON, TEXAS Park XAS AVE T E XAS AVE Great TE JP Morgan Keystone Lofts Inn at Annunci ation JP Morgan 808 Federal Southwest Parking Bayou Site MapJones - Downtown,Chase HoustonChase FTXannin Magnolia theLocatedChurch across from the Metro Rail Plaza Jones Tower Detention Life Incarnate Place Hall Center Center Lawyer ParkingBallpark Word SWB Title Academy JP Morgan C AP ITOL S T Chase St. -

GULF COAST SECTION NEWSLETTER Gulf Coast Section

MAY 2012 GULF COAST SECTION NEWSLETTER Gulf Coast Section General Meeting: Shale Gas, Emerging Fundamentals & Geopolitics Reservoir Technology Symposium May 11, 2012 Oil Patch Orientation May 9, 2012 Annual Awards Banquet May 23, 2012 XXXXXXXX: XXXXXXX CHAIRMAN’S CORNER Reservations & Information For all SPE GCS topical luncheons and social activities, by Hiep Vu, Shell please register online at www.spegcs.org. You must 2011-12 SPE GCS Chair provide your SPE member number to receive member prices. Guests who have not made a reservation online will be charged an additional amount at the door. Walk-ins are not guaranteed admittance. Respecting our Past, Honoring our Present, • Reservations and cancellations required for all events. and Building for our Future • No-shows will be billed. • Walk-ins will be charged extra. This month, the Gulf Coast Section will Mastercard, Visa, American Express, Discover, and Diner’s be hosting a celebration to recognize the Club are accepted for advance reservations only. The technical achievements of its past, current, and future and other opinions expressed by speakers at the Gulf Coast members at the annual Awards Banquet. The Section meetings may not have been reviewed by SPE and do not necessarily reflect the position of SPE, the Gulf Coast evening reception will be held at the historic Rice Section, its officers, or members. The only forum for rebuttal Hotel in downtown Houston. Marc Vandermeer, and discussion is during the meeting. better known as the Voice of the Houston Texans, will once again be on hand to provide SPE Houston Office us a good, lively show with his entertaining dialogue as emcee for the Gulf Coast Section Administrator banquet. -

Allen Center

Rebirth of Downtown The rebirth of downtown Houston as an attractive living, lodging, dining and entertainment destination coupled with existing daytime population presents the opportunity to provide a true sense of place. Houston’s THE WOODLANDS Core The Heights 5 min. KINGWOOD TOMBALL SPRING River Oaks 10 min. ATSCOCITA West University Place 11 min. 290 HUMBLE Memorial 15 min. WILLOWBROOK 59 CYPRESS 90 The Galleria 16 min. 6 Tanglewood 19 min. IAH 99 45 The Medical Center 19 min. Hobby Airport 23 min. 290 59 90 George Bush Intercontinental 27 m i n. THE Airport (IAH) HEIGHTS 10 KATY MEMORIAL 610 10 Sugar Land 28 min. TANGLEWOOD RIVER DOWNTOWN THE OAKS GALLERIA Port of Houston 30 min. WEST UNIVERSITY THE PLACE MEDICAL PORT OF CENTER HOUSTON 610 Baybrook 30 min. 59 Trinity Bay Katy 33 min. 99 HOBBY AIRPORT 90 Cypress 36 min. 45 Galveston Bay The Woodlands 37 min. 288 SUGAR LAND BAYBROOK 59 6 PEARLAND Kingwood 37 min. Downtown by the numbers 66,838 158,000 27 residents currently employees work Hotels live downtown downtown 11 1,779 new residential units 220,000 million people attend downtown planned or under people visit Houston culture and construction downtown on entertainment attractions a daily basis annually 1.2 51.4 1.2 million 8,228 150 million million people stay in hotel rooms new hotel SF of SF of office downtown Houston rooms under existing under hotels annually construction office space construction MAJOR EMPLOYERS Elysian Viaduct Sterrett William Street 1318 Studios RicheyNance McKee William Street Lofts Sterrett Walnut Sterrett Dakota Street Lofts Townhomes N.