A Study of Alternative and Fintech Payment Solutions for Airlines Submitted 15/08/19, 1St Revision 21/09/19, 2Nd Revision 18/10/19, Accepted 27/11/19

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

356 Partners Found. Check If Available in Your Market

367 partners found. Check if available in your market. Please always use Quick Check on www.hahnair.com/quickcheck prior to ticketing P4 Air Peace BG Biman Bangladesh Airl… T3 Eastern Airways 7C Jeju Air HR-169 HC Air Senegal NT Binter Canarias MS Egypt Air JQ Jetstar Airways A3 Aegean Airlines JU Air Serbia 0B Blue Air LY EL AL Israel Airlines 3K Jetstar Asia EI Aer Lingus HM Air Seychelles BV Blue Panorama Airlines EK Emirates GK Jetstar Japan AR Aerolineas Argentinas VT Air Tahiti OB Boliviana de Aviación E7 Equaflight BL Jetstar Pacific Airlines VW Aeromar TN Air Tahiti Nui TF Braathens Regional Av… ET Ethiopian Airlines 3J Jubba Airways AM Aeromexico NF Air Vanuatu 1X Branson AirExpress EY Etihad Airways HO Juneyao Airlines AW Africa World Airlines UM Air Zimbabwe SN Brussels Airlines 9F Eurostar RQ Kam Air 8U Afriqiyah Airways SB Aircalin FB Bulgaria Air BR EVA Air KQ Kenya Airways AH Air Algerie TL Airnorth VR Cabo Verde Airlines FN fastjet KE Korean Air 3S Air Antilles AS Alaska Airlines MO Calm Air FJ Fiji Airways KU Kuwait Airways KC Air Astana AZ Alitalia QC Camair-Co AY Finnair B0 La Compagnie UU Air Austral NH All Nippon Airways KR Cambodia Airways FZ flydubai LQ Lanmei Airlines BT Air Baltic Corporation Z8 Amaszonas K6 Cambodia Angkor Air XY flynas QV Lao Airlines KF Air Belgium Z7 Amaszonas Uruguay 9K Cape Air 5F FlyOne LA LATAM Airlines BP Air Botswana IZ Arkia Israel Airlines BW Caribbean Airlines FA FlySafair JJ LATAM Airlines Brasil 2J Air Burkina OZ Asiana Airlines KA Cathay Dragon GA Garuda Indonesia XL LATAM Airlines -

State and Airline Response to COVID-19. 04 May 2020 Airline Announcement Share Flights 2019 2/5/20 Aer Lingus See IAG

State and Airline Response to COVID-19. 04 May 2020 Airline Announcement Share Flights 2019 2/5/20 Aer Lingus See IAG. Plan to cut workforce by 20% [1/5]. 0.8% -91% Air Dolomiti Suspended flights (18/3–17/5). Some repatriation flights [2/4]. 0.2% Air France Flight capacity cut by 90% from 23/3 until end May [10/4]. State aid granted with commitment to reduce CO2 3.2% -97% emissions of domestic flights by 50% by 2024 [24/4]. All A380 grounded [16/3]. A ‘best case’ could be 30% of 2019 during July, but social distancing challenges [20/4]. Progressive pax domestic flights restart from 11 May [26/4]. Air Malta Suspended flights from 25/3 (until further notice) with exceptions [18/3]. Will lay off 80% of pilots (21/4). 0.2% Air Moldova Suspended flights (25/3–15/5) [26/3]. 0.1% Air Serbia Suspended passenger transport (19/3–30/4 or later) (see Serbia). State aid granted [27/4] 0.3% airBaltic Suspended flights (17/3–12/5). Flight capacity reduced by 50% 15/4-30/10 [3/4] (see Latvia). Accelerated fleet 0.6% transformation (A220-only) [22/4]. Some pax flights may resume 13/5 [28/4] Alitalia Nationalised [17/3] to resume ops with ~80% of current fleet [23/4]. Reimbursement or exchange of tickets booked 1.9% -89% until 31 May proposed [20/3]. Cargo flights to/from China extended until 11/5 [30/4]. Austrian Airlines Suspended flights (19/3–31/5) [29/4]. Expects 25%-50% of demand for Summer (vs S19). -

Global Volatility Steadies the Climb

WORLD AIRLINER CENSUS Global volatility steadies the climb Cirium Fleet Forecast’s latest outlook sees heady growth settling down to trend levels, with economic slowdown, rising oil prices and production rate challenges as factors Narrowbodies including A321neo will dominate deliveries over 2019-2038 Airbus DAN THISDELL & CHRIS SEYMOUR LONDON commercial jets and turboprops across most spiking above $100/barrel in mid-2014, the sectors has come down from a run of heady Brent Crude benchmark declined rapidly to a nybody who has been watching growth years, slowdown in this context should January 2016 low in the mid-$30s; the subse- the news for the past year cannot be read as a return to longer-term averages. In quent upturn peaked in the $80s a year ago. have missed some recurring head- other words, in commercial aviation, slow- Following a long dip during the second half Alines. In no particular order: US- down is still a long way from downturn. of 2018, oil has this year recovered to the China trade war, potential US-Iran hot war, And, Cirium observes, “a slowdown in high-$60s prevailing in July. US-Mexico trade tension, US-Europe trade growth rates should not be a surprise”. Eco- tension, interest rates rising, Chinese growth nomic indicators are showing “consistent de- RECESSION WORRIES stumbling, Europe facing populist backlash, cline” in all major regions, and the World What comes next is anybody’s guess, but it is longest economic recovery in history, US- Trade Organization’s global trade outlook is at worth noting that the sharp drop in prices that Canada commerce friction, bond and equity its weakest since 2010. -

Monthly OTP November 2019

Monthly OTP November 2019 ON-TIME PERFORMANCE AIRLINES Contents On-Time is percentage of flights that depart or arrive within 15 minutes of schedule. Global OTP rankings are only assigned to all Airlines/Airports where OAG has status coverage for at least 80% of the scheduled flights. Regional Airlines Status coverage will only be based on actual gate times rather than estimated times. This may result in some airlines / airports being excluded from this report. If you would like to review your flight status feed with OAG, please email [email protected] MAKE SMARTER MOVES Airline Monthly OTP – November 2019 Page 1 of 1 Home GLOBAL AIRLINES – TOP 50 AND BOTTOM 50 TOP AIRLINE ON-TIME FLIGHTS On-time performance BOTTOM AIRLINE ON-TIME FLIGHTS On-time performance Airline Arrivals Rank No. flights Size Airline Arrivals Rank No. flights Size JH Fuji Dream Airlines 96.5% 1 2,340 155 3H Air Inuit 37.2% 162 1,465 196 GA Garuda Indonesia 95.8% 2 12,736 48 AI Air India 40.1% 161 16,509 38 RC Atlantic Airways Faroe Islands 95.0% 3 210 295 WG Sunwing Airlines Inc. 50.3% 160 905 225 7G Star Flyer 94.0% 4 2,160 164 WO Swoop 53.4% 159 919 222 EW Eurowings 93.4% 5 15,608 40 SG SpiceJet 54.3% 158 18,288 33 SATA International-Azores 6J Solaseed 93.3% 6 2,226 161 S4 54.5% 157 448 260 Airlines S.A. XQ SunExpress 93.3% 7 3,115 135 IW Wings Air 54.7% 156 11,242 55 TA TACA International Airlines 92.8% 8 374 272 JY Intercaribbean Airways Ltd 56.1% 155 1,760 184 FA Safair 92.6% 9 2,250 159 JT Lion Air 58.0% 154 17,320 34 B7 Uni Airways 92.5% 10 4,132 123 BJ Nouvelair -

EMPIRICAL VALIDATION of BLUE OCEAN STRATEGY SUSTAINABILITY in an INTERNATIONAL ENVIRONMENT Jiri DVORAK*, Ilona RAZOVA

Foundations of Management, Vol. 10 (2018), ISSN 2080-7279 DOI: 10.2478/fman-2018-0012 143 EMPIRICAL VALIDATION OF BLUE OCEAN STRATEGY SUSTAINABILITY IN AN INTERNATIONAL ENVIRONMENT Jiri DVORAK*, Ilona RAZOVA** University of Economics, Prague, Jindrichuv Hradec, CZECH REPUBLIC * e-mail: [email protected] ** e-mail: [email protected] Abstract: This article investigates the applicability of blue ocean strategy in regard to low-cost airlines in the civil airline industry. To do so, the commercial offers of selected airlines were compared to vali- date any attempts to apply the blue ocean strategy concept. This is followed by examining the time lim- itation of the concept in a competitive environment and is illustrated by the changes in the industry for the past 30 years and a comparison of offers from similar companies. The third issue is the evalua- tion of the further contribution of blue ocean strategy when it is recognized as time-limited. The im- portance of first-mover advantage, which could be based on the ability to capture an economy of scale and advantageously shape the market, is also discussed. Keywords: blue ocean strategy, civil airliners, competitiveness, low-cost strategy, first-mover ad- vantage, Ryanair, customer value, value curve. JEL: M16, L10, L21. 1 Introduction Bonsor, 2001; Doganis, 2006). In Europe, the situa- tion began to change with the emergence of Ryanair Air transport experienced dynamic growth in the in 1985 when it entered the European market with second half of the twentieth century, which contin- a low-cost airline concept (Barrett, 2004; Thomas, ued into the early twenty-first century and still re- 2013; Ryanair, 2015a). -

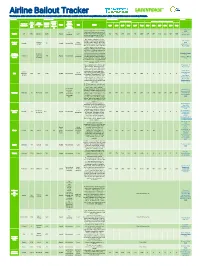

European Airline Bailout Tracker Reflects the Most up to Date Public Information Available at the Time It Was Published on June 9, 2021

Airline Bailout Tracker This European airline bailout tracker reflects the most up to date public information available at the time it was published on June 9, 2021. Financial data based on research by Profundo. Company Bailout amount Financial results Sources Amount Binding Net profits (mln €) Dividends + share buybacks (mln €) 2018 Airline/ Amount (mln €) - climate Country of Passen subsidiarie (mln €) - Under Status conditions Type Details registration gers 2019 2018 2017 2016 2015 Total 2019 2018 2017 2016 2015 Total (mln) s Agreed discussi Private on dividend ban Guardian, 6 April An initial government loan of GBP 2020 600m (ca €670m) was provided at No Reuters, 11 EasyJet UK 88.5 EasyJet 2240 Agreed Loan the start of the crisis, followed with a 393 402 246 505 742 2288 214 281 195 272 421 1383 dividends January 2021 government backed loan of GBP 1,4 bn (ca €1,570m) in January 2021. One-quarter of Norway’s rescue package for airlines (loan guarantee e24, 20 April Regional Regional Loan of NOK 6 billion ($549 million)) will 2020 Norway 121 Agreed No condition - - - - - - - - - - - - carriers carriers guarantee be divided between Widerøe, which Aeronautics, 20 offers key regional service, and other March 2020 small regional airline operators. Total pot of €455m has been made available to all airlines registered in Sweden. SAS has been loaned €137m and that has been deducted Euractiv, 13 April All airlines All airlines Loan from this amount and included in the 2020 operating in Sweden operating 318 Agreed No condition - - - - - - - - - - - - guarantee overall support provided to SAS by Finans, 17 March Sweden in Sweden Sweden and other countries, detailed 2020 the row below. -

Family Friendly Airline List

Family Friendly airline list Over 50 airlines officially approve the BedBox™! Below is a list of family friendly airlines, where you may use the BedBox™ sleeping function. The BedBox™ has been thoroughly assessed and approved by many major airlines. Airlines such as Singapore Airlines and Cathay Pacific are also selling the BedBox™. Many airlines do not have a specific policy towards personal comforts devices like the BedBox™, but still allow its use. Therefore, we continuously aim to keep this list up to date, based on user feedback, our knowledge, and our communication with the relevant airline. Aeromexico Japan Airlines - JAL Air Arabia Maroc Jet Airways Air Asia Jet Time Air Asia X Air Austral JetBlue Air Baltic Kenya Airways Air Belgium KLM Air Calin Kuwait Airways Air Caraibes La Compagnie Air China LATAM Air Europa LEVEL Air India Lion Airlines Air India Express LOT Polish Airlines Air Italy Luxair Air Malta Malaysia Airlines Air Mauritius Malindo Air Serbia Middle East Airlines Air Tahiti Nui Nok Air Air Transat Nordwind Airlines Air Vanuatu Norwegian Alaska Airlines Oman Air Alitalia OpenSkies Allegiant Pakistan International Airlines Alliance Airlines Peach Aviation American Airlines LOT Polish Airlines ANA - Air Japan Porter AtlasGlobal Regional Express Avianca Royal Air Maroc Azerbaijan Hava Yollary Royal Brunei AZUL Brazilian Airlines Royal Jordanian Bangkok Airways Ryanair Blue Air S7 Airlines Bmi regional SAS Brussels Airlines Saudia Cathay Dragon Scoot Cathay Pacific Silk Air CEBU Pacific Air Singapore Airlines China Airlines -

ANC PFC 4Th Quarterly Report Ending June 30, 2016(Revised 6.27.16)

PFC Quarterly Report - Receipts Collected For the Quarter Ended June 30, 2016 (Application No. 2) Application #05-02-C-00-ANC $14,000,000.00 Application #05-02-C-01-ANC 71,000,000.00 Total Collection Authority $85,000,000.00 PFC Revenue Received Air Carriers Current Quarter Previous Quarters Cumulative Aer Lingus - $ 141.61 $ 141.61 Aeroflot Russian Airline 49.13 508.31 557.44 Aerolane Lineas Aereas Nacionale - 112.71 112.71 Aero Mexico 387.26 2,696.37 3,083.63 Aerovias De Mexico - 20.23 20.23 Air Canada 11,274.61 405,320.53 416,595.14 Air France 401.30 11,902.66 12,303.96 Air New Zealand 115.60 5,266.68 5,382.28 Air Pacific Limited DBA Fiji Airways 95.37 1,202.24 1,297.61 Air Tahiti - 31.79 31.79 Alaska Airlines 646,271.14 28,122,906.23 28,769,177.37 Alitalia Airlines 20.23 317.90 338.13 Alitalia Societa Aerea Italiana S.P.A. - 8.67 8.67 All Nippon Airways Co 97.82 1,793.37 1,891.19 Aloha Airlines - 86.37 86.37 America West Airlines - 180,410.15 180,410.15 American Airlines 69,683.59 1,327,871.60 1,397,555.19 American Trans Air - 459.07 459.07 Asiana Airlines 892.13 33,678.54 34,570.67 Austrian Airlines 26.01 1,747.66 1,773.67 Aviacion Commercial Del America - 5.78 5.78 Avianca 156.06 685.94 842.00 Big Sky Airlines - 20.23 20.23 British Airways 440.63 15,943.76 16,384.39 Brussels - 147.39 147.39 Cape Air - 40.46 40.46 Cape Smythe Air Service, Inc - 8.67 8.67 Cathay Pacific Airways 171.82 9,590.47 9,762.29 Champion Air - 274.55 274.55 China Airlines 398.82 153,861.82 154,260.64 Compania Panamena De Aviacion 60.69 511.53 572.22 Condor Flugdienst, GMBH 13,338.32 316,967.38 330,305.70 Continental Airlines - 1,645,749.29 1,645,749.29 Corvus Airline 1,427.64 55,112.30 56,539.94 Czech Airlines - 164.73 164.73 Delta Airlines 222,216.59 4,548,134.66 4,770,351.25 Elal Israel Airlines - 242.76 242.76 Emirates 1,263.71 10,775.16 12,038.87 Etihad Airways- 2.89 2.89 Eva Airways Corp 1,835.15 17,383.35 19,218.50 Finnair - 112.71 112.71 Frontier Airlines, Inc. -

An Optimization Modelling to Evaluate Flights Scheduling at Tourist Airports Dimitrios J

World Academy of Science, Engineering and Technology International Journal of Industrial and Systems Engineering Vol:11, No:11, 2017 An Optimization Modelling to Evaluate Flights Scheduling at Tourist Airports Dimitrios J. Dimitriou 3.4% of global GDP. This continuing trend of air traffic Abstract—Airport’s serving a tourist destination are an essential growth has, however, not been matched by an adequate counterpart of the tourist demand supply chain, and their productivity expansion of air transport infrastructure, and the aviation is related to the region’s attractiveness and is enhanced by the air industry is facing the challenge of dealing with a range of transport business. In this paper, the evaluation framework of the congestion problems [5]. scheduled flights between two tourist airports is taken into consideration. By adopting a systemic approach, the arrivals from an Especially for Mediterranean countries, air transport for airport that its connectivity heavily depended on the departures of leisure purposes is the most important enabler to achieving another major airport are reviewed. The methodology framework, economic growth and development. Air transport facilitates based on inventory control theory and the numerical example, integration into the economy and provides vital connectivity promotes the use of the modelling formulation. The results would be on a national, regional, and international scale between essential for comparison and exercising to other similar cases. countries, promoting tourism growth, and creating employment opportunities in tourist destinations. Keywords—Airport connectivity, inventory control, optimization, optimum allocation. II. AIR CONNECTIVITY IN TOURIST REGIONS I. INTRODUCTION The link between tourism and the aviation industry is on the IR connectivity, especially for south European countries, top of the agenda for many academic institutes, professional Aplays an important role in regional and economic bodies and regulatory authorities. -

Fly America/Open Skies Partnership Frequently Asked Questions

FLY AMERICA/OPEN SKIES PARTNERSHIP FREQUENTLY ASKED QUESTIONS WHAT IS THE FLY AMERICA ACT? The Fly America Act (49 U.S.C. 40118) generally provides that foreign air travel funded by Federal Government money may only be conducted on United States (U.S.) air carriers. Airline tickets for grantees traveling on federal funds must be ticketed with a U.S. flag carrier code. It is understood that U.S. flag carriers are not always available to the final destination; however, a U.S. flag carrier must be used to the furthest destination possible. Additionally, a grantee must fly on a U.S. airline even if a foreign airline would be less expensive, provide preferred routing, or be more convenient. There also are exceptions to the Act, in which federal funding could be used for non-U.S. carriers (see below). WHAT IS CODE SHARING AND HOW DOES FLY AMERICA APPLY? “Code sharing” is when a ticket is issued by one airline but operated by another. When a U.S. flag carrier leases seats on a foreign carrier and the ticketing code is from the U.S. airline, it meets the Fly America Act requirements. For example, on a flight from San Francisco, California, to Hong Kong on the same Cathay Pacific Airways flight: • American Airlines flight 6117 (ticketed as AA6117) is considered a U.S. carrier; • Cathay Pacific Airways flight 873 (ticketed as CX873) is not considered a U.S. carrier. ARE THERE ANY EXCEPTIONS TO THE FLY AMERICA ACT? Federal Travel Regulation allows for limited exceptions to Fly America Act and a non-U.S. -

Monthly OTP September 2019

Monthly OTP September 2019 ON-TIME PERFORMANCE AIRLINES Contents On-Time is percentage of flights that depart or arrive within 15 minutes of schedule. Global OTP rankings are only assigned to all Airlines/Airports where OAG has status coverage for at least 80% of the scheduled flights. Regional Airlines Status coverage will only be based on actual gate times rather than estimated times. This may result in some airlines / airports being excluded from this report. If you would like to review your flight status feed with OAG, please email [email protected] MAKE SMARTER MOVES Airline Monthly OTP – September 2019 Page 1 of 1 Home GLOBAL AIRLINES – TOP 50 AND BOTTOM 50 TOP AIRLINE ON-TIME FLIGHTS On-time performance BOTTOM AIRLINE ON-TIME FLIGHTS On-time performance Airline Arrivals Rank No. flights Size Airline Arrivals Rank No. flights Size FA Safair 95.8% 1 2,180 175 JP Adria Airways 44.6% 166 1,458 206 TA TACA International Airlines 95.0% 2 399 277 AI Air India 53.3% 165 15,436 45 SATA International-Azores GA Garuda Indonesia 94.7% 3 12,582 53 S4 53.4% 164 733 255 Airlines S.A. XL LATAM Airlines Ecuador 94.7% 4 860 241 OK Czech Airlines 53.5% 163 2,363 165 CM Copa Airlines 93.8% 5 9,818 72 TP TAP Air Portugal 53.6% 162 12,434 55 FJ Fiji Airways 91.6% 6 1,943 186 IW Wings Air 55.2% 161 11,222 60 4M LATAM Airlines Argentina 91.5% 7 60 325 JY Intercaribbean Airways Ltd 55.2% 160 1,677 197 HD AirDo 90.6% 8 1,748 191 3H Air Inuit 56.9% 159 1,473 205 HA Hawaiian Airlines 89.7% 9 7,382 86 MT Thomas Cook Airlines 57.1% 158 3,959 132 7G Star Flyer 89.5% 10 1,980 183 BJ Nouvelair 60.1% 157 977 232 SU Aeroflot Russian Airlines 89.2% 11 31,270 19 WG Sunwing Airlines Inc. -

State and Airline Response to COVID-19. 30 March 2020

State and Airline Response to COVID-19. 30 March 2020 Airline Announcement Flight share 2019 Aer Lingus See IAG. Reportedly stopping flights to Spain (21 March). 0.8% Air Dolomiti Suspended flights 18 March to 19 April. Daily Milan-Frankfurt flight (23 March). 0.2% Air France Flight capacity cut by 90% from 23 March, for two months [20 March]. 3.2% Nationalisation proposed [18 March]. All A380 grounded [16 March]. Air Malta Suspended flights from 25 March (until further notice), exception for cargo, 0.2% humanitarian and repatriation or special flights [18 March]. Air Moldova Suspended flights from 25 March to 15 May [26 March]. 0.1% airBaltic Suspended flights 17 March to 14 April (see Latvia). 0.6% Alitalia Flight currently down by 84% (27 March ECTRL stats). Nationalised [17 March]. 1.9% Austrian Airlines Suspended flights from 19 March to 19 April [23 March]. 1.4% Blue Air Suspended flights from 21 March. 0.3% British Airways (BAW/SHT/CFE) See IAG. 3.0% Brussels Airlines Suspended flights from 21 March to 19 April [17 March]. 0.8% Croatia Airlines One daily return Zagreb-Frankfurt flight 15-24 March [21 March]. Dubrovnik airport 0.3% closed to 29 March [19 March]. Suspended flights to Croatian coast [15 March]. Czech Airlines Suspended flights from 16 March to 11 April. 0.3% easyJet (EZY/EJU/EZS) Suspended flights, “no visibility” on restart (30 March). 6.2% El Al Suspends all flights departing Israel from 27 March - 4 April (except cargo and 0.1% essential flights) [28 March]. Eurowings Basic flight supply from Düsseldorf, Hamburg, Stuttgart and Cologne [20 March].