Eros International (EROINT) | 165 Target : | 190 Target Period : 12 Months Potential Upside : 15% Strong Content Pipeline in FY18E…

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Top 100 Hindi Comedy Movies of All Time

Top 100 Hindi Comedy Movies Of All Time 1. 3 Idiots 51. Half Ticket 2. Ajab Prem Ki Ghajab 52. Haseena Man Jayegi Kahaani 53. Hera Pheri 3. All the Best 54. Hero No 4. Andaaj Apna Apna 55. Hey Baby 5. Angoor 56. Housefull/Housefull 2 6. Atithi Tum Kab Jaoge? 57. Hum Hai Kamal Ke 7. Auntie No 58. Hungama 8. Baaiton Baation mein 59. Ishq 9. Baap Numbri Beta Dus 60. Jaane Bhi Do Yaaro Numbri 61. Jab We Met 10. Bade Miyan Chote Miyan 62. Jodi No 11. Badshah 63. Jolly LLB 12. Barfi! 64. Judwa 13. Bawarchi 65. Khatha Meetha (New) 14. Bhagam Bhaag 66. Khatha Meetha (Old) 15. Bheja Fry 67. Khichadi: The Movie 16. Bhool Bhulaiya 68. Khiladi 17. Bhoothnaath/Bhoothnath 69. Khoobsurat (1980) Returns 70. Khosla Ka Ghosla 18. Biwi No 71. Kisi se Na Kehna 19. Bluffmaster 72. Kya Kool Hai Hum/Kya 20. Bol Radha Bol Super Cool Hai Hum 21. Bombay to Goa 73. Lage Raho Munna Bhai 22. Bombay to Goa (New) 74. Malamaal Weekly 23. Bunty aur Babli 75. Masti/Grand Masti 24. Chachi 420 76. Mr 25. Chalti ka Naam gaadi 77. Mujse Shadi Karoge (1958) 78. Munna Bhai MBBS 26. Chameli Ki Shaadi 79. Namak Halal 27. Chashme Budoor (1981) 80. Namastey London 28. Chillar Party 81. Naram garam 29. Chitchor 82. OMG! Oh My God 30. Choti Si Baat 83. Oye Lucky! Lucky Oye! 31. Chup Chup Ke 84. Padosan 32. Chupke Chupke 85. Partner 33. Coolie No 86. Phir Hera Pheri 34. Dabanng 87. -

Aspirational Movie List

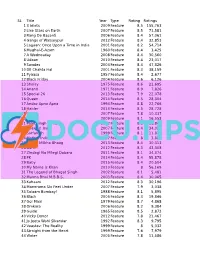

SL Title Year Type Rating Ratings 1 3 Idiots 2009 Feature 8.5 155,763 2 Like Stars on Earth 2007 Feature 8.5 71,581 3 Rang De Basanti 2006 Feature 8.4 57,061 4 Gangs of Wasseypur 2012 Feature 8.4 32,853 5 Lagaan: Once Upon a Time in India 2001 Feature 8.2 54,714 6 Mughal-E-Azam 1960 Feature 8.4 3,425 7 A Wednesday 2008 Feature 8.4 30,560 8 Udaan 2010 Feature 8.4 23,017 9 Swades 2004 Feature 8.4 47,326 10 Dil Chahta Hai 2001 Feature 8.3 38,159 11 Pyaasa 1957 Feature 8.4 2,677 12 Black Friday 2004 Feature 8.6 6,126 13 Sholay 1975 Feature 8.6 21,695 14 Anand 1971 Feature 8.9 7,826 15 Special 26 2013 Feature 7.9 22,078 16 Queen 2014 Feature 8.5 28,304 17 Andaz Apna Apna 1994 Feature 8.8 22,766 18 Haider 2014 Feature 8.5 28,728 19 Guru 2007 Feature 7.8 10,337 20 Dev D 2009 Feature 8.1 16,553 21 Paan Singh Tomar 2012 Feature 8.3 16,849 22 Chakde! India 2007 Feature 8.4 34,024 23 Sarfarosh 1999 Feature 8.1 11,870 24 Mother India 1957 Feature 8 3,882 25 Bhaag Milkha Bhaag 2013 Feature 8.4 30,313 26 Barfi! 2012 Feature 8.3 43,308 27 Zindagi Na Milegi Dobara 2011 Feature 8.1 34,374 28 PK 2014 Feature 8.4 55,878 29 Baby 2015 Feature 8.4 20,504 30 My Name Is Khan 2010 Feature 8 56,169 31 The Legend of Bhagat Singh 2002 Feature 8.1 5,481 32 Munna Bhai M.B.B.S. -

Vicky Donor Hindi Dubbed Hd Mp4 Movies Download

Vicky Donor Hindi Dubbed Hd Mp4 Movies Download Vicky Donor Hindi Dubbed Hd Mp4 Movies Download 1 / 5 2 / 5 See more ideas about movies, full movies online free, download movies. ... Asur S01 Hindi WEB Series 720p 480p WEB-DL Voot Original | hd mp4 high qaulity movie ... Vicky Donor (2012) Hindi Movie Bluray || 720p [600MB] || 1080p [2.1GB].. Vicky Donor (2012) 720p Hindi,Vicky Donor hd avi,Vicky Donor 300mb,Vicky Donor mobile movie,Vicky Donor mp4 download,Vicky Donor hd ... From here on, Chaddha's days and nights are spent in convincing Vicky to become a donor till he finally gives in. Download File. Server 1.. Download.. Vicky Donor (2012) BRRip Full Movie Download in Hd, Avi, Hd Avi And High Quality HD Bollywood movies, South Hindi Dubbed .... ... Indian Hindi Dubbed Movies, Punjabi Movies, Bengali Movies, Mp4 Movies, Hd Avi Movies, ... Vicky Donor 2012 Hindi 480P BrRip 350MB ESub ... Download Future World (2018) Full Movie Download HD 720P WEB-DL Free ... Bad Boys 1995 Download In Hindi Dubbed Dual Audio 480p BRRip 400Mb .... Vicky Donor (2012) Bollywood Hindi Full Movies Download, Vicky Donor (2012) Bollywood Hindi Full ... Latest South Indian Hindi Dubbed Movies (2020) .... Download Vicky Donor Filmyzilla 2012 300MB 480p HD Movie Download ... Mp4, Mkv, Avi etc. with the HD resolution 720p, 360p, 240p etc mobile movies HD ... filmyzilla 2019 2018 hollywood hindi dubbed movies also available in bluray ... 1000 Canciones Y Acordes De Guitarra Para Flamenco Pdf Free Vicky Donor (2012) full Movie Download, Bollywood Vicky Donor free download in hd for pc and mobile dvdrip mp4, mkv movie in 720p bluray. -

Health Officials Ramp up COVID-19 Testing

www.WeeklyVoice.com FRONT PAGE Friday, March 6, 2020 | A-1 Canada’s Leading South Asian Newspaper - Tel: 905-795-0639 Friday, MarchJune 2, 6, 2017 2020 www.WeeklyVoice.com VolVol 26, 23, No. No. 10 22 PM: 40025701 No Stay On Canadian Passenger Rights Charter, page 6 Why Pakistan Is So Perturbed About J & K, page 10 Ford Lunches With His Page Rudra Rami, page 12 Trudeau’s Approval Rating Drops 10 Points Energy & Climate Issues Singe PM; Conservatives Show Surge OTTAWA: Prime Minister latest public opinion data from rated, after weeks of conflict and Justin Trudeau and his minority the Angus Reid Institute finds the lack of resolution around the Liberal government are bearing PM’s performance has been lack- Coastal GasLi nk blockades. the scars of what has been a most ing in recent weeks, particularly The Prime Minister’s approval bruising start to a federal govern- on the energy and climate change rating has dropped 10 points, ment’s year. front, and this has had a negative and now sits at 33 per cent, right While the first 60 days of 2019 impact on his approval numbers. around where it was for most of were defined by a political scan- The most recent quarterly sur- 2019. dal, the beginning of 2020 has vey of more than 5000 adults More Key Findings: been marked by events at home shows the improved view of him • 34 per cent of Canadians and abroad that have demanded in the wake of the devastating would vote for the Conservative deft and adroit response. -

Festival Catalogue 2015

Jio MAMI 17th MUMBAI FILM FESTIVAL with 29 OCTOBER–5 NOVEMBER 2015 1 2 3 4 5 12 October 2015 MESSAGE I am pleased to know that the 17th Jio MAMI Mumbai Film Festival is being organised by the Mumbai Academy of Moving Image (MAMI) in Mumbai from 29th October to 5th November 2015. Mumbai is the undisputed capital of Indian cinema. This festival celebrates Mumbai’s long and fruitful relationship with cinema. For the past sixteen years, the festival has continued promoting cultural and MRXIPPIGXYEP I\GLERKI FIX[IIR ½PQ MRHYWXV]QIHME TVSJIWWMSREPW ERH GMRIQE IRXLYWMEWXW%W E QYGL awaited annual culktural event, this festival directs international focus to Mumbai and its continued success highlights the prominence of the city as a global cultural capital. I am also happy to note that the 5th Mumbai Film Mart will also be held as part of the 17th Mumbai Film Festival, ensuring wider distribution for our cinema. I congratulate the Mumbai Academy of Moving Image for its continued good work and renewed vision and wish the 17th Jio MAMI Mumbai Film Festival and Mumbai Film Mart grand success. (CH Vidyasagar Rao) 6 MESSAGE Mumbai, with its legacy, vibrancy and cultural milieu, is globally recognised as a Financial, Commercial and Cultural hub. Driven by spirited Mumbaikars with an indomitable spirit and great affection for the city, it has always promoted inclusion and progress whilst maintaining its social fabric. ,SQIXSXLI,MRHMERH1EVEXLM½PQMRHYWXV]1YQFEMMWXLIYRHMWTYXIH*MPQ'ETMXEPSJXLIGSYRXV] +MZIRXLEX&SPP][SSHMWXLIQSWXTVSPM½GMRHYWXV]MRXLI[SVPHMXMWSRP]FI½XXMRKXLEXE*MPQ*IWXMZEP that celebrates world cinema in its various genres is hosted in Mumbai. -

I Am the CHANGE 101-Hour National Filmmaking Challenge 2014 YES!

YES! i am the CHANGE 101-Hour National Filmmaking Challenge 2014 YES! i am the CHANGE (YIAC) is a nationwide film project that aims to inspire, engage and empower youth to participate in India’s social transformation, through the impactful medium of films. The 101-Hour National Filmmaking Challenge, where filmmakers and amateurs make short films of up to 5 minutes duration on various social issues is the flagship event of the program. Aim: • Engage with 5 lakh youth pan-India • Mobilise participation of 50,000 youth for filmmaking challenge Salient Features: • Last date of registration: August 7, 2014 o Participants register online as a team (max. 7 members per team) o Two categories for participation- Professional and Amateur • Filmmaking Challenge : August 15 to 19 o Participants receive the topic at 6 a.m. on August 15 , Independence Day. They have a challenge to make a short film in 101 hours o Topics are based on Social Causes, Everyday Heroes and Random Acts of Kindness • The film is submitted online by 11 am, on August 19 • 7- member Jury to select the winners: o Guneet Monga (Producer of The Lunch Box and the Gangs of Wasseypur) o Kailash Surendranath (Veteran Ad filmmaker) o Nina Lath (Managing Director, National Film Development Corporation) o Shoojit Sircar (Director of Vicky Donor and Madras Cafe) o Vikramaditya Motwane (Director of Udaan and Producer of Queen) o Pritish Nandy (Poet, Journalist and Film Producer) o Dr. Nagesh Rao (President and Director, MICA) • Online donation platform for participants to use their film to raise funds for a Not-for- Profit (NGO) of their choice: September 1 to October 2, 2014 • Awards ceremony on October 10 to felicitate the best filmmakers • Total grant of Rs 25 lakhs to be given to the winners. -

List of Movies - 2012

Entertainment Network India Limited Mirchi Music Awards Hindi - 5 List of movies - 2012 Sr. No. Film Album Title 1 Aalaap - Ek Nayi Roshni 2 Agent Vinod 3 Agneepath 4 Aiyyaa 5 Ajab Gazabb Love 6 Ata Pata Laapata 7 Barfi! 8 Bittoo Boss - VDO Shooter 9 Blood Money 10 Bol Bachchan 11 Bumboo 12 Chaar Din Ki Chandni 13 Chakradhar 14 Chakravyuh 15 Chal Pichchur Banate Hain 16 Challo Driver 17 Chhodo Kal Ki Baatein 18 Chittagong 19 Chutki Bajaa Ke 20 Cigarette Ki Tarah 21 Cocktail 22 Daal Mein Kuch Kaala Hai 23 Dabangg 2 24 Dam 999 25 Dangerous Ishq 3D 26 Delhi Safari 27 Department 28 Diary Of A Butterfly 29 Ek Main Aur Ekk Tu 30 Ek Tha Tiger 31 Ekk Deewana Tha 32 English Vinglish 33 Fatso! 34 Ferrari Ki Sawaari 35 From Sydney With Love 36 Future To Bright Hai Ji 37 Gali Gali Chor Hai 38 Gangs of Wasseypur 39 Gangs of Wasseypur II 40 Gattu 41 Ghost 42 Hate Story 43 Heroine 44 Housefull 2 45 I M 24 46 Ishaqzaade 47 Jab Tak Hai Jaan 48 Jalpari - The Desert Mermaid 49 Janleva 555 50 Jannat 2 51 Jeena Hai To Thok Daal 52 Jism 2 - To Love Her Is To Die 53 Jodi Breakers 54 Joker 55 Kahaani 56 Kamaal Dhamaal Malamaal 57 Khiladi 786 58 Kismet Love Paisa Dilli 59 Krishna Aur Kans 60 Kyaa Super Kool Hain Hum 61 Le Gaya Saddam 62 Life Ki Toh Lag Gayi 63 London, Paris, New York 64 Love Possible 65 Luv Shuv Tey Chicken Khurana 66 Makkhi 67 Married 2 America 68 Maximum 69 Mere Dost Picture Abhi Baki Hai 70 Mr Bhatti On Chutti 71 OMG - Oh My God! 72 Paan Singh Tomar 73 Players 74 Prem Mayee 75 Qasam Se Qasam Se 76 Qayamat Hi Qayamat 77 Raaz 3 78 Rakhtbeej 79 Riwayat 80 Rowdy Rathore 81 Rush - If You Stop. -

LIST of HINDI CINEMA AS on 17.10.2017 1 Title : 100 Days

LIST OF HINDI CINEMA AS ON 17.10.2017 1 Title : 100 Days/ Directed by- Partho Ghosh Class No : 100 HFC Accn No. : FC003137 Location : gsl 2 Title : 15 Park Avenue Class No : FIF HFC Accn No. : FC001288 Location : gsl 3 Title : 1947 Earth Class No : EAR HFC Accn No. : FC001859 Location : gsl 4 Title : 27 Down Class No : TWD HFC Accn No. : FC003381 Location : gsl 5 Title : 3 Bachelors Class No : THR(3) HFC Accn No. : FC003337 Location : gsl 6 Title : 3 Idiots Class No : THR HFC Accn No. : FC001999 Location : gsl 7 Title : 36 China Town Mn.Entr. : Mustan, Abbas Class No : THI HFC Accn No. : FC001100 Location : gsl 8 Title : 36 Chowringhee Lane Class No : THI HFC Accn No. : FC001264 Location : gsl 9 Title : 3G ( three G):a killer connection Class No : THR HFC Accn No. : FC003469 Location : gsl 10 Title : 7 khoon maaf/ Vishal Bharadwaj Film Class No : SAA HFC Accn No. : FC002198 Location : gsl 11 Title : 8 x 10 Tasveer / a film by Nagesh Kukunoor: Eight into ten tasveer Class No : EIG HFC Accn No. : FC002638 Location : gsl 12 Title : Aadmi aur Insaan / .R. Chopra film Class No : AAD HFC Accn No. : FC002409 Location : gsl 13 Title : Aadmi / Dir. A. Bhimsingh Class No : AAD HFC Accn No. : FC002640 Location : gsl 14 Title : Aag Class No : AAG HFC Accn No. : FC001678 Location : gsl 15 Title : Aag Mn.Entr. : Raj Kapoor Class No : AAG HFC Accn No. : FC000105 Location : MSR 16 Title : Aaj aur kal / Dir. by Vasant Jogalekar Class No : AAJ HFC Accn No. : FC002641 Location : gsl 17 Title : Aaja Nachle Class No : AAJ HFC Accn No. -

Popular Award Category Nomiees

POPULAR AWARD CATEGORY NOMIEES Best Screenplay Sr. No. Entries Film 1 Anurag Basu &Tani Basu Barfi ! 2 Gauri Shinde English Vinglish 3 Juhi Chaturvedi Vicky Donor Sanjay Chouhan &Tigmanshu 4 Dhulia Paan Singh Tomar 5 Sujoy Ghosh Kahaani Best Story Sr. No. Entries Film 1 Anurag Basu & Tani Basu Barfi ! 2 Bhavesh Mandalia & Umesh Shukla OMG - Oh My God 3 Gauri Shinde English Vinglish 4 Juhi Chaturvedi Vicky Donor Sanjay Chouhan & Tigmanshu 5 Dhulia Paan Singh Tomar 6 Sujoy Ghosh & Advaita Kala Kahaani Best Dialogue Sr. No. Entries Film 1 Bhavesh Mandalia & Umesh Shukla OMG - Oh My God 2 Gauri Shinde English Vinglish 3 Juhi Chaturvedi Vicky Donor 4 Ritesh Shah Kahaani 5 Sanjeev Datta Barfi ! Zuisham Quadri, Akhilesh, Sachin Ladia & Anurag 6 Kashyap Gangs of Wasseypur Best Choreography Sr. No. Entries Song Film 1 Bosco - Caesar Daaru Desi Cocktail Chinta Ta Ta Chita 2 Bosco - Caesar Chita Rowdy Rathore 3 Farah Khan Radha Student Of The Year 4 Ganesh Acharya Chikni Chameli Agneepath Vaibhavi 5 Merchant Ishq Shava Jab Tak Hai Jaan Best Lyrics Sr. No. Entries Song Film Ayushmann Khurrana & Rochak 1 Kohli Paani Da Rang Vicky Donor 2 Gulzar Saans Jab Tak Hai Jaan 3 Irshad Kamil Tum Hi Ho Bandhu Cocktail Talaash - The Answer Lies 4 Javed Akhtar Jee Le Zaraa Within 5 Sayeed Quadri Phir Le Aya Dil Barfi ! 6 Varun Grover Womaniya Gangs of Wasseypur Best Music Sr. No. Entries Film 1 A.R. Rahman Jab Tak Hai Jaan 2 Ajay - Atul Agneepath 3 Pritam Barfi ! 4 Pritam Cocktail 5 Sneha Khanwalkar Gangs of Wasseypur Best Male Singer Sr. -

The “Bollywoodization” of Popular Indian Visual Culture: a Critical Perspective

tripleC 12(1): 277-285, 2014 http://www.triple-c.at The “Bollywoodization” of Popular Indian Visual Culture: A Critical Perspective Keval J. Kumar Adjunct Professor, Mudra Institute of Communications, Ahmedabad, India. kevalku- [email protected] Abstract: The roots of popular visual culture of contemporary India can be traced to the mythological films produced by D. G. Phalke during the decades of the ‘silent’ era from 1912 to 1934. The era of the “talkies” of the 1930s ushered in the “singing’” or musical genre, which together with Phalke’s visual style remains the hallmark of Bollywood cinema. The history of Indian cinema is replete with films made in other genres and styles (e. g., social realism, satires, comedies, fantasy, horror, or stunt) in the numerous languages of the country. However, it is the popular Hindi cinema (now generally termed Bollywood) that has dominated national Indian cinema and its audiovisual culture. It has hegemonized the entire film industry as well as other popular technology-based art forms including the press, radio, television, music, advertising, the worldwide web, the social media, and telecommunica- tions media. The form and substance of these modern art forms, while adapting to the demands of the new media technologies, continued to be rooted in the visual arts and practices of folk and classical traditions of earlier times. Keywords: Visual Culture, Hegemony, Visual Style, Indian Cinema, Indian Television, Indian Advertising 1. Introduction Infinite diversity, plurality and multiplicity are the primary features that mark popular Indian visual culture. This culture has come about through centuries of absorption, integration and acculturation, as the subcontinent evolved at its own leisurely pace engaging with invaders, settlers and colonialists who brought with them audio and visual cultures of their own. -

Bollywood Hits 150 Hits, 10 CD+G Disc

Bollywood Hits 150 Hits, 10 CD+G Disc Disc One No. Artist Track 1 Aaj Dil Shayrana Holiday 2 Aaj Phir Jeene Ki Tamanna Guide 3 Aaja Re Pardesi Madhumati 4 Aaja Sanam Chori Chori 5 Aaja Tujhko Pukare Mera Pyar Neel Kamal 6 Aap Jaisa Koi Qurbani 7 Ae Mere Humsafar Qayamat Se Qayamat Tak 8 Afsana Likh Rahi Hoon Dard 9 Agar Tum Mil Jao Zeher 10 Ajeeb Dastan Hai Yeh Dil Apna Aur Preet Parai 11 Ankhiyan Milake Rattan 12 Arijit Singh Enna Sona 13 Awaara Hoon Awaara 14 Awaaz De Kahan Hai Anmol Ghadi 15 Ayega Aanewala Mahal Disc Two No. Artist Track 1 Babuji Dheere Chalna Aar Paar 2 Baby Ko Bass Pasand Hai Sultan 3 Baharon Phool Barsao Suraj 4 Bahon Ke Darmiyan Khamoshi 5 Balam Pichkari Yeh Jawaani Hai Deewani 6 Beedi Omkara 7 Behti Hawa Sa Tha Who Idiots 8 Bol Radha Bol Sangam 9 Bole Chudiyan Kabhi Khushi Kabhie Gham 10 Chaiyya Chaiyya Dil Se 11 Chalte Chalte Pakeezah 12 Chammack Challo Ra One 13 Chand Sifarish Fanaa 14 Chaudhvin Ka Chand Ho Chaudhvin Ka Chand 15 Chittiyaan Kalaiyaan Roy Disc Three No. Artist Track 1 Chod Do Anchal Zamana Kya Kahega Beta 2 Chod Do Anchal Zamana Kya Kahega Paying Guest 3 Choli Ke Peeche Khalnayak 4 Chura Liya Hai Tumne Jo Dil Ko Yaadon Ki Baaraat 5 Deewana Leke Aaya Hai 6 Deewangi Deewangi Om Shanti Om 7 Dekha Ek Khwab Silsila 8 Dekha Hai Pehli Baar Saajan 9 Dhak Dhak Karne Laga Beta 10 Dheere Dheere Se Aashiqui 11 Dhunki Mere Brother Ki Dulhan 12 Didi Tera Devar Deewana Hum Aapke Hain Koun 13 Dil Deewana Maine Pyar Kiya 14 Dil Kya Kare Jab Kisi Se Disc Four No. -

Role of Bollywood Cinema in Shaping Youngerstersfor Social Awareness

PSYCHOLOGY AND EDUCATION (2021) 58(2): 6243-6247 ISSN: 00333077 Role of Bollywood Cinema in Shaping Youngerstersfor Social Awareness Dr. Neeraj Khattri Professor and Director Institute of Media Studies Shri Ramswaroop Memorial University, IN [email protected] & Arshita Singh Researcher [email protected] ABSTRACT The potential of cinema from thebeginning is used in such a way which benefits the society.The role of Cinema on society has been recognized from the very beginning of Cinema itself. It has been seen that children who cannot get good education but can easily acquire bad habits- buy two anna tickets and watch cinema daily. The society needs to be made aware of the influence of Cinema on the social and moral turnout of the viewers. An attempt has been made to evaluate the social implications of Cinema which is the powerful medium of information, education and entertainment results in the process of opinion building in various social groups. Community is very much influenced by the cinema and they inhale psychological, cultural, sociological changes along with the drastic changes in lifestyle. In recent times cinema often started to show some sensitive issues related to menstruation, women harassment, drug consumption, sexualviolence, etc. Before these movies no one wants to talk about these things they consider it as taboo for society, people never want to talk about erectile dysfunction sanitation, menstrual hygiene etc but some director and actors raise these issue and motivate people to stand for themselves. Movies like Shubh Mangal JaydaSavdhaan,Toilet ek prem Katha, Phullu and soon address such issues and give courage to talk about that.Through this research paper the attempt was made to analyze the effect of cinema on people and how people accept them.