SECURITIES and EXCHANGE COMMISSION Metro Manila, Philippines ______

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sec Form 20-Is

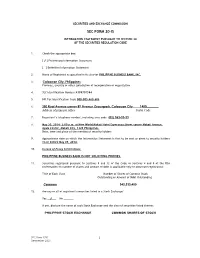

SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ √ ] Preliminary Information Statement [ ] Definitive Information Statement 2. Name of Registrant as specified in its charter PHILIPPINE BUSINESS BANK, INC. 3. Caloocan City, Philippines Province, country or other jurisdiction of incorporation or organization 4. SEC Identification Number A199701584 5. BIR Tax Identification Code 000-005-469-606 6. 350 Rizal Avenue corner 8th Avenue Gracepark, Caloocan City 1400________ Address of principal office Postal Code 7. Registrant’s telephone number, including area code (02) 363-33-33 8. May 30, 2014- 2:00 p.m. at New World Makati Hotel Esperanza Street corner Makati Avenue, Ayala Center, Makati City, 1228 Philippines. Date, time and place of the meeting of security holders 9. Approximate date on which the Information Statement is first to be sent or given to security holders on or before May 09, 2014. 10. In case of Proxy Solicitations: PHILIPPINE BUSINESS BANK IS NOT SOLICITING PROXIES. 11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding or Amount of Debt Outstanding Common 343,333,400 12. Are any or all of registrant's securities listed in a Stock Exchange? Yes __√___ No _______ If yes, disclose the name of such Stock Exchange and the class of securities listed therein: PHILIPPINE STOCK EXCHANGE COMMON SHARES OF STOCK SEC Form 17-IS 1 December 2003 PHILIPPINE BUSINESS BANK, INC. -

(“Medco”) Is a Company Incorporated in the Republic of Philippines with Limited Liability Whose Shares Are Listed on the Philippines Stock Exchange, Inc

Medco Holdings, Inc (“Medco”) is a company incorporated in the Republic of Philippines with limited liability whose shares are listed on The Philippines Stock Exchange, Inc. (“PSE”). Lippo China Resources Limited (“LCR”) is currently interested in approximately 70.7 per cent. of the issued share capital of Medco, making it a subsidiary of LCR. Lippo Limited (“Lippo”) owns shares representing approximately 71.1 per cent. of the issued share capital of LCR. Accordingly, each of LCR and Medco is a subsidiary of Lippo. The quarterly report of Medco ended 30th June, 2005 (the “Quarterly Report”) was released on the website of PSE today. The following is a reproduction of the Quarterly Report for information purpose only. COVER SHEET 39652 SEC Registration Number MEDCO HOLD I NGS , I NC . AND SUBS I D I A RY (Company’s Full Name) 31st Floor,Rufino Pacific Tower, 6784 Ayala Avenue , Makat i Ci ty (Business Address: No. Street City/Town/Province) Dionisio E. Carpio, Jr. 811-0465 (Contact Person) (Company Telephone Number) 09 30 17-Q Month Day (Form Type) Month Day 2004 AMENDED (Annual Meeting) (Secondary License Type, If Applicable) Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. SECURITIES AND EXCHANGE COMMISSION Metro Manila, Philippines ______________________ SEC FORM 17-Q QUARTERLY REPORT PURSUANT TO SECTION 11 OF THE REVISED SECURITIES ACT AND RSA RULE 11(a)-1(b)(2) THEREUNDER ______________________ 1. -

World Bank Document

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized AWorld Rank ' = Dcrelopmeni : Currency Un it - Peso : $1.00 - E;: PhP51.36 PhP1.OO - ; US$0.0195 [F ISCALYEAR January 1 - December 31 ASEAN Association of Southeast NCR National Capital Region AsianNations NGAS New Government Accountirlg AMC Asset Management Company System BIR Bureau of Internal Revenue NGO Non-Government Orgarrization I BOC Bureau of Customs hI PL Non-Performing Loan ; BOT Build Operate Transfer NRM National Resource and I' BSP Bangko Sentral ng Pilipinas Management j CMDC Capital Markets Development NSCB National Statistical I Corporation Coordination Board 1 COA Commission on Audit NSO National Statistics Office 1 COP Committee on Privatization ODA Overseas Development 1 CSC Civil Service Commission Assistance j DBM Department of Budget and OPIF Organizational Performance I Management I Indicator Framework j DOF Department of Finance PDIC Ph~lippineDeposit Insurance / DST Documentary Stamp Tax Corporation / EKB Expanded Commercial Bank PCEG Presidential Committee on / EPR Effective Protection Rate Effective Governance Reform , FIES Family Income and PPI Private Participation in Expenditure Survey Infrastructure 1 GAAP Generally Accepted Accounting PS E Philippine Stock Exchange Principles PSISSA Public Sector Institutional GDP Gross Domestic Product Strengthening and GNP Gross National Product Streamlining Agenda GOCC Government Owned and ROPOA Real and Other Properties Controlled Corporation Owned and -

Download 287.76 KB

ASIAN DEVELOPMENT BANK RRP: PHI 31655 REPORT AND RECOMMENDATION OF THE PRESIDENT TO THE BOARD OF DIRECTORS ON A PROPOSED LOAN AND TECHNICAL ASSISTANCE GRANT TO THE REPUBLIC OF THE PHILIPPINES FOR THE NONBANK FINANCIAL GOVERNANCE PROGRAM October 2001 CURRENCY EQUIVALENTS (as of 10 October 2001) Currency Unit – Peso (P) P1.00 = $0.02 $1.00 = P51.90 ABBREVIATIONS ADAPS – automated debt auction processing system ADB – Asian Development Bank ASEAN – Association of Southeast Asian Nations BOA – Board of Accountancy BSP – Bangko Sentral ng Pilipinas CMDP – Capital Market Development Program CPA – certified public accountant DOF – Department of Finance DST – documentary stamp tax DVP – delivery-versus-payment FSAP – Financial Sector Assessment Program GDP – gross domestic product GNP – gross national product GSED – Government securities eligible dealers IAS – international accounting standards IMF – International Monetary Fund IOSCO – International Organization of Securities Commissions IPO – initial public offering IRR – implementing rules and regulations LIBOR – London interbank offered rate MIS – management information system NBFI – nonbank financial institution NFG – nonbank financial governance NPL – nonperforming loan PCDI – Philippine Central Depository, Inc. PDIC – Philippine Deposit Insurance Corporation PICPA – Philippine Institute of Certified Public Accountants PNB – Philippine National Bank PRC – Professional Regulation Commission PSE – Philippine Stock Exchange QB – quasi bank RTGS – real time gross settlement SCCP – Securities Clearing Corporation of the Philippines SDR – special drawing rights SEC – Securities and Exchange Commission SRC – Securities Regulation Code SRO – self-regulatory organization TA – technical assistance USAID – United States Agency for International Development NOTE In this report, "$" refers to US dollars. CONTENTS Page LOAN AND PROGRAM SUMMARY ii I. THE PROPOSAL 1 II. INTRODUCTION 1 III. -

The Politics of Economic Reform in the Philippines the Case of Banking Sector Reform Between 1986 and 1995

The Politics of Economic Reform in the Philippines The Case of Banking Sector Reform between 1986 and 1995 A thesis submitted for the degree of PhD School of Oriental and African Studies (SOAS) University of London 2005 Shingo MIKAMO ProQuest Number: 10673052 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10673052 Published by ProQuest LLC(2017). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 2 Abstract This thesis is about the political economy of the Philippines in the process of recovery from the ruin of economic crisis in the early 1980s. It examines the dynamics of Philippine politics by focussing on banking sector reform between 1986 and 1995. After the economic turmoil of the early 1980s, the economy recovered between 1986 and 1996 under the Aquino and Ramos governments, although the country is still facing numerous economic challenges. After the "Asian currency crisis" of 1997, the economy inevitably decelerated again. However, the Philippines was seen as one of the economies least adversely affected by the rapid depreciation of its currency. The existing literature tends to stress the roles played by international financial structures, the policy preferences of the IMF, the World Bank and the US government and the interests of the dominant social force as decisive factors underlying economic and banking reform policy-making in the Philippines. -

ROBINSONS LAND CORPORATION 43Rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE

ROBINSONS LAND CORPORATION 43rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE. COR. POVEDA RD. ORTIGAS CENTER, PASIG CITY TEL. NO.: 633-7631, 637-1670, 240-8801 FAX NO.: 633-9387 OR 633-9207 July 10, 2012 PHILIPPINE STOCK EXCHANGE, INC. 3rd Floor, Philippine Stock Exchange Ayala Triangle, Ayala Avenue Makati City Attention: Ms. Janet A. Encarnacion Head – Disclosure Department PHILIPPINE DEALING AND EXCHANGE CORP. 37/F, Tower 1, The Enterprise Center 6766 Ayala Avenue corner Paseo de Roxas, Makati City Attention: Mr. Cesar B. Crisol President and Chief Operating Officer Re: Robinsons Land Corporation (RLC) List of Top 100 Stockholders and PCD Participants Gentlemen: In compliance with PSE Memo for Brokers No. 225-2003, please find attached the following. 1. List of Top 100 Stockholders of RLC as of June 30, 2012. 2. List of Top 100 PCD Participants of RLC as of June 30, 2012. Thank you. Very truly yours, ROSALINDA F. RIVERA Corporate Secretary /lbo BPI STOCK TRANSFER OFFICE ROBINSONS LAND CORPORATION TOP 100 STOCKHOLDERS AS OF JUNE 30, 2012 RANK STOCKHOLDER NUMBER STOCKHOLDER NAME NATIONALITY CERTIFICATE CLASS OUTSTANDING SHARES PERCENTAGE TOTAL 1 10003137 J. G. SUMMIT HOLDINGS, INC. FIL U 2,496,114,787 60.9725% 2,496,114,787 29/F GALLERIA CORPORATE CTR. EDSA COR. ORTIGAS AVE. MANDALUYONG CITY 2 16012118 PCD NOMINEE CORPORATION (NON-FILIPINO) NOF U 1,023,189,383 24.9934% 1,023,189,383 37/F THE ENTERPRISE CENTER TOWER 1, COR. PASEO DE ROXAS, AYALA AVENUE, MAKATI CITY 3 16012119 PCD NOMINEE CORPORATION (FILIPINO) FIL U 539,962,142 13.1896% 539,962,142 37/F THE ENTERPRISE CENTER TOWER 1, COR. -

Vmc 17C Sec Manifestation and Motion

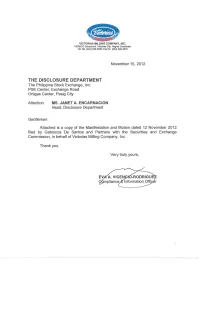

VICTORIAS..MILLING COMPANY, INC. V1CMICO Compound. Victorias City,Negros Occidental Tel. No_(034) 399-3380; Fax No. (034) 399-3675 November 15,2012 THE DISCLOSURE DEPARTMENT The Philippine Stock Exchange, Inc. PSE Center, Exchange Road Ortigas Center, Pasig City Attention: MS. JANET A. ENCARNACION Head, Disclosure Department Gentlemen: Attached is a copy of the Manifestation and Motion dated 12 November 2012 filed by Gabionza De Santos and Partners with the Securities and Exchange Commission, in behalf of Victorias Milling Company, Inc. Thank you. Very truly yours, EVj{A. VICENYtO-RODRIGU pliance%lnformation Officer ; ;; " iREPUlBUC OF THE PiI-llUPPilfllES SECUiRnJESA!MtD EXCHANGE COMMISSJON • ' . SEC Bldg." E~SA, Gri?eTl:hjIJs, Mamlaluyonfj City i>f nftS) IN TiHIE MA1TER OF THE PElITION , ~ . , ~~':¥~ FOR DECLARATION OF A. STATE Of . ~: \ l:..L2 : ' \ ~~ ! i!-'- \ 1 ~ \ 1 SUSPENSION OF PAYMB':IT; fOR l'l ," " >'''12 1\\ THE APPROVAL OF A i: :;~! , .' :.u, \\' \ R.E.H.AS. JUT.A.TION PLAN, AND THE . trlS'3~")U L..::.l.!-~ APpm~TlIVlENT Of A MANAGEMENT -~-;, W'" COMMJnEE,. SEC CASE NO.'07-97-5 VICTORJASfit,ILUNG COJVJPANY, INC. Petiiioner: ~----------------~ . , ~ MANifESTATION AtW MOTION PETUlONER VICTORIAS MlLlING COMPANY, INC. r VMC"), in the above-errlitled case, by its undersigned counsel, 10 this Honorable Commission respectfully manifests thaI there was one {'I) Board seat previously reserved lOT the Joinl Venture Partner under the Approved - RehabmtBt~on Plans r AiR?"), particularly the Proposed Alternative I Rehabiliiafion Plan, and the Debt Restructuring Agreement ("DHA") and \formerly occupied by the nominee of Tanduay Holdings, Inc ("THl") as a I conseqeeoceot its IT nfLlslon of the amount of Three Hundred Milljon Pesos (,R300;OOO,OOO.OD) into. -

ROBINSONS LAND CORPORATION 43Rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE

ROBINSONS LAND CORPORATION 43rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE. COR. POVEDA RD. ORTIGAS CENTER, PASIG CITY TEL. NO.: 633-7631, 637-1670, 240-8801 FAX NO.: 633-9387 OR 633-9207 April 11, 2012 PHILIPPINE STOCK EXCHANGE, INC. 3rd Floor, Philippine Stock Exchange Ayala Triangle, Ayala Avenue Makati City Attention: Ms. Janet A. Encarnacion Head – Disclosure Department PHILIPPINE DEALING AND EXCHANGE CORP. 37/F, Tower 1, The Enterprise Center 6766 Ayala Avenue corner Paseo de Roxas, Makati City Attention: Mr. Cesar B. Crisol President and Chief Operating Officer Re: Robinsons Land Corporation (RLC) List of Top 100 Stockholders and PCD Participants Gentlemen: In compliance with PSE Memo for Brokers No. 225-2003, please find attached the following. 1. List of Top 100 Stockholders of RLC as of March 31, 2012. 2. List of Top 100 PCD Participants of RLC as of March 30, 2012. Thank you. Very truly yours, ROSALINDA F. RIVERA Corporate Secretary /lbo BPI STOCK TRANSFER OFFICE ROBINSONS LAND CORPORATION TOP 100 STOCKHOLDERS AS OF MARCH 31, 2012 RANK STOCKHOLDER NUMBER STOCKHOLDER NAME NATIONALITY CERTIFICATE CLASS OUTSTANDING SHARES PERCENTAGE TOTAL 1 10003137 J. G. SUMMIT HOLDINGS, INC. FIL U 2,496,114,787 60.9725% 2,496,114,787 29/F GALLERIA CORPORATE CTR. EDSA COR. ORTIGAS AVE. MANDALUYONG CITY 2 16012118 PCD NOMINEE CORPORATION (NON-FILIPINO) NOF U 984,568,985 24.0500% 984,568,985 37/F THE ENTERPRISE CENTER TOWER 1, COR. PASEO DE ROXAS, AYALA AVENUE, MAKATI CITY 3 16012119 PCD NOMINEE CORPORATION (FILIPINO) FIL U 578,290,337 14.1258% 578,290,337 37/F THE ENTERPRISE CENTER TOWER 1, COR. -

Small Business Lending and Social Capital: Are Rural Relationships Different?

Small Business Lending and Social Capital: Are Rural Relationships Different? Robert DeYoung** University of Kansas, Lawrence, KS USA Dennis Glennon* Office of the Comptroller of the Currency, Washington DC USA Peter Nigro Bryant University, Smithfield, RI USA Kenneth Spong* Federal Reserve Bank of Kansas City, Kansas City, MO USA June 2012 Abstract: Rural communities often are described as places where “everyone knows each other’s business.” Such intra-community information is likely to translate into a stock “social capital” that supports well-informed financial transactions (Guiso, Sapienza and Zingales 2004). We investigate whether and how the “ruralness” of small banks and small business borrowers influences loan default rates, using data on over 18,000 U.S. Small Business Administration (SBA) loans originated and held by rural and urban community banks between 1984 and 2001. These data provide a good test of the value of soft information and lending relationships because (a) these borrowers tend to be smaller, younger, and more credit-challenged than other small businesses and (b) these loans were originated largely before the advent of small business credit scoring and securitization, and hence they were held in portfolio and put some bank capital directly at risk. We have two main findings. First, loans originated by rural community banks and/or loans borrowed by rural businesses default substantially less often than loans made by urban banks and/or in urban areas. Second, loan default rates are significantly higher when borrowers are located outside the geographic market of their lenders, even after accounting for the physical distance between the bank and the small business. -

2003 Turned out to Be a Productive Year for Export and Industry Bank (EIB)

Letter to Shareholders Financial Highlights Corporate Governance Board of Directors Board Committees Senior Management Senior Officers in Board Committees Corporate Profile Exportbank Group of Companies Statement of Management’s Responsibility Report of Independent Public Accountants Statements of Condition Statements of Income Statements of Changes in Capital Funds Statements of Cash Flows Notes to Financial Statements Products and Services Branches Letter to Shareholders Dear Fellow Shareholders, Amidst the economic and political difficulties, 2003 turned out to be a productive year for Export and Industry Bank (EIB). The operating results are noteworthy taking into account the tough post merger challenges that EIB faced. In 2003 the bank consolidated and prioritized sound liquidity management and strengthening of the balance sheet and took on the final and crucial stages of the Liability Servicing Plan (LSP). The EIB Group managed to register an after tax profit of Php130.1 million in 2003 as against the previous year’s net income of Php380.8 million. The results are not as impressive but they actually reveal the growing confidence of customers in your merged bank. 2002’s income was boosted primarily by revenues coming from the discounting of repayment notes issued under the LSP. This business activity significantly declined in 2003 indicating that there was a significantly higher population of LSP depositors and investors retained by and affirming their faith in the bank. The Bank’s solvency and economic capital position stayed within prudential standards in 2003. The risk based capital adequacy ratio (CAR) stood at 16.3% and 15.9% on a consolidated and solo basis, respectively, which were way above the minimum CAR requirements of the Bank Letter to Shareholders for International Settlements (BIS) of 8% and Bangko Sentral ng Pilipinas of 10%, respectively. -

Securities and Exchange Commission Sec Form 20-Is

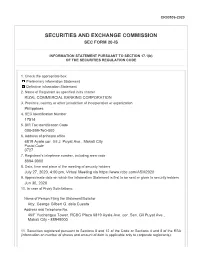

CR03536-2020 SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 17.1(b) OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: Preliminary Information Statement Definitive Information Statement 2. Name of Registrant as specified in its charter RIZAL COMMERCIAL BANKING CORPORATION 3. Province, country or other jurisdiction of incorporation or organization Philippines 4. SEC Identification Number 17514 5. BIR Tax Identification Code 000-599-760-000 6. Address of principal office 6819 Ayala cor. Gil J. Puyat Ave., Makati City Postal Code 0727 7. Registrant's telephone number, including area code 8894-9000 8. Date, time and place of the meeting of security holders July 27, 2020, 4:00 pm, Virtual Meeting via https://www.rcbc.com/ASM2020 9. Approximate date on which the Information Statement is first to be sent or given to security holders Jun 30, 2020 10. In case of Proxy Solicitations: Name of Person Filing the Statement/Solicitor Atty. George Gilbert G. dela Cuesta Address and Telephone No. 46/F Yuchengco Tower, RCBC Plaza 6819 Ayala Ave. cor. Sen. Gil Puyat Ave., Makati City - 88949000 11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 1,935,628,896 13. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange - common The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. -

World Bank Document

Report No.: 23687-PH Public Disclosure Authorized Combating Corruption in the Philippines: An Update September 30, 2001 Public Disclosure Authorized Philippine Country Management Unit East Asia and Pacific Regional Office Public Disclosure Authorized Public Disclosure Authorized Document of the World Bank CURRENCY EQUIVALENTS (As of September 30, 2001) Currency Unit = Peso (P) $1.00 = P51.34 1 Peso = $0.019 FISCAL YEAR January 1 - December 31 GLOSSARY OF ACRONYMS ADB Asian Development Bank ICT Information and Communications AusAID Australian Agency for Technology International Development LGU Local government unit BIR Bureau of Internal Revenue MBC Makati Business Club BSP Bangko Sentral ng Pilipinas MTPDP Medium-Term Philippine Development BWRC Best World Resources Plan Corporation NBI National Bureau of Investigation CG Consultative Group NEDA National Economic and Development CIDA Canadian Intemational Authority Development Agency NGO Non-governmental Organization COA Commission on Audit OECD Organization for Economic Cooperation CPI Corruption Perception Index and Development CSC Civil Service Commission P Philippine peso DAP Development Academy of the PAGC Presidential Anti-Graft Commission Philippines PCAGC Presidential Commission Against Graft DBM Department of Budget and and Corruption Management PCEG Presidential Committee on Effective DECS Department of Education, Culture Governance and Sports PCGG Presidential Commission on Good DENR Department of Environment and Governance Natural Resources PCIJ Philippine Center for Investigative