2003 Turned out to Be a Productive Year for Export and Industry Bank (EIB)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sec Form 20-Is

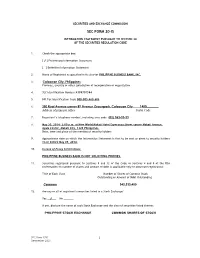

SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ √ ] Preliminary Information Statement [ ] Definitive Information Statement 2. Name of Registrant as specified in its charter PHILIPPINE BUSINESS BANK, INC. 3. Caloocan City, Philippines Province, country or other jurisdiction of incorporation or organization 4. SEC Identification Number A199701584 5. BIR Tax Identification Code 000-005-469-606 6. 350 Rizal Avenue corner 8th Avenue Gracepark, Caloocan City 1400________ Address of principal office Postal Code 7. Registrant’s telephone number, including area code (02) 363-33-33 8. May 30, 2014- 2:00 p.m. at New World Makati Hotel Esperanza Street corner Makati Avenue, Ayala Center, Makati City, 1228 Philippines. Date, time and place of the meeting of security holders 9. Approximate date on which the Information Statement is first to be sent or given to security holders on or before May 09, 2014. 10. In case of Proxy Solicitations: PHILIPPINE BUSINESS BANK IS NOT SOLICITING PROXIES. 11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding or Amount of Debt Outstanding Common 343,333,400 12. Are any or all of registrant's securities listed in a Stock Exchange? Yes __√___ No _______ If yes, disclose the name of such Stock Exchange and the class of securities listed therein: PHILIPPINE STOCK EXCHANGE COMMON SHARES OF STOCK SEC Form 17-IS 1 December 2003 PHILIPPINE BUSINESS BANK, INC. -

(“Medco”) Is a Company Incorporated in the Republic of Philippines with Limited Liability Whose Shares Are Listed on the Philippines Stock Exchange, Inc

Medco Holdings, Inc (“Medco”) is a company incorporated in the Republic of Philippines with limited liability whose shares are listed on The Philippines Stock Exchange, Inc. (“PSE”). Lippo China Resources Limited (“LCR”) is currently interested in approximately 70.7 per cent. of the issued share capital of Medco, making it a subsidiary of LCR. Lippo Limited (“Lippo”) owns shares representing approximately 71.1 per cent. of the issued share capital of LCR. Accordingly, each of LCR and Medco is a subsidiary of Lippo. The quarterly report of Medco ended 30th June, 2005 (the “Quarterly Report”) was released on the website of PSE today. The following is a reproduction of the Quarterly Report for information purpose only. COVER SHEET 39652 SEC Registration Number MEDCO HOLD I NGS , I NC . AND SUBS I D I A RY (Company’s Full Name) 31st Floor,Rufino Pacific Tower, 6784 Ayala Avenue , Makat i Ci ty (Business Address: No. Street City/Town/Province) Dionisio E. Carpio, Jr. 811-0465 (Contact Person) (Company Telephone Number) 09 30 17-Q Month Day (Form Type) Month Day 2004 AMENDED (Annual Meeting) (Secondary License Type, If Applicable) Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. SECURITIES AND EXCHANGE COMMISSION Metro Manila, Philippines ______________________ SEC FORM 17-Q QUARTERLY REPORT PURSUANT TO SECTION 11 OF THE REVISED SECURITIES ACT AND RSA RULE 11(a)-1(b)(2) THEREUNDER ______________________ 1. -

World Bank Document

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized AWorld Rank ' = Dcrelopmeni : Currency Un it - Peso : $1.00 - E;: PhP51.36 PhP1.OO - ; US$0.0195 [F ISCALYEAR January 1 - December 31 ASEAN Association of Southeast NCR National Capital Region AsianNations NGAS New Government Accountirlg AMC Asset Management Company System BIR Bureau of Internal Revenue NGO Non-Government Orgarrization I BOC Bureau of Customs hI PL Non-Performing Loan ; BOT Build Operate Transfer NRM National Resource and I' BSP Bangko Sentral ng Pilipinas Management j CMDC Capital Markets Development NSCB National Statistical I Corporation Coordination Board 1 COA Commission on Audit NSO National Statistics Office 1 COP Committee on Privatization ODA Overseas Development 1 CSC Civil Service Commission Assistance j DBM Department of Budget and OPIF Organizational Performance I Management I Indicator Framework j DOF Department of Finance PDIC Ph~lippineDeposit Insurance / DST Documentary Stamp Tax Corporation / EKB Expanded Commercial Bank PCEG Presidential Committee on / EPR Effective Protection Rate Effective Governance Reform , FIES Family Income and PPI Private Participation in Expenditure Survey Infrastructure 1 GAAP Generally Accepted Accounting PS E Philippine Stock Exchange Principles PSISSA Public Sector Institutional GDP Gross Domestic Product Strengthening and GNP Gross National Product Streamlining Agenda GOCC Government Owned and ROPOA Real and Other Properties Controlled Corporation Owned and -

Download 287.76 KB

ASIAN DEVELOPMENT BANK RRP: PHI 31655 REPORT AND RECOMMENDATION OF THE PRESIDENT TO THE BOARD OF DIRECTORS ON A PROPOSED LOAN AND TECHNICAL ASSISTANCE GRANT TO THE REPUBLIC OF THE PHILIPPINES FOR THE NONBANK FINANCIAL GOVERNANCE PROGRAM October 2001 CURRENCY EQUIVALENTS (as of 10 October 2001) Currency Unit – Peso (P) P1.00 = $0.02 $1.00 = P51.90 ABBREVIATIONS ADAPS – automated debt auction processing system ADB – Asian Development Bank ASEAN – Association of Southeast Asian Nations BOA – Board of Accountancy BSP – Bangko Sentral ng Pilipinas CMDP – Capital Market Development Program CPA – certified public accountant DOF – Department of Finance DST – documentary stamp tax DVP – delivery-versus-payment FSAP – Financial Sector Assessment Program GDP – gross domestic product GNP – gross national product GSED – Government securities eligible dealers IAS – international accounting standards IMF – International Monetary Fund IOSCO – International Organization of Securities Commissions IPO – initial public offering IRR – implementing rules and regulations LIBOR – London interbank offered rate MIS – management information system NBFI – nonbank financial institution NFG – nonbank financial governance NPL – nonperforming loan PCDI – Philippine Central Depository, Inc. PDIC – Philippine Deposit Insurance Corporation PICPA – Philippine Institute of Certified Public Accountants PNB – Philippine National Bank PRC – Professional Regulation Commission PSE – Philippine Stock Exchange QB – quasi bank RTGS – real time gross settlement SCCP – Securities Clearing Corporation of the Philippines SDR – special drawing rights SEC – Securities and Exchange Commission SRC – Securities Regulation Code SRO – self-regulatory organization TA – technical assistance USAID – United States Agency for International Development NOTE In this report, "$" refers to US dollars. CONTENTS Page LOAN AND PROGRAM SUMMARY ii I. THE PROPOSAL 1 II. INTRODUCTION 1 III. -

The Prospectus Is Being Displayed in the Website to Make the Prospectus Accessible to More Investors. the Pse Assumes No Respons

THE PROSPECTUS IS BEING DISPLAYED IN THE WEBSITE TO MAKE THE PROSPECTUS ACCESSIBLE TO MORE INVESTORS. THE PSE ASSUMES NO RESPONSIBILITY FOR THE CORRECTNESS OF ANY OF THE STATEMENTS MADE OR OPINIONS OR REPORTS EXPRESSED IN THE PROSPECTUS. FURTHERMORE, THE STOCK EXCHANGE MAKES NO REPRESENTATION AS TO THE COMPLETENESS OF THE PROSPECTUS AND DISCLAIMS ANY LIABILITY WHATSOEVER FOR ANY LOSS ARISING FROM OR IN RELIANCE IN WHOLE OR IN PART ON THE CONTENTS OF THE PROSPECTUS. ERRATUM Page 51 After giving effect to the sale of the Offer Shares and PDRs under the Primary PDR Offer (at an Offer price of=8.50 P per Offer Share and per PDR) without giving effect to the Company’s ESOP, after deducting estimated discounts, commissions, estimated fees and expenses of the Combined Offer, the net tangible book value per Share will be=1.31 P per Offer Share. GMA Network, Inc. GMA Holdings, Inc. Primary Share Offer on behalf of the Company of 91,346,000 Common Shares at a Share Offer Price of=8.50 P per share PDR Offer on behalf of the Company of 91,346,000 PDRs relating to 91,346,000 Common Shares and PDR Offer on behalf of the Selling Shareholders of 730,769,000 PDRs relating to 730,769,000 Common Shares at a PDR Offer Price of=8.50 P per PDR to be listed and traded on the First Board of The Philippine Stock Exchange, Inc. Sole Global Coordinator, Bookrunner Joint Lead Manager, Domestic Lead Underwriter and Lead Manager and Issue Manager Participating Underwriters BDO Capital & Investment Corporation First Metro Investment Corporation Unicapital Incorporated Abacus Capital & Investment Corporation Pentacapital Investment Corporation Asian Alliance Investment Corporation RCBC Capital Corporation UnionBank of the Philippines Domestic Selling Agents The Trading Participants of the Philippine Stock Exchange, Inc. -

Domestic Branch Directory BANKING SCHEDULE

Domestic Branch Directory BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays cor Gen. Araneta St. and Aurora Blvd., Cubao, Quezon 1 Q.C.-Cubao Main 911-2916 / 912-1938 9:00 AM – 4:00 PM City 912-3070 / 912-2577 / SRMC Bldg., 901 Aurora Blvd. cor Harvard & Stanford 2 Q.C.-Cubao-Harvard 913-1068 / 912-2571 / 9:00 AM – 4:00 PM Sts., Cubao, Quezon City 913-4503 (fax) 332-3014 / 332-3067 / 3 Q.C.-EDSA Roosevelt 1024 Global Trade Center Bldg., EDSA, Quezon City 9:00 AM – 4:00 PM 332-4446 G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 4 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Elliptical Road cor. Kalayaan Avenue, Diliman, Quezon 920-3353 / 924-2660 / 5 Q.C.-Elliptical Road 9:00 AM – 4:00 PM City 924-2663 Aurora Blvd., near PSBA, Brgy. Loyola Heights, 421-2331 / 421-2330 / 6 Q.C.-Katipunan-Aurora Blvd. 9:00 AM – 4:00 PM Quezon City 421-2329 (fax) 335 Agcor Bldg., Katipunan Ave., Loyola Heights, 929-8814 / 433-2021 / 7 Q.C.-Katipunan-Loyola Heights 9:00 AM – 4:00 PM Quezon City 433-2022 February 07, 2014 : G/F, Linear Building, 142 8 Q.C.-Katipunan-St. Ignatius 912-8077 / 912-8078 9:00 AM – 4:00 PM Katipunan Road, Quezon City 920-7158 / 920-7165 / 9 Q.C.-Matalino 21 Tempus Bldg., Matalino St., Diliman, Quezon City 9:00 AM – 4:00 PM 924-8919 (fax) MWSS Compound, Katipunan Road, Balara, Quezon 927-5443 / 922-3765 / 10 Q.C.-MWSS 9:00 AM – 4:00 PM City 922-3764 SRA Building, Brgy. -

The Politics of Economic Reform in the Philippines the Case of Banking Sector Reform Between 1986 and 1995

The Politics of Economic Reform in the Philippines The Case of Banking Sector Reform between 1986 and 1995 A thesis submitted for the degree of PhD School of Oriental and African Studies (SOAS) University of London 2005 Shingo MIKAMO ProQuest Number: 10673052 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10673052 Published by ProQuest LLC(2017). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 2 Abstract This thesis is about the political economy of the Philippines in the process of recovery from the ruin of economic crisis in the early 1980s. It examines the dynamics of Philippine politics by focussing on banking sector reform between 1986 and 1995. After the economic turmoil of the early 1980s, the economy recovered between 1986 and 1996 under the Aquino and Ramos governments, although the country is still facing numerous economic challenges. After the "Asian currency crisis" of 1997, the economy inevitably decelerated again. However, the Philippines was seen as one of the economies least adversely affected by the rapid depreciation of its currency. The existing literature tends to stress the roles played by international financial structures, the policy preferences of the IMF, the World Bank and the US government and the interests of the dominant social force as decisive factors underlying economic and banking reform policy-making in the Philippines. -

ROBINSONS LAND CORPORATION 43Rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE

ROBINSONS LAND CORPORATION 43rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE. COR. POVEDA RD. ORTIGAS CENTER, PASIG CITY TEL. NO.: 633-7631, 637-1670, 240-8801 FAX NO.: 633-9387 OR 633-9207 July 10, 2012 PHILIPPINE STOCK EXCHANGE, INC. 3rd Floor, Philippine Stock Exchange Ayala Triangle, Ayala Avenue Makati City Attention: Ms. Janet A. Encarnacion Head – Disclosure Department PHILIPPINE DEALING AND EXCHANGE CORP. 37/F, Tower 1, The Enterprise Center 6766 Ayala Avenue corner Paseo de Roxas, Makati City Attention: Mr. Cesar B. Crisol President and Chief Operating Officer Re: Robinsons Land Corporation (RLC) List of Top 100 Stockholders and PCD Participants Gentlemen: In compliance with PSE Memo for Brokers No. 225-2003, please find attached the following. 1. List of Top 100 Stockholders of RLC as of June 30, 2012. 2. List of Top 100 PCD Participants of RLC as of June 30, 2012. Thank you. Very truly yours, ROSALINDA F. RIVERA Corporate Secretary /lbo BPI STOCK TRANSFER OFFICE ROBINSONS LAND CORPORATION TOP 100 STOCKHOLDERS AS OF JUNE 30, 2012 RANK STOCKHOLDER NUMBER STOCKHOLDER NAME NATIONALITY CERTIFICATE CLASS OUTSTANDING SHARES PERCENTAGE TOTAL 1 10003137 J. G. SUMMIT HOLDINGS, INC. FIL U 2,496,114,787 60.9725% 2,496,114,787 29/F GALLERIA CORPORATE CTR. EDSA COR. ORTIGAS AVE. MANDALUYONG CITY 2 16012118 PCD NOMINEE CORPORATION (NON-FILIPINO) NOF U 1,023,189,383 24.9934% 1,023,189,383 37/F THE ENTERPRISE CENTER TOWER 1, COR. PASEO DE ROXAS, AYALA AVENUE, MAKATI CITY 3 16012119 PCD NOMINEE CORPORATION (FILIPINO) FIL U 539,962,142 13.1896% 539,962,142 37/F THE ENTERPRISE CENTER TOWER 1, COR. -

List of BDO Branches Authorized to Exchange Foreign Currencies As of (March 8, 2021)

List of BDO Branches Authorized to Exchange Foreign Currencies as of (March 8, 2021) I. US Dollar (USD) – All BDO Branches II. Other Currencies • Australian Dollar (AUD) • Japanese Yen (JPY) • Bahrain Dinar (BHY) • Korean Won (KRW) • British Pound (GBP) • Saudi Rial (SAR) • Brunei Dollar (BND) • Singapore Dollar (SGD) Chinese Yuan (CNY) • Canadian Dollar (CAD) • Swiss Frank (CHF) • Euro (EUR) • Taiwan Dollar (TWD) • Hongkong Dollar (HKD) • Thailand Baht (THB) • Indonesian Rupiah (IDR) • UAE Dirham (AED) 1 A Place - Coral Way 1 A. Arnaiz – Paseo 2 A. Bonifacio Ave. - Balintawak 2 A. Arnaiz-San Lorenzo Village 3 A. Santos - St. James 3 A. Santos - St. James 4 Acropolis - E. Rodriguez Jr. 4 ADB Avenue Ortigas 5 ADB Avenue Ortigas 5 Alabang Hills 6 Alabang - Madrigal Ave 6 Alabang - Madrigal Ave 7 Angeles City – Miranda 7 Araneta Center Ali Mall II 8 Angono – M.L. Quezon Avenue 8 Arranque 9 Arranque 9 Asia Tower - Paseo 10 Arranque - T. Alonzo 10 Aurora Blvd. - Broadway Centrum 11 Asia Tower - Paseo 11 Aurora Blvd - Notre Dame 12 Aurora Blvd - Broadway Centrum 12 Aurora Blvd. - Yale 13 Aurora Blvd - Notre Dame 13 Ayala Alabang - Richville Center 14 Aurora Blvd. - Yale 14 Ayala Avenue - People Support 15 Ayala Alabang - Richville Center 15 Ayala Avenue - SGV1 Bldg 16 Ayala Avenue - People Support 16 Ayala Triangle 1 17 Ayala Avenue - SGV1 Bldg 17 Baclaran 18 Ayala – Rufino 18 Bacolod – Araneta 19 Baclaran 19 Bacolod - Capitol Shopping 20 Bacolod – Araneta 20 Baguio - Session Road 21 Bacolod - Capitol Shopping 21 Baguio - Marcos Highway Centerpoint 22 Bacolod – Gonzaga 22 Banawe - Agno 23 Bacoor - Aguinaldo Highway 23 Banawe - Amoranto 24 Bagtikan – Chino Roces Avenue 24 Batangas - Sto. -

Copy of 2020 Acas Website Updating Part2.Xlsx

PHILIPPINE NATIONAL BANK Domestic Branches as of February 22, 2021 NO. BRANCH NAME ADDRESS 1 ABRA-BANGUED McKinley corner Peñarrubia Streets, Zone 4, Bangued, Abra 2 ABRA-BANGUED-MAGALLANES Taft corner Magallanes Streets, Zone 5, Bangued, Abra 3 AGOO-CONSOLACION Corner Verceles Street, Consolacion Agoo, La Union 4 AGOO-SAN ANTONIO B&D Building National Highway, San Antonio, Agoo, La Union 5 AGUSAN DEL SUR-BAYUGAN CITY Mendoza Square, Narra Avenue, Poblacion, Bayugan City, Agusan del Sur 6 AGUSAN DEL SUR-SAN FRANCISCO Roxas Street, Barangay 4, San Francsico, Agusan del Sur 7 AKLAN-CATICLAN Edsa Building, National Road, Caticlan, Malay, Aklan 8 AKLAN-KALIBO-MARTELINO 0624 S. Martelino Street, Kalibo, Aklan 9 AKLAN-KALIBO-PASTRANA 0508 G. Pastrana Street, Kalibo, Aklan 10 ALAMINOS CITY-QUEZON AVE. Quezon Avenue, Poblacion, Alaminos City, Pangasinan 11 ALBAY-DARAGA Baylon Compound, Market Site, Rizal Street, Daraga, Albay 12 ALBAY-LIGAO San Jose Street, Dunao, Ligao City, Albay 13 ALBAY-POLANGUI National Road, Ubaliw, Polangui, Albay 14 ALBAY-TABACO Ziga Avenue corner Bonifacio Street, Tayhi, Tabaco City 15 ANGELES-MACARTHUR HIGHWAY V&M Building Barangay Sto Cristo, MacArthur Highway, Angeles City, Pampanga 16 ANGELES-STO. ROSARIO 730 Santo Rosario Street, Angeles City, Pampanga 17 ANTIPOLO-CIRCUMFERENTIAL Circumferential Road, Barangay Dalig, Antipolo City, Rizal 18 ANTIPOLO-P. OLIVEROS 89 P. Oliveros Street, Kapitolyo Arcade, San Roque, Antipolo City, Rizal G/F, Unit 2, Antipolo Triangle Mall, Sen. L. Sumulong Memorial Circle, Brgy. San Jose, Antipolo City, 19 ANTIPOLO-SUMULONG MEM. CIRCLE Rizal 20 ANTIPOLO-SUMULONG-MASINAG F. N. Crisostomo Building 2, Sumulong Highway, Mayamot, Antipolo City, Rizal 21 ANTIQUE-SAN JOSE Calixto O. -

BDO Unibank, Inc. List of Branches As of February 2020

BDO Unibank, Inc. List of Branches as of February 2020 NO. BRANCH NAME ADDRESS 1 6780 AYALA AVENUE G/F 6780 Ayala Avenue Bldg., 6780 Ayala Avenue, Brgy. San Lorenzo, Makati City 2 A PLACE - CORAL WAY G/F A Place, Coral Way Drive, MOA Complex, Central Business Park 1, Island A, Pasay City 3 A. ARNAIZ - PASEO G/F Joni`s Bldg., 832 Arnaiz Ave. corner Edades St., Makati City 4 A. ARNAIZ-SAN LORENZO VILLAGE L & R Bldg., 1018 A. Arnaiz Avenue, Makati City 5 A. BONIFACIO AVE. - CLOVERLEAF 2/f, Space No. 201a, Ayala Malls Cloverleaf, A. Bonifacio Avenue, Brgy. Balingasa, Quezon City Unit R1 G/F, Hollywood Garden Square Bldg., 1709 A. Mabini St. cor. Gen Malvar St, Brgy. 699, Zone 076, 6 A. MABINI - GEN. MALVAR Malate Manila 7 A. SANTOS - ST. JAMES 8406 A. Santos Avenue, Sucat Parañaque City 1700 8 ABRA - BANGUED Unit 12, The Rosario Bldg., Taft St. corner Magallanes St., 2800 Bangued, Abra Stall No. 22 East Wing, G/F ELJCC Bldg. Sgt. E.A. Esguerra Avenue corner Mother Ignacia St., Brgy. 9 ABS CBN - MOTHER IGNACIA ST. South Triangle, Quezon City 10 ACROPOLIS - E. RODRIGUEZ JR. G/F The Spa Bldg., E. Rodriguez, Jr. Ave., Brgy. Bagumbayan, Quezon City 11 ADB AVENUE ORTIGAS Robinson`s PCIBank Tower, ADB Avenue, Ortigas Center, 1600 Pasig City 12 ADRIATICO - STA. MONICA 1347 Adriatico near corner Sta. Monica across Robinson’s Place Manila, Brgy. 669, Ermita, Manila AGUSAN DEL SUR - SAN FRANCISCO G/F Stall 28 & 29, Gaisano Grand Mall San Francisco, Davao-Agusan National Highway, Brgy. -

2010 BDO Annual Report

We find ways® BDO Corporate Center 7899 Makati Avenue, Makati City Tel. 840-7000 www.bdo.com.ph 2010 ANNUAL REPORT Production Corporate Affairs, BDO Marketing Communications Design and Concept Xpress Media Philippines, Inc. Photography Wig Tysmans and Francis Rivera Printing Transprint Corporation 2010 Annual Report We find ways® Table of CONTENTS 01 Financial Highlights 02 Message from the Chairman Emeritus 04 Message from the Chairman 06 Message from the Review of Operations President 35 Statements of Income 08 Review of Operations: Economic Environment 36 Management Directory 10 Review of Operations: 38 Products and Services Operational Highlights 39 BDO Group of 18 Accolades Companies 20 Corporate Governance 40 Branch Directory 24 Corporate Social Responsibility Corporate Social Responsibility 28 Board of Directors 30 Directors’ Profile 33 Statement of Management’s Responsibility for Financial Statements 34 Statements of Financial Position Products and Services We find ways CORPORATE PROFILE he product of a merger heralded as CORPORATE MISSION unprecedented in size and scale in the Philippine To be the preferred bank in every banking industry, Banco De Oro Unibank (BDO) market we serve by consistently providing innovative products today represents a firm consolidation of distinct and flawless delivery of services, strengths and advantages built over the years by proactively reinventing ourselves T to meet market demands, creating the entities behind its history. BDO is an institution that shareholders value through superior honors its past, continues to improve on its present, and returns, cultivating in our people a moves towards the future with confidence and strength. sense of pride and ownership, and striving to be always better than what BDO is a full-service universal bank.