Download 117.99 KB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Frequently Asked Questions on What Is Pesonet?

Frequently Asked Questions on What is PESONet? PESONet is a new electronic fund transfer service that enables customers of participating banks, e- money issuers or mobile money operators to transfer funds in Philippine Peso currency to another customer of other participating banks, e-money issuers or mobile money operators in the Philippines. It is more inclusive platform for Electronic Fund Transfers which will make G2B(Government-to- Business) and G2C(Government-to-Consumer) payments more practical, convenient, fast, and secure. What is the purpose of PESONet? Through PESONet, businesses, government, and individuals will be able to conveniently pay or transfer funds from their account to one or multiple recipient accounts in other financial institutions. PESONet is the perfect alternative to the still widely used paper-based check system. What are the features of PESONet? What are the uses of PESONet? How does PESONet work? Customers instruct their financial institution to send credit instructions to other financial institutions via online banking, mobile banking or over-the-counter transaction. They need to provide the payees’ financial institution, account number, and amount. The credit instruction is transmitted by the financial institution to the clearing switch operator, which currently is the Philippine Clearing House Corporation (PCHC). The funds are settled in the respective financial institutions demand deposit accounts held in Bangko Sentral ng Pilipinas (BSP) through BSP’s Philippine Payments and Settlement System (PhilPaSS). Upon settlement, the beneficiary’s or payee’s financial institution will credit the payee's account. How long does it take to transfer funds via PESONet? The availability of funds to the receiving account shall depend on the facility used to carry out your transaction. -

Sec Form 20-Is

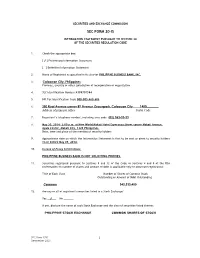

SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ √ ] Preliminary Information Statement [ ] Definitive Information Statement 2. Name of Registrant as specified in its charter PHILIPPINE BUSINESS BANK, INC. 3. Caloocan City, Philippines Province, country or other jurisdiction of incorporation or organization 4. SEC Identification Number A199701584 5. BIR Tax Identification Code 000-005-469-606 6. 350 Rizal Avenue corner 8th Avenue Gracepark, Caloocan City 1400________ Address of principal office Postal Code 7. Registrant’s telephone number, including area code (02) 363-33-33 8. May 30, 2014- 2:00 p.m. at New World Makati Hotel Esperanza Street corner Makati Avenue, Ayala Center, Makati City, 1228 Philippines. Date, time and place of the meeting of security holders 9. Approximate date on which the Information Statement is first to be sent or given to security holders on or before May 09, 2014. 10. In case of Proxy Solicitations: PHILIPPINE BUSINESS BANK IS NOT SOLICITING PROXIES. 11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding or Amount of Debt Outstanding Common 343,333,400 12. Are any or all of registrant's securities listed in a Stock Exchange? Yes __√___ No _______ If yes, disclose the name of such Stock Exchange and the class of securities listed therein: PHILIPPINE STOCK EXCHANGE COMMON SHARES OF STOCK SEC Form 17-IS 1 December 2003 PHILIPPINE BUSINESS BANK, INC. -

(“Medco”) Is a Company Incorporated in the Republic of Philippines with Limited Liability Whose Shares Are Listed on the Philippines Stock Exchange, Inc

Medco Holdings, Inc (“Medco”) is a company incorporated in the Republic of Philippines with limited liability whose shares are listed on The Philippines Stock Exchange, Inc. (“PSE”). Lippo China Resources Limited (“LCR”) is currently interested in approximately 70.7 per cent. of the issued share capital of Medco, making it a subsidiary of LCR. Lippo Limited (“Lippo”) owns shares representing approximately 71.1 per cent. of the issued share capital of LCR. Accordingly, each of LCR and Medco is a subsidiary of Lippo. The quarterly report of Medco ended 30th June, 2005 (the “Quarterly Report”) was released on the website of PSE today. The following is a reproduction of the Quarterly Report for information purpose only. COVER SHEET 39652 SEC Registration Number MEDCO HOLD I NGS , I NC . AND SUBS I D I A RY (Company’s Full Name) 31st Floor,Rufino Pacific Tower, 6784 Ayala Avenue , Makat i Ci ty (Business Address: No. Street City/Town/Province) Dionisio E. Carpio, Jr. 811-0465 (Contact Person) (Company Telephone Number) 09 30 17-Q Month Day (Form Type) Month Day 2004 AMENDED (Annual Meeting) (Secondary License Type, If Applicable) Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. SECURITIES AND EXCHANGE COMMISSION Metro Manila, Philippines ______________________ SEC FORM 17-Q QUARTERLY REPORT PURSUANT TO SECTION 11 OF THE REVISED SECURITIES ACT AND RSA RULE 11(a)-1(b)(2) THEREUNDER ______________________ 1. -

World Bank Document

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized AWorld Rank ' = Dcrelopmeni : Currency Un it - Peso : $1.00 - E;: PhP51.36 PhP1.OO - ; US$0.0195 [F ISCALYEAR January 1 - December 31 ASEAN Association of Southeast NCR National Capital Region AsianNations NGAS New Government Accountirlg AMC Asset Management Company System BIR Bureau of Internal Revenue NGO Non-Government Orgarrization I BOC Bureau of Customs hI PL Non-Performing Loan ; BOT Build Operate Transfer NRM National Resource and I' BSP Bangko Sentral ng Pilipinas Management j CMDC Capital Markets Development NSCB National Statistical I Corporation Coordination Board 1 COA Commission on Audit NSO National Statistics Office 1 COP Committee on Privatization ODA Overseas Development 1 CSC Civil Service Commission Assistance j DBM Department of Budget and OPIF Organizational Performance I Management I Indicator Framework j DOF Department of Finance PDIC Ph~lippineDeposit Insurance / DST Documentary Stamp Tax Corporation / EKB Expanded Commercial Bank PCEG Presidential Committee on / EPR Effective Protection Rate Effective Governance Reform , FIES Family Income and PPI Private Participation in Expenditure Survey Infrastructure 1 GAAP Generally Accepted Accounting PS E Philippine Stock Exchange Principles PSISSA Public Sector Institutional GDP Gross Domestic Product Strengthening and GNP Gross National Product Streamlining Agenda GOCC Government Owned and ROPOA Real and Other Properties Controlled Corporation Owned and -

Download 287.76 KB

ASIAN DEVELOPMENT BANK RRP: PHI 31655 REPORT AND RECOMMENDATION OF THE PRESIDENT TO THE BOARD OF DIRECTORS ON A PROPOSED LOAN AND TECHNICAL ASSISTANCE GRANT TO THE REPUBLIC OF THE PHILIPPINES FOR THE NONBANK FINANCIAL GOVERNANCE PROGRAM October 2001 CURRENCY EQUIVALENTS (as of 10 October 2001) Currency Unit – Peso (P) P1.00 = $0.02 $1.00 = P51.90 ABBREVIATIONS ADAPS – automated debt auction processing system ADB – Asian Development Bank ASEAN – Association of Southeast Asian Nations BOA – Board of Accountancy BSP – Bangko Sentral ng Pilipinas CMDP – Capital Market Development Program CPA – certified public accountant DOF – Department of Finance DST – documentary stamp tax DVP – delivery-versus-payment FSAP – Financial Sector Assessment Program GDP – gross domestic product GNP – gross national product GSED – Government securities eligible dealers IAS – international accounting standards IMF – International Monetary Fund IOSCO – International Organization of Securities Commissions IPO – initial public offering IRR – implementing rules and regulations LIBOR – London interbank offered rate MIS – management information system NBFI – nonbank financial institution NFG – nonbank financial governance NPL – nonperforming loan PCDI – Philippine Central Depository, Inc. PDIC – Philippine Deposit Insurance Corporation PICPA – Philippine Institute of Certified Public Accountants PNB – Philippine National Bank PRC – Professional Regulation Commission PSE – Philippine Stock Exchange QB – quasi bank RTGS – real time gross settlement SCCP – Securities Clearing Corporation of the Philippines SDR – special drawing rights SEC – Securities and Exchange Commission SRC – Securities Regulation Code SRO – self-regulatory organization TA – technical assistance USAID – United States Agency for International Development NOTE In this report, "$" refers to US dollars. CONTENTS Page LOAN AND PROGRAM SUMMARY ii I. THE PROPOSAL 1 II. INTRODUCTION 1 III. -

The Politics of Economic Reform in the Philippines the Case of Banking Sector Reform Between 1986 and 1995

The Politics of Economic Reform in the Philippines The Case of Banking Sector Reform between 1986 and 1995 A thesis submitted for the degree of PhD School of Oriental and African Studies (SOAS) University of London 2005 Shingo MIKAMO ProQuest Number: 10673052 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10673052 Published by ProQuest LLC(2017). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 2 Abstract This thesis is about the political economy of the Philippines in the process of recovery from the ruin of economic crisis in the early 1980s. It examines the dynamics of Philippine politics by focussing on banking sector reform between 1986 and 1995. After the economic turmoil of the early 1980s, the economy recovered between 1986 and 1996 under the Aquino and Ramos governments, although the country is still facing numerous economic challenges. After the "Asian currency crisis" of 1997, the economy inevitably decelerated again. However, the Philippines was seen as one of the economies least adversely affected by the rapid depreciation of its currency. The existing literature tends to stress the roles played by international financial structures, the policy preferences of the IMF, the World Bank and the US government and the interests of the dominant social force as decisive factors underlying economic and banking reform policy-making in the Philippines. -

ROBINSONS LAND CORPORATION 43Rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE

ROBINSONS LAND CORPORATION 43rd FLOOR ROBINSONS EQUITABLE TOWER ADB AVE. COR. POVEDA RD. ORTIGAS CENTER, PASIG CITY TEL. NO.: 633-7631, 637-1670, 240-8801 FAX NO.: 633-9387 OR 633-9207 July 10, 2012 PHILIPPINE STOCK EXCHANGE, INC. 3rd Floor, Philippine Stock Exchange Ayala Triangle, Ayala Avenue Makati City Attention: Ms. Janet A. Encarnacion Head – Disclosure Department PHILIPPINE DEALING AND EXCHANGE CORP. 37/F, Tower 1, The Enterprise Center 6766 Ayala Avenue corner Paseo de Roxas, Makati City Attention: Mr. Cesar B. Crisol President and Chief Operating Officer Re: Robinsons Land Corporation (RLC) List of Top 100 Stockholders and PCD Participants Gentlemen: In compliance with PSE Memo for Brokers No. 225-2003, please find attached the following. 1. List of Top 100 Stockholders of RLC as of June 30, 2012. 2. List of Top 100 PCD Participants of RLC as of June 30, 2012. Thank you. Very truly yours, ROSALINDA F. RIVERA Corporate Secretary /lbo BPI STOCK TRANSFER OFFICE ROBINSONS LAND CORPORATION TOP 100 STOCKHOLDERS AS OF JUNE 30, 2012 RANK STOCKHOLDER NUMBER STOCKHOLDER NAME NATIONALITY CERTIFICATE CLASS OUTSTANDING SHARES PERCENTAGE TOTAL 1 10003137 J. G. SUMMIT HOLDINGS, INC. FIL U 2,496,114,787 60.9725% 2,496,114,787 29/F GALLERIA CORPORATE CTR. EDSA COR. ORTIGAS AVE. MANDALUYONG CITY 2 16012118 PCD NOMINEE CORPORATION (NON-FILIPINO) NOF U 1,023,189,383 24.9934% 1,023,189,383 37/F THE ENTERPRISE CENTER TOWER 1, COR. PASEO DE ROXAS, AYALA AVENUE, MAKATI CITY 3 16012119 PCD NOMINEE CORPORATION (FILIPINO) FIL U 539,962,142 13.1896% 539,962,142 37/F THE ENTERPRISE CENTER TOWER 1, COR. -

Philequity Corner (May 8, 2017) by Wilson Sy the Hunter Games After

Philequity Corner (May 8, 2017) By Wilson Sy The Hunter Games After consolidating for more than three months between 7,100 to 7,400, the PSEi closed last Friday at 7,842. Aside from robust global markets, one of the catalysts that contributed to the PSEi’s strong move is the speculation about possible M&As in the banking sector. Speculation on RCBC takeover leads bank stocks higher Recently, there has been speculation that some banks may be in play as potential acquisition targets. This started with RCB’s gap up move on April 17. 4/12/17 5/5/17 % Chg RCB 39.00 58.70 50.5% PNB 57.50 68.65 19.4% EW 20.80 22.70 9.1% MBT 84.50 86.95 2.9% UBP 79.65 81.95 2.9% BDO 121.00 123.00 1.7% BPI 105.00 105.10 0.1% SECB 217.00 215.60 -0.6% CHIB 38.20 36.45 -4.6% Sources: Bloomberg, Wealth Research From the table above, it can be seen that RCB has risen 50.5% since April 12. Moreover, it has surged 104.2% from its bottom of 28.75 on March 22, 2016 (at the height of the AMLA investigations). Note that RCB has been rumoured to be a takeover target for several years. PNB and EastWest Bank follow RCBC’s lead Aside from RCB, both PNB and EastWest Bank (EW) gained significantly since mid-April. Not surprisingly, these three banks were trading below book value and were the cheapest among liquid banking stocks before this recent move ensued. -

Banking Laws and Jurisprudence

Banking Laws and Jurisprudence I. Universal bank A universal bank has the same powers as a commercial bank with the following additional powers: the powers of an investment house as provided in existing laws and the power to invest in non-allied enterprises.1 List of local universal banks Government-owned Development Bank of the Philippines Land Bank of the Philippines Private-owned Allied Bank Corporation Banco de Oro Universal Bank Bank of the Philippine Islands China Banking Corporation Metropolitan Bank and Trust Company Philippine National Bank Philippine Savings Bank Philtrust Bank (Philippine Trust Company) Rizal Commercial Banking Corporation Security Bank United Coconut Planters Bank II. Commercial banks In addition to having the powers of a thrift bank, a commercial bank has the power to accept drafts and issue letters of credit; discount and negotiate promissory notes, drafts, bills of exchange, and other evidences of debt; accept or create demand deposits; receive other types of deposits and deposit substitutes; buy and sell foreign exchange and gold or silver bullion; acquire marketable bonds and other debt securities; and extend credit.2 List of local commercial banks Bank of Commerce Business and Commercial Bank Philippine Veterans Bank III. Thrift bank A thrift bank has the power to accept savings and time deposits, act as a correspondent with other financial institutions and as a collection agent for government entities, issue mortgages, engage in real estate transactions and extend credit. In addition, -

Remittance Bank List of Philippines Bank Name

Remittance Bank List of Philippines Bank Name AL AMANAH ISLAMIC INVESTMENT BANK ALLBANK ANZ BANK ASIA UNITED BANK BANK OF AMERICA BANK OF CHINA BOF, INC (A Rural Bank) - (BANK OF Florida) BANGKOK BANK PUBLIC CO LTD BDO - BANCO DE ORO BDO NETWORK BANK BDO PRIVATE BANK BOC - BANK OF COMMERCE BPI - BANK OF THE PHILIPPINE ISLANDS BPI FAMILY BANK BPI DIRECT BANKO CAMALIG BANK, INC (A Rural Bank) CEBUANA LHUILLIER RURAL BANK INC CHINA BANK CHINA BANK SAVINGS CTBC BANK ( FORMER CHINA TRUST) CIMB BANK PHILIPPINES, INC. CITIBANK DBP - DEVELOPMENT BANK OF THE PHILIPPINES DEUTSCHE BANK DUNGGANON BANK EAST WEST BANK EASTWEST RURAL BANK EQUICOM SAVINGS BANK INC FIRST CONSOLIDATED BANK HSBC - HONGKONG AND SHANGHAI BANKING CORPORATION HSBC SAVINGS BANK INDUSTRIAL BANK OF KOREA ING BANK N.V. ISLA BANK INC. KEB HANA (Korea Exchange Bank) JP MORGAN CHASE BANK LBP - LAND BANK OF THE PHILIPPINES MALAYAN BANK SAVINGS AND MORTGAGE BANK INC (MALAYAN SVGS) MAYBANK PHILIPPINES INC (PNB Republic) MEGA INTL COMML BANK CO LTD (ICBC) MIZUHO BANK LTD (FUJI BANK) MUFG BANK LTD (BANK OF TOKYO) PARTNER RURAL BANK (COTABATO) INC PBCOM - PHILIPPINE BANK OF COMMUNICATIONS PHIL BUSINESS BANK PHILIPPINE VETERANS BANK PHILTRUST CO (Philtrust Bank) PNB - PHILIPPINE NATIONAL BANK (Allied Bank) PRODUCERS SAVINGS BANK CORP PSBANK - PHILIPPINE SAVINGS BANK QUEZON CAPITAL RURAL BANK INC RCBC - RIZAL COMMERCIAL BANKING CORPORATION ROBINSONS BANK CORPORATION RURAL BANK OF GUINOBATAN INC (RBGI) SECURITY BANK CORPORATION SHINHAN BANK STERLING BANK OF ASIA SUMITOMO MITSUI BANKING CORP SUN SAVINGS BANK INC THE STANDARD CHARTERED BANK UCPB - UNITED COCONUT PLANTERS BANK UCPB SAVINGS BANK UNION BANK OF THE PHILIPPINES (City Savings Bank) UNITED OVERSEAS BANK PHILIPPINES WEALTH DEVELOPMENT BANK YUANTA SAVINGS BANK PHILS INC (Tongyang) . -

Negotiable Instruments Law

Mercantile Law – Negotiable Instruments Law Case Digest DEAN’S CIRCLE 2019 – UST FACULTY OF CIVIL LAW UNIVERSITY OF SANTO TOMAS FACULTY OF CIVIL LAW LIST OF CASES Negotiable Instruments Law A. Forms and Interpretation 1. Requisites of Negotiability Equitable Banking Corporation vs. the Honorable Intermediate Appellate Court and The Edward J. Nell Co., G.R. No. 74451, May 25, 1988 Juanita Salas vs. Hon. Court of Appeals and First Finance & Leasing Corporation, G.R. No. 76788 January 22, 1990 Metropolitan Bank & Trust Company vs. Court Of Appeals, Golden Savings & Loan Association, Inc., Lucia Castillo, Magno Castillo and Gloria Castillo, G.R. No. 88866, February 18, 1991 Caltex (Philippines), Inc. vs. Court of Appeals and Security Bank and Trust Company, G.R. No. 97753, August 10, 1992 Traders Royal Bank vs. Court of Appeals, Filriters Guaranty Assurance Corporation and Central Bank of the Philippines, G.R. No. 93397, March 3, 1997 Philippine National Bank vs. Erlando T. Rodriguez and Norma Rodriguez, G.R. No. 170325, September 26, 2008 People of the Philippines vs. Gilbert Reyes Wagas, G.R. No. 157943, September 4, 2013 2. Kinds of Negotiable Instruments Philippine Education Co., inc. vs. Mauricio A. Soriano, et al., G.R. No. L-22405, June 30, 1971 Firestone Tire & Rubber Company of the Philippines vs. Court of Appeals and Luzon Development Bank, G.R. No. 113236, March 5, 2001 Philippine National Bank vs. Erlando T. Rodriguez and Norma Rodriguez, G.R. No. 170325, September 26, 2008 Prudential Bank v. Commissioner of Internal Revenue (CIR), G.R. No. 180390, July 27, 2011 B. -

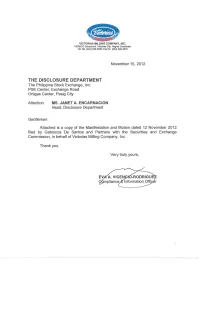

Vmc 17C Sec Manifestation and Motion

VICTORIAS..MILLING COMPANY, INC. V1CMICO Compound. Victorias City,Negros Occidental Tel. No_(034) 399-3380; Fax No. (034) 399-3675 November 15,2012 THE DISCLOSURE DEPARTMENT The Philippine Stock Exchange, Inc. PSE Center, Exchange Road Ortigas Center, Pasig City Attention: MS. JANET A. ENCARNACION Head, Disclosure Department Gentlemen: Attached is a copy of the Manifestation and Motion dated 12 November 2012 filed by Gabionza De Santos and Partners with the Securities and Exchange Commission, in behalf of Victorias Milling Company, Inc. Thank you. Very truly yours, EVj{A. VICENYtO-RODRIGU pliance%lnformation Officer ; ;; " iREPUlBUC OF THE PiI-llUPPilfllES SECUiRnJESA!MtD EXCHANGE COMMISSJON • ' . SEC Bldg." E~SA, Gri?eTl:hjIJs, Mamlaluyonfj City i>f nftS) IN TiHIE MA1TER OF THE PElITION , ~ . , ~~':¥~ FOR DECLARATION OF A. STATE Of . ~: \ l:..L2 : ' \ ~~ ! i!-'- \ 1 ~ \ 1 SUSPENSION OF PAYMB':IT; fOR l'l ," " >'''12 1\\ THE APPROVAL OF A i: :;~! , .' :.u, \\' \ R.E.H.AS. JUT.A.TION PLAN, AND THE . trlS'3~")U L..::.l.!-~ APpm~TlIVlENT Of A MANAGEMENT -~-;, W'" COMMJnEE,. SEC CASE NO.'07-97-5 VICTORJASfit,ILUNG COJVJPANY, INC. Petiiioner: ~----------------~ . , ~ MANifESTATION AtW MOTION PETUlONER VICTORIAS MlLlING COMPANY, INC. r VMC"), in the above-errlitled case, by its undersigned counsel, 10 this Honorable Commission respectfully manifests thaI there was one {'I) Board seat previously reserved lOT the Joinl Venture Partner under the Approved - RehabmtBt~on Plans r AiR?"), particularly the Proposed Alternative I Rehabiliiafion Plan, and the Debt Restructuring Agreement ("DHA") and \formerly occupied by the nominee of Tanduay Holdings, Inc ("THl") as a I conseqeeoceot its IT nfLlslon of the amount of Three Hundred Milljon Pesos (,R300;OOO,OOO.OD) into.