SEC Complaint: Thomas L. Kivisto

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Excellence in Leadership Award Winners

Excellence in Leadership Award Winners Statewide Community The Statewide Community Award recognizes an organization or company that, through specific projects or efforts, has reached across our valued differences to develop among Oklahomans a keen sense of common purpose and a more profound sense of loyalty to our state. This award has been created to promote a heightened sense of appreciation for the possibilities available when Oklahomans work together as a single statewide community. 1999 American Fidelity Assurance Company, Oklahoma City 2000 The Samuel Roberts Noble Foundation, Ardmore 2001 The CAMA Coalition, (The Oklahoma Child Abuse Multi-Disciplinary Account Coalition), Tulsa 2002 SBC, Oklahoma City 2003 The Oklahoma Educational Television Authority (OETA), Oklahoma City 2004 Oklahoma Natural Gas, a division of ONEOK, Inc., Oklahoma City 2005 Chesapeake Energy Corporation, Oklahoma City 2006 Bank of Oklahoma, N.A., Tulsa 2007 Oklahoma State Academy for State Goals, Oklahoma City 2008 Cox Oklahoma, Oklahoma City 2009 Griffin Communications, Oklahoma City 2010 OGE Energy Corp., Oklahoma City 2011 Blue Cross and Blue Shield of Oklahoma, Tulsa 2012 BancFirst, Oklahoma City 2013 The Oklahoma City Thunder, Oklahoma City 2014 The Chickasaw Nation, Ada 2015 Oklahoma Heritage Association & Gaylord-Pickens Museum, Oklahoma City 2016 George Kaiser Family Foundation, Tulsa 2017 Oklahoma Energy Resources Board (OERB), Oklahoma City 2018 Arvest Bank, Oklahoma City 2019 Home Creations, Moore 2020 McNellie’s Group, Tulsa Business Leadership -

Business Location Data

BUSINESS LOCATION DATA #TulsaChamber TULSA BUSINESS LOCATION DATA Facilities Business Environment · Industrial Buildings 4 · Largest Employers 14 · Office Buildings 4 · Incentives 14 · Land 5 · Taxes 16 · Retail Buildings 5 · Community Data 17 · Business Announcements 18 Utilities · Electricity 6 Quality of Life · Natural Gas 6 · Tulsa MSA Demographics 19 · Water & Sewer 6 · Cost of Living Index 20 · Telecommunications 7 · Education 20 · Health Care 23 · Culture & Recreation 24 Workforce · · Labor Force 8 Climate 25 · · Wage & Salary Employment 8 Other Facts 25 · Employment by Sector 8 · Unemployment Rates 9 Location & Maps · Wage Rates 9 · Tulsa & Region Maps 26 · Union Information 10 · Workers’ Compensation 10 Market Access · Air 11 · Motor Freight 12 · Rail 13 · Waterway 13 The Tulsa Business Location Data is a publication of: Tulsa Regional Chamber, Economic Development Williams Center Tower I One West Third Street, Suite 100 Tulsa, OK 74103 Ph: 918.585.1201 · 800.624.6822 Fx: 918.585.8386 GrowMetroTulsa.com FACILITIES A customized listing of available properties and sites is available through the Tulsa Regional Chamber’s Economic Development Division: 800.624.6822 or 918.585.1201 INDUSTRIAL BUILDINGS Market size – 78,879,954 sq. ft. Available sq. ft. – 4,326,767, Vacancy -- 5.5% Rental rates – $4.47 to $6.86 sq. ft. triple net 2015 city construction permits – 35 issued for 2,890,100 sq. ft. or $43.6 million INDUSTRIAL MARKET SUMMARY SUBMARKET LEASABLE SQ. FT. VACANT SQ. FT. LEASE RATE $ VACANCY % Northeast 21,858,879 699,484 6.0 3.2 Northwest 13,765,344 151,419 4.47 1.1 South Central 18,134,996 1,614,015 6.40 8.9 Southeast 15,006,532 1,305,568 6.86 8.7 Southwest 10,114,203 556,281 4.78 5.5 Market Total 78,879,954 4,326,767 5.59 5.5 CBRE Oklahoma Tulsa Industrial Mid-Year 2016 & Research Wizard City/County Library Aug. -

Tortoise North American Energy Infrastructure Fund a Sub-Fund of Tortoise SICAV

Tortoise North American Energy Infrastructure Fund A sub-fund of Tortoise SICAV 3Q 2019 QUARTERLY COMMENTARY Investment strategy The broader energy sector, as represented by the S&P Energy Select Sector® Index, fell during the third quarter, returning -6.2%, bringing year-to-date performance to 6.1%. The fund will primarily invest in Energy demand is at an all-time high and a global energy transition is taking place securities of North American reducing global carbon emissions while meeting that demand. We are witnessing the midstream energy infrastructure next phase of U.S. energy independence emerge as the U.S. becomes a net exporter companies. Midstream energy of low-cost energy to the rest of the world. Against that backdrop, approximately $15 infrastructure companies own and trillion1 of investment in global energy infrastructure is required to support this energy operate a network of asset systems transition, making it a compelling opportunity for midstream energy investors. that transport, store, distribute, North American pipeline sector update gather and process natural gas, Midstream sector performance fared slightly better than broader energy for the third quarter with natural gas liquids (primarily the Tortoise North American Pipeline IndexSM return of -0.8% and the Tortoise MLP Index® return propane), crude oil or refined of -4.3%, bringing year to date performance to 22.2% and 14.2%, respectively. Phillips 66 Partners petroleum products. LP (PSXP) announced the elimination of its Incentive Distribution Rights (IDRs) in the third quarter. As the era of simplification comes to a close, the results have advanced the midstream sector and accomplished widespread cost of capital and corporate governance improvements. -

Pipeline and Processing Fac... - Pipeline Projects with Length Greater Than 20 Miles

12/29/2015 Pipeline and Processing Fac... - Pipeline projects with Length Greater than 20 Miles Pipeline projects with DEC-29-2015 Pipeline and Processing Facilities : SAVED REPORTS Length Greater than 1:37 PM 20 Miles Pipeline projects with Length Greater than 20 Miles Holding Company or Parent Operating Company: Project Status Project Project Name: Length Organization: Type: (New Miles) AK (6 Pipeline projects) Energia Cura Fairbanks Pipeline Doubtful New Arctic Fox (Fairbanks Pipeline) 443 Company Linc Energy Linc Energy On New Umiat Oil Field Pipeline 80 Hold/Postponed Alaska Housing Finance Alaska Gasline On New Alaska Stand Alone Pipeline (ASAP) 737 Corporation Development Hold/Postponed Corporation BP BP Under New Point Thomson Gas Field 22 Construction NovaGold Resources Inc. Donlin Gold, LLC Advanced New Donlin Gold 312 Development Alaska LNG Early New Alaska LNG (AKLNG) 800 Development TOT 2,394 AL (6 Pipeline projects) Southern Company Alabama Power Under New Gaston Natural Gas Pipeline 30 Construction Spectra Energy Spectra Energy Advanced New Sabal Trail 515 Development Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 1 20 Pipeline Company LLC Development Miller Energy Resources Early New Trans - Foreland Pipeline (TFPL) system 23 Development Laclede Gas Alagasco On-going Replacement Alagasco Pipeline replacement program 850 PRP Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 2 and 3 24 Pipeline Company LLC Development TOT 1,462 Alberta (43 Pipeline projects) TransCanada Imperial Oil Early New Mackenzie Gas Project 758 Development Enbridge Inc. Enbridge Income Fund Advanced New Northern Gateway Pipeline (westward 731 Development crude for export) TransCanada TransCanada Advanced New Keystone XL 1,661 Development Enhance Energy Inc. -

Case Study: Semgroup ESSBASE & PLANNING REPLACE MANUAL, SPREADSHEET-DRIVEN REPORTING

Case Study: SemGroup ESSBASE & PLANNING REPLACE MANUAL, SPREADSHEET-DRIVEN REPORTING SERVICE Business Challenge Strategy Infrastructure Headquartered in Tulsa, Oklahoma, SemGroup is a transporter of oil and Implementation natural gas through pipelines from refineries to end users, as well as a Upgrade & Migration manufacturer and seller of asphalt. After emerging from bankruptcy, SemGroup Managed Services implemented Oracle Hyperion Financial Management (HFM) and Hyperion Training Strategic Finance (HSF) to support financial close and consolidations as well as strategic long-range modeling. SOLUTION Planning & Forecasting Once HFM and HSF were successfully implemented and in use, it shone a light Financial Close & Consolidation on the shortcomings of several key management activities for SemGroup’s FP&A Master Data Management and accounting teams. Key challenges they were facing included: Business Intelligence Big Data • Internal financial management reporting for actuals was extremely time consuming and manual. Requests for different views of the data required extensive effort to pull the data, format, and send the reported INDUSTRY results to senior leadership. New requests required a long delay to meet. Consumer Products The HSF and HFM applications were structured differently, so combining Energy & Utilities data for reporting and analysis took additional time. Financials Healthcare • Forecasting and budgeting for SemGroup and business units was Industrials Excel-focused and manually intensive. The business unit (Rose Rock) Information Technology spent over 80 percent of their time managing dozens of spreadsheets. Materials In addition, spreadsheets from operational, corporate, treasury, and finance departments were needed to create each forecast and plan. 877.828.USAS | [email protected] | www.us-analytics.com The spreadsheet-based planning process came with several challenges: • Timeliness of the plan was difficult because the underlying drivers to support the plan process were not clear. -

Semgroup and Exterran Holdings Announce New Gas Processing Plant Intended to Meet Growing Demand for Midstream Services

SemGroup and Exterran Holdings Announce New Gas Processing Plant Intended to Meet Growing Demand for Midstream Services November 22, 2011 SemGas To Team with Exterran TULSA, Okla., Nov 22, 2011 (BUSINESS WIRE) -- SemGroup(R) Corporation (NYSE:SEMG) and Exterran Holdings, Inc. (NYSE: EXH) announce the development of a new gas processing plant for SemGas(R),L.P. The new plant and equipment are needed to meet the growing demand for midstream services in the Mississippi play. "SemGroup is focused on capturing the growing demand for midstream services," says Norm Szydlowski, President and Chief Executive Officer of SemGroup. "We are excited about this new opportunity for growth and what it means for our business and shareholders." SemGas(R) has entered into a Letter of Intent with Exterran, a global leader in full service natural gas compression and processing, to purchase a new gas processing plant and associated compression equipment. It is expected that the plant will be designed and fabricated by Exterran to handle a throughput of 60 million cubic feet per day of gas, and will feature state-of-the-art cryogenic technology for natural gas liquid extraction and enhanced ethane recovery. Exterran offers pre-engineered processing plants in 60, 150 and 200 million cubic feet per day nominal capacity to meet the demanding performance and delivery needs of today's leading midstream service providers. "The agreement with Exterran is another step forward in our strategy to become the service provider of choice among active producers in the Mississippi Zone," says Wayne Ziegler, Vice President of SemGas. "We believe there is an immediate and growing need for more processing capacity in SemGas' Northern Oklahoma system." Matt Sucy, Regional Vice President for Exterran, adds, "Commodity pricing in today's market dictates an ever increasing focus on natural gas liquids extraction. -

Semgroup Corporation

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 SCHEDULE 14A INFORMATION PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE SECURITIES EXCHANGE ACT OF 1934 Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐ Check the appropriate box: ☐ Preliminary Proxy Statement ☐ CONFIDENTIAL, FOR USE OF THE COMMISSION ONLY (AS ☒ Definitive Proxy Statement PERMITTED BY RULE 14A-6(E)(2)) ☐ Definitive Additional Materials ☐ Soliciting Material Pursuant to Rule 14a-12 SemGroup Corporation (Name of Registrant as Specified in Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): ☒ No fee required. ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee was calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ☐ Fee paid previously with preliminary materials. ☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: Table of Contents 2015SemGroup StatementProxy MayNotice 14, of 2015 Annual Meeting of Stockholders to be held on Table of Contents SEMGROUP CORPORATION Two Warren Place 6120 S. -

Energy Transfer Lp

SECURITIES AND EXCHANGE COMMISSION FORM 10-Q Quarterly report pursuant to sections 13 or 15(d) Filing Date: 2019-11-07 | Period of Report: 2019-09-30 SEC Accession No. 0001276187-19-000051 (HTML Version on secdatabase.com) FILER Energy Transfer LP Mailing Address Business Address 8111 WESTCHESTER DRIVE 8111 WESTCHESTER DRIVE CIK:1276187| IRS No.: 300108820 | State of Incorp.:DE | Fiscal Year End: 1231 SUITE 600 SUITE 600 Type: 10-Q | Act: 34 | File No.: 001-32740 | Film No.: 191200992 DALLAS TX 75225 DALLAS TX 75225 SIC: 4922 Natural gas transmission 2149810700 Copyright © 2019 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended September 30, 2019 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 1-32740 ENERGY TRANSFER LP (Exact name of registrant as specified in its charter) Delaware 30-0108820 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 8111 Westchester Drive, Suite 600, Dallas, Texas 75225 (Address of principal executive offices) (zip code) (214) 981-0700 (Registrant’s telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

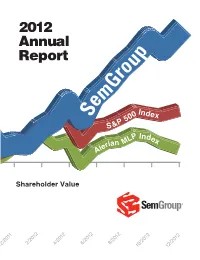

Semgroup’S Track Record of Building Shareholder Value

60% 40% 20% 0% -20% 2012 Annual Report 12/2010 2/2011 4/2011 6/2011 8/2011 Shareholder Value SemGroup 10/2011 S &P 12/2011 5 Al 00 I eria n n d ML e 2/2012 P x In d e 4/2012 x 6/2012 8/2012 10/2012 12/2012 SemGroup’s Track Record of Building Shareholder Value Purchased additional 25% interest in Glass Mountain Pipeline Launched IPO Accomplished for MLP, Rose Announced SemGroup planned Rock Midstream plans to expand stock refinancing- Completed White Cliffs begins 40% cash RRMS stock 1.95 million Pipeline to trading on interest savings begins trading barrel Cushing 150,000 barrels NYSE over 2010 on NYSE expansion per day May June March March October February November November 2010 2011 December 2012 Agreement with Eagle Contributed Announced plans Agreement Energy Company to SemStream to for Joint Venture finalized for Glass gather and process NGL Energy with Chesapeake Mountain Pipeline natural gas in the Partners for cash and Gavilon Joint Venture with Mississippi Lime Play and equity interests Chesapeake and in Oklahoma Gavilon Announced Cushing Announced plans expansion 1.95 million with Noble to additional barrels build Wattenberg Oil Trunkline in Colorado Dear Fellow Stockholders, 2012 was a year of exceptional performance for SemGroup Corporation (NYSE: SEMG). We delivered strong results at the high end of our guidance range, saw stock price increase 50% and launched new infrastructure projects to continue the growth. It is an exciting time for midstream energy. Taking advantage of the need for new infrastructure, we: • completed 1.95 million barrel expansion at our Cushing, Oklahoma terminal; • purchased an additional 25% interest in Glass Mountain Pipeline; • benefited from the growing need for the White Cliffs Pipeline where volumes increased 69% over 2011 and • increased our U.S. -

SEMGROUP CORPORATION (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2012 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number: 1-34736 SEMGROUP CORPORATION (Exact name of registrant as specified in its charter) Delaware 20-3533152 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification Number) Two Warren Place 6120 S. Yale Avenue, Suite 700 Tulsa, OK 74136-4216 (Address of principal executive offices and zip code) (918) 524-8100 (Registrant’s telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes ☒ No ☐ Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files): Yes ☒ No ☐ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. -

Carson Et Al V. Semgroup Energy Partners, L.P. Et Al 08-MD-01989

IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF OKLAHOMA IN RE SEMGROUP ENERGY PARTNERS, L.P., CASE NO. 08-MD-1989-GKF-FHM SECURITIES LITIGATION CORRECTED CONSOLIDATED SECURITIES CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE FEDERAL SECURITIES LAWS NELSON, ROSELIUS, TERRY BARROWAY TOPAZ KESSLER O’HARA & MORTON MELTZER & CHECK, LLP Douglas A. Terry (Bar Number 15855) Stuart L. Berman (admitted pro hac vice) Jason E. Roselius (Bar Number 16721) Gregory M. Castaldo (admitted pro hac vice) Guy R. Wood (Bar Number 15875) Lauren Wagner Pederson (admitted pro hac vice) P. O. Box 138800 Sharan Nirmul (admitted pro hac vice) Oklahoma City, Oklahoma 73113-8800 Naumon A. Amjed (admitted pro hac vice) Telephone: (405) 705-3600 Michelle M. Newcomer (admitted pro hac vice) Facsimile: (405) 705-2573 280 King of Prussia Road Radnor, PA 19087 Telephone: (610) 667-7706 Liaison Counsel for Lead Plaintiff Facsimile: (610)667-7056 and the Class Counsel for Lead Plaintiff and the Class TABLE OF CONTENTS I. NATURE OF THE ACTION - 2 - II. JURISDICTION AND VENUE - 10 - III. PARTIES - 11 - A. Lead Plaintiff - 11 - B. Company-Related Defendants - 11 - C. Individual Defendants - 12 - D. Underwriter Defendants - 15 - E. Investment Company Defendants - 19 - F. Relevant Non-Parties - 21 - IV. OVERVIEW OF DEFENDANTS’ SECURITIES LAWS VIOLATIONS - 22 - V. VIOLATIONS OF THE SECURITIES ACT - 23 - A. Background to SGLP’s Public Offerings - 23 - 1. SemGroup’s Undisclosed Speculative Trading - 25 - 2. Westback Trading - 33 - 3. SemGroup’s Margin Balance Grows - 35 - 4. SemGroup’s Collapse Into Bankruptcy - 38 - B. SemGroup’s July 2007 IPO - 41 - C. -

Excellence in Leadership Award Winners

Excellence in Leadership Award Winners Statewide Community The Statewide Community Award recognizes an organization or company that, through specific projects or efforts, has reached across our valued differences to develop among Oklahomans a keen sense of common purpose and a more profound sense of loyalty to our state. This award has been created to promote a heightened sense of appreciation for the possibilities available when Oklahomans work together as a single statewide community. 1999 American Fidelity Assurance Company, Oklahoma City 2000 The Samuel Roberts Noble Foundation, Ardmore 2001 The CAMA Coalition, (The Oklahoma Child Abuse Multi-Disciplinary Account Coalition), Tulsa 2002 SBC, Oklahoma City 2003 The Oklahoma Educational Television Authority, Oklahoma City 2004 Oklahoma Natural Gas, a division of ONEOK, Inc., Oklahoma City 2005 Chesapeake Energy Corporation, Oklahoma City 2006 Bank of Oklahoma N.A., Tulsa 2007 Oklahoma State Academy for State Goals, Oklahoma City 2008 Cox Oklahoma, Oklahoma City 2009 Griffin Communications, Oklahoma City 2010 OGE Energy Corp., Oklahoma City 2011 Blue Cross and Blue Shield of Oklahoma, Tulsa 2012 BancFirst, Oklahoma City 2013 The Oklahoma City Thunder, Oklahoma City 2014 The Chickasaw Nation, Ada 2015 Oklahoma Heritage Association & Gaylord-Pickens Museum, Oklahoma City 2016 George Kaiser Family Foundation, Tulsa 2017 Oklahoma Energy Resources Board, Oklahoma City Business Leadership The Business Leadership Award was created to recognize a business entity for its impact in promoting leadership