Third Quarter 2020 Conference Call Remarks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hess Corporation Is a Leading Global Independent Energy Company Engaged in the Exploration and Production of Crude Oil and Natural Gas

2017 ANNUAL REPORT Table of Contents 1 Financial and Operating Highlights 2 Letter to Shareholders 5 Global Operations 9 Sustainability 12 Board of Directors and Corporate Officers Our Company Hess Corporation is a leading global independent energy company engaged in the exploration and production of crude oil and natural gas. We are committed to meeting the highest standards of corporate citizenship by protecting the health and safety of our employees, safeguarding the environment and making a positive impact on the communities in which we do business. Cover: Drilling Operations, North Dakota Financial and Operating Highlights HESS CORPORATION Amounts in millions, except per share data Financial — for the year 2017 2016 Sales and other operating revenues $ 5,466 $ 4,762 Net income (loss) attributable to Hess Corporation $ (4,074) $ (6,132) Net income (loss) per share diluted (a) $ (13.12) $ (19.92) Common stock dividends per share $ 1.00 $ 1.00 Net cash provided by operating activities $ 945 $ 795 E&P capital and exploratory expenditures $ 2,047 $ 1,871 Midstream capital expenditures $ 121 $ 283 Weighted average diluted shares outstanding 314.1 309.9 Financial — at year end 2017 2016 Total assets $ 23,112 $ 28,621 Cash and cash equivalents $ 4,847 $ 2,732 Total debt $ 6,977 $ 6,806 Total equity $ 12,354 $ 15,591 Debt to capitalization ratio (b) 36.1% 30.4% Common stock price $ 47.47 $ 62.29 Operating — for the year 2017 2016 Net production Crude oil and natural gas liquids (thousands of barrels per day) United States 153 165 International 66 70 Total 219 235 Natural gas (thousands of MCF per day) United States 211 258 International 309 265 Total 520 523 Barrels of oil equivalent (thousands of barrels per day) 306 322 (a) Calculated as net income (loss) attributable to Hess Corporation less preferred stock dividends as applicable, divided by weighted average number of diluted shares. -

CALIFORNIA RESOURCES CORPORATION 2019 PROXY REPORT and NOTICE of ANNUAL MEETING Letter to Shareholders from the Chairman of the Board

CALIFORNIA RESOURCES CORPORATION 2019 PROXY REPORT AND NOTICE OF ANNUAL MEETING Letter to Shareholders from the Chairman of the Board Dear Shareholders, Strong execution, financial discipline and sustained community engagement are compelling hallmarks of California Resources Corporation (“CRC”), reflecting the Company’s core values of Character, Responsibility and Commitment and the high expectations set by the Board of Directors (the “Board”). In 2018, CRC achieved strong results through the exceptional leadership of our management team and the dedication of our diverse workforce who operate critical infrastructure and supply essential resources to Californians with an innovative and entrepreneurial mindset. With the Board’s active direction, CRC thoughtfully navigated a volatile pricing environment with a dynamic and flexible operating plan that prioritized projects to deliver value both in the immediate and longer term, while continuing to meaningfully strengthen our financial position. We believe this value-driven approach to managing our business truly sets CRC apart. It enables us to capture the full value of our robust portfolio of assets throughout the commodity cycle and ensures effective capital allocation that delivers positive results for our shareholders. Coupled with an unwavering focus on operational excellence that unifies the organization, it is a powerful strategic approach that sustains CRC’s high levels of safety, environmental stewardship, reliability and quality. In 2018, an engaged Board aligned with shareholder priorities brought to bear a wealth of experience and varied perspectives from within the energy industry, as well as from financial services, accounting, real estate, human resources and organizational disciplines. To ensure that CRC continues to attract and maintain the most effective mix of Board talent, we regularly engage in a review process to evaluate desired skill sets that strengthen governance, promote diversity of thought, and align with the evolving demands of our business. -

Hess Announces Sale of Its Enhanced Oil Recovery Assets in the Permian Basin

Hess Announces Sale of Its Enhanced Oil Recovery Assets in the Permian Basin June 19, 2017 NEW YORK--(BUSINESS WIRE)--Jun. 19, 2017-- Hess Corporation (NYSE:HES) today announced it has entered into an agreement to sell its interests in enhanced oil recovery (EOR) assets in the Permian Basin to Occidental Petroleum Corporation (NYSE:OXY) for a total consideration of $600 million, effective June 1, 2017. Proceeds from the sale will be used to fund the company’s strong growth opportunities. The transaction consists of the following Hess-operated assets: the Seminole-San Andres Unit (Hess 34.2% interest) and the Seminole Gas Processing Plant (Hess 46.6% interest) in Texas; the West Bravo Dome C02 field in New Mexico (Hess 100% interest); and a 9.9% non-operated interest in the Bravo Dome unit in New Mexico. These assets produced an average of 8,200 barrels of oil equivalent per day in 2016 net to Hess. The agreement is subject to regulatory approvals and other customary closing conditions and is expected to close August 1, 2017. Hess Corporation is a leading global independent energy company engaged in the exploration and production of crude oil and natural gas. More information on Hess Corporation is available at http://www.hess.com. Cautionary Statements This news release contains projections and other forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These projections and statements reflect the company’s current views with respect to future events and financial performance. -

June 2021 20

Annual Report 2020 June 2021 20 202 Olie Gas Danmark — Annual Report 2020 DBU Employees Offshore Tabel of contents 3 Board of Directors 4 Foreword 7 Key Achievements 2020 Climate and Sustainability Health, Safety and Environment Skills and Capabilities 14 Communication and External Engagement Communication Legal & Regulatory Affairs Partnering and recognition Publications 17 International engagement IOGP Bilateral collaboration around the North Sea 18 Covid-19 related activities 20 Current Oil Gas Denmark Members 21 Committee and Workgroup members 24 Financial Performance 2020 25 Employees Annual Report 2020 — Olie Gas Danmark 3 Board of Directors Martin Rune Pedersen Verner Andersen Christian Krüger Vice President and Country Vice President, Semco VP, Global Account Chair for TotalEnergies Den- Maritime, Vice Chairman of Oil Management, Welltec A/S mark, Chairman of Oil Gas Gas Denmark Denmark Martin is responsible for TotalEnergies’ ac- Verner is VP of Semco Maritime´s Opera- Christian is VP, Global Account Manage- tivities in Denmark, and as Vice President tions Support in the Oil & Gas Division. ment of Welltec. His background is an MSc Offshore Development he is responsible His background is an electrical engineer. in Geology from the University of Copen- for global development support to conven- He joined Semco Maritime after having hagen. He has more than 30 years of expe- tional offshore operation. He holds an MSc held several managerial positions in vari- rience from the oil & gas industry and has in Engineering from Aalborg University as ous offshore companies in Scandinavia. worked both in the field and in managerial well as a Graduate degree in Management He is also member of the Board in Esbjerg positions around the world. -

Independents Find Gulf Opportunities

JUNE 2015 The “Better Business” Publication Serving the Exploration / Drilling / Production Industry Independents Find Gulf Opportunities By Al Pickett crude oil production, and federal natural in the Gulf.” Special Correspondent gas production in the Gulf accounts for 7 He says the key is good exploration, percent of total U.S. dry gas production. and he credits Houston Energy for de- Deeper drilling and new reservoir dis- • There are more than 3,000 platforms veloping many of the prospects that Red coveries are but two of the reasons why operating in waters up to 650 feet deep, Willow participates in. In fact, Zahradnik the Gulf of Mexico remains an exciting and an increasing number of rigs are says, Red Willow Offshore and Houston area for development and exploration. drilling in ultradeep waters up to 9,000 Energy partnered to submit the largest While the nation’s unconventional shale feet deep. Additionally, there are more single bid of $52 million for Walker plays seemingly have garnered much of than 25,000 miles of oil and gas pipeline Ridge Block 107 in more than 5,000 feet the attention these days, the Gulf of on the Gulf of Mexico seafloor. of water in Central Gulf Lease Sale 235 Mexico still is enormously important to “We have been in a lot of unconven- in March. the nation’s energy production. tional plays, such as the Bakken and the “It looks like a good prospect,” he Consider a couple GOM facts from Anadarko Basin, as well as coalbed says matter-of-factly. “We believe it is the U.S. -

Harvest Energy Leaders Plus Income

Harvest Energy Leaders Plus QUARTERLY PORTFOLIO DISCLOSURE Income ETF as at June 30, 2019 Total Net Asset Value Portfolio Breakdown The total net asset value of the Harvest Energy Leaders % of Net Plus Income ETF was $20,831,758. Top Holdings Asset Value Kinder Morgan, Inc. 5.5 TC Energy Corporation 5.5 Summary of Investment Portfolio Occidental Petroleum Corporation 5.4 % of Net Chevron Corporation 5.4 Sector Allocation Asset Value Total S.A. ADR 5.1 Integrated Oil & Gas 35.5 Phillips 66 5.1 Oil & Gas Exploration & Production 32.0 Royal Dutch Shell PLC ADR 5.1 Oil & Gas Refining & Marketing 14.7 Valero Energy Corporation 5.0 Oil & Gas Storage & Transportation 11.1 Hess Corporation 5.0 Oil & Gas Equipment & Services 3.8 Exxon Mobil Corporation 4.9 Suncor Energy Inc. 4.9 Total Portfolio Assets 97.1 BP PLC ADR 4.9 Foreign currency forwards 1.9 Marathon Petroleum Corporation 4.8 Cash and other assets and liabilities 1.0 ConocoPhillips 4.8 Net Asset Value 100.0 Anadarko Petroleum Corporation 4.8 CNOOC Limited ADR 4.7 EOG Resources, Inc. 4.6 Devon Energy Corporation 4.4 % of Net Marathon Oil Corporation 4.0 Portfolio Allocation Asset Value Halliburton Company 3.9 Common Shares 78.0 Foreign currency forwards 1.9 ADRs 19.8 Cash and other assets and liabilities 1.0 Equity options (0.7) Equity options (0.7) Total Portfolio Assets 97.1 Foreign currency forwards 1.9 Cash and other assets and liabilities 1.0 Net Asset Value 100.0 The summary of investment portfolio may change due to ongoing portfolio transactions of the investment fund. -

Hess Corporation 2011 Annual Report

2011 ANNUAL REPORT OUr COMPANY Hess Corporation is a leading global independent energy company engaged in the exploration for and production of crude oil and natural gas, as well as in refining and in marketing refined petroleum products, natural gas and electricity. Our strategy is to build a company that will sustain profitable growth and create significant shareholder value. We are committed to meeting the highest standards of corporate citizenship by protecting the health and safety of our employees, safeguarding the environment and making a positive impact on the communities in which we do business. Table OF CONTENTS 1 Financial Highlights 2 L etter to Stockholders 4 O UR Global Operations 6 E xploration and Production 12 Marketing and Refining 16 C orporate and Social Responsibility 20 Board of Directors and Corporate Officers Cover: Drilling Operations, North Dakota FINANCIAL and OPERATING HIGHLIGHTS HESS CORPORATION Amounts in millions, except per share data FINANCIAL — FOR THE YEAR 2011 2010 Sales and other operating revenues $ 38,466 $ 33,862 Net income attributable to Hess Corporation $ 1,703 $ 2,125 Net income per share diluted $ 5.01 $ 6.47 Common stock dividends per share $ .40 $ .40 Net cash provided by operating activities $ 4,984 $ 4,530 Capital and exploratory expenditures $ 7,462 $ 5,855 Weighted average diluted shares outstanding 339.9 328.3 FINANCIAL — AT YEAR END 2011 2010 Total assets $ 39,136 $ 35,396 Total debt $ 6,057 $ 5,583 Total equity $ 18,592 $ 16,809 Debt to capitalization ratio(a) 24.6 % 24.9 % Common stock -

2019-October-Ir-Handout.Pdf

Hess Corporation INVESTOR RELATIONS PRESENTATION October 2019 Forward-Looking Statements & Other Information This presentation contains projections and other forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These projections and statements reflect the company’s current views with respect to future events and financial performance. No assurances can be given, however, that these events will occur or that these projections will be achieved, and actual results could differ materially from those projected as a result of certain risk factors. A discussion of these risk factors is included in the company’s periodic reports filed with the Securities and Exchange Commission. We use certain terms in this presentation relating to reserves other than proved, such as unproved resources. Investors are urged to consider closely the disclosure relating to proved reserves in Hess’ Form 10-K for the year ended December 31, 2018, available from Hess Corporation, 1185 Avenue of the Americas, New York, New York 10036 c/o Corporate Secretary and on our website at www.hess.com. You can also obtain this form from the SEC on the EDGAR system. This presentation includes certain non-GAAP financial measures, including Net Debt and Cash Return on Capital Employed (CROCE), EBITDAX, and Debt to EBITDAX. These Non-GAAP financial measures should be considered only as supplemental to, and not as superior to, financial measures prepared in accordance with GAAP. Please refer to the Appendix of this presentation for a reconciliation of the non-GAAP financial measures included in this presentation to the most directly comparable financial measures prepared in accordance with GAAP. -

Hess Corporation

EQUINIX CUSTOMER SUCCESS STORY HESS CORPORATION EQUINIX PROFESSIONAL SERVICES FOR CLOUD (EPS CLOUD) Leading global energy company successfully Customer Profile enables billion dollar divestment by migrating History entire enterprise IT suite to the cloud. Founded in 1933, Hess Corporation is a leading independent energy concern, engaged in the global exploration and “We had an obligation to deliver a functioning, operational production of crude oil and natural gas. infrastructure to the buyer. We also had an obligation to Hess to Headquarters make sure that infrastructure could be handed off in short order, New York City, NY both legally and physically. Using the cloud enabled us to meet The company also has regional all of these requirements and we are thrilled with the results.” headquarters in Houston, Texas and Kuala Lumpur, Malaysia. Jim McDonald, Lead Architect, Hess Corporation Overview/Executive Summary Hess Corporation, a leading global independent energy company engaged in the exploration and production of crude oil and natural gas, wanted to streamline its business to focus on energy exploration and production (E&P); and in March 2013 announced its intention to divest its downstream businesses, including retail, energy marketing and terminals. As part of this initiative, Hess IT needed to separate business systems and data for potential buyers and it looked to EPS Cloud to help it migrate those systems and data to the cloud. Business Challenge Companies acquire and divest businesses for strategic, financial and other reasons. If not managed effectively, the process can negatively affect the company, causing disruptions for the organization and the business. After Hess decided to streamline its business to focus on energy exploration and production in 2013, Hess IT determined that they would need to separate business systems and data for potential buyers, and initiated work on Amazon Web Services (AWS) in July 2013, with a contractual agreement to have the new environment operational and in production by January 2014. -

News Release

HESS CORPORATION News Release Hess, ExxonMobil, CNOOC Pledge More Than US$100 Million for Guyana Capacity Building Programs NEW YORK, Feb. 9, 2021 -- Hess, ExxonMobil and CNOOC Limited, co-venturers in offshore oil development in the Stabroek Block, have announced formation of the Greater Guyana Initiative, a 10-year commitment of more than US$100 million to significantly expand capacity building efforts and promote sustainable economic development in Guyana. The Greater Guyana Initiative’s capacity development efforts will include programs designed in consultation with Guyana’s Technical and Vocational Education and Training, the Centre for Local Business Development and University of Guyana. The initiative will also focus on supporting regional initiatives and capacity development of diverse sectors including health and agriculture. The Greater Guyana Initiative’s multi-faceted approach will grow the Guyanese workforce, increase competitiveness of local businesses across sectors and build upon the foundation for a thriving business environment and sustained economic growth. To meet the goals of the initiative, national and local leaders, community members and the private sector will be engaged to bolster the effectiveness of programs and ensure alignment with Guyana’s development priorities as they evolve over the coming years. The Greater Guyana Initiative will expand the current support for the Centre for Local Business Development by ExxonMobil, Hess and CNOOC Limited and facilitate its transition into a long- term center of excellence for broader industry. More than 2,400 Guyanese companies are registered with the centre, which was established by the co-venturers in 2017 with the mission of supporting local businesses to become globally competitive. -

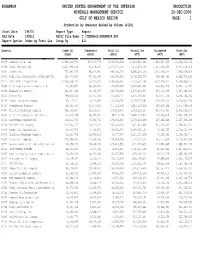

Ranking Operator by Gas 1947

PDRANKOP UNITED STATES DEPARTMENT OF THE INTERIOR PRODUCTION MINERALS MANAGEMENT SERVICE 22-DEC-2000 GULF OF MEXICO REGION PAGE: 1 Production by Operator Ranked by Volume (4120) Start Date : 194701 Report Type : Report End Date : 199512 ASCII File Name: C:\TIMSWork\PDRANKOP.DAT Report Option: Order by Total Gas Group By : All Operator Crude Oil Condensate Total Oil Natural Gas Casinghead Total Gas (BBLS) (BBLS) (BBLS) (MCF) (MCF) (MCF) 00078 Chevron U.S.A. Inc. 1,926,333,769 137,016,779 2,063,350,548 11,063,925,241 2,504,607,294 13,568,532,535 00689 Shell Offshore Inc. 1,417,893,524 85,274,236 1,503,167,760 7,372,318,798 2,025,230,206 9,397,549,004 00001 Conoco Inc. 797,691,267 90,614,940 888,306,207 6,665,540,300 1,270,468,340 7,936,008,640 00540 MOBIL OIL EXPLORATION & PRODUCING SOUT 323,970,684 67,931,345 391,902,029 6,452,624,776 498,954,383 6,951,579,159 00276 Exxon Mobil Corporation 1,093,558,792 56,026,660 1,149,585,452 5,223,562,198 1,323,290,927 6,546,853,125 00985 Union Exploration Partners, Ltd. 172,994,887 68,962,600 241,957,487 5,693,340,954 248,803,779 5,942,144,733 00081 Tenneco Oil Company 213,224,062 48,335,567 261,559,629 5,587,612,854 279,449,349 5,867,062,203 00040 Texaco Inc. 189,506,674 33,936,036 223,442,710 4,576,194,031 442,571,025 5,018,765,056 00114 Amoco Production Company 97,147,101 34,421,651 131,568,752 3,175,779,982 235,024,436 3,410,804,418 00167 PennzEnergy Company 191,565,059 26,157,422 217,722,481 2,812,024,858 262,674,308 3,074,699,166 00967 Atlantic Richfield Company 242,193,417 18,221,055 260,414,472 -

Leasing Activities Information

Leasing Activities Information U.S. Department of the Interior Minerals Management Service MMS Gulf of Mexico OCS Region LEASE SALE 205 CGOM STATISTICS As of February 15, 2008 107 Tracts in Phase 1 - Bids Deemed Acceptable 723 Total Tracts + 596 Tracts in Phase 2 - Bids Deemed Acceptable 703 Tracts - Bids Deemed Acceptable 703 Total Tracts - Bids Deemed Acceptable - 18 Tracts - Bids Rejected - 2 Tracts - Bids Forfeited 0 Tracts Remaining Bids on the following tracts were deemed acceptable on , February 14, 2008, in Phase 2 of the GOM Central Sale 205. The tracts are listed in GOM Company Number order. PHASE 2 ACCEPTANCES BY SUBMITTER 00059 Hess Corporation G31684 Garden Banks 987 G31852 Keathley Canyon 20 00078 Chevron U.S.A. Inc. G31644 Garden Banks 674 G31662 Garden Banks 807 G31668 Garden Banks 862 G31669 Garden Banks 863 G31676 Garden Banks 907 G31681 Garden Banks 953 G31682 Garden Banks 954 G31686 Garden Banks 996 G31688 Garden Banks 998 G31854 Keathley Canyon 22 G31857 Keathley Canyon 64 00689 Shell Offshore Inc. G31677 Garden Banks 910 00724 Marathon Oil Company G31733 Green Canyon 492 01207 Petrobras America Inc. G31679 Garden Banks 951 G31680 Garden Banks 952 G31776 Green Canyon 1001 G31777 Green Canyon 1002 02079 Nexen Petroleum Offshore U.S.A. Inc. G31865 Keathley Canyon 110 G31884 Keathley Canyon 302 02169 Hydro Gulf of Mexico, L.L.C. G31891 Keathley Canyon 368 02421 Devon Energy Production Company, L.P G31886 Keathley Canyon 325 02481 BP Exploration & Production Inc. G31631 Garden Banks 587 G31632 Garden Banks 588 G31687 Garden Banks 997 02748 Statoil Gulf of Mexico LLC G31635 Garden Banks 630 G31636 Garden Banks 631 02873 Cobalt International Energy, L.P.