Analysis of the Phoenix, Arizona Housing Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cy Martin Collection

University of Oklahoma Libraries Western History Collections Cy Martin Collection Martin, Cy (1919–1980). Papers, 1966–1975. 2.33 feet. Author. Manuscripts (1968) of “Your Horoscope,” children’s stories, and books (1973–1975), all written by Martin; magazines (1966–1975), some containing stories by Martin; and biographical information on Cy Martin, who wrote under the pen name of William Stillman Keezer. _________________ Box 1 Real West: May 1966, January 1967, January 1968, April 1968, May 1968, June 1968, May 1969, June 1969, November 1969, May 1972, September 1972, December 1972, February 1973, March 1973, April 1973, June 1973. Real West (annual): 1970, 1972. Frontier West: February 1970, April 1970, June1970. True Frontier: December 1971. Outlaws of the Old West: October 1972. Mental Health and Human Behavior (3rd ed.) by William S. Keezer. The History of Astrology by Zolar. Box 2 Folder: 1. Workbook and experiments in physiological psychology. 2. Workbook for physiological psychology. 3. Cagliostro history. 4. Biographical notes on W.S. Keezer (pen name Cy Martin). 5. Miscellaneous stories (one by Venerable Ancestor Zerkee, others by Grandpa Doc). Real West: December 1969, February 1970, March 1970, May 1970, September 1970, October 1970, November 1970, December 1970, January 1971, May 1971, August 1971, December 1971, January 1972, February 1972. True Frontier: May 1969, September 1970, July 1971. Frontier Times: January 1969. Great West: December 1972. Real Frontier: April 1971. Box 3 Ford Times: February 1968. Popular Medicine: February 1968, December 1968, January 1971. Western Digest: November 1969 (2 copies). Golden West: March 1965, January 1965, May 1965 July 1965, September 1965, January 1966, March 1966, May 1966, September 1970, September 1970 (partial), July 1972, August 1972, November 1972, December 1972, December 1973. -

SURVEY of CURRENT BUSINESS September 1966

SEPTEMBER 1966 / VOLUME 46 NUMBER OF CONTENTS U.S. Department of Commerce John T« Connor / Secretary THE BUSINESS SITUATION Summary 1 Office of Business Economies George Jaszi / Dime tor Capital Spending Programs in Second Half of 1966 3 Morris R. Goldman Louis J. Paradiso Associate Directors Manufacturers' Inventory and Sales Expectations 8 in Second Half 1966 Murray F. Foss / Editor Leo V* Barry, Jr. / Statistics Editor National Income and Product Tables 11 Billy Jo Hurley / Graphics ARTICLES STAFF CONTRIBUTORS TO THIS ISSUE The Balance of International Payments: 14 Business Review* Second Quarter 1966 David R. Hull, Jr. Foreign Investments, 1965-66 30 Francis L, Hirt Donald A. King Genevieve B. Wimsatt Marie P. Hertzberg Articles: Walther Lederer CURRENT BUSINESS STATISTICS Evelyn M, Parrish Samuel Pizer General S1-S24 Frederick Cutler Industry S24-S40 Subscription prices* including weekly statistical sup~ Subject Index (Inside Back Cover) plements, are $6 a year for domestic and $9*75 for foreign mailing. Single issue 45 cents* Make checks payable to the Superintendent of Docu- ments and send to U.S. Government Printing Office* Washington, D.C. 204029 or to any U.S. Department of Commerce Field Office. U.S. DEPARTMENT OF COMMERCE .FIELD OFFICES Allbnaqsiercpie, N. Mex.' 97101 Cheyenne, Wyo. 82001 Detroit, Mich. 48226 Memphis, Tfc*m. 38103 Portland, Greg. 97204 - ILS. Courthouse Ph. 247-0311. • ' 6022 U.S. Federal Bldg, 445 Federal Bldg. Ph. 226-6088. ; Ph. 634-5920. 345 Federal Oftice Bldg. 217 Old U.S. Courthouse Bldg. Anchorage, Alaska 99501 Ph. 534-3214. Ph. 226-3361. Loussac-Sogn Bldg, 272-6331. Greensboro, N.C. -

1968 Motor Vehicle Person Accident Calendar Year Public Use File Layout

MV-1 NHIS CALENDAR YEAR 1968 PUBLIC USE FILE MOTOR VEHICLE PERSON ACCIDENT (RECORD TYPE 7) Number of records – 929 __________________________________________________________________________________________ File Var. Name Location Quest. No. Title and Code __________________________________________________________________________________________ 1 QUARTER QUARTER HH-8 5. July-September (1967 if loc 108=7; 1968 if loc 108=8) 6. October-December 1967 7. January-March 1968 8. April-June 1968 9. July-September 1968 1. July-September 1967 2. October-December 1967 3. January-March 1968 4. April-June 1968 __________________________________________________________________________________________ 2 REGION REGION Recode 1. Northeast (includes sections 1 and 2) 2. Midwest (includes sections 3,4 and 5) 3. South (includes sections 6,7,8 and 9) 4. West (includes sections 10 and 11) __________________________________________________________________________________________ 3-9 BLANK BLANK __________________________________________________________________________________________ 10-12 PSURANDR PSU – RANDOM RECODE Recode __________________________________________________________________________________________ 13-14 WEEK WEEK OF QUARTER HH-6a Serially numbered from 01-13 within quarter * __________________________________________________________________________________________ 15-16 SEGMENT SEGMENT NUMBER HH-6a __________________________________________________________________________________________ 17-18 HHID HOUSEHOLD NUMBER HH-7 Numbers assigned within -

The Kentucky High School Athlete, September 1968 Kentucky High School Athletic Association

Eastern Kentucky University Encompass The Athlete Kentucky High School Athletic Association 9-1-1968 The Kentucky High School Athlete, September 1968 Kentucky High School Athletic Association Follow this and additional works at: http://encompass.eku.edu/athlete Recommended Citation Kentucky High School Athletic Association, "The Kentucky High School Athlete, September 1968" (1968). The Athlete. Book 142. http://encompass.eku.edu/athlete/142 This Article is brought to you for free and open access by the Kentucky High School Athletic Association at Encompass. It has been accepted for inclusion in The Athlete by an authorized administrator of Encompass. For more information, please contact [email protected]. K.H.S.A.A. SCHOOL FOR FOOTBALL OFFICIALS » • t f Above are area representatives who attended the School for Football Officials, held in Lexing- ton on August 2-3. They are: (Left to Right) Front Row—Tom Murray, Fort Mitchell; George Mercker, Louisville; School Director Edgar McNabb, Fort MitcheH; Bill Mordica, Ashland; Howard Moss, Paclucah; Bernard Johnson, Lexington. Second Row—Clyde Parsley, Provi- dence; E. B. May, Jr., Prestonsburg; Ray Canady, Barbourville; Kean Jenkins, EMzabeth- j-own; Paul Walker, Glasgow; Joe Russell, Russellville. Official Organ of the KENTUCKY HIGH SCHOOL ATHLETIC ASSOCIATION September, 1968 ———— Football Districts and Regions FILMS The football districts and regions for 1968 The films listed below are in the Film Library of the are as follows: University of Kentucky College of Education. The code letters, "e, j, s, c, a," refer to elementary, junior high, Class AAA senior high, college and adult audiences who may enjoy the particular film listed. -

Alumni Association Newsletter: September 1968 La Salle University

La Salle University La Salle University Digital Commons La Salle Alumni Association Newsletter University Publications 9-1968 Alumni Association Newsletter: September 1968 La Salle University Follow this and additional works at: http://digitalcommons.lasalle.edu/alumni_assoc_newsletter Recommended Citation La Salle University, "Alumni Association Newsletter: September 1968" (1968). La Salle Alumni Association Newsletter. 9. http://digitalcommons.lasalle.edu/alumni_assoc_newsletter/9 This Book is brought to you for free and open access by the University Publications at La Salle University Digital Commons. It has been accepted for inclusion in La Salle Alumni Association Newsletter by an authorized administrator of La Salle University Digital Commons. For more information, please contact [email protected]. LA SALLE COLLEGE ALUMNI ASSOCIATION Vol. Ill No. 1 September 1968 KANE CALLS LEADERSHIP CONFERENCE ON ALUMNI INVOLVEMENT The Alumni Association will sponsor its second Leadership Conference on campus on Saturday morning, September 14, 1968. In announcing the theme, “Involvement ‘68,” Alumni President Daniel H. Kane expressed the hope that the conference will be suc- cessful in producing greater involvement on the part of our alumni. Brother Daniel Bernian, F.S.C., President of the College will welcome the partici pating alumni at 9:00 a.m. in the College Union Theatre. Following this, John L. McCloskey, Vice President of Public Relations, will offer a projection on La Salle’s future and James J. McDonald, Director of Alumni, will discuss the direction of alumni activity in recent years. Then President Kane will offer his plan for an alumni advisory council. Following a coffee break at 10 o’clock, discussion groups, formed largely along professional lines, will con sider the plan offered by Mr. -

By P. E. Scbmid Goddurd Space Flight Center Greedelt, Md

NASA TECHNICAL NOTE NASA TN 0-6822 cv N SURFACE-REFRACTIVITY MEASUREMENTS AT NASA SPACECRAFT TRACKING SITES by P. E. Scbmid Goddurd Space Flight Center Greedelt, Md. 20771 NATIONAL AERONAUTICS AND SPACE ADMINISTRATION 0 WASHINGTON, D. C. SEPTEMBER 1972 TReport No. 2. Government Accession No. 3. Recipient's Catalog No. NASA IY D-u&?~ 4. Title and Subtitle 5. Report Date Surface-Refractivity Measurements at SepLernber 19 (2 NASA Spacecraft Tracking Sites 6. Performing Organization Code 7. Author(s) 8. Performing Organization Report No. P. E. Schmid G-1052 9. Performing Organization Name and Address IO. Work Unit No. Goddard Space Flight Center - 11. Contract or Grant No. Greenbelt, Maryland 2077 1 13. Type of Report and Period Covered 12. Sponsoring Agency Name and Address Technical Note National Aeronautics and Space Administration Washington, D.C. 20546 14. Sponsoring Agency Code IS. Supplementary Notes 16. Abstract High-accuracy spacecraft tracking requires tropospheric modeling which is generally scaled by either estimated or measured values of surface refractivity. This report summarizes the results of a worldwide surface-refractivity test conducted in 1968 in support of the Apollo program. The results are directly applicable to all NASA radio-tracking systems. I 17. Key Words (Selected by Author(r)) 18. Distribution Statement Troposphere Surface Refractivity Unclassified-Unlimited Meteorological Measurements Unclassified Unclassified 48 *For sale by the National Technical Information Service, Springfield, Virginia 22 151. CONTENTS Page I Abstract .................................. i I ~ INTRODUCTION .............................. 1 I CALCULATION OF SURFACE REFRACTIVITY .................. 2 I Scope of Test .............................. 2 I Mathematical Formulation of Refractivity ................... 4 SURFACE-REFRACTIVITY MEASUREMENT RESULTS .............. 5 Monthly Variations ........................... -

UNITED NATIONS Distr

UNITED NATIONS Distr. GENERAL GENERAL A/7753 ASSEMBLY 7 November 1969 ORIGINAL: ENGLISH THenty-fourth session Agenda item 63 INFORMJ;TION FROM NON-SELF-GOVERNING TERRITORIES TRANSMITTED UNDER !IRTICLE 73 e OF THE CHAR·TER Report of the Secretary-General l. Under the terms oi' Article 73 e of the Charter of the United Nacions, Member States vhich have or assume responsibilities for the ac1:ninistration of Territories whose peoples have no,; yet attained a full meocsure of self -government cmdertake to transmit regularly to the Secretary-Geners.l infol~mation relatine; to economic, social and educationsl conditions ifl the TerJ.."itories for 1.;hich they are reS)Otlsible, other than those Territories to which che International Trusteeship SJcscem applies. In addition, the General Assembly in several r·esolutions, the most recent of which was resolution 2L,22 (XXIII) of' 18 Dece c;;:.er 1968, urged the e.dministerin:o Pm<ers concerned nto transn1it, or continue to transmit, to the Secretary-Genel.... e.l the information p:!:"escribed in Article 73 e of the Charter, as well as the f'J.ll_est possible inforw.ation on political and constitutional developments in -~he 11 Territories concerned .. 2. The table annexed to the present report sh()';IS the dates on \·lhich information called for in Article 73 e was transmitted to the Secretary-General in respect of the years 1967 and 1958 up to 3 November 1969. 3. The information transmitted under Article 73 e of the Charter follows in general the standard form approved b:r the General Assembly and incLudes information on geography, history, population, economic, social and educational conditions. -

The Kentucky High School Athlete, September 1966 Kentucky High School Athletic Association

Eastern Kentucky University Encompass The Athlete Kentucky High School Athletic Association 9-1-1966 The Kentucky High School Athlete, September 1966 Kentucky High School Athletic Association Follow this and additional works at: http://encompass.eku.edu/athlete Recommended Citation Kentucky High School Athletic Association, "The Kentucky High School Athlete, September 1966" (1966). The Athlete. Book 122. http://encompass.eku.edu/athlete/122 This Article is brought to you for free and open access by the Kentucky High School Athletic Association at Encompass. It has been accepted for inclusion in The Athlete by an authorized administrator of Encompass. For more information, please contact [email protected]. HiqhSchoofAfhIete K.H.S.A.A. SCHOOL FOR FOOTBALL OFFICIALS Above are ares representatives who attended the School for Football Officials, held in Lexington on August 5-6. They are: (Left to Right) Front Row—Joe Treas, Fulton; Ray Canady, Barbourville; George Mercker, Louisville; Bill Mayhew, Elizabethtown; Bill Moi^ dica, Ashland; Gordon Reed, Fort Thomas. Second Row—Clyde Parsley, Providence; E. B. May, Jr., Prestonsburg; Robert Fallon, Hazard; Vic Brizendlne, Louisville; School Director Edgar McNabb, South Fort Mitchell; Bernard Johnson, Lexington; Paul Walker, Glasgow. Official Organ of tlie KENTUCKY HIGH SCHOOL ATHLETIC ASSOCIATION SEPTEMBER, 1966 — Football Districts and Regions "Bl is not eligible to continue to participate until the The football districts and regions for equipment has been sanctioned, or if illegal, is re- moved." are as follows: 1966, Page 28, Play 122B: Delete the entire piay. Class AAA Page 32, Play 131: The third line from the bottom REGION I of the page is misplaced. -

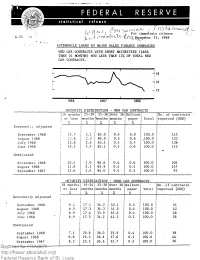

Federal Reserve

FEDERAL RESERVE statistical release L-L " y / * J] For r immediatimmediatee releasreiea:e /•- (lumber 13, 1968 AUTOMOBILE LOANS BY MAJOR SALES FINANCE COMPANIES NEW CAR CONTRACTS WITH SHORT MATURITIES (LESS THAN 24 MONTHS) NOW LESS THAN 12% OF TOTAL NEW CAR CONTRACTS. 1968 MATURITY DISTRIBUTION - NEW CAR CONTRACTS |24 months 25-30 31-36 Over 36 Balloon No. of contracts I or less months months months Total reported (000) I 1 % % % P % Seasonally adjusted j September 1968 j 11.7 2.1 85.0 0.4 0.8 100.0 115 August 1968 , 12.6 2.3 84.0 0.5 0.6 ,100.0 122 July 1968 j 12.8 2.6 83.5 0.4. 0.7 100.0 136 June 1968 j 13.2 2.5 83.2 0.5 0.6 100.0 112 Unadjusted | September 1968 1 10.4 2.0 86.6 0.4 0.6 100.0 104 August 1968 I 11.0 2.1 85.9 0.5 0.5 100.0 137 September 1967 12.6 2.4 84.0 0.5 0.5 100.0 92 MATURITY DISTRIBUTION - USED CAR CONTRACTS j18 months 19-24 25-30 Over 30 Balloon No. of contracts months months months Total reported (000) ! % % % % V Seasonally adjusted September 1968 6.1 17.1 34.2 42.1 0.5 100.0 41 August 1968 6.5 17.3 34.3 41.5 0.4 100.0 42 July 1968 6.9 17.4 33.9 41.4 0.4 100.0 46 June 1968 6.9 17.5 34.2 41.2 0.2 100.0 38 Unadjusted September 1968 7.1 20.6 36.0 35.9 0.4 100.0 38 August 1968 6.8 19.3 36.6 37.0 0.3 100.0 44 September 1967 8.2 22.2 36.6 32.7 0.3 100.0 36 Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. -

Participate, Without Vote, in the Discussion of the Question

participate, without vote, in the discussion of the Resolution 251 (1968) question. of 2 May 1968 The Security Council, Noting the Secretary-General's reports of 26 April At the 1412th meeting, on 4 April 1968, as a result (S/8561)27 and 2 May 1968 (S/8567),27 of consultations which had taken place on this item, Recalling resolution 250 (1968) of 27 April 1968, the President read the following statement: Deeply deplores the holding by Israel of the miiltary "Having heard the statements of the parties in parade in Jerusalem on 2 May 1968 in disregard of the regard to the renewal of the hostilities, the members unanimous decision adopted by the Council on 27 April of the Security Council are deeply concerned at the 1968. deteriorating situation in the area. They therefore Adopted unanimously at the consider that the Council should remain seized of the 1420th meeting. situation and keep it under close review". At its 1416th meeting, on 27 April 1968, the Council Decision decided to invite the representatives of Jordan and Israel to participate, without vote, in the discussion of the item entitled "The situation in the Middle East: At its 1421st meeting, on 3 May 1968, the Council Letter dated 25 April 1968 from the Permanent Rep decided to invite Mr. Rouhi El-Khatib, in accordance resentative of Jordan to the President of the Security with rule 39 of the provisional rules of procedure, to Council (S/8560)".24 make a statement before the Council. Resolution 250 (1968) Resolution 252 (1968) of 27 April 1968 of 21 May 1968 The Security Council, The Security Council, Hewing heard the statements of the representatives Recalling General Assembly resolutions 2253 (ES-V) of Jordan and Israel, of 4 July 1967 and 2254 (ES-V) of 14 July 1967, Having considered the Secretary-General's note Having considered the letter of the Permanent Rep a5 (S/8561), particularly his note to the Permanent resentative of Jordan on the situation in Jerusalem Representative of Israel to the United Nations, (S/8560)28 and. -

Official Records • NEW YG RK

.j CORRIGENDUM Supplement No. 2 (A/6702) 7 December 1967 Official Records • NEW YG RK REPORT OF THE SECURITY COUNCIL 16 July 1966-15 July 1967 Page.s 93-94 Paragraph 842 should be replaced by the following text: 842. Listed below and briefly summarized are the letters from the repre sentative of Cambodia to the Presiden~ of the Security Council for the information of the Council: Let~er dated 5 August 1966 (8/7451) charginr firing by United States-South Viet-Namese aircraft on Cambodian villag ~s on 31 July and 3 August. in the latter case in the presence cf investigatir ~members of the International Control Commission; Letter dated 23 September 1966 (S/7511) cl> 'ging that incidents tcok place on 18 and 20 P '""'Ust and 4 and 7 Septerr. 'r involving firing across the frontier and aircraft machine-gunning Camt jan border villages; Letter dated 28 September (8/7515) and 4 Oc .ober 1966 (S/7528) charging machine-gunning and rocket firing by heliCI pters on 20 September at a Cambodian guard post; Letter dated 11 October 1966 (S/7543) charging that incidents took place between 17 August and 16 September 1966; Letter dated 24 October 1966 (S/7566) charging incidents of firing across the demarcation line into Cambodian territory between12 and 18 September 1966; Letter dated 11 November 1966 (S/7583) charging that incidents took place between 29 August and 10 October 1966; Letter dated 14 November 1966 (S/7588) charging that incidents took place between 12 August and 14 October; Letter dated 22 November 1966 (S/7597) chargingviolations of Cambodian -

Northwest Friend, September 1966

Digital Commons @ George Fox University Northwest Yearly Meeting of Friends Church Northwest Friend (Quakers) 9-1966 Northwest Friend, September 1966 George Fox University Archives Follow this and additional works at: https://digitalcommons.georgefox.edu/nwym_nwfriend Recommended Citation George Fox University Archives, "Northwest Friend, September 1966" (1966). Northwest Friend. 260. https://digitalcommons.georgefox.edu/nwym_nwfriend/260 This Book is brought to you for free and open access by the Northwest Yearly Meeting of Friends Church (Quakers) at Digital Commons @ George Fox University. It has been accepted for inclusion in Northwest Friend by an authorized administrator of Digital Commons @ George Fox University. For more information, please contact [email protected]. SEPTEMBER 1 9 6 6 'Quaker journal of the Paeifie florthwest" Vol. XLVI No. 6 IN THIS ISSUE: | We Were There I The Recruitment of Friends Ministers I May I Introduce Jack L. Willcuts (Cover picture ^ows Dorwln Smith, Presiding Clerk of Oregon as serving on the Board of Evangelism. He, Yearly Meeting, center, widi Jack L. WiUcuts, left, and Dean Gregory, retiring General SuperintendenL ) aloi^ with his family, have given unstintingly of their effort as missionaries in Bolivia. He has been active in the work of the Publication May I Introduce Board, has served as a representative from Oregon Yearly Meeting on the George Fox Jack L. Willcuts Press, Evangelical Friends Alliance as well as other inter-yearly meeting committees. jt CCORDING TO the Discipline of Oregon He has also been very successful in pastoral Yearly Meeting it is the responsibility work and a member of the Friendsview Manor of the Executive Council "to nominate to Board to name a few of the areas in which he 'Eyewitnesses of His Mnjesfy' the Yearly Meeting persons to serve as Gen has been engaged.