HALF YEAR REPORT 2020 Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Manager's Comment Performance Total Return

UPDATE 30 November 2017 Manager’s Comment Investment Objective: To achieve capital growth through a focused BTEM’s NAV was essentially unchanged over the month with portfolio of investments, particularly in companies whose share prices local currency gains - driven mostly by discount narrowing - stand at a discount to estimated underlying net asset value. being offset by adverse FX moves (a strengthening Pound). We now have over 20% of NAV in Japanese holdings and these were a key source of performance over the month. Tokyo Broadcasting System, Digital Garage, Toshiba Plant, and the Japan Special Situations Basket all performed strongly. Performance Total Return Outside of Japan, GP Investments, Cosan Limited (which was until now an undisclosed position), JPEL Private Equity, and This investment management report relates to performance figures to Third Point Offshore Investors contributed to returns; Exor, 30 November 2017. Investor AB, Adler, Symphony, and Swire Pacific were detractors. Month Financial Yr* Calendar Yr to date to date We wrote last month on Tokyo Broadcasting System (TBS) and our public campaign to encourage the company to reduce its stock portfolio. TBS’ BTEM NAV1 0.0% 3.5% 12.6% share price rose +20% over November on the back of publicity surrounding our actions and strong operating profit growth (+38% for H1-17) in the MSCI ACWI Ex US3 -1.1% 1.8% 14.1% underlying operating business. Despite the share price increase, non-core assets (listed equities, investment properties, and net cash) more than cover 1 the market cap with the high quality operating business being implicitly MSCI ACWI Ex US Value -1.4% 1.0% 10.0% assigned a negative value by the market. -

Japan Under Construction: Corruption, Politics, and Public Works

Preferred Citation: Woodall, Brian. Japan under Construction: Corruption, Politics, and Public Works. Berkeley, Calif: University of California Press, c1996 1996. http://ark.cdlib.org/ark:/13030/ft5489n9zf/ Japan Under Construction Corruption, Politics, and Public Works Brian Woodall UNIVERSITY OF CALIFORNIA PRESS Berkeley · Los Angeles · Oxford © 1996 The Regents of the University of California To Joyce, Leslie, and Melissa Preferred Citation: Woodall, Brian. Japan under Construction: Corruption, Politics, and Public Works. Berkeley, Calif: University of California Press, c1996 1996. http://ark.cdlib.org/ark:/13030/ft5489n9zf/ To Joyce, Leslie, and Melissa ― ix ― Acknowledgments In researching this book, I have drawn extensively on Japanese-language materials: newspaper reports, periodicals, industry association publications, and government documents. In addition, I conducted over one hundred open-ended interviews, primarily in 1987–1988 and in 1993–1994. Almost all of these interviews were conducted in Japanese, each lasting about an hour. I spoke with construction contractors, industry association officials, elected politicians and their aides, political party officials, government bureaucrats, newspaper reporters, and academics. Because of the highly sensitive, and sometimes sub rosa, nature of the subject matter, I cannot identify these individuals by name. For their willingness to answer sometimes naive questions and to assist in other ways, however, I owe a deep debt of gratitude. At the time I undertook this study, sensible people warned me about the quagmire that lay ahead. They alerted me to the difficulties of handling the shadowy actors engaged in the complex and secretive process of rigging bids on public works projects. Others warned me about dealings with the government bureaucrats and legislators who also animate the policymaking stage in this heretofore strictly "domestic" domain. -

Code Issue Size 1 1301 KYOKUYO CO.,LTD. Topixsmall TOPIX1000

TOPIX New Index Series (As end of October , 2012) (sort by Local Code) As of October 5, 2012 Code Issue TOPIX New Index Series Size 1 1301 KYOKUYO CO.,LTD. TOPIXSmall TOPIX1000 小型 2 1332 Nippon Suisan Kaisha,Ltd. TOPIX Mid400 TOPIX 500 TOPIX1000 中型 3 1334 Maruha Nichiro Holdings,Inc. TOPIX Mid400 TOPIX 500 TOPIX1000 中型 4 1352 HOHSUI CORPORATION TOPIXSmall 小型 5 1377 SAKATA SEED CORPORATION TOPIXSmall TOPIX1000 小型 6 1379 HOKUTO CORPORATION TOPIXSmall TOPIX1000 小型 7 1414 SHO-BOND Holdings Co.,Ltd. TOPIXSmall TOPIX1000 小型 8 1417 MIRAIT Holdings Corporation TOPIXSmall TOPIX1000 小型 9 1514 Sumiseki Holdings,Inc. TOPIXSmall 小型 10 1515 Nittetsu Mining Co.,Ltd. TOPIXSmall TOPIX1000 小型 11 1518 MITSUI MATSUSHIMA CO.,LTD. TOPIXSmall TOPIX1000 小型 12 1605 INPEX CORPORATION TOPIX Large70 TOPIX 100 TOPIX 500 TOPIX1000 大型 13 1606 Japan Drilling Co.,Ltd. TOPIXSmall 小型 14 1661 Kanto Natural Gas Development Co.,Ltd. TOPIXSmall TOPIX1000 小型 15 1662 Japan Petroleum Exploration Co.,Ltd. TOPIX Mid400 TOPIX 500 TOPIX1000 中型 16 1712 Daiseki Eco.Solution Co.,Ltd. TOPIXSmall 小型 17 1719 HAZAMA CORPORATION TOPIXSmall TOPIX1000 小型 18 1720 TOKYU CONSTRUCTION CO., LTD. TOPIXSmall 小型 19 1721 COMSYS Holdings Corporation TOPIX Mid400 TOPIX 500 TOPIX1000 中型 20 1722 MISAWA HOMES CO.,LTD. TOPIXSmall TOPIX1000 小型 21 1762 TAKAMATSU CONSTRUCTION GROUP CO.,LTD. TOPIXSmall 小型 22 1766 TOKEN CORPORATION TOPIXSmall TOPIX1000 小型 23 1780 YAMAURA CORPORATION TOPIXSmall 小型 24 1801 TAISEI CORPORATION TOPIX Mid400 TOPIX 500 TOPIX1000 中型 25 1802 OBAYASHI CORPORATION TOPIX Mid400 TOPIX 500 TOPIX1000 中型 26 1803 SHIMIZU CORPORATION TOPIX Mid400 TOPIX 500 TOPIX1000 中型 27 1805 TOBISHIMA CORPORATION TOPIXSmall TOPIX1000 小型 28 1808 HASEKO Corporation TOPIX Mid400 TOPIX 500 TOPIX1000 中型 29 1810 MATSUI CONSTRUCTION CO.,LTD. -

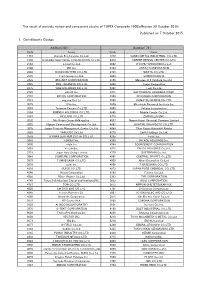

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Form5500 Annual Return/Report of Employee Benefit Plan

Annual Return/Report of Employee Benefit Plan OMB Nos. 1210-0110 Form 5500 1210-0089 This form is required to be filed for employee benefit plans under sections 104 and 4065 of the Employee Retirement Income Security Act of 1974 (ERISA) and Department of the Treasury Internal Revenue Service sections 6057(b) and 6058(a) of the Internal Revenue Code (the Code). 2017 Department of Labor Complete all entries in accordance with Employee Benefits Security Administration the instructions to the Form 5500. Pension Benefit Guaranty Corporation This Form is Open to Public Inspection Part I Annual Report Identification Information For calendar plan year 2017 or fiscal plan year beginning 01/01/2017 and ending 12/31/2017 X a multiemployer plan a multiple-employer plan (Filers checking this box must attach a list of A This return/report is for: X X participating employer information in accordance with the form instructions.) X a single-employer plan X a DFE (specify) _C_ B This return/report is: X the first return/report X the final return/report X an amended return/report X a short plan year return/report (less than 12 months) C If the plan is a collectively-bargained plan, check here. X D Check box if filing under: X Form 5558 X automatic extension X the DFVC program X special extension (enter description) ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDE Part II Basic Plan Information—enter all requested information 1a Name of plan 1b Three-digit plan 001 ABCDEFGHIPRODUCERS-WRITERS ABCDEFGHI GUILD ABCDEFGHI OF AMERICA PENSIONABCDEFGHI PLAN ABCDEFGHI ABCDEFGHI ABCDEFGHI number (PN) 001 ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI 1c Effective date of plan YYYY-MM-DD03/31/1960 2a Plan sponsor’s name (employer, if for a single-employer plan) 2b Employer Identification Mailing address (include room, apt., suite no. -

Notice on Acquisition of Domestic Real Estate

December 17, 2012 To whom it may concern: <Investment Corporation> Japan Real Estate Investment Corporation Noritada Terasawa, Executive Director (TSE code: 8952) <Asset Management Company> Japan Real Estate Asset Management Co., Ltd. Hiroshi Katayama, CEO & President Contact: Ryuta Yoshida, General Manager, Planning Department Phone: +81-3-3211-7921 Notice on Acquisition of Domestic Real Estate Announcement is hereby made that on December 17, 2012, Japan Real Estate Investment Corporation (the “Company”) decided to acquire the following domestic real estate property. 1. Outline of the acquisition 1) Asset to be acquired: Domestic Real Estate Land: Ownership (share of co-ownership) Building: Compartmentalized building units and co-ownership of compartmentalized building units (ownership percentage for building: 2.859811%) (Note 1) 2) Name of asset: Harmony Tower 3) Acquisition price: ¥ 520 million 4) Scheduled acquisition date: December 19, 2012 (scheduled) 5) Seller: 4 individuals (Note 2) 6) Method of Settlement: Lump sum payment at closing of acquisition 7) Acquisition funds: Own funds (scheduled) Note 1: The Company acquired a share of ownership of the property (29.253305% of the share of ownership of the building) on February 28, 2005. Following the above acquisition of an additional share, the Company’s share of ownership of the building will be 32.113115%. Note 2: Details of the sellers are not disclosed due to non-approval of disclosure by individuals of the sellers. 2. Reason for the acquisition The Company will acquire the assets based on the basic policies and investment attitude for acquisition under the Articles of Incorporation of the Company. In particular, the following points have been highly evaluated in the determination of the acquisition. -

Company Overview Valuation Data Source

Valuation Data Source company overview No. Company No. Company No. Company "Bank "Saint-Petersburg" Public 60 AbClon Inc. 117 Activision Blizzard, Inc. 1 Joint-Stock Company Abdullah Al-Othaim Markets 118 Actron Technology Corporation 61 2 1&1 Drillisch AG Company 119 Actuant Corporation 3 1-800-FLOWERS.COM, Inc. Abdulmohsen Al-Hokair Group for 120 Acuity Brands, Inc. 62 4 11 bit studios S.A. Tourism and Development Company 121 Acushnet Holdings Corp. 5 1st Constitution Bancorp 63 Abengoa, S.A. 122 Ad-Sol Nissin Corporation 6 1st Source Corporation 64 Abeona Therapeutics Inc. 123 Adairs Limited 7 21Vianet Group, Inc. 65 Abercrombie & Fitch Co. 124 ADAMA Ltd. 8 22nd Century Group, Inc. 66 Ability Enterprise Co., Ltd. 125 Adamas Pharmaceuticals, Inc. Ability Opto-Electronics Technology 126 Adamis Pharmaceuticals Corporation 9 2U, Inc. 67 Co.,Ltd. 127 Adani Enterprises Limited 10 3-D Matrix, Ltd. 68 Abiomed, Inc. 128 Adani Gas Limited 11 361 Degrees International Limited 69 ABIST Co.,Ltd. 129 Adani Green Energy Limited 12 3D Systems Corporation 70 ABL Bio Inc. Adani Ports and Special Economic 13 3i Group plc 130 71 Able C&C Co., Ltd. Zone Limited 14 3M Company 131 Adani Power Limited 72 ABM Industries Incorporated 15 3M India Limited 132 Adani Transmissions Limited 73 ABN AMRO Bank N.V. 16 3S KOREA Co., Ltd. 133 Adaptimmune Therapeutics plc 74 Aboitiz Equity Ventures, Inc. 17 3SBio Inc. 134 Adastria Co., Ltd. 75 Aboitiz Power Corporation 18 500.com Limited 135 ADATA Technology Co., Ltd. 76 Abraxas Petroleum Corporation 19 51 Credit Card Inc. -

JPX-Nikkei Mid Small Constituents (Updated on Dec. 22, 2016)

JPX-Nikkei Mid and Small Cap Index (As of March 13, 2017) Published on December 14, 2016 Updated on December 22, 2016 No. of constituents : 199 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) The FFW Ratio following cap-adjustment for each constituents will be announced as soon as they are decided. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1407 J West Holdings Corporation 3107 1 Daiwabo Holdings Co.,Ltd. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3179 1 Syuppin Co.,Ltd. 1722 1 MISAWA HOMES CO.,LTD. 3244 1 Samty Co.,Ltd. 1805 1 TOBISHIMA CORPORATION 3254 1 PRESSANCE CORPORATION 1813 1 Fudo Tetra Corporation 3258 1 UNIZO Holdings Company,Limited 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3276 1 Japan Property Management Center Co.,Ltd. 1822 1 DAIHO CORPORATION 3284 1 Hoosiers Holdings 1827 1 NAKANO CORPORATION 3341 1 NIHON CHOUZAI Co.,Ltd. 1852 1 ASANUMA CORPORATION 3387 1 create restaurants holdings inc. 1870 1 YAHAGI CONSTRUCTION CO.,LTD. 3649 1 FINDEX Inc. 1873 1 NIHON HOUSE HOLDINGS CO.,LTD. 3654 1 HITO-Communications,Inc. 1879 1 SHINNIHON CORPORATION 3657 1 Poletowin Pitcrew Holdings,Inc. 1882 1 TOA ROAD CORPORATION 3662 1 Ateam Inc. 1890 1 TOYO CONSTRUCTION CO.,LTD. 3676 1 Hearts United Group Co.,Ltd. 1896 1 OBAYASHI ROAD CORPORATION 3844 1 COMTURE CORPORATION 1898 1 SEIKITOKYU KOGYO CO.,LTD. 3857 J LAC Co.,Ltd. 1899 1 FUKUDA CORPORATION 4008 1 Sumitomo Seika Chemicals Company,Limited. -

Form5500 Annual Return/Report of Employee Benefit Plan

Annual Return/Report of Employee Benefit Plan OMB Nos. 1210-0110 Form 5500 1210-0089 This form is required to be filed for employee benefit plans under sections 104 and 4065 of the Employee Retirement Income Security Act of 1974 (ERISA) and Department of the Treasury Internal Revenue Service sections 6057(b) and 6058(a) of the Internal Revenue Code (the Code). 2016 Department of Labor Complete all entries in accordance with Employee Benefits Security Administration the instructions to the Form 5500. Pension Benefit Guaranty Corporation This Form is Open to Public Inspection Part I Annual Report Identification Information For calendar plan year 2016 or fiscal plan year beginning 01/01/2016 and ending 12/31/2016 X a multiemployer plan X a multiple-employer plan (Filers checking this box must attach a list of A This return/report is for: participating employer information in accordance with the form instructions.) X a single-employer plan X a DFE (specify) _C_ B This return/report is: X the first return/report X the final return/report X an amended return/report X a short plan year return/report (less than 12 months) C If the plan is a collectively-bargained plan, check here. X D Check box if filing under: X Form 5558 X automatic extension X the DFVC program X special extension (enter description) ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDE Part II Basic Plan Information—enter all requested information 1a Name of plan 1b Three-digit plan 001 ABCDEFGHIPRODUCERS-WRITERS ABCDEFGHI GUILD OF AMERICA ABCDEFGHI PENSION PLAN ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI number (PN) 001 ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI ABCDEFGHI 1c Effective date of plan YYYY03/31/1960-MM-DD 2a Plan sponsor’s name (employer, if for a single-employer plan) 2b Employer Identification Mailing address (include room, apt., suite no. -

Timber Takeaway

Timber Takeaway... Japanese Over-consumption—the Forgotten Campaign A Briefing Document by Global Witness. October 1999 CONTENTS RECOMMENDATIONS1 PREFACE 2 INTRODUCTION 2 THE JAPANESE TIMBER TRADE: AN OVERVIEW 3-6 Import Trends 3 The boom in Japanese timber imports Recent changes in the trade Trends in Imported Wood Products 4 Value-added wood products Other wood-related products Wooden furniture The Housing Industry: Japan’s Greatest Timber Consumer 5 Housing starts Short durability and high cost Waste 5 Alternative Building Materials 6 Formwork Other building materials Certified timber THE COMPANIES INVOLVED AND THEIR MARKETS 6-8 The Sogo Shosha 6 The Big Six The Construction Industry 6-7 Civil Engineering 7 The Housing Industry 7 The Building Materials Industry 7 The Fittings and Furniture Industry 7 The Paper Industry 7-8 ECONOMIC FACTORS AFFECTING THE JAPANESE TIMBER TRADE 8-9 A Declining Japanese Economy 8-9 Effects on the domestic timber market Effects on the international Timber market International Trade Liberalisation 9 Domestic Forestry 9 NGO OPERATIONS IN JAPAN 10-13 Japanese NGOs and their Campaigns 10-11 Current activities of Japanese groups and NGOs Japan Tropical Forest Action Network (JATAN): background Sarawak Campaign Committee: background The Status of NGOs in Japan 11-12 Cultural factors inhibiting the potential of NGOs Legal status, funding and manpower Emerging NGO legislation Freedom of information Working with western NGOs Green potential in Japan The Government, Industry and Forest Conservation 12-13 The industry response to environmental campaigns The government response to environmental campaigns Focus Areas for the Involvement of International NGOs 13 CONCLUSION 13 APPENDIX 14-21 REFERENCES 22 RECOMMENDATIONS NON GOVERNMENTAL ORGANISATIONS International NGOs should: Provide financial support for Japanese NGOs, by providing grants and through fundraising on their behalf. -

Of Calculation and Publication of New Index “JPX-Nikkei Mid and Small Cap Index”

(Reference Translation) December 14, 2016 Tokyo Stock Exchange, Inc. Nikkei, Inc. Start of Calculation and Publication of New Index “JPX-Nikkei Mid and Small Cap Index” As announced on October 27, Tokyo Stock Exchange, Inc. (“TSE”) and Nikkei Inc. (“Nikkei”) are proceeding with the joint-development of a new index. Details regarding the index have been determined as below, and the index will start to be calculated from the next March. 1. Main Points of Index (For details on constituent selection, calculation, etc., please refer to the JPX-Nikkei Mid and Small Cap Index Guidebook.) JPX-Nikkei Mid and Small Cap Index Name Abbrev.: JPX-Nikkei Mid Small No. of Constituents 200 issues Common stocks whose main market is the TSE 1st Section, 2nd Section, Mothers, or Eligible Issues JASDAQ market Constituent selection and review will be conducted as follows. [Selection Criteria] Constituents are selected according to the following process and criteria. (1) Screening ① Screening by Eligibility Criteria Constituent Issues are excluded from selection if they fall under any of the following criteria. Selection/Review ・Listed for under 3 years (excluding technical listings) Method ・Liabilities in excess of assets during any of the past 3 fiscal years ・Operating deficit in all of the past 3 fiscal years ・Overall deficit in all of the past 3 fiscal years ・Designation as Security to be Delisted, etc. 1 ② Removal of large cap issues Issues constituting the top 20% of market capitalization on the base date shall be removed from ① above. Notwithstanding the foregoing, those in the top 18% that are issues eligible as constituents of JPX-Nikkei Mid and Small Cap Index on the base date shall be removed. -

Information Productivity™ Rankings by Country

Strassmann, Inc. Global Information PRoductivity™ Rankings © Copyright 1996, All Rights Reserved Companies Total Revenues Weighted Country in Database (US$000) Average IP™ ARGENTINA 3 881,675 -0.751 AUSTRALIA 20 25,393,032 -0.119 AUSTRIA 11 12,234,878 -0.042 BELGIUM 23 17,921,628 -0.128 BRAZIL 33 60,641,605 -0.346 CANADA 311 265,364,969 -0.367 CHILE 15 8,009,723 0.017 COLOMBIA 6 1,662,989 -0.219 DENMARK 78 45,369,476 -0.159 FINLAND 57 58,337,766 0.078 FRANCE 124 511,606,973 -0.145 GERMANY 123 650,231,734 -0.036 GREECE 1 9 2,977,286 -0.606 HONG KONG 6 6,149,926 -2.658 INDIA 1 168,241 0.251 IRELAND 48 20,526,573 0.077 ITALY 161 346,779,093 -0.214 JAPAN 1,767 5,233,053,608 -0.170 KOREA (SOUTH) 41 113,933,255 -0.120 LUXEMBOURG 3 6,507,677 -0.060 MALAYSIA 2 1,158,941 0.679 MEXICO 30 28,921,380 -0.619 NETHERLANDS 78 321,808,668 0.066 NEW ZEALAND 6 5,704,196 1.097 NORWAY 65 28,838,430 0.042 PAKISTAN 2 44,402 0.302 PHILIPPINES 1 128,325 -0.325 PORTUGAL 3 301,723 1.671 SINGAPORE 1 1,388,783 -0.188 SOUTH AFRICA 9 18,655,473 0.032 SPAIN 4 3,031,222 -1.152 SWEDEN 24 75,540,278 0.117 SWITZERLAND 108 244,267,380 -0.689 TAIWAN 1 2,472,902 -0.651 THAILAND 14 2,924,239 0.292 UNITED KINGDOM 1,178 1,032,147,384 -0.032 UNITED STATES 2,959 4,839,398,019 0.077 7,335 13,994,483,852 IP Ranking within Country Overall Rank 1994 1994 IP Rank Company Name Within Country Revenues ($000) IP™ ARGENTINA 3770 ASTRA COMPANIA ARGENTINA DE PE 1 304,211 -0.127 5711 GAROVAGLIO Y ZORRAQUIN S.A.