Dr. Tim Schwanen

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Post-Pandemic Reflections: Future Mobility COVID-19’S Potential Impact on the New Mobility Ecosystem

THEMATIC INSIGHTS Post-Pandemic Reflections: Future Mobility COVID-19’s potential impact on the new mobility ecosystem msci.com msci.com 1 Contents 04 Mobility-as-a-Service and the COVID-19 shock 06 Growing Pains in the Future Mobility Market 16 Mobility Services: Expansion and Acceleration 18 COVID-19: A Catalyst for Autonomous Delivery? 2 msci.com msci.com 3 Future Mobility A growing database collated by Neckermann Strategic Advisors has over Mobility-as- 700 public and private companies involved with different elements of the autonomous Mobility-as-a-Service (MaaS) value chain. a-Service A list that doesn’t yet include all the producers of electric, two-wheeled and public transport that contribute to the full and the mobility ecosystem. In the 1910s, the automotive industry was COVID-19 shock vast, and the rising tide was lifting every boat, albeit not profitably. However, by the time the Roaring Twenties came to an end in Even prior to the COVID-19 crisis, we discussed in our first Thematic 1929, the number of US auto manufacturers Insight1 how the world might be in the midst of the largest transformation had already fallen to 44, only to consolidate in mobility since the advent of the automobile some 120 years ago. Will much further after the Great Depression. the current pandemic prove to be a system shock that accelerates the It is, of course, tempting to see a parallel demise of inflexible and unprofitable business models and acts as a to the last five years in mobility. Just prior catalyst for the growth of more digital and service-oriented businesses in to the COVID-19 crisis, there were initial the mobility space? How might industry-wide headwinds affect the new signs of stress in this tapestry of privately- business models and technologies at least in the short-term? funded companies in the Future Mobility New industries naturally go through a series of iterations before becoming ecosystem. -

Warsaw in Short

WarsaW TourisT informaTion ph. (+48 22) 94 31, 474 11 42 Tourist information offices: Museums royal route 39 Krakowskie PrzedmieÊcie Street Warsaw Central railway station Shops 54 Jerozolimskie Avenue – Main Hall Warsaw frederic Chopin airport Events 1 ˚wirki i Wigury Street – Arrival Hall Terminal 2 old Town market square Hotels 19, 21/21a Old Town Market Square (opening previewed for the second half of 2008) Praga District Restaurants 30 Okrzei Street Warsaw Editor: Tourist Routes Warsaw Tourist Office Translation: English Language Consultancy Zygmunt Nowak-Soliƒski Practical Information Cartographic Design: Tomasz Nowacki, Warsaw Uniwersity Cartographic Cathedral Photos: archives of Warsaw Tourist Office, Promotion Department of the City of Warsaw, Warsaw museums, W. Hansen, W. Kryƒski, A. Ksià˝ek, K. Naperty, W. Panów, Z. Panów, A. Witkowska, A. Czarnecka, P. Czernecki, P. Dudek, E. Gampel, P. Jab∏oƒski, K. Janiak, Warsaw A. Karpowicz, P. Multan, B. Skierkowski, P. Szaniawski Edition XVI, Warszawa, August 2008 Warsaw Frederic Chopin Airport Free copy 1. ˚wirki i Wigury St., 00-906 Warszawa Airport Information, ph. (+48 22) 650 42 20 isBn: 83-89403-03-X www.lotnisko-chopina.pl, www.chopin-airport.pl Contents TourisT informaTion 2 PraCTiCal informaTion 4 fall in love wiTh warsaw 18 warsaw’s hisTory 21 rouTe no 1: 24 The Royal Route: Krakowskie PrzedmieÊcie Street – Nowy Âwiat Street – Royal ¸azienki modern warsaw 65 Park-Palace Complex – Wilanów Park-Palace Complex warsaw neighborhood 66 rouTe no 2: 36 CulTural AttraCTions 74 The Old -

20-03 Residential Carshare Study for the New York Metropolitan Area

Residential Carshare Study for the New York Metropolitan Area Final Report | Report Number 20-03 | February 2020 NYSERDA’s Promise to New Yorkers: NYSERDA provides resources, expertise, and objective information so New Yorkers can make confident, informed energy decisions. Mission Statement: Advance innovative energy solutions in ways that improve New York’s economy and environment. Vision Statement: Serve as a catalyst – advancing energy innovation, technology, and investment; transforming New York’s economy; and empowering people to choose clean and efficient energy as part of their everyday lives. Residential Carshare Study for the New York Metropolitan Area Final Report Prepared for: New York State Energy Research and Development Authority New York, NY Robyn Marquis, PhD Project Manager, Clean Transportation Prepared by: WXY Architecture + Urban Design New York, NY Adam Lubinsky, PhD, AICP Managing Principal Amina Hassen Associate Raphael Laude Urban Planner with Barretto Bay Strategies New York, NY Paul Lipson Principal Luis Torres Senior Consultant and Empire Clean Cities NYSERDA Report 20-03 NYSERDA Contract 114627 February 2020 Notice This report was prepared by WXY Architecture + Urban Design, Barretto Bay Strategies, and Empire Clean Cities in the course of performing work contracted for and sponsored by the New York State Energy Research and Development Authority (hereafter the "Sponsors"). The opinions expressed in this report do not necessarily reflect those of the Sponsors or the State of New York, and reference to any specific product, service, process, or method does not constitute an implied or expressed recommendation or endorsement of it. Further, the Sponsors, the State of New York, and the contractor make no warranties or representations, expressed or implied, as to the fitness for particular purpose or merchantability of any product, apparatus, or service, or the usefulness, completeness, or accuracy of any processes, methods, or other information contained, described, disclosed, or referred to in this report. -

Bollore 2019

Bolloré 2019 Universal registration document Including the annual financial report This Universal registration document was filed on April 29, 2020 with the French Autorité des marchés financiers (AMF), the competent authority under EU Regulation 2017/1129, without prior approval in accordance with article 9 of said regulation. The Universal registration document may be used to support a public securities offer or admission of securities to trading on a regulated market if accompanied by a securities note and, where applicable, a summary of and all amendments made to the Universal registration document. The package thus created must be approved by the French Autorité des marchés financiers (AMF) in accordance with EU Regulation 2017/1129. The Universal registration document may be consulted and downloaded from the website www.bollore.com. Message from the Chairman 02 Overview of the Group and its activities 04 Profile 06 Key figures 08 Economic organizational chart 10 Stock exchange data 11 Our locations 12 Group strategy 14 Business model 16 CSR key figures 18 Governance 19 Activities 20 Corporate social responsibility 48 History of the Group 54 2 Non-financial performance 57 CSR challenges and strategy, four pillars of CSR engagement, duty of care, summary table, report of the independent third party 3 Risk factors and internal control 127 Risk analysis, risk management and internal control tools, compliance 1 4 Corporate governance 137 Administrative and management bodies, compensation and benefits 5 Analysis of operations and the -

Ev Shared-Use Mobility Program a Transportation Electrification Concept

EV SHARED-USE MOBILITY PROGRAM A TRANSPORTATION ELECTRIFICATION CONCEPT by Alexander Walsh Nick Nigro Atlas Public Policy April 2017 ATLAS PUBLIC POLICY WASHINGTON, DC USA EV Shared-Use Mobility Program ABOUT THIS CONCEPT SUMMARY This concept summary is part of the Transportation Electrification Toolkit, designed to help Connecticut municipalities develop strategies to encourage transportation electrification through the pairing of electric vehicles and residential solar photovoltaic systems and electric shared-use mobility solutions. The toolkit consists of summaries of each transportation electrification concept, a case study of the concept from outside Connecticut, and potential approaches to deploy the concept for policymakers. The toolkit also consists of a resource library and interactive data dashboards that provide quick access to relevant information on transportation electrification in Connecticut. The toolkit is a joint effort of Atlas Public Policy, Connecticut Green Bank, and the Connecticut Department of Energy and Environmental Protection. In 2016, Atlas Public Policy began working with the Connecticut Green Bank and the Connecticut Department of Energy and Environmental Protection on the Green Bank’s strategy to accelerate alternative fuel vehicle deployment in the state. Atlas began with a market potential assessment of various alternative fuels and vehicles tailored to local conditions in Connecticut. Atlas then identified promising electric mobility concepts, including electric vehicle shared-use mobility, the pairing of electric vehicles and residential solar, and high-powered electric vehicle charging infrastructure. Atlas evaluated the suitability of these concepts as part of a strategic planning process for the Connecticut Green Bank to help the Green Bank define its role in growing the alternative fuel vehicle market in the state. -

Shared Use Mobility: European Experience and Lessons Learned

FHWA Global Benchmarking Program Report SHARED USE MOBILITY European Experience and Lessons Learned NOTICE This document is disseminated under the sponsorship of the U.S. Department of Transportation in the interest of information exchange. The U.S. Government assumes no liability for the use of the information contained in this document. The U.S. Government does not endorse products or manufacturers. Trademarks or manufacturers’ names appear in this report only because they are considered essential to the objective of the document. QUALITY ASSURANCE STATEMENT The Federal Highway Administration (FHWA) provides high-quality information to serve Government, industry, and the public in a manner that promotes public understanding. Standards and policies are used to ensure and maximize the quality, objectivity, utility, and integrity of its information. FHWA periodically reviews quality issues and adjusts its programs and processes to ensure continuous quality improvement. Cover Photo Source: Hamburger Hochbahn AG Technical Report Documentation Page 1. Report No. 2. Government Accession 3. Recipient’s Catalog No. FHWA-PL-18-026 No. 4. Title and Subtitle 5. Report Date Shared Use Mobility: European Experience and Lessons September 2018 Learned 6. Performing Organization Code 7. Authors 8. Performing Organization Sharon Feigon, Tim Frisbie, Cassie Halls, Colin Murphy Report No. 9. Performing Organization Name and Address 10. Work Unit No. (TRAIS) Leidos Shared Use Mobility Center 11251 Roger Bacon Drive 125 S. Clark St., 17th Floor 11. Contract or Grant No. Reston, VA 20190 Chicago, IL 60603 Contract No. DTFH61-12-D-00050 12. Sponsoring Agency Name and Address 13. Type of Report and Period Federal Highway Administration Covered U.S. -

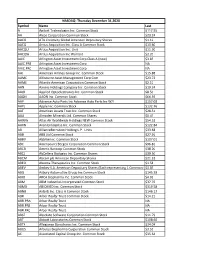

NASDAQ Index

NASDAQ- Thursday December 31,2020 Symbol Name Last A Agilent Technologies Inc. Common Stock $117.55 AA Alcoa Corporation Common Stock $23.24 AACG ATA Creativity Global American Depositary Shares $1.19 AACQ Artius Acquisition Inc. Class A Common Stock $10.60 AACQU Artius Acquisition Inc. Unit $11.30 AACQW Artius Acquisition Inc Warrant $2.20 AAIC Arlington Asset Investment Corp Class A (new) $3.85 AAIC.PRB Arlington Asset Investment Corp NA AAIC.PRC Arlington Asset Investment Corp NA AAL American Airlines Group Inc. Common Stock $15.88 AAMC Altisource Asset Management Corp Com $23.72 AAME Atlantic American Corporation Common Stock $2.10 AAN Aarons Holdings Company Inc. Common Stock $19.34 AAOI Applied Optoelectronics Inc. Common Stock $8.50 AAON AAON Inc. Common Stock $66.59 AAP Advance Auto Parts Inc Advance Auto Parts Inc W/I $157.02 AAPL Apple Inc. Common Stock $132.76 AAT American Assets Trust Inc. Common Stock $28.51 AAU Almaden Minerals Ltd. Common Shares $0.47 AAWW Atlas Air Worldwide Holdings NEW Common Stock $54.52 AAXN Axon Enterprise Inc. Common Stock $122.84 AB AllianceBernstein Holding L.P. Units $33.68 ABB ABB Ltd Common Stock $27.91 ABBV AbbVie Inc. Common Stock $107.01 ABC AmerisourceBergen Corporation Common Stock $96.81 ABCB Ameris Bancorp Common Stock $38.20 ABCL AbCellera Biologics Inc. Common Shares $39.50 ABCM Abcam plc American Depositary Shares $21.32 ABEO Abeona Therapeutics Inc. Common Stock $1.58 ABEV Ambev S.A. American Depositary Shares (Each representing 1 Common Share)$3.03 ABG Asbury Automotive Group Inc Common Stock $145.39 ABIO ARCA biopharma Inc. -

Barriers and Opportunities for Shared Battery Electric Vehicles Draft Report

Barriers and opportunities for shared battery electric vehicles Draft report Barriers and opportunities for shared battery electric vehicles A report for Transport and Environment Final report 14th January 2021 1 Element Energy Limited, Suite 1, Bishop Bateman Court, Thompson’s Lane, Cambridge, CB5 8AQ UK Tel: +44 (0)1223 852499 Barriers and opportunities for shared battery electric vehicles Final report Executive summary Background and objectives The UK government has committed to reducing carbon emissions to net zero by 2050. While it is critical that cars are rapidly transitioned to fully electric, no vehicle is ‘zero emission’ when considering the impact of vehicle production. The UK Science & Technology Committee lists reduced personal vehicle ownership as one of its 10 priorities to meet the 2050 net zero target. Transitioning to shared car models, such as electric car clubs, can reduce both car ownership and car travel demand alongside reduced in- use tailpipe emissions. Despite the benefits of shared cars, uptake in the UK has lagged behind other European countries and operators have reported facing challenges when launching or expanding car clubs (the most mature form of car sharing). The objective of this research is to review the barriers to the adoption of shared battery electric vehicles in the UK, identify opportunities for increased uptake, and make recommendations for policies and strategies to mitigate these barriers. The research benefitted from a review of the existing literature and Element Energy’s on-going work with local authorities and was complemented by interviews with industry stakeholders. Barriers to shared battery electric vehicle (BEV) adoption Car club operator perspective A number of recurring barriers to the growth of car clubs in the UK and the deployment of BEVs in their fleet were identified, the core ones are summarised in Table 1. -

Better Data for Smarter Decision-Making the Proposed Car Club-Local Authority Data Standard

Mobility • Safety • Economy • Environment Better data for smarter decision-making The proposed Car Club-Local Authority Data Standard Chenyang Wu, Aruna Sivakumar, Scott Le Vine Urban Systems Lab, Imperial College London December 2020 The Royal Automobile Club Foundation for Motoring Ltd is a transport policy and research organisation which explores the economic, mobility, safety and environmental issues relating to roads and their users. The Foundation publishes independent and authoritative research with which it promotes informed debate and advocates policy in the interest of the responsible motorist. RAC Foundation 89–91 Pall Mall London SW1Y 5HS Tel no: 020 7747 3445 www.racfoundation.org Registered Charity No. 1002705 December 2020 © Copyright Royal Automobile Club Foundation for Motoring Ltd Mobility • Safety • Economy • Environment Better data for smarter decision-making The proposed Car Club-Local Authority Data Standard Chenyang Wu, Aruna Sivakumar, Scott Le Vine Urban Systems Lab, Imperial College London December 2020 About the Author Dr Chenyang Wu is currently a Lecturer (Assistant Professor) at Southeast University (in Nanjing, China). She obtained her PhD degree at Imperial College London in 2019, and worked as a Research Associate at Imperial College London until summer 2020. Her research is focused on understanding the preference of travellers, providing mobility services based on the needs of travellers, and mitigating the problems that are brought by the excessive use of private cars. Dr Aruna Sivakumar is a senior lecturer in travel behaviour and urban systems modelling at the Centre for Transport Studies, Imperial College London. She is director of the Urban Systems Lab, and leads several smart city and systems modelling initiatives. -

London Car Club Survey | Report

www.como.org.uk 2017/18 Survey forLondon Car ClubAnnual Contents Foreword………………………………………………………………………………………………………………………………. Executive Summary ............................................................................................................. i 1 Introduction ....................................................................................................................... 1 2 Round-trip Member Survey ................................................................................................ 6 Profile of car club users ................................................................................................................ 8 Reasons for joining a car club ....................................................................................................... 9 Impact of car clubs on car ownership ......................................................................................... 10 Impact of car clubs on car purchasing ........................................................................................ 11 Impact of car clubs on miles travelled ........................................................................................ 12 Use of other shared mobility ...................................................................................................... 13 Impact of joining a car club on new members’ travel behaviour ............................................... 14 Travel behaviour of all members ............................................................................................... -

Residential Carshare Study for the New York Metropolitan Area

Residential Carshare Study for the New York Metropolitan Area Final Report | Report Number 20-03 | February 2020 NYSERDA’s Promise to New Yorkers: NYSERDA provides resources, expertise, and objective information so New Yorkers can make confident, informed energy decisions. Mission Statement: Advance innovative energy solutions in ways that improve New York’s economy and environment. Vision Statement: Serve as a catalyst – advancing energy innovation, technology, and investment; transforming New York’s economy; and empowering people to choose clean and efficient energy as part of their everyday lives. Residential Carshare Study for the New York Metropolitan Area Final Report Prepared for: New York State Energy Research and Development Authority New York, NY Robyn Marquis, PhD Project Manager, Clean Transportation Prepared by: WXY Architecture + Urban Design New York, NY Adam Lubinsky, PhD, AICP Managing Principal Amina Hassen Associate Raphael Laude Urban Planner with Barretto Bay Strategies New York, NY Paul Lipson Principal Luis Torres Senior Consultant and Empire Clean Cities NYSERDA Report 20-03 NYSERDA Contract 114627 February 2020 Notice This report was prepared by WXY Architecture + Urban Design, Barretto Bay Strategies, and Empire Clean Cities in the course of performing work contracted for and sponsored by the New York State Energy Research and Development Authority (hereafter the "Sponsors"). The opinions expressed in this report do not necessarily reflect those of the Sponsors or the State of New York, and reference to any specific product, service, process, or method does not constitute an implied or expressed recommendation or endorsement of it. Further, the Sponsors, the State of New York, and the contractor make no warranties or representations, expressed or implied, as to the fitness for particular purpose or merchantability of any product, apparatus, or service, or the usefulness, completeness, or accuracy of any processes, methods, or other information contained, described, disclosed, or referred to in this report. -

D3.1 Analysis of Business Models for Car Sharing

Ref. Ares(2018)1889878 - 09/04/2018 Research and Innovation action H2020-MG-2016-2017 Analysis of business models for car sharing Deliverable D3.1 Authors: Suzi Tart (LGI), Peter Wells (Cardiff University), & Stefano Beccaria (GM), Esti Sanvicente (LGI) www.stars-h2020.eu This project has received funding from the Horizon 2020 programme under the grant agreement n°769513 Analysis of business models for car sharing Document Information Grant Agreement 769513 Project Title Shared mobility opporTunities And challenges foR European citieS Project Acronym STARS Project Start Date 01 October 2017 Related work package WP3 – Business model innovation to enable car sharing Related task(s) Task 3.1 – Inventory of existing business models for car sharing services Lead Organisation LGI Submission date 9 April 2018 Dissemination Level PU History Date Submitted by Reviewed by Version (Notes) 18 March 2018 Suzi TART Peter WELLS, Initial collation of all Stefano BECCARIA, contributions Andrea CHICCO 6 April 2018 Suzi TART Marco DIANA Final version GA n°769513 Page 2 of 77 Analysis of business models for car sharing Table of contents SUMMARY ...................................................................... 5 1 Introduction ....................................................................................................................... 7 2 Trends in Car Sharing Business Models ....................................................................... 9 2.1 Analysis of Car Sharing Business Models ........................................................................