Upper Perkiomen School District, PA

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UPPER PERKIOMEN SCHOOL DISTRICT 2229 East Buck Road Pennsburg PA 18073

UPPER PERKIOMEN SCHOOL DISTRICT 2229 East Buck Road Pennsburg PA 18073 April 8, 2021 CALL TO ORDER The regular meeting of the Board of School Directors of the Upper Perkiomen School District was called to order by President Melanie Cunningham, at 7:00 p.m. as a virtual and in-person meeting at the Upper Perkiomen Education Center. The following Board members attended: Stephen Cunningham, Melanie Cunningham, Mike Elliott, Dana Hipszer, Raeann Hofkin, Judy Maginnis, Keith McCarrick, and Peg Pennepacker. Absent member was: Kerry Drake. Administration in attendance were: Allyn J. Roche, EdD., Andrea Farina, EdD., Sandra M. Kassel, Kimberly Bast and Georgiann Fisher. Others in attendance were: Kyle Somers, Doug Kenwood, Jim Roth, J.P. Prego, Jennifer Hartzell, Carmina Taylor, Judy Sledgen, Mary Cannon, Linda Davidheiser, and Gene Dolloff. BOARD PRESIDENT’S REPORT President Cunningham reported that she was very happy about school being back in session four days a week. Mrs. Cunningham had sent out an email to staff beforehand and said she received great feedback from many excited teachers and she hoped there were many excited students as well. Many comments that she received after school started were about how well everything was going. SUPERINTENDENT’S REPORT Dr. Roche gave an update on increased in-person instruction. He reported that there were smiles all around from students to teachers to parents to support staff. Dr. Roche said overall there was a smooth transition with a few bumps that will get better and shared pictures of the students back in the different schools. Dr. Roche reported that the high school graduation is being planned for an outdoor ceremony on Thursday June 10, 2021. -

Wyndchimes Summer 2014 #Forever14 Has a Sweet Graduation This Year’S Graduating Class Proclaimed Themselves #Forever14

The Wyndcroft School WyndChimes Summer 2014 #Forever14 Has a Sweet Graduation This year’s graduating class proclaimed themselves #Forever14. A fitting title for a group of 14 students graduating in 2014. At their Graduation, held on Friday, June 6, they were addressed by David Allain, President of the Board of Trustees. Here is a portion of his words to the class: Members of the Wyndcroft Class of 2014, let me first suggest that you are a filled candy. It’s not really important what filled candy comes to your mind, but you have been filled—or I could say it another way. You are blessed. First and most importantly you have had lots of loving, supporting family and friends, including all your teachers here at Wyndcroft. You have had amazing opportunities here to learn various academic subjects. More importantly, I hope and believe you have learned skills and attitudes: the idea of Non Sibi, working hard, managing your time, and work- ing and getting along with others. I am sure you can think of a million other lessons you have learned about others and yourself here at Wyndcroft. So you have been filled. You have been blessed. Students Achievements Recognized Each year, Wyndcroft recognizes the achievements of its students at three award The Wyndcroft ceremonies: Awards Day, Honors Day, and Graduation. School Mission At Awards Day each year, one Fifth Grader is given the Statement Jean B. Sawyer Award. This student, in the eyes of the The Wyndcroft School is a faculty, best embodies the traits of this esteemed retired Wyndcroft teacher. -

Pennsylvania Independent School Athletics Association BOYS BASKETBALL Tournament February 21, 2020

Pennsylvania independent school athletics association BOYS BASKETBALL Tournament February 21, 2020 #1 WESTTOWN SCHOOL vs. #4 PERKIOMEN SCHOOL—6:00pm #3 MALVERN PREP vs. #7 PHELPS SCHOOL—8:00pm 2019-2020 BOYS BASKETBALL SCHEDULE 21-7 DAY DATE OPPONENT TIME/RESULT Fri. Nov. 22 Rock Top W 66-55 Sat. Nov. 23 Kiski W 76-55 Sun. Nov. 24 First Love Christian Academy L 70-71 Tue. Dec. 03 @ Rock Top W 82-56 MOOSE BOYS BASKETBALL Sat. Dec. 07 @ Neumann-Goretti L 59-64 Tue. Dec. 10 George School W 71-52 No. Name Height Class Fri. Dec. 13 @ Friends' Select School W 73-35 0 Ny’mire Little 6’4” 12 Sun. Dec. 15 @ Brewster Academy W 73-72 1 Noah Collier* 6’8” 12 Fri. Dec. 20 @ Hillcrest Prep L 47-64 2 Jalen Warley* 6’5” 11 Sat. Dec. 21 @ Word of God W 46-43 3 Quin Berger 6’1” 10 Mon. Dec. 23 @ Legacy Early L 49-51 4 Trey O’Neil 5’9” 9 Sat. Dec. 28 @ Hudson Catholic W 48-27 5 Kevin Kang 6’1” 10 Sun. Dec. 29 @ National Christian Acad. W 66-56 10 Junior Yiljep 6’5” 10 Sun. Jan. 05 Hill School W 54-50 13 Isaiah Myers 5’7” 11 Tue. Jan. 07 Moorestown Friends W 83-39 20 TJ Berger* 6’4” 12 Thu. Jan. 09 Shipley School W 78-48 21 Wade Chiddick 6’4” 10 Sat. Jan. 11 Olympus Prep W 63-28 22 Franck Kepnang* 6’11” 11 Sun. Jan. 12 @ Our Savior Lutheran L 60-70 24 Dereck Lively 7’0” 10 Tue. -

The Official Boarding Prep School Directory Schools a to Z

2020-2021 DIRECTORY THE OFFICIAL BOARDING PREP SCHOOL DIRECTORY SCHOOLS A TO Z Albert College ON .................................................23 Fay School MA ......................................................... 12 Appleby College ON ..............................................23 Forest Ridge School WA ......................................... 21 Archbishop Riordan High School CA ..................... 4 Fork Union Military Academy VA ..........................20 Ashbury College ON ..............................................23 Fountain Valley School of Colorado CO ................ 6 Asheville School NC ................................................ 16 Foxcroft School VA ..................................................20 Asia Pacific International School HI ......................... 9 Garrison Forest School MD ................................... 10 The Athenian School CA .......................................... 4 George School PA ................................................... 17 Avon Old Farms School CT ...................................... 6 Georgetown Preparatory School MD ................... 10 Balmoral Hall School MB .......................................22 The Governor’s Academy MA ................................ 12 Bard Academy at Simon's Rock MA ...................... 11 Groton School MA ................................................... 12 Baylor School TN ..................................................... 18 The Gunnery CT ........................................................ 7 Bement School MA................................................. -

Navigating the Maze of Philly's Private Schools

PRIVATE SCHOOLS FROM THE PUBLISHERS OF PHILADELPHIA MAGAZINE 20 19 PRIVATE SCHOOLS REGIONAL GUIDE PRIVATE SCHOOLS 101 WITH SUCH A WEALTH OF OPTIONS, however, it can be hard to NAVIGATING THE MAZE OF know where to begin. Whether you’re looking for an elemen- tary school that will provide more support to your struggling child or a high school with exciting opportunities for your PHILLY’S PRIVATE SCHOOLS young adult, here’s a helpful guide to the Philadelphia With small class sizes, impressive facilities and region’s private schools. All it takes to ensure the best possible tight-knit communities, the appeal of a private fi t for your child is a bit of research, some careful planning, school education is clear. and an open mind to the innumerable opportunities private schools can aff ord. PHILLYMAG.COM/PRIVATESCHOOLGUIDE 55 Sponsor Content / PRIVATE SCHOOL GUIDE 20 19 PRIVATE SCHOOLS REGIONAL GUIDE ADMISSIONS 101 Acing the Application The application process can be rigorous, but with THE SEARCH Beyond that, there are also single- some preparation and sex, coeducational, boarding and organization, you’ll be well day options. on your way to a brand-new CHOOSING THE CONSIDER YOUR CHILD’S GOALS. educational experience E Is your child a budding musi- for your child. Here are a RIGHT SCHOOL cian? Do they want to be the next few things to keep in mind Jane Goodall? Or are they aiming throughout the process: “Private” is an umbrella term that for an athletic scholarship down encompasses a broad range of the line? Diff erent private schools schools that are not administered put an emphasis on research STAY ON TOP OF DEADLINES. -

Carol Dougherty

200 SEMINARY STREET • P.O. BOX 130 • PENNSBURG, PA 18073 PHONE 215-679-1131 • FAX 215-679-1146 • E-MAIL [email protected] CAROL DOUGHERTY PROFESSIONAL EXPERIENCE 1986 – present Perkiomen School Pennsburg, PA Assistant Head of School Admissions: Enrollment, Re-enrollment, Financial Aid, Marketing, Advertising, Communications materials (print, video, web) Development: Capital Campaign, Planned Giving, Grant Writing, Communications materials (print, video, web) Additional responsibilities: Schumo Academic Center and Hollenbach Middle School Center Construction Committee, Strategic Planning, Middle States Self- evaluation sub-committees College Advisor Also served as faculty member, girls’ lacrosse coach, dorm parent, yearbook advisor, newspaper advisor 1983 - 1986 The Knox School St. James, NY Faculty member Taught mathematics, computer science, social studies yearbook advisor; coached boys’ J.V. lacrosse, dorm parent EDUCATION 1988 University of Hartford Hartford, CT M.Ed. Educational Administration 1983 Hobart and William Smith Colleges Geneva, NY B.A. Political Science minor Mathematics MIDDLE STATES EVALUATIONS 2006 Assistant Chair, Ursuline Academy, New Rochelle, NY 2006 Chair of 5 year review, George School, Newtown, PA 2005 Chair, Oldfields School, Oldfields, MD CONFERENCES/WORKSHOPS 2008 The Association of Boarding Schools Conference, Baltimore, Md 2007 Association of Delaware Valley Independent Schools (ADVIS) Workshop, Branding and Marketing to Generational Differences, Rosemont, PA 2006 Harvard University, Principals -

COLLEGE COUNSELING at PERKIOMEN SCHOOL

COLLEGE COUNSELING at PERKIOMEN SCHOOL 3 FULL-TIME on-campus counselors, nationally recognized for their expertise in the field of admissions Katie Park ‘07, SOUTH KOREA Finance, University of Notre Dame 11:1 students to Vice-President, Goldman Sachs teacher ratio Halle Brown ‘17, USA 25:1 students to Engineering & Physics, Smith College Intern, NASA counselor ratio 125+ university representatives connect with students each year Closed testing site exclusively for Perkiomen students Keeshawn Kellman ‘19, USA ACT Princeton University AP® Men’s Basketball Team PSAT® TOEFL® Emma Zhao ‘19, USA Molecular & Cell Biology, SAT® University of California, Berkeley “Perkiomen School’s Office of College Counseling offers everything your student needs, accessible right here on campus. Outside consultants or agents are not necessary. The relationships built by our College Counseling team give our students an edge because of their deep, personal connections with university admissions representatives. We are fortunate to be led by David Antoniewicz, one of the leaders in the college admissions field and a Board Director for the National Association for College Admission Counseling. Our primary goal is to help our students connect with the right-fit university where they can pursue their passions and find success.” — Mark A. Devey, Head of School Rex Xu ‘19, CHINA New York University Pennsburg, Pennsylvania, USA | (215) 679-1132 | perkiomen.org Fairleigh Dickinson University (Metropolitan Campus) Neumann University Towson University Fisher College New -

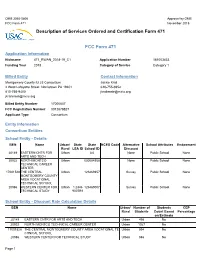

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 November 2015 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname 471_RWAN_2018-19_C1 Application Number 181003433 Funding Year 2018 Category of Service Category 1 Billed Entity Contact Information Montgomery County IU 23 Consortium Jackie Krail 2 West Lafayette Street Norristown PA 19401 610-755-9352 610-755-9400 [email protected] [email protected] Billed Entity Number 17000647 FCC Registration Number 0012678827 Applicant Type Consortium Entity Information Consortium Entities School Entity - Details BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 20149 EASTERN CNTR FOR Urban 0.0 None Public School None ARTS AND TECH 20932 NORTH MONTCO Urban 000004958 None Public School None TECHNICAL CAREER CENTER 17001528 THE CENTRAL Urban 123460957 Survey Public School None MONTGOMERY COUNTY AREA VOCATIONAL TECHNICAL SCHOOL 20986 WESTERN CENTER FOR Urban 1.2346 123469007 Survey Public School None TECHNICAL STUDY 9007E8 School Entity - Discount Rate Calculation Details BEN Name Urban/ Number of Students CEP Rural Students Count Based Percentage on Estimate 20149 EASTERN CNTR FOR ARTS AND TECH Urban 498 No 20932 NORTH MONTCO TECHNICAL CAREER CENTER Urban 1027 No 17001528 THE CENTRAL MONTGOMERY COUNTY AREA VOCATIONAL TE Urban 594 No CHNICAL SCHOOL 20986 WESTERN CENTER FOR TECHNICAL STUDY Urban 846 No Page 1 Related School District Entity - Details BEN Name Urban/ State State NCES School District -

November 12, 2020 7:00 P.M

Upper Perkiomen School District School Board Hybrid Meeting /Virtual & MS Auditorium November 12, 2020 7:00 p.m. Welcome to the regular meeting of the Board of Directors Of the Upper Perkiomen School District CODE OF ETHICS The Board of School Directors agrees to: ▪ Welcome and encourage participation and cooperation by all ▪ Work with constituents in a spirit of harmony ▪ Base decision on the facts, vote our honest convictions, and be unswayed by partisan bias ▪ Devote time, thought, and study to our duties and responsibilities ▪ Resist any temptation or outside pressure to use our position to benefit ourselves ▪ Understand and evaluate the educational program and plan for school operations ▪ Provide oversight to the business of the School District, establish policies, and vest administration in the Superintendent of Schools ▪ Help the community have all the facts, all the time, about their schools ▪ Strive to maximize school board service in a spirit of teamwork and devotion to public education BOARD OF DIRECTORS Dr. Kerry Drake, President Raeann Hofkin Mike Elliott, Vice President Judith Maginnis Stephen Cunningham, Treasurer Keith McCarrick Melanie Cunningham Peg Pennepacker Dana Hipszer Sandra Kassel, Board Secretary (non-voting member) ADMINISTRATORS Dr. Allyn J. Roche, Superintendent Dr. Andrea J. Farina, Assistant Superintendent Sandra M. Kassel, Business Administrator Georgiann M. Fisher, Director of Human Resources SOLICITOR Kyle J. Somers, Esq. Sweet Stevens Katz & Williams, LLP In order to assist in keeping an accurate record of the proceeding of this meeting, the meeting is being videotaped by the District. AGENDA –NOVEMBER 12, 2020 I. CALL TO ORDER A. Pledge of Allegiance B. -

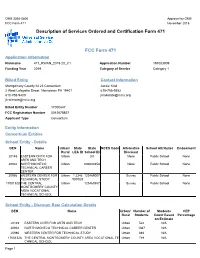

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 November 2015 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname 471_RWAN_2019-20_C1 Application Number 191003909 Funding Year 2019 Category of Service Category 1 Billed Entity Contact Information Montgomery County IU 23 Consortium Jackie Krail 2 West Lafayette Street Norristown PA 19401 610-755-9352 610-755-9400 [email protected] [email protected] Billed Entity Number 17000647 FCC Registration Number 0012678827 Applicant Type Consortium Entity Information Consortium Entities School Entity - Details BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 20149 EASTERN CNTR FOR Urban 0.0 None Public School None ARTS AND TECH 20932 NORTH MONTCO Urban 000004958 None Public School None TECHNICAL CAREER CENTER 20986 WESTERN CENTER FOR Urban 1.2346 123469007 Survey Public School None TECHNICAL STUDY 9007E8 17001528 THE CENTRAL Urban 123460957 Survey Public School None MONTGOMERY COUNTY AREA VOCATIONAL TECHNICAL SCHOOL School Entity - Discount Rate Calculation Details BEN Name Urban/ Number of Students CEP Rural Students Count Based Percentage on Estimate 20149 EASTERN CNTR FOR ARTS AND TECH Urban 522 N/A 20932 NORTH MONTCO TECHNICAL CAREER CENTER Urban 1087 N/A 20986 WESTERN CENTER FOR TECHNICAL STUDY Urban 846 N/A 17001528 THE CENTRAL MONTGOMERY COUNTY AREA VOCATIONAL TE Urban 719 N/A CHNICAL SCHOOL Page 1 Related School District Entity - Details BEN Name Urban/ State State NCES School -

Annual Report 2014

CLIMB ON annual report 2014 A WORD FROM OUR EXECUTIVE DIRECTOR POBS RESULTS IN 2014 FINANCIALS Dear Friends: UNAUDITED FOR 2014 $63,000 RESTRICTED OPERATIONAL 2014 was an adventurous year at the Philadelphia Outward SINGLE- AND MULTI-DAY COURSE OFFERINGS POBS REVENUE OVERVIEW 2014: FUNDS Bound School. $1,485,000 2012 2013 2014 You may have met one of the 4,100 students who participated 120 in one of our experiential education programs this past 110 year. You may have spoken with one of our instructors who collectively delivered 9,191 student program days in 2014. 95 100 Or, you may have seen us in the news during our annual Building Adventure event in mid-October where over 120 78 80 people rappelled 31 stories (418 feet) from the top of One Logan Square in Center City. The Philadelphia Outward Bound School is the “school” that inspires leadership and 5755 60 service to communities through single and multi-day 51 outdoor experiences that change lives through challenge and discovery. 40 2014 In truth, the Philadelphia Outward Bound School is not a 21 20 REVENUE traditional educational institution. We educate by “doing,” 11 12 10 $805,000 $617,000 and our students find us through our many partnerships 5 6 TOTAL FUNDS PROGRAM TUITION & with schools and youth-serving organizations across the 0 RAISED CO-PAYS greater Philadelphia metropolitan region. Together, with these educational partners, we inspire more than 4,000 SHORT LONG CORPORATE ONE-DAY EXPEDITION EXPEDITION TEAMBUILDING INSIGHT youth to be more than they thought they could be - and to (</= 7 DAYS) (8+ DAYS) PROGRAMS PROGRAMS graduate from high school, to finish college and to return home to make their world a better place. -

Schools Eligible to Receive Opportunity Scholarship Students In

Schools Eligible to Receive Opportunity Scholarship Students in the 2015-16 School Year For additional details about any of the schools listed, please refer to the contact information provided. Additional information about the Opportunity Scholarship Tax Credit Program can be found on the Pennsylvania Department of Community and Economic Development's website at www.newpa.com/ostc. Designation (Public/ County School Name Contact Address Phone Number Email Address Tuition and Fees for the 2014-15 School Year Nonpublic) Adams County Christian Norma Coates, 1865 Biglerville Rd., Elementary school tuition - $4,680 (K-6); High school Adams Academy Nonpublic Secretary Gettysburg, PA 17325 717-334-6793 [email protected] tuition - $4,992 (7-12) Registration fee- $150 Mrs. Patricia Foltz, 316 North St., Tuition - $3,125 (Catholic); $4,200 (Non-Catholic); Adams Annunciation B.V.M. Nonpublic Principal McSherrytown, PA 17344 717-637-3135 [email protected] Registration fee - $75 140 S Oxford Ave., Maureen C. Thiec, McSherrystown, PA Adams Delone Catholic High School Nonpublic Ed.D., Principal 17344 717-637-5969 [email protected] Tuition - $5,400 (Catholic); $7,080 (Non-Catholic) Karen L. Trout, 3185 York Rd., Adams Freedom Christian Schools Nonpublic Principal Gettysburg, PA 17325 717-624-3884 [email protected] $3,240 Gettysburg Seventh-Day Marian E. Baker, 1493 Biglerville Rd., Adams Adventist Church School Nonpublic Principal Gettysburg, PA 17325 717-338-1031 [email protected] Tuition for kindergarten - $3,800; Registration fee - $325 Donna Hoffman, 101 N Peter St., New Adams Immaculate Conception Nonpublic Principal Oxford, PA 17350 717-624-2061 [email protected] Tuition - $2,900 (Catholic); $4,700 (Non-Catholic) Crystal Noel, 55 Basicila Rd., Hanover, Adams Sacred Heart Nonpublic Principal PA 17331 717-632-8715 [email protected] Tuition - $2,875 (Catholic); $3,950 (Non-Catholic) Rebecca Sieg, 465 Table Rock Rd., Adams St.