United Japan Growth Fund

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Alma Eikoh Japan Large Cap Equity Fund a Sub-Fund of Alma Capital Investment Funds SICAV

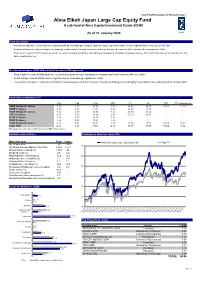

FOR PROFESSIONAL INVESTORS ONLY Alma Eikoh Japan Large Cap Equity Fund A sub-fund of Alma Capital Investment Funds SICAV As of 31 January 2020 Eikoh Fund description • Investment objective: seek long-term capital growth by investing generally in Japanese large cap stocks (with market capitalisation in excess of US$ 1bn) • Investment process: analyse long term company fundamentals through extensive in-house bottom up research with a strong risk management ethos • Portfolio of around 25-30 companies which are well managed, profitable and with good prospects. Portfolio managers believe that Cash Flow Return on Investment and value creation are key Investment manager: ACIM (Alma Capital Investment Management) • Alma Capital Investment Management is a Luxembourg based asset management company and holds a branch office in London • ACIM manages assets of $4bn and is regulated by the Luxembourg regulator the CSSF • The portfolio managers, led by James Pulsford, worked together at Eikoh Research Investment Management managing the portfolio before joining ACIM in January 2020 Cumulative performance (%) 1 M 3 M 6 M YTD 1Y 3Y ITD ITD (annualized) I GBP Hedged C shares -0.29 4.47 12.94 -0.29 24.54 26.44 86.03 11.36 I GBP C shares -0.58 2.63 4.95 -0.58 23.80 24.93 - - I EUR Hedged C shares -0.43 4.29 12.94 -0.43 23.69 23.44 - - I JPY C shares -0.35 4.53 13.85 -0.35 25.10 26.48 - - I EUR C shares 1.36 5.60 14.74 1.36 - - - - I EUR D shares 1.36 5.58 14.67 1.36 - - - - I USD Hedged C shares -0.20 5.06 14.81 -0.20 27.84 33.92 94.05 12.47 Topix (TR) -2.14 1.21 8.88 -2.14 10.17 18.46 53.20 7.86 Fund launched on 12 June 2014 (I USD Hedged C and I GBP Hedged C shares) Portfolio characteristics Performance (Indexed - Base 100) Main indicators Fund Index Alma Eikoh Japan Large Cap Equity Fund Topix TR No. -

Factset-Top Ten-0521.Xlsm

Pax International Sustainable Economy Fund USD 7/31/2021 Port. Ending Market Value Portfolio Weight ASML Holding NV 34,391,879.94 4.3 Roche Holding Ltd 28,162,840.25 3.5 Novo Nordisk A/S Class B 17,719,993.74 2.2 SAP SE 17,154,858.23 2.1 AstraZeneca PLC 15,759,939.73 2.0 Unilever PLC 13,234,315.16 1.7 Commonwealth Bank of Australia 13,046,820.57 1.6 L'Oreal SA 10,415,009.32 1.3 Schneider Electric SE 10,269,506.68 1.3 GlaxoSmithKline plc 9,942,271.59 1.2 Allianz SE 9,890,811.85 1.2 Hong Kong Exchanges & Clearing Ltd. 9,477,680.83 1.2 Lonza Group AG 9,369,993.95 1.2 RELX PLC 9,269,729.12 1.2 BNP Paribas SA Class A 8,824,299.39 1.1 Takeda Pharmaceutical Co. Ltd. 8,557,780.88 1.1 Air Liquide SA 8,445,618.28 1.1 KDDI Corporation 7,560,223.63 0.9 Recruit Holdings Co., Ltd. 7,424,282.72 0.9 HOYA CORPORATION 7,295,471.27 0.9 ABB Ltd. 7,293,350.84 0.9 BASF SE 7,257,816.71 0.9 Tokyo Electron Ltd. 7,049,583.59 0.9 Munich Reinsurance Company 7,019,776.96 0.9 ASSA ABLOY AB Class B 6,982,707.69 0.9 Vestas Wind Systems A/S 6,965,518.08 0.9 Merck KGaA 6,868,081.50 0.9 Iberdrola SA 6,581,084.07 0.8 Compagnie Generale des Etablissements Michelin SCA 6,555,056.14 0.8 Straumann Holding AG 6,480,282.66 0.8 Atlas Copco AB Class B 6,194,910.19 0.8 Deutsche Boerse AG 6,186,305.10 0.8 UPM-Kymmene Oyj 5,956,283.07 0.7 Deutsche Post AG 5,851,177.11 0.7 Enel SpA 5,808,234.13 0.7 AXA SA 5,790,969.55 0.7 Nintendo Co., Ltd. -

The Demonstra#On of Smart City and Expansion to the Urban Disaster

1 The demonstraon of smart city and expansion to the urban disaster recovery promo-on area in Japan Toshiba corporaon Community Solu-on Div. Yoshimasa Kudo 2 Contents ! " Japanese Smart City Demonstraon ! " Toshiba’s success story - Miyako island smart grid system - Yokohama smart city project ! " Concept of Toshiba’s smart city ! " Urban disaster recovery area in Japan 3 Contents ! " Japanese Smart City Demonstraon ! " Toshiba’s success story - Miyako island smart grid system - Yokohama smart city project ! " Concept of Toshiba’s smart city ! " Urban disaster recovery area in Japan 4 Roadmap of smart city project 2009 2010 2011 2012 2013 2014 2015 - Miyako island smart grid project Energy stabilization Demand response project Effects & evaluaon of large PV/ many PV Distribution network system of next generations Energy management of Realiza<on of electric and thermal control smart city Energy conservaon project (BEMS/HEMS) Demonstration Smart EV project of basic technology (EV charging) New Mexico smart grid project (Overseas project) & others Demonstration The four-location smart city operational experiments (Japanese project) & others of smart city Business model project Earthquake (DR, Aggregator) 5 Contents ! " Japanese Smart City Demonstraon ! " Toshiba’s success story - Miyako island smart grid system - Yokohama smart city project ! " Concept of Toshiba’s smart city ! " Urban disaster recovery area in Japan 6 Miyako island smart grid system 7 Major smart city project in Japan 4 areas were selected as the smart city of first pilot -

Mitsui Fudosan and LINK-J to Participate in the BRAVE

Press Release December 7, 2016 Beyond Next Ventures Life Science Innovation Network Japan, Inc. (LINK-J) Mitsui Fudosan Co. Ltd. Mitsui Fudosan and LINK-J to Participate in the BRAVE Acceleration Program as Partners to Support Business Startups of University-originated Technology Business Ventures Life Sciences Award established at the Final Examination to invite the winner to a U.S. event organized by Biocom, with approximately 800 members around the world Tokyo, Japan, December 7, 2016 - Life Science Innovation Network Japan Inc. (LINK-J), an incorporated association founded by Mitsui Fudosan Co., Ltd. (Mitsui Fudosan) and a group of volunteers from academia, and Mitsui Fudosan are pleased to announce that they will take part in the BRAVE Acceleration Program operated by Beyond Next Ventures Inc. (Beyond Next Ventures), a company making incubation investments in university-originated technology business ventures, as corporate partners. Beyond Next Ventures is a venture capital firm with strength in incubation investments in university-originated technology business ventures at the seed level in the fields of medical and health care, robots, artificial intelligence (AI), Internet of Things (IoT), big data and other advanced technologies. In November 2016, it moved its head office from Chiyoda-ku to Nihonbashi in Chuo-ku in Tokyo, where life sciences firms are clustered. Its president and representative director Tsuyoshi Ito serves as a LINK-J Supporter*. Outline of the BRAVE Acceleration Program The BRAVE Acceleration Program is a platform that helps researchers and entrepreneurs in universities and research institutes and those aiming for commercialization to launch business based on innovative technologies. It is intended to offer knowledge, expertise and a network for achieving commercialization. -

Stoxx® Japan 600 Esg-X Index

STOXX® JAPAN 600 ESG-X INDEX Components1 Company Supersector Country Weight (%) Toyota Motor Corp. Automobiles & Parts Japan 3.87 Sony Corp. Consumer Products & Services Japan 2.55 Softbank Group Corp. Telecommunications Japan 2.44 Keyence Corp. Industrial Goods & Services Japan 1.77 RECRUIT HOLDINGS Industrial Goods & Services Japan 1.54 Mitsubishi UFJ Financial Group Banks Japan 1.48 Shin-Etsu Chemical Co. Ltd. Chemicals Japan 1.36 Nippon Telegraph & Telephone C Telecommunications Japan 1.36 Nintendo Co. Ltd. Consumer Products & Services Japan 1.30 Nidec Corp. Technology Japan 1.30 Fast Retailing Co. Ltd. Retail Japan 1.25 Daikin Industries Ltd. Construction & Materials Japan 1.19 Takeda Pharmaceutical Co. Ltd. Health Care Japan 1.18 Tokyo Electron Ltd. Technology Japan 1.16 Honda Motor Co. Ltd. Automobiles & Parts Japan 1.10 Daiichi Sankyo Co. Ltd. Health Care Japan 1.08 Sumitomo Mitsui Financial Grou Banks Japan 1.04 Murata Manufacturing Co. Ltd. Technology Japan 1.03 KDDI Corp. Telecommunications Japan 1.02 Hitachi Ltd. Industrial Goods & Services Japan 0.92 Itochu Corp. Industrial Goods & Services Japan 0.92 Fanuc Ltd. Industrial Goods & Services Japan 0.90 Hoya Corp. Health Care Japan 0.84 Mitsubishi Corp. Industrial Goods & Services Japan 0.83 Mizuho Financial Group Inc. Banks Japan 0.76 SOFTBANK Telecommunications Japan 0.75 Denso Corp. Automobiles & Parts Japan 0.72 Mitsui & Co. Ltd. Industrial Goods & Services Japan 0.71 Tokio Marine Holdings Inc. Insurance Japan 0.70 Oriental Land Co. Ltd. Travel & Leisure Japan 0.68 SMC Corp. Industrial Goods & Services Japan 0.68 Mitsubishi Electric Corp. Industrial Goods & Services Japan 0.67 Seven & I Holdings Co. -

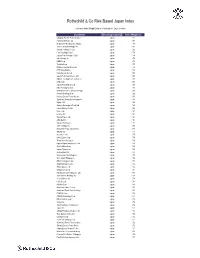

Rothschild & Co Risk-Based Japan Index

Rothschild & Co Risk-Based Japan Index Indicative Index Weight Data as of January 31, 2020 on close Constituent Exchange Country Index Weight (%) Chugoku Electric Power Co Inc/ Japan 1.01 Yamada Denki Co Ltd Japan 0.91 McDonald's Holdings Co Japan L Japan 0.88 Sushiro Global Holdings Ltd Japan 0.82 Skylark Holdings Co Ltd Japan 0.82 Fast Retailing Co Ltd Japan 0.78 Japan Post Holdings Co Ltd Japan 0.78 Ain Holdings Inc Japan 0.78 KDDI Corp Japan 0.77 Toshiba Corp Japan 0.75 Mizuho Financial Group Inc Japan 0.74 NTT DOCOMO Inc Japan 0.73 Kobe Bussan Co Ltd Japan 0.72 Japan Post Insurance Co Ltd Japan 0.69 Nippon Telegraph & Telephone C Japan 0.69 LINE Corp Japan 0.69 Japan Post Bank Co Ltd Japan 0.68 Nitori Holdings Co Ltd Japan 0.67 MS&AD Insurance Group Holdings Japan 0.66 Konami Holdings Corp Japan 0.66 Kyushu Electric Power Co Inc Japan 0.65 Sumitomo Realty & Development Japan 0.65 Fujitsu Ltd Japan 0.63 Suntory Beverage & Food Ltd Japan 0.63 Japan Airlines Co Ltd Japan 0.62 NEC Corp Japan 0.61 Lawson Inc Japan 0.60 Sekisui House Ltd Japan 0.60 ABC-Mart Inc Japan 0.60 Kyushu Railway Co Japan 0.60 ANA Holdings Inc Japan 0.59 Mitsubishi Heavy Industries Lt Japan 0.58 ORIX Corp Japan 0.57 Secom Co Ltd Japan 0.57 Seiko Epson Corp Japan 0.56 Trend Micro Inc/Japan Japan 0.56 Nippon Paper Industries Co Ltd Japan 0.56 Suzuki Motor Corp Japan 0.56 Japan Tobacco Inc Japan 0.55 Aozora Bank Ltd Japan 0.55 Sony Financial Holdings Inc Japan 0.55 West Japan Railway Co Japan 0.54 MEIJI Holdings Co Ltd Japan 0.54 Sugi Holdings Co Ltd Japan 0.54 Tokyo -

List:The 2019 Competitive IT Strategy Companies

Selection of Companies for 2019 Competitive IT Strategy Company Stock Selection and and Noteworthy IT Strategy Companies Programs Announced - METI and the TSE selected outstanding listed companies implementing a Competitive IT Strategy to enhance corporate value - The Ministry of Economy, Trade and Industry (METI) and the Tokyo Stock Exchange (TSE) have jointly been conducting a selection of outstanding companies for their efforts for IT utilization under the Competitive IT Strategy Company Stock Selection program. METI hereby announces that METI and the TSE have selected 29 companies under the 2019 Competitive IT Strategy Company Stock Selection program and 20 companies under the 2019 Noteworthy IT Strategy Companies program. These programs were held five times this year. 1. Outline of the Competitive IT Strategy Company Stock Selection program The program targets TSE-listed companies proactively engaging in efforts for IT utilization to improve management innovations, earnings and productivity in terms of improving mid- to long-term corporate value and fortifying competitiveness. METI and the TSE select such companies among all TSE-listed companies as Competitive IT Strategy Company Stocks by sector and introduce them to the public. In the 2019 program, METI and the TSE assessed companies that have been engaging in promotion of efforts for digital transformation (DX)* in accordance with the DX Promotion Guidelines and whose management has strongly been committed to such efforts. To assess companies’ current efforts for IT utilization, METI conducted a survey titled “2019 Survey of Competitive IT Strategies,” targeting all TSE-listed companies. In screening candidate companies, METI assigned scores to the responses concerning the following five areas and financial situation, and finally selected 29 companies screened by the final examination of the examination committee. -

Mitsui Fudosan Co., Ltd. Notice of the 109Th Ordinary General

[Translation for Reference and Convenience Purposes Only] Please note that the following is an unofficial English translation of the original Japanese text of the Notice of the 109th Ordinary General Shareholders’ Meeting of Mitsui Fudosan Co., Ltd. The Company provides this translation for reference and convenience purposes only and without any warranty as to its accuracy or otherwise. In the event of any discrepancy between this translation and the original Japanese, the latter shall prevail. Securities Code: 8801 June 7, 2021 To the Shareholders of Mitsui Fudosan Co., Ltd. Masanobu Komoda President and Chief Executive Officer Mitsui Fudosan Co., Ltd. 1-1, Nihonbashi Muromachi 2-chome Chuo-ku, Tokyo, Japan Notice of the 109th Ordinary General Shareholders’ Meeting Mitsui Fudosan Co., Ltd. (hereinafter referred to as the “Company”) announces that the 109th Ordinary General Shareholders’ Meeting (hereinafter referred to as the “Meeting”) will be held, as given below. Instead of attending the Meeting, you can exercise your voting rights in writing or via the Internet as provided below. Please take the time to review the attached Reference Materials for the Meeting, and exercise your voting rights by no later than 5:30 p.m. on Monday, June 28, 2021 (Tokyo Time). Exercise of voting rights You may exercise your voting rights by one of the following three methods. Please review the attached Reference Materials (on pages 4 to 17) for the Meeting, and exercise your voting rights. Recommended 1. Exercise of voting rights in writing Please indicate your approval or disapproval of each proposed item on the attached Exercise of Voting Rights form, and return the form to the Company. -

Ranking of Stocks by Market Capitalization(As of End of Dec.2018)

Ranking of Stocks by Market Capitalization(As of End of Dec.2018) 1st Section Rank Code Issue Market Capitalization \100mil. 1 7203 TOYOTA MOTOR CORPORATION 209,027 2 9437 NTT DOCOMO,INC. 93,517 3 9984 SoftBank Group Corp. 80,403 4 8306 Mitsubishi UFJ Financial Group,Inc. 74,378 5 6861 KEYENCE CORPORATION 67,709 6 6758 SONY CORPORATION 67,664 7 9433 KDDI CORPORATION 66,439 8 9434 SoftBank Corp. 65,009 9 9983 FAST RETAILING CO.,LTD. 59,793 10 9432 NIPPON TELEGRAPH AND TELEPHONE CORPORATION 56,992 11 7182 JAPAN POST BANK Co.,Ltd. 54,450 12 7267 HONDA MOTOR CO.,LTD. 52,431 13 8316 Sumitomo Mitsui Financial Group,Inc. 51,008 14 8058 Mitsubishi Corporation 48,020 15 9022 Central Japan Railway Company 47,719 16 6098 Recruit Holdings Co.,Ltd. 45,154 17 8411 Mizuho Financial Group,Inc. 43,243 18 3382 Seven & I Holdings Co.,Ltd. 42,398 19 7974 Nintendo Co.,Ltd. 41,487 20 4661 ORIENTAL LAND CO.,LTD. 40,205 21 7751 CANON INC. 40,026 22 4452 Kao Corporation 39,848 23 6902 DENSO CORPORATION 38,554 24 8766 Tokio Marine Holdings,Inc. 37,683 25 6594 NIDEC CORPORATION 37,193 26 7201 NISSAN MOTOR CO.,LTD. 37,154 27 9020 East Japan Railway Company 37,078 28 4063 Shin-Etsu Chemical Co.,Ltd. 36,500 29 4519 CHUGAI PHARMACEUTICAL CO.,LTD. 35,707 30 2914 JAPAN TOBACCO INC. 34,886 31 6367 DAIKIN INDUSTRIES,LTD. 34,279 32 6954 FANUC CORPORATION 34,013 33 6981 Murata Manufacturing Co.,Ltd. -

Presentation 6

Yokohama Smart City Project (Project cost: 13 billion USD) (Coordination between Yokohama City, 34 businesses, and 15 projects) Development of community‐based energy management covering a large area of existing urban districts and its feasibility project Installed/target (between FYs 2010 and 2014) HEMS 4,200 cases PV panels 37 MW, electrical vehicles 2,300 units Residential complexes Condominium equipped with HEMS (JX Nippoin Oil & Energy, Batteries for demand/supply control Battery SCADA equipped with HEMS (Tokyo Mitsui Fudosan Residential and Toshiba) (Toshiba, Hitachi, Meidensha and NEC) (Toshiba and TEPCO) Homes with HEMS Gas, (Panasonic) NTT‐F and NTT Docomo) Condominium with HEMS Customer batteries (Sony (Daikyo Astage) Energy Devices and Sharp) Homes with HEMS (Mitsui Data exchange system Fudosan Residential and Battery SCADA (Hitachi and Toshiba) Toshiba) FEMS (Meidensha and HEMS CEMS (Toshiba and Sumitomo Electric Recharging stations (JX Nippoin Oil & Energy Accenture) Industries) and Tokyo Institute of Technology) CARWINGS Data Center FEMS (Nissan Motor Corporation) CEMS Integrated BEMS (Toshiba) Smart BEMS (Toshiba and Taisei Corporation) EV Smart BEMS (JGC Corporation Chargeable and Dischargeable EVs (Nissan Motor BEMS for commercial buildings and JGC Information Systems Corporation, Hitachi, ORIX and (Toshiba, Marubeni, Mitsubishi Company) ORIX Auto Corporation) Estate and Smart BEMS (Meidensha Mitsui Fudosan) Smart BEMS (Shimizu and NEC) BEMS Corporation) 1 City to City Collaboration Country Bilateral Cooperation Japan JICA,JBIC,ADB,WB, etc Collaboration with aid and international agencies City City to City Collaboration Yokohama Technical Cooperation in Urban Development Private Sectors B to B and Academic Private And Academies Collaboration Sectors and Academies Support in Urban Development through PPP PPP dialogue to provide urban solutions 2 Goal 6. -

Printmgr File

November 30, 2020 Semi-Annual Report DBX ETF Trust Xtrackers Eurozone Equity ETF (EURZ) Xtrackers International Real Estate ETF (HAUZ) Xtrackers Japan JPX-Nikkei 400 Equity ETF (JPN) DBX ETF Trust Table of Contents Page Shareholder Letter ....................................................................... 1 Portfolio Summary Xtrackers Eurozone Equity ETF ......................................................... 3 Xtrackers International Real Estate ETF .................................................. 4 Xtrackers Japan JPX-Nikkei 400 Equity ETF .............................................. 5 Fees and Expenses ....................................................................... 6 Schedules of Investments Xtrackers Eurozone Equity ETF ......................................................... 7 Xtrackers International Real Estate ETF .................................................. 12 Xtrackers Japan JPX-Nikkei 400 Equity ETF .............................................. 21 Statements of Assets and Liabilities ........................................................ 26 Statements of Operations ................................................................. 27 Statements of Changes in Net Assets ....................................................... 28 Financial Highlights ...................................................................... 30 Notes to Financial Statements ............................................................. 32 Additional Information ................................................................... -

Annual Report(1.3MB)

This annual report is printed with 100% recycled paper utilizing used OA paper collected from office buildings managed by Mitsui Fudosan. Annual Report 2003 Year ended March 31, 2003 ANNUAL REPORT 2003 This report was produced in July, 2003 Printed in Japan Profile Corporate Data (Parent Company) The MITSUI FUDOSAN GROUP is Japan’s Largest Comprehensive Real Estate Group. The Group’s businesses comprise “leasing,” “sales of Mitsui Fudosan Co., Ltd. housing, office building and land,” “construction,” “brokerage, consignment sales and consulting,” “property management,” Head Office : “sales of housing materials and merchandise,” “facility 1-1, Nihonbashi-Muromachi 2-chome, Chuo-ku, Tokyo, operations” and “others.” 103-0022, Japan The real estate market in Japan is undergoing significant Date of Establishment : transformation in the wake of global changes in views toward July 15, 1941 real estate and the makeup of real estate markets. Quick to grasp these trends and changes, Mitsui Fudosan Co., Ltd. Share Capital : remains in a constant state of evolution. ¥134,433 million Looking beyond existing real estate business convention, the Mitsui Fudosan Group strives to Listing : make optimal use of its power to create value Tokyo, Osaka, Sapporo with the ultimate goal of reinforcing its presence as a leading real estate company. Number of Shares : Authorized: 1,770,000,000 Issued and outstanding: 823,390,384 Corporate Data 55 Number of Shareholders : 53,252 Number of Employees : 1,655 URL : http://www.mitsuifudosan.co.jp/english E-mail : [email protected] Contents Consolidated Financial Highlights ................................. 1 Cautionary Statement To Our Shareholders ..................................................... 2 Statements made in this report with respect to the Mitsui Fudosan Group’s current plans, estimates, Feature Article .............................................................