The 2020 Vision of Saudi Arabia's Vision 2030

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Saudi Arabia

The Programme for International Student Assessment (PISA) is a triennial survey of 15-year-old students that assesses the extent to which they have acquired the key knowledge and skills essential for full participation in society. The assessment focuses on proficiency in reading, mathematics, science and an innovative domain (in 2018, the innovative domain was global competence), and on students’ well-being. Saudi Arabia What 15-year-old students in Saudi Arabia know and can do Figure 1. Snapshot of performance in reading, mathematics and science Note: Only countries and economies with available data are shown. Source: OECD, PISA 2018 Database, Tables I.1 and I.10.1. • Students in Saudi Arabia scored lower than the OECD average in reading, mathematics and science. • Compared to the OECD average, a smaller proportion of students in Saudi Arabia performed at the highest levels of proficiency (Level 5 or 6) in at least one subject; at the same time a smaller proportion of students achieved a minimum level of proficiency (Level 2 or higher) in all three subjects. 2 | Saudi Arabia - Country Note - PISA 2018 Results What students know and can do in reading • In Saudi Arabia, 48% of students attained at least Level 2 proficiency in reading. These students can identify the main idea in a text of moderate length, find information based on explicit, though sometimes complex criteria, and can reflect on the purpose and form of texts when explicitly directed to do so. • Almost no student was a top performer in reading, meaning that they attained Level 5 or 6 in the PISA reading test. -

United Arab Emirates (Uae)

Library of Congress – Federal Research Division Country Profile: United Arab Emirates, July 2007 COUNTRY PROFILE: UNITED ARAB EMIRATES (UAE) July 2007 COUNTRY اﻟﻌﺮﺑﻴّﺔ اﻟﻤﺘّﺤﺪة (Formal Name: United Arab Emirates (Al Imarat al Arabiyah al Muttahidah Dubai , أﺑﻮ ﻇﺒﻲ (The seven emirates, in order of size, are: Abu Dhabi (Abu Zaby .اﻹﻣﺎرات Al ,ﻋﺠﻤﺎن Ajman , أ مّ اﻟﻘﻴﻮﻳﻦ Umm al Qaywayn , اﻟﺸﺎرﻗﺔ (Sharjah (Ash Shariqah ,دﺑﻲّ (Dubayy) .رأس اﻟﺨﻴﻤﺔ and Ras al Khaymah ,اﻟﻔﺠﻴﺮة Fajayrah Short Form: UAE. اﻣﺮاﺗﻰ .(Term for Citizen(s): Emirati(s أﺑﻮ ﻇﺒﻲ .Capital: Abu Dhabi City Major Cities: Al Ayn, capital of the Eastern Region, and Madinat Zayid, capital of the Western Region, are located in Abu Dhabi Emirate, the largest and most populous emirate. Dubai City is located in Dubai Emirate, the second largest emirate. Sharjah City and Khawr Fakkan are the major cities of the third largest emirate—Sharjah. Independence: The United Kingdom announced in 1968 and reaffirmed in 1971 that it would end its treaty relationships with the seven Trucial Coast states, which had been under British protection since 1892. Following the termination of all existing treaties with Britain, on December 2, 1971, six of the seven sheikhdoms formed the United Arab Emirates (UAE). The seventh sheikhdom, Ras al Khaymah, joined the UAE in 1972. Public holidays: Public holidays other than New Year’s Day and UAE National Day are dependent on the Islamic calendar and vary from year to year. For 2007, the holidays are: New Year’s Day (January 1); Muharram, Islamic New Year (January 20); Mouloud, Birth of Muhammad (March 31); Accession of the Ruler of Abu Dhabi—observed only in Abu Dhabi (August 6); Leilat al Meiraj, Ascension of Muhammad (August 10); first day of Ramadan (September 13); Eid al Fitr, end of Ramadan (October 13); UAE National Day (December 2); Eid al Adha, Feast of the Sacrifice (December 20); and Christmas Day (December 25). -

BAHRAIN and the BATTLE BETWEEN IRAN and SAUDI ARABIA by George Friedman, Strategic Forecasting, Inc

BAHRAIN AND THE BATTLE BETWEEN IRAN AND SAUDI ARABIA By George Friedman, Strategic Forecasting, Inc. The world's attention is focused on Libya, which is now in a state of civil war with the winner far from clear. While crucial for the Libyan people and of some significance to the world's oil markets, in our view, Libya is not the most important event in the Arab world at the moment. The demonstrations in Bahrain are, in my view, far more significant in their implications for the region and potentially for the world. To understand this, we must place it in a strategic context. As STRATFOR has been saying for quite a while, a decisive moment is approaching, with the United States currently slated to withdraw the last of its forces from Iraq by the end of the year. Indeed, we are already at a point where the composition of the 50,000 troops remaining in Iraq has shifted from combat troops to training and support personnel. As it stands now, even these will all be gone by Dec. 31, 2011, provided the United States does not negotiate an extended stay. Iraq still does not have a stable government. It also does not have a military and security apparatus able to enforce the will of the government (which is hardly of one mind on anything) on the country, much less defend the country from outside forces. Filling the Vacuum in Iraq The decision to withdraw creates a vacuum in Iraq, and the question of the wisdom of the original invasion is at this point moot. -

Saudi Arabia.Pdf

A saudi man with his horse Performance of Al Ardha, the Saudi national dance in Riyadh Flickr / Charles Roffey Flickr / Abraham Puthoor SAUDI ARABIA Dec. 2019 Table of Contents Chapter 1 | Geography . 6 Introduction . 6 Geographical Divisions . 7 Asir, the Southern Region � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �7 Rub al-Khali and the Southern Region � � � � � � � � � � � � � � � � � � � � � � � � � �8 Hejaz, the Western Region � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �8 Nejd, the Central Region � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �9 The Eastern Region � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �9 Topographical Divisions . .. 9 Deserts and Mountains � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �9 Climate . .. 10 Bodies of Water . 11 Red Sea � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 11 Persian Gulf � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 11 Wadis � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 11 Major Cities . 12 Riyadh � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �12 Jeddah � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �13 Mecca � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � -

NEOM: $500Bn Smart City

NEOM: $500Bn Smart City Key Facts “NEOM will be Key Saudi Vision 2030 Project constructed from the 26,500 sqkm of space straddling Saudi ground-up, on greenfield to be invested by the Public Investment Arabia, Jordan and Egypt making NEOM the $500 billion first private zone to span three countries sites, allowing it a Fund, apart from private and global investors unique opportunity to be First phase to be completed by 2025 EGYPT JORDAN S.ARABIA distinguished from all other places that have Special zone with autonomous judicial system & been developed and economic framework Situated in an area rich in wind and solar energy constructed over 468 km of pristine resources coastline and hundreds of years and Aspirations for NEOM spectacular beaches A new local tourist we will use this NEOM’s contribution to the Kingdom’s GDP is set NEOM destination for opportunity to build a to reach at least $100 billion by 2030 Saudi citizens new way of life with Highest GDP per capita in the world 70% of the world’s excellent economic population lives 8 Free highest-speed internet prospects.” Around 10% of hours flight away the world’s trade Net zero carbon footprint His Royal Highness Prince Mohammed bin flows through the Salman bin Abdulaziz Al Saud, Crown Prince, Red Sea 10 degrees cooler Deputy Prime Minister and Chairman of the A destination topping the 'world’s most than rest of GCC livable cities index' Public Investment Fund. Key pillars of NEOM economy: $70Bn opportunity Energy & Water Mobility Biotech Food Advanced Media Entertainment Technology Living Powered by Connected with Hub for Cutting-edge Manufacturing Hub for production Centre of sports, Artificial Modern renewable energy 100% green next-generation technologies such Home to innovations houses and studios performance and intelligence. -

New Saudi Poll Shows Sharp Rise in Support for Israel Ties, Despite Caveats by David Pollock

MENU Policy Analysis / Fikra Forum Correction: New Saudi Poll Shows Sharp Rise in Support for Israel Ties, Despite Caveats by David Pollock Dec 8, 2020 Also available in Arabic ABOUT THE AUTHORS David Pollock David Pollock is the Bernstein Fellow at The Washington Institute, focusing on regional political dynamics and related issues. Brief Analysis New polling data provides a window into popular Saudi views of the Abraham Accords and other foreign policy concerns facing the kingdom. midst American and Israeli press reports—and official Saudi denials—of Prime Minister Binyamin A Netanyahu’s recent meeting with Crown Prince Muhammad bin Salman in Neom, Saudi Arabia, a reliable new public opinion poll commissioned by The Washington Institute shows that the Saudi public is divided but increasingly open to contacts with Israel. (This corrected version of a November 25 report is based on revised data received from the pollster, after remedying a technical error.) 41% Back UAE/Bahrain Peace with Israel; 37% Back Personal Contacts Asked about September’s peace agreements between Israel and the two Saudi neighbors, the UAE and Bahrain, 41% of the Saudi public call the agreements a “positive development.” A narrow majority (54%), however, label the agreements as negative. The detailed responses are as follows: very positive, 12%; somewhat positive, 29%; somewhat negative, 30%; very negative, 24%; haven’t heard or read enough to say, 1%; don’t know, 2%; no answer, 1%. A plurality of Saudis (37%) also agree, either "somewhat" or "strongly," that “people who want to have business or sports contacts with Israelis should be allowed to do so.” This is quadruple the proportion who agreed with this statement in the previous survey in June 2020, The rapid growth demonstrates that popular attitudes on this supposedly sensitive point are actually quite fluid, probably responding both to new events and official guidance. -

FARA Second Semi-Annual Report

U.S. Department of Justice Washington, D.C. 20530 Report of the Attorney General to the Congress of the United States on the Administration of the Foreign Agents Registration Act of 1938, as amended, for the six months ending December 31, 2018 Report of the Attorney General to the Congress of the United States on the Administration of the Foreign Agents Registration Act of 1938, as amended, for the six months ending December 31, 2018 TABLE OF CONTENTS INTRODUCTION ................................................... 1-1 AFGHANISTAN......................................................1 ALBANIA..........................................................2 ALGERIA..........................................................3 ANGOLA...........................................................4 ANTIGUA & BARBUDA................................................5 ARGENTINA........................................................6 ARMENIA..........................................................7 ARUBA............................................................8 AUSTRALIA........................................................9 AUSTRIA..........................................................11 AZERBAIJAN.......................................................12 BAHAMAS..........................................................14 BAHRAIN..........................................................15 BANGLADESH.......................................................17 BARBADOS.........................................................19 BELGIUM..........................................................20 -

The Red Sea Project

A KEY PART OF A VIBRANT SOCIETY - Strong roots - Fulfilling lives - Strong foundations A THRIVING ECONOMY - Rewarding opportunities - Open for business - Investing for the long term - Leveraging its unique position AN AMBITIOUS NATION - Effectively governed - Responsibly enabled 2 4 3 The Red Sea project The Red Sea Project will be a luxury resort destination that will be developed across a group of natural islands and steeped in nature and culture. It will set new standards for sustainable development and bring about the next generation of luxury travel, putting Saudi Arabia on the international tourism map. 6 5 Location and resources The Red Sea Project is located along the western coast of the Kingdom of Saudi Arabia, between the cities of Umluj and Al Wajh. Envisioned as an exquisite luxury resort destination built on 50 unspoiled natural islands that stretch along 200 kilometers of stunning coastline, the Red Sea Project will be situated on the site of one of the world’s hidden natural treasures. The islands form an archipelago that is home to environmentally protected coral reefs, mangroves, and several endangered marine species, including the hawksbill, a slender sea turtle. It also boasts dormant volcanoes; the most recently active has a recorded history of activity that dates back to the 17th century AD. In addition, the Red Sea Project’s nature preserve is inhabited by rare wildlife, including Arabian leopards, Arabian wolves, Arabian wildcats, and falcons. 8 7 Mada’in Saleh Tourists will also be able to visit the ancient ruins at Mada’in Saleh. The ruins date back thousands of years and are renowned for their beauty and historical significance. -

Nationals of Bahrain, Kuwait, Oman, Saudi Arabia and U

International Civil Aviation Organization STATUS OF AIRPORTS OPERABILITY AND RESTRICTION INFORMATION - MID REGION Updated on 26 September 2021 Disclaimer This Brief for information purposes only and should not be used as a replacement for airline dispatch and planning tools. All operational stakeholders are requested to consult the most up-to-date AIS publications. The sources of this Brief are the NOTAMs issued by MID States explicitly including COVID-19 related information, States CAA websites and IATA travel center (COVID-19) website. STATE STATUS / RESTRICTION 1. Passengers are not allowed to enter. - This does not apply to: - nationals of Bahrain, Kuwait, Oman, Saudi Arabia and United Arab Emirates; - passengers with a residence permit issued by Bahrain; - passengers with an e-visa obtained before departure; - passengers who can obtain a visa on arrival; - military personnel. 2. Passengers are not allowed to enter if in the past 14 days they have been in or transited through Bangladesh, Bosnia and Herzegovina, Costa Rica, Ecuador, Ethiopia, Georgia, Indonesia, Iran, Iraq, Malawi, Malaysia, Mexico, Mongolia, Mozambique, Myanmar, Namibia, Nepal, Philippines, Slovenia, South Africa, Sri Lanka, Tunisia, Uganda, Ukraine, Viet Nam or Zimbabwe. - This does not apply to: - nationals of Bahrain; - passengers with a residence permit issued by Bahrain. BAHRAIN 3. Passengers must have a negative COVID-19 PCR test taken at most 72 hours before departure. The test result must have a QR code if arriving from Bangladesh, Bosnia and Herzegovina, Costa Rica, Ecuador, Ethiopia, Georgia, Indonesia, Iran, Iraq, Malawi, Malaysia, Mexico, Mongolia, Mozambique, Myanmar, Namibia, Nepal, Philippines, Slovenia, South Africa, Sri Lanka, Tunisia, Uganda, Ukraine, Viet Nam or Zimbabwe. -

Data Insightsinsight 09/27/2018

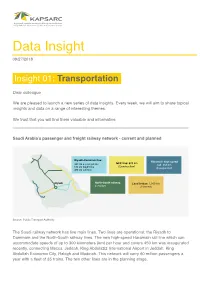

DataData InsightsInsight 09/27/2018 Insight09/27/2018 01: Transportation Dear colleague We are pleased to launch a new series of data insights. Every week, we will aim to share topical insights and data on a range of interesting themes. We trust that you will find them valuable and informative. Saudi Arabia’s passenger and freight railway network - current and planned Riyadh-Dammam line: Haramain high speed GCC line: 28 km 449 km passenger line rail: 450 km (onstruction) 54 km freight line (Inaugurated) 400 km su-lines Riyadh North-South railway: Land bridge: 1,30 km 2,750 km (Planned) Source: Public Transport Authority The Saudi railway network has five main lines. Two lines are operational: the Riyadh to Dammam and the North-South railway lines. The new high-speed Haramain rail line which can accommodate speeds of up to 300 kilometers (km) per hour and covers 450 km was inaugurated recently, connecting Mecca, Jeddah, King Abdulaziz International Airport in Jeddah, King Abdullah Economic City, Rabigh and Madinah. This network will carry 60 million passengers a year with a fleet of 35 trains. The two other lines are in the planning stage. The existing North-South Railway project is one of the largest railway projects, covering more than 2,750 kilometers of track. It connects Riyadh and the northern border through the cities of Al-Qassim and Hail. The Riyadh to Dammam line was the first operational line: • The freight line opened in the 1950s, connecting King Abdulaziz Port in Dammam with Riyadh, through Al-Ahsa, Abqaiq, Al-Kharj, Haradh, and Al-Tawdhihiyah. -

Volume 2138, A-20378 the Government of the Kingdom Of

Volume 2138, A-20378 [TRANSLATION -- TRADUCTION] The Government of the Kingdom of Spain has examined the reservation made by the Government of the Kingdom of Saudi Arabia to the Convention on the Elimination of All Forms of Discrimination against Women on [7] September 2000, regarding any interpreta- tion of the Convention that may be incompatible with the norms of Islamic law and regard- ing article 9, paragraph 2. The Government of the Kingdom of Spain considers that the general reference to Is- lamic law, without specifying its content, creates doubts among the other States parties about the extent to which the Kingdom of Saudi Arabia commits itself to fulfil its obliga- tions under the Convention. The Government of the Kingdom of Spain is of the view that such a reservation by the Government of the Kingdom of Saudi Arabia is incompatible with the object and purpose of the Convention, since it refers to the Convention as a whole and seriously restricts or even excludes its application on a basis as ill-defined as the general reference to Islamic law. Furthermore, the reservation to article 9, paragraph 2, aims at excluding one of the ob- ligations concerning non- discrimination, which is the ultimate goal of the Convention. The Government of the Kingdom of Spain recalls that according to article 28, para- graph 2, of the Convention, reservations that are incompatible with the object and purpose of the Convention shall not be permitted. Therefore, the Government of the Kingdom of Spain objects to the said reservations by the Government of the Kingdom of Saudi Arabia to the Convention on the Elimination of All Forms of Discrimination against Women. -

Agreement 22 February 1958

page 1| Delimitation Treaties Infobase | accessed on 13/03/2002 Bahrain-Saudi Arabia boundary agreement 22 February 1958 Whereas the regional waters between the Kingdom of Saudi Arabia and the Government of Bahrain meet together in many places overlooked by their respective coasts, And in view of the royal proclamation issued by the Kingdom of Saudi Arabia on the 1st Sha'aban in the year 1368 (corresponding to 28 May 1949) and the ordinance issued by the Government of Bahrain on 5 June 1949 about the exploitation of the sea-bed, And in view of the necessity for an agreement to define the underwater areas belonging to both countries, And in view of the spirit of affection and mutual friendship and the desire of H.M. the King of Saudi Arabia to extend every possible assistance to the Government of Bahrain, The following agreement has been made: First clause 1. The boundary line between the Kingdom of Saudi Arabia and the Bahrain Government will begin, on the basis of the middle line from point 1, which is situated at the mid-point of the line running between the tip of the Ras al Bar (A) at the southern extremity of Bahrain and Ras Muharra (B) on the coast of the Kingdom of Saudi Arabia. 2. Then the above-mentioned middle line will extend from point 1 to point 2 situated at the mid-point of the line running between point A and the northern tip of the island of Zakhnuniya (C). 3. Then the line will extend from point 2 to point 3 situated at the mid-point of the line running between point A and the tip of Ras Saiya (D).