Summary Translation of Question & Answer Session at FY

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fujitsu Data Book 2008.10

History of Fujitsu ●Business Developments● ●Product Development● Jun 20, 1935 1935 ~ ◦Fuji Tsushinki Manufacturing Corporation, the company that later becomes Fujitsu Limited, is born as an Aug 1937 offshoot of the communications division ◦Fuji Tsushinki Manufacturing Corporation becomes Japanese Ministry of Fuji Electric. The new company is of Telecommunications-designated company for production of carrier capitalized at ¥3 million and has 700 equipment. employees. The first president was ◦Delivery of first carrier equipment order to South Manchuria Railways Manjiro Yoshimura, then president of Co. Fuji Electric. 1940 Sep 1938 ◦Delivery of the first Japanese-made T-type automatic telephone ◦Groundbreaking begins for construction of a new plant switchboard to the Nara Telephone Exchange. in Nakahara Ward, Kawasaki City, on the site of the present Kawasaki Research & Manufacturing Facilities. Dec 1945 ◦Fuji Tsushinki is granted government recognition by Japanese Ministry of Telecommunications as an officially approved telephone developer and manufacturer. May 1951 ◦Production of electronic computing machines begins. Apr 1942 ◦Suzaka Plant opens for mass production of telephones. Aug 1953 ◦Manufacture of radio communications equipment begins (Kawasaki Nov 1944 Plant). ◦Kanaiwa Kousakusho Co., Ltd. (now Fujitsu Frontech Limited) becomes part of the Fujitsu Group. Apr 1954 ◦Production of electronic devices begins (Kawasaki Plant). May 1949 ◦Stock is listed on the newly reopened Tokyo Stock Oct 1954 Exchange. ◦Japan’s first relay-type, automated electronic computer, the FACOM 100, is completed. Jun 1957 ◦Shinko Electric Industries Co., Ltd. becomes part of the Dec 1956 Fujitsu Group. ◦Japan's first NC is completed. Nov 1959 Sep 1958 ◦Oyama Plant opens for mass production of radio ◦First FACOM200 parametron computer is completed. -

Fujitsu to Split Off HDD Business in Reorganization

Fujitsu Limited Fujitsu to Split Off HDD Business in Reorganization Tokyo, May 21, 2009 – Fujitsu Limited (“Fujitsu”) today announced that it will split off its hard disk drive business (“HDD business”) and merge the business into its wholly owned subsidiary, Toshiba Storage Device Corporation (“Toshiba Storage Device”), through a simple absorption-type separation, on July 1, 2009. In a transaction scheduled for July 1, 2009, Fujitsu will then sell 80.1 percent of its shares of Toshiba Storage Device to Toshiba Corporation (“Toshiba”). By the end of December 2010, Fujitsu plans to sell its remaining 19.9 percent to Toshiba, at which point Toshiba Storage Device will become a wholly owned subsidiary of Toshiba. 1. Objectives of the Corporate Split On April 30, 2009, Fujitsu Limited signed a definitive agreement with Toshiba to transfer ownership of its HDD business. This corporate split is part of the implementation of the ownership transfer. 2. Outline of the Corporate Split (1) Schedule May 21, 2009 Signing of corporate split contract July 1, 2009 (scheduled) Effective date of corporate split This corporate split, pursuant to Article 784 (3) of the Corporate Law, will be executed without the requirement of the approval of a General Meeting of the Shareholders as stipulated under Article 783 (1) of the Corporate Law (Simple Absorption-type Separations). (2) Method Fujitsu will be the transferor company and Toshiba Storage Device will be the successor company (Simple Separation). (3) Decrease in Capital or Other, Resulting from the Corporate Split There will be no decrease in capital or other, resulting from the corporate split. -

Enhancing System Solutions

Enhancing System Solutions FUJITSU MICROELECTRONICS EUROPE Enhancing System Solutions Services Automotive Multimedia Mobile Communications Networking/Telecoms Here at Fujitsu Microelectronics Europe (FME) we are engaged in an on-going program of responding to the changing nature of the “European market. We provide state-of-the-art semiconductor devices and leading-technology plasma and liquid crystal display panels. But, more than that, we endeavor to develop systems solutions in partnership with our customers while at the same time, we try to broaden the scope of our operation and genuinely add value wherever possible. The global perspective Fujitsu is a world leader in customer-oriented IT and communications solutions concentrated on three areas: software & services, hardware platforms and electronic devices. Our global goal is to focus on customer needs, quality, timeliness and management speed. 25 years of experience in Europe Over the past 25 years we have established ourselves in the major European markets of Automotive, Networking/Telecoms, Mobile Communications, Multimedia and Industrial & Home appliances through a special blend of technical experience and applied expertise. What’s more, FME continues to drive technologies forward to meet the ever-increasing demands of tomorrow's applications – in which Europe leads the world! ” Shimpei Hirata President Fujitsu Microelectronics Europe GmbH Dreieich-Buchschlag / Frankfurt / Germany 2 Industrial & Home Appliances Flat Panel Displays Quality Environment Local Support European Offices Enhancing System Solutions ujitsu’s traditional corporate strengths, in markets ranging from together with re-use of intellectual property and a company-wide Finformation technology to telecommunications and from displays system solution focus, benefits the fastest-growing sectors of the to semiconductors, have helped it become one of the world’s leading information age. -

PDF Download [1

Annual Report 2002 TOKYO ELECTRON Profile Established in 1963, Tokyo Electron (TEL) is a world-leading supplier of semiconductor production equipment (SPE) and related services for the semiconductor industry. The Company develops, manufactures and markets a broad lineup of products, including oxidation/diffusion/LP-CVD systems, single wafer CVD and PVD systems, coater/developers, spin-on dielectric (SOD) coaters, etch systems, cleaning systems, wafer probers, and others. Tokyo Electron also uses its accumulated expertise in SPE to develop, manufacture and market coater/developers and etch/ash systems for the manufacture of Flat Panel Display (FPD). Most of the Company’s semiconductor and FPD production systems hold the leading share in their respective markets. Tokyo Electron also maintains a strong presence as a distributor, providing a wide array of semiconductor production systems, storage Disclaimer regarding area network and Internet related products for broadband solutions, and Forward-looking Statements electronic components in Japan from other leading suppliers. With a Matters discussed in this annual report, including network spanning 16 countries on three continents, Tokyo Electron forecasts of future business performance of Tokyo Electron, management strategies, beliefs provides superior products and services to its customers, and superior and other statements are based on the returns to its shareholders. Company’s assumption in light of information that is currently available. These forward-looking statements involve known -

Coolplug Coolinkhub HVAC Bridge Quick Installation Guide

CoolPlug CooLinkHub HVAC Bridge Quick Installation Guide Warning Read and understand the following Safety Guidelines and Warnings to ensure a safe installation Failure to follow WARNING may result in injury or death. This equipment is to be installed by accredited Install the equipment only in a restricted access electrician or similar technical personnel, as per location. these installation instructions. When wall mounting, be sure to fix firmly on a stable Read the installation instructions before connecting surface and in accordance to the instructions below. the system to the power source. When DIN rail mount fix the devices properly to All electrical work must be performed by a licensed the DIN rail following the instructions below. technician, according to local regulations. When mounting on DIN rail inside a metallic cabinet Ultimate disposal of this product should be handled be sure to properly connected to earth. according to all national laws and regulations. Unplug power when connecting the wires. Installation of the equipment must comply with local Pay attention to the polarity of power and and national electrical legislation for installation of communication cables when connecting them electric equipment. Disconnect power of any bus or communication Do not install the devices outdoors or exposed to cable before connecting the system direct solar radiation, water, high relative humidity or dust. 3 Caution Failure to follow CAUTION may result in serious injury, DO NOT INSTALL COOLINKHUB or COOLPLUG property damage or in some circumstances, even IN THE FOLLOWING LOCATIONS: death. a) Where mineral oil mist or oil spray or vapor is Do not allow children to play with the CoolPlug or produced, for example, in a kitchen. -

Fujitsu/ Panasonic/ Dbj/ Jv

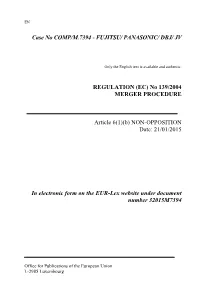

EN Case No COMP/M.7394 - FUJITSU/ PANASONIC/ DBJ/ JV Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 21/01/2015 In electronic form on the EUR-Lex website under document number 32015M7394 Office for Publications of the European Union L-2985 Luxembourg EUROPEAN COMMISSION Brussels, 21.01.2015 C(2015) 333 final PUBLIC VERSION SIMPLIFIED MERGER PROCEDURE To the notifying parties Dear Madam and Sir, Subject: Case M.7394 – FUJITSU / PANASONIC / DBJ / JV Commission decision pursuant to Article 6(1)(b) of Council Regulation (EC) 1 No 139/2004 and Article 57 of the Agreement on the European Economic Area2 1. On 17 December 2014, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Fujitsu Limited (“Fujitsu”, Japan), Panasonic Corporation (“Panasonic”, Japan) and Development Bank of Japan Inc. (“DBJ”, Japan) acquire within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation joint control of a newly created joint venture (“NewCo”, Japan), by way of contribution of assets.3 1 OJ L 24, 29.1.2004, p. 1 ("the Merger Regulation"). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ("TFEU") has introduced certain changes, such as the replacement of "Community" by "Union" and "common market" by "internal market". The terminology of the TFEU will be used throughout this decision. 2 OJ L 1, 3.1.1994, p.3 ("the EEA Agreement"). 3 Publication in the Official Journal of the European Union No C 465, 24.12.2014, p. -

What's So Great About Fujitsu and PRIMERGY?

Fact Sheet What’s so great about Fujitsu and PRIMERGY Fact Sheet What’s so great about Fujitsu and PRIMERGY? What’s so great about Fujitsu and PRIMERGY? realizing high-speed interconnections are Fujitsu America Inc., a wholly owned subsidiary achievements that will set Fujitsu apart of Fujitsu Limited, the third largest IT Company from competitors. in the world, is pleased to present this overview of our PRIMERGY® server. Customers have found PRIMERGY Servers to be a superior investment. With the Fujitsu mainframe Fujitsu has been in the x86 server market since heritage, they are designed to be the solution 1995 as part of a joint venture with Siemens® for enterprise computing environments. through the creation of the Fujitsu-Siemens PRIMERGY Servers will play a significant Computers partnership. The joint venture role in meeting business objectives with: company played a particularly important role as a product development base for x86 servers. ■ Industry-leading Reliability - Fujitsu The decision to fully consolidate Fujitsu PRIMERGY servers integrate Japanese Siemens Computers and unify PRIMERGY server innovation with German engineering. Our development under the successor company, PRIMERGY servers have an average mean Fujitsu Technology Solutions, accelerates time between failures (MTBF) of over 6 product development and enables us to years and a life expectancy of over 10 years. provide globally standardized products. Fujitsu ■ Cool-safe® Technology - Fujitsu PRIMERGY made the investment to buy Siemens half of servers use an average of 20% less power the joint venture as of April 1, 2009. than our competitor’s servers of a similar model. In fact, the PRIMERGY TX120 Drawing on the long Fujitsu heritage and model cuts energy costs in half over experience of designing rock-solid mainframe standard servers. -

Convocation Notice of the 100Th Ordinary General Meeting of Shareholders

This document has been translated from a part of the Japanese original for reference purposes only. In the event of any discrepancy between this translated document and the Japanese original, the original shall prevail. Fujitsu General Limited assumes no responsibility for this translation or for direct, indirect or any other forms of damages arising from the translations. Securities code: 6755 May 31, 2019 To Our Shareholders: Etsuro Saito President & Representative Director Fujitsu General Limited 3-3-17, Suenaga, Takatsu-ku, Kawasaki, Japan CONVOCATION NOTICE OF THE 100TH ORDINARY GENERAL MEETING OF SHAREHOLDERS You are cordially invited to attend the 100th Ordinary General Meeting of Shareholders (the “Meeting”) of Fujitsu General Limited (the “Company”) to be held as indicated below. If you are unable to attend the Meeting, you may exercise your voting rights either in writing or via the Internet. Please review the attached “Reference Materials for the General Meeting of Shareholders” and exercise your voting rights no later than 5:00 p.m., Thursday, June 20, 2019 (Japan Standard Time), in accordance with the guidance on the following pages. Thank you very much for your cooperation. 1. Date and Time: June 21, 2019(Friday) at 10:00 a.m. 2. Place: 3-3-17, Suenaga, Takatsu-ku, Kawasaki, Japan Hall, sixth floor, research laboratory building, the Company headquarters 3. Meeting Agenda: Matters to be reported: 1. The Business Report and the Consolidated Financial Statements for the 100th Fiscal Year (April 1, 2018 to March 31, 2019), and the results of audits of the Consolidated Financial Statements by the Accounting Auditor and the Audit & Supervisory Board 2. -

Initiatives for AI Ethics: Formulation of Fujitsu Group AI Commitment

Initiatives for AI Ethics: Formulation of Fujitsu Group AI Commitment Tsuneo Nakata Tatsuki Araki Satoshi Tsuchiya Yuri Nakao Aisha Naseer Junichi Arahori Takahiko Yamamoto While AI technology provides significant benefits, downsides of AI have also been reported, including AI that uses biased data for learning makes unfair decisions. To prevent further ad- vancements in the technology from causing serious side effects, AI ethics are being discussed and many organizations and companies have recently announced new guidelines regarding AI. When Fujitsu released FUJITSU Human Centric AI Zinrai in 2015, we proposed “collabora- tive, human centric AI” and have paid attention to the ethical aspects of AI. In March 2019, we announced the Fujitsu Group AI Commitment that expresses our approach to AI ethics in a concrete and easy-to-understand manner based on the results of over 30 years of R&D and so- cial implementation of AI. The promises of the Fujitsu Group AI Commitment were formulated in cooperation with AI4People, Europe’s expert forum, and are in accordance with the AI eth- ics principles that the forum advocates. They are Fujitsu’s message to its major stakeholders, including customers, people, society, shareholders, and employees. This paper presents the social trends related to AI ethics and describes the basic concept of Fujitsu’s AI Commitment. 1. Introduction the ethical aspects of AI. Furthermore, in March 2019, Progress in AI technologies has led to the develop- we announced the “Fujitsu Group AI Commitment,”1) ment of new methods for prediction and optimization which summarizes Fujitsu’s AI ethics promises based on based on the use of massive amounts of data and has its more than 30 years of experience in R&D and social brought about major benefits to human society. -

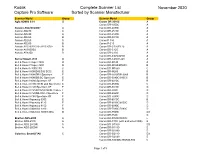

Kodak Capture Pro Software Complete Scanner List Sorted By

Kodak Complete Scanner List November 2020 Capture Pro Software Sorted by Scanner Manufacturer Scanner Model Group Scanner Model Group Agfa ADMIS S 61 G Canon DR-2010C A Canon DR-2050C A Avision AV220C2/D2+ A Canon DR-2080C A Avision AD230 A Canon DR-2510C A Avision AD240 A Canon DR-2580C A Avision AD250 B Canon DR-3010C A Avision AD260 A Canon P-150 A Avision AD280 B Canon P-215 A Avision AV320/AV320+/AV320D2+ B Canon DR-C120/F120 A Avision AV3850SU B Canon DR-C125 A Avision AV8350 D Canon DR-C130 A Canon DR-C225/225W A Bell & Howell 2138 D Canon DR-C230/C240 A Bell & Howell Truper 3200 D Canon DR-M140 A Bell & Howell Truper 3600 D Canon DR-M160/M160II B Bell & Howell 730DC FB C Canon DR-M1060 C Bell & Howell 8080D-B/S-B SCSI E Canon DR-M260 B Bell & Howell 8080DB-I Spectrum E Canon DR-3020/DR-3060 B Bell & Howell 8080SB/SC Spectrum E Canon DR-3080C/380CII B Bell & Howell 8090 Spectrum XF E Canon DR-4010C B Bell & Howell 8100 (SCSI and Spectrum) E Canon DR-4580U C Bell & Howell 8120 Spectrum XF F Canon DR-5010C D Bell & Howell 8125S/8125D SCSI / Video F Canon DR-5020 D Bell & Howell 8125DB-I/DC-I Spectrum F Canon DR-5060F D Bell & Howell 8140 Spectrum XF F Canon DR-5080C D Bell & Howell Ngenuity 9090 E Canon DR-6010C B Bell & Howell Ngenuity 9125 E Canon DR-6030C/6050C D Bell & Howell Ngenuity 9150 F Canon DR-6080C D Bell & Howell SideKick 1200 B Canon DR-7080C/7090C D Bell & Howell SideKick 1400/1400u B Canon DR-7550C DX Canon DR-7580 D Brother ADS-2000 A Canon DR-9050C/9080C E Brother ADS-2100 A Canon DR-X10C (with and w/out VRS) E Brother -

SUMITOMO ELECTRIC Annual Report 2009 the Ever-Evolving Principles

Annual Report 2009 Year Ended March 31, 2009 TM Each company of the Sumitomo Electric Group combines its unsurpassed creativity with knowledge and experience to generate dynamics that allow the Group to contribute to society. April 2008 Business Activities Launched Full-scale Local Production of Optical Devices and Transceivers in Suzhou, China Sumitomo Electric Photo-Electronics Components (Suzhou), Ltd. started the integrated production of optical device manufacturing and optical transceiver assembly in Suzhou, China. This integrated production system enabled us to reinforce our supply systems to the global market by successfully reducing production lead times and greatly improving production efficiency. July 2008 New Products & Technologies Developed Technique for Analyzing Red Phosphorus Content in Resins Sumitomo Electric has succeeded in developing the June 2008 New Products & Technologies world’s first method never before possible for Completed Prototype of the World’s measuring red phosphorus content in resins. We First Superconducting Electric Car anticipate the method’s applications to wide areas ranging from material development for resin products To verify the suitability of high-temperature superconducting technology to quality control and incoming inspections. used for electric cars, as well as to widely appeal to industrial sectors and society to adopt the technology, we have produced a superconducting electric car on a trial basis. The car runs on a motor incorporating Sumitomo Electric’s high-temperature September 2008 -

Vendor Product Name Type OS Version Fujitsu ARROWS Ef FJL21

Vendor Product Name Type OS version Fujitsu ARROWS ef FJL21 Smartphone Android 4.0.4 Fujitsu ARROWS X F-02E Smartphone Android 4.1.2 Fujitsu ARROWS NX F-06E Smartphone Android 4.2.2 Fujitsu Disney Mobile on docomo F-07E Smartphone Android 4.2.2 Google Google Nexus 4 LG-E960 Smartphone Android 4.2.1 Android 4.1.1 Google Google Nexus 7 Tablet Android 4.2.1 Android 4.2.2 HTC HTC One X S7200 Smartphone Android 4.0.3 HTC HTC J butterfly HTL21 Smartphone Android 4.1.1 HTC HTC J One HTL22 Smartphone Android 4.1.2 iida(HTC) INFOBAR A02 Smartphone Android 4.1.1 KYOCERA DIGNO S KYL21 Smartphone Android 4.0.4 KYOCERA URBANO L01 Smartphone Android 4.2.2 LG Optimus G LGL21 Smartphone Android 4.0.4 LG Optimus G Pro L-04E Smartphone Android 4.1.2 LG Optimus it L-05E Smartphone Android 4.2.2 Motorola Droid RAZR MAXX HD Smartphone Android 4.1.2 NEC MEDIAS X N-06E Smartphone Android 4.2.2 Panasonic ELUGA X P-02E Smartphone Android 4.1.2 Panasonic ELUGA P P-03E Smartphone Android 4.2.2 PANTECH VEGA PTL21 Smartphone Android 4.1.2 SAMSUNG Galaxy S3 GT-I9300 Smartphone Android 4.0.4 SAMSUNG Galaxy Nexus GT-I9250 Smartphone Android 4.0.1 SAMSUNG Galaxy S4 GT-I9505 Smartphone Android 4.2.2 SAMSUNG GALAXY SII WiMAX ISW11SC Smartphone Android 4.0.4 SAMSUNG GALAXY S II LTE SC-03D Smartphone Android 4.0.4 SAMSUNG GALAXY NEXUS SC-04D Smartphone Android 4.1.1 SAMSUNG GALAXY Note SC-05D Smartphone Android 4.0.4 SAMSUNG GALAXY S4 SC-04E Smartphone Android 4.2.2 SHARP ISW16SH Smartphone Android 4.0 (Aquos Phone Series) SHARP AQUOS PHONE SERIE SHL22 Smartphone Android