Policy Paper No. 4: Economic Relations and Trade – Mapping EU

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Audited Annual Report 2012 Nordea 1, SICAV Socie´Te´ D’Investissement A` Capital Variable A` Compartiments Multiples

Audited Annual Report 2012 Nordea 1, SICAV Socie´te´ d’Investissement a` Capital Variable a` compartiments multiples Investment Fund under Luxembourg Law 562, rue de Neudorf L-2220 Luxembourg Grand Duchy of Luxembourg R.C.S. number: Luxembourg B-31442 No subscriptions can be received on the basis of these fi nancial reports. Subscriptions are only valid if made on the basis of the current prospectus accompanied by the latest annual report and the most recent semi-annual report, if published thereafter. Table of Contents Report of the Board of Directors 2 Report of the Investment Manager 3 Report of the Réviseur d’Entreprises agréé 4 Statement of Net Assets as of 31/12/2012 6 Statement of Operations and Changes in Net Assets for the year ended 31/12/2012 16 Statement of Statistics as at 31/12/2012 34 Statement of Investments in Securities and Other Net Assets as of 31/12/2012 Nordea 1 - African Equity Fund 44 Nordea 1 - Brazilian Equity Fund 46 Nordea 1 - Climate and Environment Equity Fund 47 Nordea 1 - Danish Bond Fund 48 Nordea 1 - Danish Kroner Reserve 49 Nordea 1 - Danish Mortgage Bond Fund 50 Nordea 1 - Emerging Consumer Fund 51 Nordea 1 - Emerging Market Blend Bond Fund 52 Nordea 1 - Emerging Market Bond Fund 55 Nordea 1 - Emerging Market Corporate Bond Fund 59 Nordea 1 - Emerging Market Local Debt Fund 62 Nordea 1 - Emerging Markets Focus Equity Fund 64 Nordea 1 - Emerging Stars Equity Fund 66 Nordea 1 - Euro Bank Debt Fund 68 Nordea 1 - Euro Diversifi ed Corporate Bond Fund 69 Nordea 1 - European Alpha Fund 72 Nordea 1 - European -

Interim Report Q2 2011 11082011En

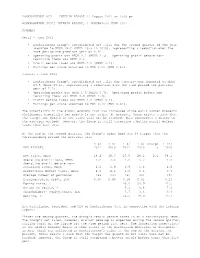

HONKARAKENNE OYJ INTERIM REPORT 11 August 2011 at 3:00 pm HONKARAKENNE OYJ’S INTERIM REPORT, 1 JANUARY–30 JUNE 2011 SUMMARY April - June 2011 • Honkarakenne Group’s consolidated net sales for the second quarter of the year amounted to MEUR 18.2 (MEUR 19.6 in 2010), representing a reduction over the same period the previous year of 6.9%. • Operating profit was MEUR 2.2 (MEUR 2.5). Operating profit before non- recurring items was MEUR 2.2. • Profit before taxes was MEUR 2.0 (MEUR 2.1). • Earnings per share amounted to EUR 0.30 (EUR 0.45). January - June 2011 • Honkarakenne Group’s consolidated net sales for January-June amounted to MEUR 27.5 (MEUR 28.1), representing a reduction over the same period the previous year of 2.2%. • Operating profit was MEUR 1.0 (MEUR 0.7). Operating profit before non- recurring items was MEUR 0.8 (MEUR 1.4). • Profit before taxes was MEUR 1.0 (MEUR 0.1). • Earnings per share amounted to EUR 0.18 (EUR 0.01). The uncertainty in the global economy that has increased since early summer presents challenges, especially for growth in net sales. At present, there exists a risk that the target for growth in net sales will not be reached. This represents a change to the previous outlook. However, the Group is still targeting a better result before taxes than last year. At the end of the second quarter, the Group’s order book was 3% larger than the corresponding period the previous year. 4-6/ 4-6/ 1-6/ 1-6/ Change 1-12/ KEY FIGURES 2011 2010 2011 2010 % 2010 Net sales, MEUR 18.2 19.6 27.5 28.1 2.2 58.1 Operating profit/loss, -

Honkarakenne Oyj Board of Directors’ Report and Financial Statements 2018 Honkarakenne Board of Directors’ Report and Financial Statements 2018

HONKARAKENNE OYJ BOARD OF DIRECTORS’ REPORT AND FINANCIAL STATEMENTS 2018 HONKARAKENNE BOARD OF DIRECTORS’ REPORT AND FINANCIAL STATEMENTS 2018 Index BOARD OF DIRECTORS’ REPORT 1.1.–31.12.2018 3 CONSOLIDATED FINANCIAL STATEMENTS (IFRS) Consolidated Statement of Comprehensive Income (IFRS) 12 Consolidated Balance Sheet (IFRS) 13 Consolidated Statement of Cash Flows (IFRS) 14 Consolidated Statement of Changes In Equity 15 Accounting policies used in the consolidated financial statements (IFRS) 16 Notes to Consolidated Financial Statements 26 OTHER INFORMATION 49 PARENT COMPANY FINANCIAL STATEMENTS (FAS) Parent company income statement (FAS) 55 Parent company balance sheet (FAS) 55 Parent company cash flow statement 58 Accounting principles of the parent company 59 Notes to the financial statements of the parent company 60 DIVIDEND PROPOSAL 69 SIGNATURES FOR THE FINANCIAL STATEMENTS AND BOARD OF DIRECTORS’ REPORT 69 AUDITOR’S REPORT 70 CORPORATE GOVERNANCE STATEMENT 2018 72 2 Directors’ Report, 1 January to 31 December 2018 The Honkarakenne Group’s consolidated net sales totalled MEUR 48.9 (MEUR 43.4 in 2017, MEUR 36.1 in 2016). The Group posted an operating profit of MEUR 1.6 (MEUR 1.7; MEUR -0.8). Profit before taxes was MEUR 1.5 (MEUR 1.7; MEUR -1.2), and earnings per share were EUR 0.20 (EUR 0.15; EUR -0.29). The Board of Directors will propose to the General Meeting that no dividends be paid for the financial year now ended. BUSINESS REVIEW The Group’s net sales rose by 13 per cent on 2017.This growth stemmed from net sales in Global Markets and demand In Finland, there were positive developments in net sales with year-on-year growth of 20 per cent. -

Baltic Rim Economies – a List of Writers

Baltic Rim Economies – a list of writers The following expert articles have been published in the previous reviews: Review Author(s) Position Title of article 1/2021 Krista Mikkonen Minister of the Environment and Climate State of the Baltic Sea is a Change, priority to the Finnish Ministry of the Environment, government Finland 1/2021 Minna Arve Mayor, Sustainability as the policy City of Turku, framework Finland 1/2021 Brita Bohman Senior Lecturer in Environmental Law, Updating the Baltic Sea Action Department of Law, Stockholm University, Plan Sweden 1/2021 Anna Törnroos Assistant Professor (tenure track), The Decade for oceans and Faculty of Science and Engineering, Åbo humanity Akademi University, Finland 1/2021 Mati Kahru Ph.D., Researcher, The changing Baltic Sea Scripps Institution of Oceanography, University of California, San Diego, USA 1/2021 Karoliina A. Koho Dr., Project Officer, Towards a “green” future of the BONUS Secretariat (EEIG), Baltic Sea Helsinki, Finland 1/2021 Maciej Zalewski European Regional Centre For Ecohydrology Green Deal – Ecohydrological PAS, nature-based solutions for UNESCO Chair on Ecohydrology and improvement of Baltic ecological Applied Ecology, status Łódź, Poland 1/2021 Aija Caune Chairperson, Hope, stability and protection Coalition Clean Baltic Mikhail Durkin Executive Secretary, Coalition Clean Baltic Nils Höglund Fisheries Policy Officer, Coalition Clean Baltic 1 1/2021 Hannu Klemola Areal Manager, Vulnerable sea needs voluntary Finnish Association for Nature Conservation work to support common -

422263.Pdf (1.056Mb)

ORGANISATIONAL LEARNING AND KNOWLEDGE ACQUISITION A case study of internationalising manufacturers of wood-based prefabricated buildings Master´s Thesis in International Business Author: Clemens Kraus Supervisors: D.Sc. Birgitta Sandberg M.Sc. Elina Pelto 4.11.2012 Turku Turun kauppakorkeakoulu • Turku School of Economics Table of contents 1 INTRODUCTION ................................................................................................... 9 1.1 Internationalisation opportunities and challenges for manufacturers of wood-based prefabricated buildings............................................................... 9 1.2 The role of knowledge in the internationalisation process of firms ............. 10 1.3 Definitions .................................................................................................... 12 1.4 Research gap, research question and contribution ....................................... 14 1.5 Positioning of the study ................................................................................ 16 1.6 Structure of the study ................................................................................... 18 2 THEORIES OF INTERNATIONALISATION .................................................... 19 2.1 Overview over different theories of internationalisation ............................. 19 2.2 The Uppsala Model ...................................................................................... 21 2.2.1 Explanation of the Uppsala Model and underlying assumptions..... 21 2.2.2 Criticism of the Uppsala -

Semi-Annual Report 2013 Nordea 1, SICAV Socie´Te´ D’Investissement A` Capital Variable A` Compartiments Multiples

Unaudited Semi-Annual Report 2013 Nordea 1, SICAV Socie´te´ d’Investissement a` Capital Variable a` compartiments multiples Investment Fund under Luxembourg Law 562, rue de Neudorf L-2220 Luxembourg Grand Duchy of Luxembourg R.C.S. number: Luxembourg B-31442 No subscriptions can be received on the basis of these fi nancial reports. Subscriptions are only valid if made on the basis of the current prospectus accompanied by the latest annual report and the most recent semi-annual report, if published thereafter. Table of Contents Statement of Net Assets as of 30/06/2013 2 Statement of Operations and Changes in Net Assets for the period ended 30/06/2013 12 Statement of Statistics as at 30/06/2013 30 Statement of Investments in Securities and Other Net Assets as of 30/06/2013 Nordea 1 - African Equity Fund 40 Nordea 1 - Brazilian Equity Fund 42 Nordea 1 - Climate and Environment Equity Fund 43 Nordea 1 - Danish Bond Fund 44 Nordea 1 - Danish Kroner Reserve 45 Nordea 1 - Danish Mortgage Bond Fund 46 Nordea 1 - Emerging Consumer Fund 47 Nordea 1 - Emerging Market Blend Bond Fund 48 Nordea 1 - Emerging Market Bond Fund 51 Nordea 1 - Emerging Market Corporate Bond Fund 54 Nordea 1 - Emerging Market Local Debt Fund 57 Nordea 1 - Emerging Markets Focus Equity Fund 59 Nordea 1 - Emerging Stars Equity Fund 61 Nordea 1 - Euro Bank Debt Fund 63 Nordea 1 - Euro Diversifi ed Corporate Bond Fund 64 Nordea 1 - European Corporate Bond Fund 67 Nordea 1 - European Corporate Bond Fund Plus 70 Nordea 1 - European Covered Bond Fund 73 Nordea 1 - European Cross Credit -

Rəsmi Salamlama •

Rəsmi Salamlama • Hörmətli xanımlar və cənablar, əziz dostlar! Əsası Ümummilli liderimiz Heydər Əliyev tərəfindən qoyulan tikinti–quruculuq işləri gördüyünüz kimi indi də Möhtərəm prezidentimiz İlham Əliyevin rəhbərliyi altında yeni sürət və vüsətlə davam edir. İlbəil əsas kapitala investisiya qoyuluşunda daxili mənbələrin xüsusi çəkisi və bu istiqamətdə dövlət büdcəsinin fəallığı yüksəlir. Tikinti-investisiya fəaliyyəti genişləndikcə təbii ki, layihələndirmə və memarlıq fəaliyyəti üçün də yeni imkanlar yaranmışdır. Bilavasitə ölkənin coğrafi mövqeyindən, sosial-iqtisadi səviyyəsindən, dövlətin siyasi mahiyyətindən və əhalinin milli–mənəvi sanbalından asılı olduğundan şəhərsalma sahəsində demək olar ki, hər bir ölkənin öz fərdi inkişaf yolu, inkişaf konsepsiyası olur. Bu baxımdan Azərbaycanda şəhərsalmanın tarixi, inkişaf təcrübəsi və gələcək perspektivləri öz fərdiliyi və hətta örnək obyekti olması ilə fərqləndirilə bilər. Heydər Əliyevin tikinti–quruculuq siyasətində də varisliyə sadiqliyini əməli fəaliyyətilə nümayiş etdirən cənab prezidentimiz İlham Əliyevin biləvasitə səyi nəticəsində əyalət şəhərlərimizin əksəriyyəti artıq müasir səviyyəli inzibati–mədəni mərkəzlərə çevrilmişdir. Yeni – yeni yaşayış evlərinin, inzibati binaların, idman–səhiyyə, energetika, hasilat, emal, kənd təsərrüfatı və sair təyinatlı obyektlərin inşası şəhərsalmaya yeni prizmadan ictimai–sosial baxışın nəticəsi kimi qiymətləndirilməlidir. Regionların sosial–iqtisadi inkişafı proqramlarının həyata keçirilməsi nəticəsində respublikamızda sosial və istehsalat -

Varma's Report of the Board of Directors and Financial Statements

REPORT OF THE BOARD OF DIRECTORS AND FINANCIAL STATEMENTS 2017 Contents 3 Report of the Board of Directors 2017 34 18. Loan receivables itemised by guarantee 10 Financial statements 34 19. Total pension loan receivables itemised 10 Income statement by balance sheet item 11 Balance sheet 34 20. Loans to related parties 12 Statement of source and application of funds 34 21. Derivatives 13 Notes to the financial statements 35 22. Liabilities to Group companies, other liabilities 13 Accounting principles 35 23. Technical provisions 16 Group companies 31 Dec 2017 35 24. Solvency capital 19 Notes to the income statement 35 25. Guarantees and liabilities, Parent Company 19 1. Premiums written 36 26. Capital and reserves 19 2. Claims paid 36 27. Capital and reserves after proposed profit 20 3. Breakdown of net investment return distribution 20 4. Operating expenses in the income statement 36 28. Distributable profits 20 5. Overall operating expenses by function 36 29. Guarantee capital 21 6. Personnel expenses 37 30. Guarantees and liabilities, Parent Company 21 7. Management salaries and remunerations 38 31. Guarantees and liabilities, Parent Company 21 8. Auditors' fees 39 32. Balance sheet and income statement 21 9. Income taxes at fair values 22 Notes to the balance sheet 40 Risk management 22 10. Investments at fair value and valuation 47 Key figures and analyses differences, Parent Company 47 33. Summary 23 11. Investments at fair value and valuation 47 34. Performance analysis differences, Group 48 35. Solvency 24 12. Investments in Group companies 49 36. Investment allocation at fair value and associates, Parent Company 50 37. -

IDBM Program Is to Develop and Diffuse World-Class Expertise in Global Design Business Management Through Interdisciplinary Research and Learning

Can you Can you write engineer usability? an identity? Can you Can you buy lead innovation? a culture? Can you Can you compute segment a product? fashion? Meet the Teams of the Future The International Design Business Management (IDBM) Program is a joint Business teaching and research platform of Aalto University’s schools of business, design 1/3 of students from Business Background and technology. Arising from the needs of the industry, this program gives future business man- agers, engineers and designers an opportunity to both develop systemic and Design interdisciplinary skills through specialized courses and to create tangible value 1/3 of students from Design Background for industry partners through collaborative, real-life projects. The purpose of the IDBM program is to develop and diffuse world-class expertise in global design business management through interdisciplinary research and learning. The key offering is based on a unique and innovative combination of theory and practice-based teaching methods that provide students with relevant capabilities and innovative problem solving techniques that address the needs and create solutions for the real world. The Master’s-level program aims to accelerate professional development in the global design-intensive business by emphasizing the importance of design as a competitive factor, by developing on the potential value of state-of-the-art tech- nology and by building on creating and managing industry-changing business models. IDBM is offered both as a two-year, full-time Master’s degree program or alterna- tively as a two-semester-long minor studies package. The program builds on the business, design and technology knowledge and competence achieved through previous studies, enabling students to make full use of their own potential and knowledge as members of interdisciplinary teams within project-based work. -

Honkarakenne Oyj

HONKARAKENNE OYJ BOARD OF DIRECTORS’ REPORT AND FINANCIAL STATEMENTS 2019 HONKARAKENNE BOARD OF DIRECTORS’ REPORT AND FINANCIAL STATEMENTS 2019 Index BOARD OF DIRECTORS’ REPORT 1.1.–31.12.2019 3 CONSOLIDATED FINANCIAL STATEMENTS (IFRS) Consolidated Statement of Comprehensive Income (IFRS) 12 Consolidated Balance Sheet (IFRS) 13 Consolidated Statement of Cash Flows (IFRS) 14 Consolidated Statement of Changes In Equity 15 Accounting policies used in the consolidated financial statements (IFRS) 16 Notes to Consolidated Financial Statements 28 OTHER INFORMATION 50 PARENT COMPANY FINANCIAL STATEMENTS (FAS) Parent company income statement (FAS) 60 Parent company balance sheet (FAS) 60 Parent company cash flow statement 62 Accounting principles of the parent company 63 Notes to the financial statements of the parent company 64 DIVIDEND PROPOSAL 73 SIGNATURES FOR THE FINANCIAL STATEMENTS AND BOARD OF DIRECTORS’ REPORT 73 AUDITOR’S REPORT 74 CORPORATE GOVERNANCE STATEMENT 2019 76 2 Directors’ Report, 1 January to 31 December 2019 The Honkarakenne Group’s net sales amounted to MEUR 47.5 (MEUR 48.9 in 2018, MEUR 43.4 in 2017). The Group posted an ope- rating profit of MEUR 3.4 (MEUR 1.6; MEUR 1.7). Profit before taxes was MEUR 3.2 (MEUR 1.5; MEUR 1.7), and earnings per share were EUR 0.40 (EUR 0.20; EUR 0.15). The Board of Directors proposes to the Annual General Meeting that no dividend be paid for the financial year ending 31 December 2019. In addition, the Board proposes the repayment of capital totalling EUR 0.12 per share from the fund for invested unrestricted equity. -

Honkarakenne Oyj Interim Report 11 November 2010 3:00 Pm

HONKARAKENNE OYJ INTERIM REPORT 11 NOVEMBER 2010 3:00 PM HONKARAKENNE OYJ'S INTERIM REPORT, 1 JANUARY - 30 SEPTEMBER 2010 SUMMARY July-September 2010 • Honkarakenne Group's consolidated net sales for the third quarter of the year amounted to EUR 15.0 million (EUR 12.0 million), an increase of 25% on the previous year's corresponding period • Operating profit was EUR 0.2 million (EUR –1.4 million). Operating profit without non-recurring items was EUR 0.6 million • Profit before taxes was EUR 0.1 million (EUR –1.5 million) • Earnings per share amounted to EUR 0.02 (EUR –0.41) January-September 2010 • Honkarakenne Group's consolidated net sales for January-September 2010 amounted to EUR 43.1 million (EUR 39.6 million), an increase of 9% on the previous year's corresponding period • Operating profit was EUR 0.9 million (EUR -1.8 million). Operating profit without non-recurring items was EUR 2.0 million • Profit before taxes was EUR 0.2 million • Earnings per share amounted to EUR 0.03 (EUR -0.52) The net sales of the entire year is expected to increase slightly from the level of the previous year, and the Group aims at a profitable result during the financial year. The earnings forecast has not changed from what it was before. The timing of deliveries in the last quarter of 2010 is the greatest risk to the achievement of the profit target. It is characteristic of construction work at the end of the year that orders are sometimes postponed by some weeks by customers because of weather conditions. -

Staying Power to Finnish Cultural Exports

Ministry of Education Staying Power to Finnish Cultural Exports The Cultural Exportation Project of the Ministry of Education, the Ministry for Foreign Affairs and the Ministry of Trade and Industry Publications of the Ministry of Education, Finland 2005:9 Hannele Koivunen Staying Power to Finnish Cultural Exports The Cultural Exportation Project of the Ministry of Education, the Ministry for Foreign Affairs and the Ministry of Trade and Industry Publications of the Ministry of Education, Finland 2005:9 Hannele Koivunen Opetusministeriö • Kulttuuri-, liikunta- ja nuorisopolitiikan osasto • 2005 Ministry of Education • Department for Cultural, Sport and Youth Policy • 2005 Ministry of Education Department for Cultural, Sport and Youth Policy P.O. Box 29, FI-00023 Government http://www.minedu.fi http://www.minedu.fi/minedu/publications/index.html Layout: Liisa Heikkilä, Ministry of Education ISBN 952-442-886-5 (hbk.) ISSN 1458-8110 Publications of the Ministry of Education, Finland 2005:9 Abstract Meaning-intensive production and creative economy are emerging as crucial assets in international competition. Many countries revised their cultural exportation strategies in the 1990s, adopting the creative economy sector as a key strategy in international competitiveness. The strengths of Finnish cultural exports are our large creative capital, high-standard education in the creative fields, strong technological know-how, good domestic infrastructure in culture, well-functioning domestic market and high-quality creative production. Our cultural production is highly valued internationally, and we cannot meet the international demand for Finnish culture. The weak points in our cultural exports are leakage points in the value chain, information, marketing, promotion, and lack of a strategy and coordination in cultural exportation.