Toll Global Forwarding – Strategy Rollout Continued, Earnings and Margins Improving

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Autumn 2017 Twuwheel

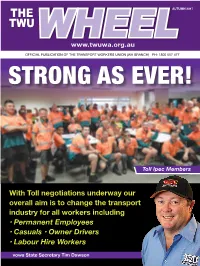

THE AUTUMN 2017 TWUWHEEL www.twuwa.org.au OFFICIAL PUBLICATION OF THE TRANSPORT WORKERS UNION (WA BRANCH) PH: 1800 657 477 STRONG AS EVER! Toll Ipec Members With Toll negotiations underway our overall aim is to change the transport industry for all workers including • Permanent Employees • Casuals • Owner Drivers • Labour Hire Workers vows State Secretary Tim Dawson Do you need a HR truck licence? We offer 1 or 2 day HR-B for $990* or lessons to suit your requirement Other transport essentials available Fatigue Management Certificate III Driver operations First Aid Load Restraint / Secure Cargo Implement Traffic Management Plan Forklift Call us today to discuss your requirements Unit 2 / 347 Great Eastern Hwy Fire Courses Redcliffe WA 6104 Supply Fire & First Aid equipment (08) 6180 -8065 / 0427 159 039 RTO 40599 Considering a career in Public Transport? With 13 depots across Perth and the SouthWest, there is sure to be one near you. Contact 9247 7500 or download an application form at www.swantransit.com.au Published by Perth Advertising Services. Phone: 9375 1922. Fax: 9275 2955. RATECUTTING RIFE! system to tackle the root causes of ‘Things have never many truck crashes. Instead, pressure is increasing on drivers to speed, drive long hours and been this bad for skip their mandatory rest breaks. The Turnbull Government’s own report showed the RSRT would have cut truck owner drivers’ crashes by 28% and yet it went ahead claims TIM DAWSON and tore it down. It is clearly willing to play politics with people’s lives. Throughout the transport industry the highest for any industry, according hundreds of owner-drivers are either to Safe Work Australia. -

Annual Report 2020 Contents Contents

ANNUAL REPORT 2020 CONTENTS CONTENTS About Us ..............................................................................4 ALC Members ......................................................................5 Message From ALC Chair, Philip Davies .............................6 Message From CEO, Kirk Coningham, OAM ......................8 Board Members ...................................................................12 Our Values ...........................................................................14 ALC Team Members ............................................................14 Committees .........................................................................15 Strategic Plan ......................................................................18 COVID-19 ............................................................................20 @AustLogistics Key Policy & Advocacy Achievements ................................22 Key Safety Achievements ....................................................24 linkedin.com/company/australian-logistics-council Appendix .............................................................................26 Policies ..........................................................................27 Suite 17B, National Press Club Building Submissions ..................................................................27 16 National Circuit, BARTON, ACT 2611 P: +61 2 6273 0755 Media Releases .............................................................28 E: [email protected] Financials .......................................................................30 -

For Personal Use Only Use Personal For

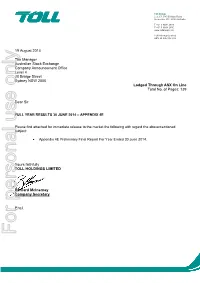

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 F +61 3 9694 2880 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 19 August 2014 The Manager Auustralian Stock Exchange Company Announcement Office Level 4 20 Bridge Street Sydney NSW 2000 Lodged Through ASX On Line Total No. of Pages: 139 Dear Sir FULL YEAR RESULTS 30 JUNE 2014 – APPENDIX 4E Please find attached for immediate release to the market the following with regard the abovementioned subject: • Appendix 4E Preliminary Final Report For Year Ended 30 June 2014. Yours faithfully TOLL HOLDINGS LIMITED Bernard McInerney Company Secretary Encl. For personal use only TOLL HOLDINGS LIMITED AND ITS CONTROLLED ENTITIES Preliminary Final Report for the Year Ended 30 June 2014 ASX Appendix 4E Preliminary Final Report Name of entity Toll Holdings Limited ABN 25 006 592 089 Reporting period Year ended 30 June 2014 Previous corresponding period Year ended 30 June 2013 Results for announcement to the market 201 4 201 3 Change Change $M $M $M % Revenue 8,811.2 8,719.4 91.8 +1.1 EBIT pre individually significant items 444.4 425.9 18.5 +4.3 NPAT pre individually significant items 298.5 282.4 16.1 +5.7 Individually significant items (net of tax) (5.4) (190.7) 185.3 Net profit after tax 293.1 91.7 201.4 +219.6 Non-controlling interests (7.0) (7.2) 0.2 +2.8 NPAT attributable to shareholders 286.1 84.5 201.6 +238.6 Refer to attached Media Release for commentary on results. -

Media Release

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 Media Release 30 October 2017 Peter Stokes joins Toll Group global leadership team Toll Group has appointed Peter Stokes as President, Group Operational Services, where he will lead a centralised network of operational functions to service Toll’s three divisions in express networks, contract logistics and global forwarding. Mr Stokes brings with him over 20 years of senior leadership experience in logistics and mining operations, with previous leadership roles at Barminco, Linfox and Accenture. He brings significant global experience having worked in markets across Africa, Asia, Australia, the UK and the USA. Toll Group’s Managing Director, Michael Byrne said Mr Stokes joins Toll at an important period, as the business builds a world-class logistics operations capability. “Mr Stokes brings a wealth of senior leadership experience, with a strong focus on safety and operational excellence. He will play a key role in delivering the next generation of Toll’s operational capability so we can support our customers and drive significant improvements in safety and productivity,” said Mr Byrne. Created in July 2017, Toll’s Group Operational Services covers linehaul, equipment, labour resourcing, property and procurement. The formation of the Group is expected to drive significant improvements to safety, operating efficiency and procurement outcomes through standardization of process and removal of duplication. Mr Stokes holds a MBA from Bond University, Queensland and recently attended an Advanced Management Program at Harvard Business School. -

CAE in Australia

CAE in Australia Overview CAE is an experienced training systems integrator across air, naval, land and public safety domains. The company employs 10,000 people at more than 160 sites and training locations in 35 countries. CAE offers customers a complete range of highly innovative products, services and training centre solutions designed to help them meet their mission critical needs for safety, efficiency and readiness. Defence and Security For over 25 years CAE Australia Pty Ltd, now based in Homebush, New South Wales, has had a significant presence in Australia that today includes approximately 200 employees supporting training in Australia and New Zealand at more than 20 sites serving the defence, civil aviation and healthcare markets. CAE Australia Pty Ltd is one of the key regional business operations that make up CAE’s global Defence and Security business unit. CAE Australia is consistently recognized as one of the top small-to-medium sized enterprises in Australia. Leveraging the full breadth of CAE’s global capabilities and leading-edge simulation technologies, CAE Australia brings proven solutions to the Australian market and surrounding region in addition to delivering world-class engineering and support services. Major programs for the Australian Defence Forces ÎÎRAAF Hawk Mk 127 Lead-in Fighter training ÎÎMRH90 training systems and support and support services at RAAF Pearce and services at Oakey and Townsville; RAAF Williamtown; ÎÎMH-60R Seahawk training systems and ÎÎPrime contractor on the Maintenance and support services at HMAS Albatross; Support of ADF Aerospace Simulators ÎÎAP-3C maintenance support services at RAAF (MSAAS) contract, as well as the Edinburgh; In addition, CAE supports the Royal Aerospace Simulation Through Life Support (ASTLS) contract; ÎÎKing Air 350 full-flight simulator training and Australian Air Force’s participation in support services at East Sale; Coalition Virtual Flag, which is one of the ÎÎKC-30A training systems and comprehensive world’s largest virtual air combat exercises. -

Regional Area Surcharge

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia Toll Transport Pty Ltd ABN: 31006604191 Regional Area Surcharge Regional area surcharges are applicable for pick up or delivery to regional, remote or off-shore locations where Toll incurs additional costs to service. Priority Service Suburb Postcode Price Abingdon Downs 4892 $ 51.50 Acacia Hills 0822 $ 26.00 Adavale 4474 $ 51.50 Adelaide River 0846 $ 26.00 Aherrenge 0872 $ 26.00 Alawa 0810 $ 26.00 Ali Curung 0872 $ 26.00 Alice Springs 0872 $ 26.00 Alice Springs 0870 $ 26.00 Almaden 4871 $ 51.50 Aloomba 4871 $ 51.50 Alyangula 0885 $ 26.00 Amata 0872 $ 26.00 American Beach 5222 $ 51.50 American River 5221 $ 51.50 Amoonguna 0873 $ 51.50 Ampilatwatja 0872 $ 26.00 Anatye 0872 $ 26.00 Andamooka 5722 $ 77.50 Anduramba 4355 $ 51.50 Angledool 2834 $ 51.50 Angurugu 0822 $ 26.00 Anindilyakwa 0822 $ 26.00 Anmatjere 0872 $ 26.00 Annie River 0822 $ 26.00 Antewenegerrde 0872 $ 26.00 Anula 0812 $ 26.00 Araluen 0870 $ 26.00 Archer 0830 $ 26.00 Archer River 4892 $ 51.50 Archerton 3723 $ 26.00 Area C Mine 6753 $ 51.50 Areyonga 0872 $ 26.00 Arnold 0852 $ 26.00 Arumbera 0873 $ 51.50 Ascot 4359 $ 77.50 Atitjere 0872 $ 26.00 Aurukun 4892 $ 51.50 Austinville 4213 $ 26.00 Avon Downs 0862 $ 26.00 Ayers Range South 0872 $ 26.00 Ayers Rock 0872 $ 26.00 Ayton 4895 $ 51.50 Badu Island 4875 $ 77.50 Bagot 0820 $ 26.00 1 Regional Area Surcharge (RAS) Baines 0852 $ 26.00 Bakewell 0832 $ 26.00 Balgowan 5573 $ 26.00 Balladonia 6443 $ 77.50 Balranald 2715 $ 77.50 Bamaga 4876 $ 77.50 Banks Island 4875 $ 77.50 -

CAE in Australia

CAE in Australia Overview technologies, CAE Australia brings proven In addition, CAE supports the Royal solutions to the Australian market and Australian Air Force’s participation in CAE is an experienced training systems surrounding region in addition to delivering Coalition Virtual Flag, which is one of the integrator across air, land, naval and world-class engineering and support world’s largest virtual air combat exercises. public safety domains. The company services. Some of the major programs led CAE Australia also includes an experienced employs 8,500 people at more than 160 by CAE Australia for the Australian Defence professional services group, which is a sites and training locations in 35 countries. Forces include: market-leading consulting and engineering CAE offers customers a complete range services organization that leverages of highly innovative product, service and ÎÎRAAF Hawk 127 Lead-in Fighter training and modelling and simulation technologies training centre solutions designed to help support services at Pearce and Williamtown; and expertise to develop software-based them meet their mission critical needs for ÎÎManagement and Support of ADF Aerospace solutions for decision support and training safety, efficiency and readiness. Simulators (MSAAS) – CAE Australia is an Authorised Engineering Organisation and in complex environments. delivers a range of training support services; ÎÎKC-30A training systems and comprehensive training services at RAAF Amberley; ÎÎC-130J training systems and support services at RAAF Richmond, including a C-130J Fuselage Trainer in development and live C-130J flight instruction; ÎÎS-70A Black Hawk full-flight and mission simulator, maintenance training systems CMMI Level 3 rating and support services at Oakey; CAE Australia is the first defence contractor ÎÎMRH90 training systems and support in Australia to achieve the CMMI Level For over 20 years CAE Australia Pty Ltd, services at Oakey and Townsville; 3 rating specifically for Services. -

Toll Group Biography Brian Kruger Managing Director-Elect

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 F +61 3 9694 2880 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 4 August 2011 The Manager Australian Stock Exchange Company Announcement Office Level 4 20 Bridge Street Sydney NSW 2000 Lodged Through ASX On Line Total No. of Pages: 5 Dear Sir MEDIA RELEASE : Former BHP and Bluescope executive, Toll CFO Brian Kruger appointed Managing Director Please find attached a media release for immediate release to the market. Yours faithfully TOLL HOLDINGS LIMITED Bernard McInerney Company Secretary Encl. Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 F +61 3 9694 2880 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 MEDIA RELEASE 4 August 2011 Former BHP and Bluescope executive, Toll CFO Brian Kruger appointed Managing Director The Board of Toll Holdings today announced that CFO Mr Brian Kruger will become the company’s Managing Director (MD) on 1 January 2012. The appointment follows a rigorous international search after the announcement in October 2010 of the planned retirement of logistics icon Mr Paul Little AO. With two years’ service with Toll and before that more than 25 years with the world’s largest miner and Australia’s largest steelmaker, Mr Kruger has extensive executive and operational experience. Chairman Ray Horsburgh AM said, “The Board congratulates Brian on his appointment. He has an outstanding business pedigree and will be a highly capable successor to Paul. He has demonstrated his capability in operational and financial roles in Australia as well as internationally. -

E-AWB Performance Monitoring Top 100 Airports Overview – September 2020

e-AWB performance monitoring Top 100 Airports Overview – September 2020 To represent, lead and serve the airline industry Top 100 Airports Overview – List of airports in scope AKL Auckland, New Zealand 3 EWR Newark, USA 35 MEL Melbourne, Australia 67 YUL Montreal, Canada 99 AMS Amsterdam, Netherlands 4 EZE Buenos Aires, Argentina 36 MEX Mexico City, Mexico 68 YVR Vancouver, Canada 100 ARN Stockholm, Sweden 5 FCO Rome, Italy 37 MIA Miami, USA 69 YYZ Toronto, Canada 101 ATH Athens, Greece 6 FRA Frankfurt, Germany 38 MMX Malmo, Sweden 70 ZRH Zurich, Switzerland 102 ATL Atlanta, USA 7 FUK Fukuoka, Japan 39 MNL Manila, Philippines 71 AUH Abu Dhabi, United Arab Emirates 8 GDL Guadalajara, Mexico 40 MUC Munich, Germany 72 BCN Barcelona, Spain and Canary Islands 9 GLA Glasgow, United Kingdom 41 MXP Milan, Italy 73 BKK Bangkok, Thailand 10 GRU Sao Paulo, Brazil 42 NBO Nairobi, Kenya 74 BLL Billund, Denmark 11 GVA Geneva, Switzerland 43 NGO Nagoya, Japan 75 BLR Bengaluru, India 12 HAJ Hannover, Germany 44 NRT Tokyo, Japan 76 BNE Brisbane, Australia 13 HAM Hamburg, Germany 45 NUE Nuremberg, Germany 77 BOG Bogota, Colombia 14 HEL Helsinki, Finland 46 ORD Chicago, USA 78 BOM Mumbai, India 15 HKG Hong Kong, Hong Kong (SAR), China 47 OSL Oslo, Norway 79 BOS Boston, USA 16 HND Tokyo, Japan 48 PEK Beijing, People's Republic of China 80 BRU Brussels, Belgium 17 IAD Washington, USA 49 PEN Penang, Malaysia 81 BSL Basel/Mulhouse, Switzerland 18 IAH Houston, USA 50 PER Perth, Australia 82 BUD Budapest, Hungary 19 ICN Seoul, Korea, Republic of 51 PRG Prague, -

CV Newsletter – Issue 13, JUNE 2015

ISSUE 13, JUNE 2015 Realising Opportunities Continuing our successful track record investing in Australasian growth companies CHAMP Ventures has had a busy year, completing four new investments over the last six months, across a diverse range of sectors – financial services, education, real estate services and contract Gareth Banks [email protected] catering. Director Phone: +61 2 8248 8859 Sea Swift has also executed a sale agreement to acquire the business Nicholas Chin [email protected] assets of Toll Marine in North Queensland and the Northern Territory. Associate Phone: +61 2 8248 8816 The CHAMP Ventures 7 portfolio now comprises seven investments, Jonathan Kelly [email protected] Director Phone: +61 2 8248 8852 following the successful realisation of SG Fleet at IPO in March 2014. Adrian Kerley [email protected] We also welcome two new team members, with CHAMP Ventures now Associate Director Phone: +61 2 8248 8834 totalling eleven investment professionals. Ghazaleh Lyari [email protected] CHAMP Ventures partners with entrepreneurs and management teams Consultant Phone: +61 2 8248 8839 to achieve their growth plans. We are actively investing $20-80 million in both minority shareholding and control opportunities. William Middleton [email protected] Associate Phone: +61 2 8248 8862 We look forward to hearing from you. Paul Readdy [email protected] Director Phone: +61 7 3010 9309 Please contact any member of the CHAMP Ventures team to discuss a potential opportunity. Greg Smith [email protected] -

Toll Holdings Limited Annual Report 2012 Toll Group Is the Asian Region’S Leading Provider of Integrated Logistics

For personal use only Toll Holdings Limited Annual Report 2012 Toll Group is the Asian region’s leading provider of integrated logistics. Operating out of the Asia Pacific region, with a global reach, Toll employs around 45,000 people in over 55 countries. The Group is divided into six divisions. Toll Global Toll Global Toll Global Toll Global Toll Domestic Toll Specialised Resources Logistics Forwarding Express Forwarding and Domestic Provides logistics World-class contract International freight Market leading Domestic freight Freight services to the oil logistics solutions forwarding and express freight operator forwarding across Provides a & gas, mining, and provider in the advanced supply in Australia providing Australia and comprehensive suite of government and Asia Pacific region. chain management time sensitive freight New Zealand. options Australia-wide defence sectors services. distribution, and top for palletised freight, in Australia, Asia 10 express logistics liquids distribution, and Africa. provider in Japan. chemicals distribution and warehousing, through to relocation services. Industries we worked Revenue split by with in FY12 division in FY12 32% 14% Toll Global Resources 17% Toll Global Logistics 10% Toll Global Forwarding 15% 16% Toll Global Express 10% 26% 8% 8% 6% 5% 16% Toll Domestic Forwarding 17% Toll Specialised and Retail, foodMining and beverage andSteel resources and industrialTransport GovernmentAutomotive and defenceChemical and machinery andOther agribusiness Domestic Freight Contents 2012 highlights 1 Corporate -

The ACE Training Centre and Seeing Machines to Launch Unique Eye Tracking Technology Trial

Toll Group Level 7, 380 St Kilda Road Melbourne VIC 3004 Australia T +61 3 9694 2888 www.tollgroup.com Toll Holdings Limited ABN 25 006 592 089 Media release 8 March 2019 The ACE Training Centre and Seeing Machines to launch unique eye tracking technology trial Toll Helicopters and Seeing Machines have joined forces to launch a unique eye tracking technology trial this month as part of the Toll AW-139 Full Flight Simulator (FFS) at the ACE Training Centre in Sydney. The trial is based on Seeing Machines’ Crew Training System prototype which incorporates modern eye tracking technology. The system supports aviation training instructors, pilots and crewmen with intelligent, evidence based data to provide detailed insights into pilot scanning techniques and situational awareness. The 2019 trial will build on insights gathered from smaller trials conducted by Toll and Seeing Machines over the past 24 months, which have produced tangible benefits for pilots, aircrewmen and instructors: • Instructors – can observe crew instrument and broader cockpit scanning in real-time in the Full Flight Simulator environment, as well as during debriefs. The unique technology provides instructors an objective assessment of what their trainees are looking at (such as speed tape, height, glide slope, heading, flight mode annunciator), at any given point in time during a flying sequence. The information can be used to quickly identify scan breakdowns, missed information, CRM (crew resource management) attention distribution, and standard operating procedure / Flight Crew Operating Manual (FCOM) adherence or deviation. • Trainee pilots – will benefit from objective feedback from their eye tracking replay, as they achieve even higher levels of performance.