A New Era in China Navigating Shifting Perceptions, Changing Realities a New Era in China Navigating Shifting Perceptions, Changing Realities

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Base De Datos De Códigos De Marcas De Vehículos Automotores Y Afines Actualizado Al 03 De Marzo De 2020

BASE DE DATOS DE CÓDIGOS DE MARCAS DE VEHÍCULOS AUTOMOTORES Y AFINES ACTUALIZADO AL 03 DE MARZO DE 2020 Nombre de marca Código FOREDIL 1 ASTRA 2 KOBELCO 3 ALFA ROMEO 4 ALPINE 5 APRILIA 6 AMBASSADOR 7 LIBERTY 8 A.M.X 9 AEOLUS 10 GORFETT 11 ARO 12 LOTUS 13 ASCORT 14 KRESKE 15 AUDI 16 AUSTIN 17 CURTIS WRIGHT 18 PANGARO 19 ELLIOT MACH 20 MHNCK 21 BENTLEY 22 B.M.W. 23 MACAL 24 BERT 25 BOND 26 BUSH HOG 27 BUICK 28 CADILLAC 29 EUROMOTOS 30 KRAZ 31 CHEVROLET 32 CHRYSLER 33 Nombre de marca Código BARQUARD 34 CITROEN 35 MINZK 36 CLENET 37 CIAO 38 DAF 39 DAIHATSU 40 DAIMLER 41 DATSUN 42 DESMCO 43 DE LOREAN SSS 44 PALI 45 D.K.W. 46 DODGE 47 ENZMAN 48 ESCALIBUR 49 CHARCK 50 FERRARI 51 FIAT 52 CEDARAPIDS 53 FORD 54 FORD-WILLYS 55 CARLIN 56 FRUEHAUF 57 GILBERN 58 ZILL 59 GREMLIN 60 HILLMAN 61 HONDA 62 HORNET 63 HUMBER 64 IMPERIAL 65 INNOCENTI 66 URB3A3 67 INTERNATIONAL 68 ALAB 69 ISUZU 70 JAGUAR 71 Nombre de marca Código JAVELIN 72 JEEP 73 TRAILEZE 74 LAMBORGHINI 75 LANCIA 76 LEYLAND-INNOCENTI 77 TFI 78 LINCOLN 79 COTTRELL 80 STER AZUL 81 MARLIN 82 MASERATI 83 MATADOR 84 MATRA 85 MERCURY 86 M.G. 87 OHIO 88 MITSUBISHI 89 BILLIS 90 MORRIS 91 MOSKOVITCH 92 NISSAN 93 N.S.U. 94 OWENS 95 JINCHENG 96 BETA 97 FSO 98 HAPAG LLOYD 99 TRANS GLOBAL 100 PLYMOUTH 101 PONTIAC 102 PORSCHE 103 SSANG YONG 104 ROVER 105 HARMEN 106 RENAULT 107 BEIJING 108 JIANSHE 109 Nombre de marca Código ROLLS-ROYCE 110 ZIL 111 RUGER 113 SAAB 114 SABRA 115 ORENSTEIN & KOPPEL 116 SCALDIA 117 SHIGULI 118 SIMCA 119 SCHAEFF 120 SKODA 121 FONTA 122 SUBARU 123 SUNBEAM 124 SUZUKI 125 TATSA 126 MORINI 127 THUNDERBIRD 128 FORDSON 129 TOYOTA 130 TRAILER 131 TRIDENT 132 TRIUMPH 133 BB & W 134 CLUB CAR 135 VAUXHALL 136 VOLKSWAGEN 137 VOLVO 138 HYOSUNG 139 PULLMAN 140 GILLI PHANTOM 141 WILLYS 142 WOLSELEY 143 TITAN 144 ZAZ 145 HERITAGE 146 BELLE 147 AUTOCAR 148 Nombre de marca Código ALL AMERICAN 149 ALLIS CHALMER 150 AMERICA MOTOR 151 ARMSTRONG 152 B.M.G. -

Volvo CE in China (Lingong) - a Case Study of Dual - Brand Strategy

ACADEMY OF EDUCATION AND BUSINESS STUDIES DEPARTMENT OF BUSINESS AND ECONOMIC STUDIES Volvo CE in China (Lingong) - a case study of dual - brand strategy Peng Shao Zeliang Sun June 2011 Bachelor’s Thesis in Business Administration Supervisor: Dr. Ernst.Hollander and Dr. Pär Vilhelmson Abstract Author: Peng Shao 890401T178 Zeliang Sun 880224T318 Supervisor: Ernst Hollander & Pär Vihelmson Date: 2012-02-22 Level: Bachelor Thesis Introduction: The part of introduction is presented to help readers give insight into the setting of our thesis. Firstly, we present the background of Volvo CE and Lingong. With the rapid economy growth and large amount of infrastructure construction projects, the large demand for CE push Volvo to accelerate its pace into Chinese market, the situation of the Chinese market and the importance are introduced continuously. We are aimed to analyze the dual - brand strategy implemented by Volvo and Lingong, and what synergies produced. We will also face two major limitations such as limited materials and hard access to interviewees. Lastly, we also have brief introduction for the outlet of the thesis. Theory Framework: This part includes three related theoretical fields. First one is global strategic marketing, as a MNE, Volvo CE entered China, which is one member of BRICs, and took acquisition of Lingong. The following is cross - boundaries culture and customer behavior, if one company wants to gain success in an overseas market, a good adaption to the local culture is essential. The last one is brand management field, brand is a intangible asset, however, in order to avoid cross - boundaries problems, Volvo CE decide to implement a dual - brand strategy, so we can use brand alliance theories to analyze. -

Código Reval. Marca Modelo Año Tipo Vehículo Atributo Combustible Carga Ejes Cilindros H.P

Aforo con Aforos Sin Código Reval. Marca Modelo Año Tipo Vehículo Atributo Combustible Carga Ejes Cilindros H.P. Cdada. Patente 2010 ($) IVA (U$S) IVA (U$S) 124620 AGRALE MA 8.5 2009 MICROBUS S/ATRIBUTO GAS OIL 2500 2 4 0 4800 98.820 81.000 73.265 124373 AGRALE MA 8.5 2009 CAMION FURGON BLINDADO GAS OIL 2500 2 4 0 4300 99.063 81.199 40.803 125085 AGRALE MA 9.2 SENIOR TUR. 2009 MICROBUS S/ATRIBUTO GAS OIL 0 2 4 41 4100 96.300 78.934 71.396 123824 ALFA ROMEO 147 TWIN SPARK 2.0 2009 SEDAN 4 PUERTAS S/ATRIBUTO NAFTA 0 2 4 20 2000 42.990 35.238 31.873 124392 ALFONZO 2009/15T 2009 REMOLQUE CARGA GENERAL S/MOTOR 15000 2 0 0 0 32.000 26.230 5.206 125047 ANCHI MC 6320 PRINCE 2009 SEDAN 2 PUERTAS S/ATRIBUTO NAFTA 0 2 4 0 800 11.890 9.746 8.815 123313 APOLLO AGB-30 2009 MOTOCICLETA S/ATRIBUTO NAFTA 0 2 1 0 150 2.250 1.844 1.070 123979 APOLLO AGB-30 E 2009 MOTOCICLETA S/ATRIBUTO NAFTA 0 2 1 0 250 2.690 2.205 1.540 124587 APOLLO AGB-31 2009 MOTOCICLETA S/ATRIBUTO NAFTA 0 2 1 2 250 3.400 2.787 2.171 123282 APOLO AGB30 2009 MOTOCICLETA S/ATRIBUTO NAFTA 0 2 1 2 250 2.690 2.205 1.540 124986 ARAGAN S/MODELO 2009 REMOLQUE FURGON S/MOTOR 250 1 0 0 0 500 410 193 123925 ARTIGAS S/MODELO 2009 REMOLQUE CARGA GENERAL S/MOTOR 18000 2 0 0 0 26.000 21.311 9.253 124316 ASAKI ASQ6 2009 CAMIONETA S/ATRIBUTO NAFTA 900 2 4 10 1050 9.750 7.992 7.229 124831 ASAKI AUTOMATIC 100 2009 MOTOCICLETA S/ATRIBUTO NAFTA 0 2 1 1 100 890 730 498 123931 ASAKI AZ 110 2009 MOTOCICLETA S/ATRIBUTO NAFTA 0 2 1 0 110 925 758 498 124112 ASAKI CX 125 2009 MOTOCICLETA S/ATRIBUTO NAFTA 0 2 1 -

Volvo-Group-Presentation.Pdf

Volvo Group presentation Driving prosperity through transport solutions OUR MISSION Driving prosperity through transport solutions Modern logistics is a prerequisite for our economic welfare: transport helps combat poverty. Transport is not an end in itself, but rather a means allowing people to access what they need, economically and socially. Volvo Group Company presentation 2 2019 Q1 OUR VISION Be the most desired and successful transport solution provider in the world We are in a people business. We operate in a business-to-business market, where people make the decisions. Trust and relations are as important as the total offer. By bringing together the best of everything from the offer to the relationship, we will become the customers’ preferred choice. Volvo Group Company presentation 3 2019 Q1 OUR ASPIRATIONS Have leading customer Be the most Have industry satisfaction for all brands admired employer leading profitability in their segments in our industry Volvo Group Company presentation 4 2019 Q1 OUR VALUES Customer success We make our customers win. Trust We trust each other. Passion We have passion for what we do. Change We change to stay ahead. Performance We are profitable to shape our future. Volvo Group Company presentation 5 2019 Q1 Volvo Group We are one of the world’s leading manufacturers of trucks, buses, construction equipment and marine and industrial engines. We also provide complete solutions for financing and service. Volvo Group Company presentation 6 2019 Q1 Volvo Group We employ almost 100.000 PEOPLE, have production facilities in 18 COUNTRIES and sell our products in more than 190 MARKETS. -

Land of Opportunity

STORIES FROM THE WORLD OF VOLVO GROUP SALES EDITION THE BUS BUZZ LEADING THE WAY IN SUSTAINABLE PUBLIC TRANSPORT SOLUTIONS CREATING ENGAGEMENT HIGHLY ENGAGED TEAMS SHARE THEIR BEST TIPS WORKING UNDER COVER IMPROVING SERVICES THROUGH MYSTERY CUSTOMERS “I spend about a week at a time out on the road, together with my two dogs.” Danny Locklear, a truck driver Land of for 14 years opportunity In the US, the Volvo Group is successfully adapting its products and services to better meet local customer needs EDITORIALL 10 We are committed and will stick to the plan N APRIL 22, the AB Volvo Board of Directors appointed Martin Lundstedt new President and CEO of the Volvo Group. Martin will take office in October. Until then I have been entrusted to lead the Volvo Group, together with the entire OGroup Executive Team. Our top priorities for the rest of 2015 remain the same. 28 WE ARE COMMITTED to continuing the work we do every day to create value for our customers. And we are committed to delivering on our strategic efficiency programme to reduce the structural cost level in the Group. Both are vital to our company’s future success. We will always put our customers first, delivering products and services that enable them to keep the promises they have made to their customers. We need to deliver on the strategic efficiency programme and close the gap to our competitors. As we presented in our first quarter report, it is clear that we are well on our way but more remains to be done. -

Volvo Group Presentation 2015 English

Volvo Group 2016 Day in and day out, all around the year, people’s decisions and basic needs create demand for transports and infrastructure solutions. Without the type of products and services the Volvo Group provides, the societies where many of us live would not function. Together we move the world Volvo Group Headquarters The Volvo Group is one of the world’s leading manufacturers of trucks, buses, construction equipment and marine and industrial engines. The Volvo Group also provides complete solutions for financing and service. Volvo Group Headquarters The Volvo Group, which employs about 100,000 people, has production facilities in 18 countries and sales of products in more than 190 markets. Volvo Group Headquarters VisionOur vision Be the most desired and successful transport solution provider in the world Volvo Group Headquarters Our mission Driving prosperity through transport solutions Volvo Group Headquarters On the road In the city Off road At sea Volvo Group Headquarters Passion for customer success The majority of the Volvo Group’s customers are companies within the transportation or infrastructure industries. The reliabilityand productivity of the products are important and in many cases crucial to our customers’ success and profitability. Volvo Group Headquarters The employer of choice Customer success We make our customers win. Trust We trust each other. Passion We have passion for what we do. Change We change to stay ahead. Performance We are profitable to shape our future. Volvo Group Headquarters Our Organization CEO -

Volvo Group Annual and Sustainability Report 2019

VOLVO GROUP ANNUAL AND SUSTAINABILITY REPORT 2019 PERFORM AND TRANSFORM The Volvo Group 2019 Group Volvo The www.volvogroup.com A GLOBAL GROUP 2019 OVERVIEW DRIVING PROSPERITY Every company exists for a reason – it has a purpose. Our solutions to global challenges are driven by our mission to drive prosperity through transport solutions and our vision to be the most desired and successful transport solution provider in the world. We continuously develop our products and services to create value for our customers and to support sustainable soci- eties and the well-being and safety of people. OUR CUSTOMERS MAKE SOCIETIES WORK The Volvo Group’s products and services contribute to much of what we all expect of a well-functioning society. Our trucks, buses, engines, construction equipment and financial services are involved in many of the functions that most of us rely on every day. The major- ity of the Volvo Group’s customers are companies within the transportation or infrastruc- ture industries. The reliability and productivity of the products are important and in many cases c rucial to our customers’ success and profitability. A GLOBAL GROUP 2019 OVERVIEW ON THE ROAD OFF ROAD IN THE CITY AT SEA Our products help ensure that Engines, machines and vehicles Our products are part of daily Our products and services are people have food on the table, from the Volvo Group can be life. They take people to work, there, regardless of whether can travel to their destination found at construction sites, in collect rubbish and keep lights someone is at work on a ship, and have roads to drive on. -

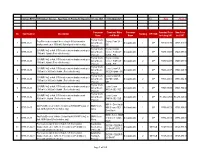

Contract RT57-2019 Contract Circular - Year Three (3) Pricing for the Period 01 July 2021 to 31 October 2021 Date Date 29-Jul-21

Contract RT57-2019 Contract Circular - Year three (3) Pricing for the period 01 July 2021 to 31 October 2021 Date Date 29-Jul-21 Contractor Combined Make Converter Awarded Price New Price No Item Number Description Ranking GP/ SUB Name and Model Name Including VAT Incl. VAT Toyota South Four/Five seater sedan 4 door or hatch 3/5 doors-piston Toyota Prius 1.8 - 1 RT57-00-01 Africa Motors Not Applicable 1 GP R518,531.55 R518,531.55 displacement up to 1900cm3, Hybrid (pool vehicles only) 42H (Pty) Ltd Toyota South Toyota Corolla SUV/MPV 4x2 or 4x4, 5/7/9 seater- piston displacement up to 2 RT57-00-04 Africa Motors Cross 1.8 XS CVT Not Applicable 1 GP R458,134.70 R429,497.64 1900cm3, Hybrid (Pool vehicles only) (Pty) Ltd Hybrid - P04 Toyota South Toyota Corolla SUV/MPV 4x2 or 4x4, 5/7/9 seater- piston displacement up to 3 RT57-00-04 Africa Motors Cross 1.8 XR CVT Not Applicable 2 GP R490,542.85 R459,651.55 1900cm3, Hybrid (Pool vehicles only) (Pty) Ltd Hybrid - P05 Toyota South SUV/MPV 4x2 or 4x4, 5/7/9 seater- piston displacement up to Lexus Lexus UX 4 RT57-00-05 Africa Motors Not Applicable 1 GP R660,220.75 R660,220.75 1901cm3 to 3000cm3, Hybrid (Pool vehicles only) 250 EX Hybrid - 68J (Pty) Ltd Toyota South Lexus Lexus UX SUV/MPV 4x2 or 4x4, 5/7/9 seater- piston displacement up to 5 RT57-00-05 Africa Motors 250 SE Hybrid - Not Applicable 2 GP R730,404.10 R730,404.10 1901cm3 to 3000cm3, Hybrid (Pool vehicles only) (Pty) Ltd 68K Toyota South SUV/MPV 4x2 or 4x4, 5/7/9 seater- piston displacement up to Lexus Lexus 6 RT57-00-05 Africa Motors -

2020PERMENDAGRI8.Pdf

SALINAN MENTERI DALAM NEGERI REPUBLIK INDONESIA PERATURAN MENTERI DALAM NEGERI REPUBLIK INDONESIA NOMOR 8 TAHUN 2020 TENTANG PENGHITUNGAN DASAR PENGENAAN PAJAK KENDARAAN BERMOTOR DAN BEA BALIK NAMA KENDARAAN BERMOTOR TAHUN 2020 DENGAN RAHMAT TUHAN YANG MAHA ESA MENTERI DALAM NEGERI REPUBLIK INDONESIA, Menimbang : bahwa untuk melaksanakan ketentuan Pasal 5 ayat (9) Undang-Undang Nomor 28 Tahun 2009 tentang Pajak Daerah dan Retribusi Daerah, perlu menetapkan Peraturan Menteri Dalam Negeri tentang Penghitungan Dasar Pengenaan Pajak Kendaraan Bermotor dan Bea Balik Nama Kendaraan Bermotor Tahun 2020; Mengingat : 1. Undang-Undang Nomor 39 Tahun 2008 tentang Kementerian Negara (Lembaran Negara Republik Indonesia Tahun 2008 Nomor 166, Tambahan Lembaran Negara Republik Indonesia Nomor 4916); 2. Undang-Undang Nomor 22 Tahun 2009 tentang Lalu Lintas dan Angkutan Jalan (Lembaran Negara Republik Indonesia Tahun 2009 Nomor 96, Tambahan Lembaran Negara Republik Indonesia Nomor 5025); 3. Undang-Undang Nomor 28 Tahun 2009 tentang Pajak Daerah dan Retribusi Daerah (Lembaran Negara Republik Indonesia Tahun 2009 Nomor 130, Tambahan Lembaran Negara Republik Indonesia Nomor 5049); - 2 - 4. Undang-Undang Nomor 23 Tahun 2014 tentang Pemerintahan Daerah (Lembaran Negara Republik Indonesia Tahun 2014 Nomor 244, Tambahan Lembaran Negara Republik Indonesia Nomor 5587) sebagaimana telah beberapa kali diubah, terakhir dengan Undang- Undang Nomor 9 Tahun 2015 tentang Perubahan Kedua atas Undang-Undang Nomor 23 Tahun 2014 tentang Pemerintahan Daerah (Lembaran Negara -

Volvo Group Acquires 45% of Dongfeng Commercial Vehicles

Volvo Group acquires 45% of Dongfeng Commercial Vehicles JANUARY 26, 2013 Volvo Group Headquarters Volvo-Dongfeng - December xx, 2012 Volvo to become the world’s largest heavy-duty truck manufacturer • AB Volvo has signed an agreement with the Chinese vehicle manufacturer Dongfeng Motor Group Company Limited (DFG) to acquire 45% of a new subsidiary of DFG, Dongfeng Commercial Vehicles (DFCV), which will include the major part of Dongfeng’s medium and heavy commercial vehicles business. • Completion of the transaction will make the Volvo Group the world’s largest manufacturer of heavy-duty trucks with a combined annual volume (2011) of 326,000 HD trucks and 98,000 MD trucks. • The transaction is subject to approval of relevant Chinese authorities and anti-trust agencies. Volvo Group Headquarters Volvo-Dongfeng - December xx, 2012 2 Group Trucks’ strategic objectives 2013-2015 3.1 By optimizing the brand assets become number 1 or 2 in combined Group Trucks HD market share This agreement supports the 3.2 Establish required commercial strategic objective for the Volvo Group’s presence to support revenue growth by 50% in APAC and 25% in Africa truck business to capture profitable 3.3 Establish required OtD footprint and supply chain in APAC & Africa growth in Asia Pacific achieving lead time reduction by 15% and capital tied up reduction by 15% 3.4 Increase Aftermarket sales per unit in operation by 12%, including total commercial solution offer for second owner 3.5 Build 1 BSEK new businesses complementary to existing offering Volvo Group Headquarters Investor Day 2012 3 Volvo Group acquires 45% of DFCV for RMB 5.6 bn Purchase price RMB 5.6 bn for 45% ownership Volvo Dongfeng Group (DFG) 45% 55% DFCV DFCV 100% DND Volvo Group Headquarters Volvo-Dongfeng - December xx, 2012 4 DFCV: a large commercial vehicle company with a strong position in China VOLUMES FINANCIALS (RMB) * 1 RMB = 1.05 SEK 2011 2012 FY2011 Q312 YTD HD trucks 142,000 102,000 Net sales 39 bn 22 bn MD trucks 49,000 46,000 Op Inc. -

John F. Kennedy Space Center

GP-589 Revised July 1973 JOHN F. KENNEDY SPACE CENTER (NASA-TM-X-69523) A SELECTIVE LIST OF N73-32908 ACRONIHS AND ABBREVIATIONS (NASA) 205 p HC $12.25 CSCL 05B Unclas G3/34 18468 A SELECTIVE LIST OF ACRONYMS AND ABBREVIATIONS Compiled by THE DOCUMENTS DEPARTMENT KENNEDY SPACE CENTER LIBRARY Reproduced by NATIONAL TECHNICAL INFORMATION SERVICE US Department of Commerce Springfield, VA. 22151 NASA-PAFB APR/70 N73-32908 A SELECTIVE LIST OF ACRONYMS AND ABBREVIATIONS July 1973 DISTRIBUTED BY: KKn National Technical Information Service U. S. DEPARTMENT OF COMMERCE 5285 Port Royal Road, Springfield Va. 22151 NOTICE THIS DOCUMENT HAS BEEN REPRODUCED FROM THE BEST COPY FURNISHED US BY THE SPONSORING AGENCY. ALTHOUGH IT IS RECOGNIZED THAT CER- TAIN PORTIONS ARE ILLEGIBLE, IT IS BEING RE- LEASED IN THE INTEREST OF MAKING AVAILABLE AS MUCH INFORMATION AS POSSIBLE. July 1973 JOHN F. KENNEDY SPACE CENTER, NASA GP-589 Revised A SELECTIVE LIST OF ACRONYMS AND ABBREVIATIONS KENNEDY SPACE CENTER LIBRARY APPROVAL (Mrs.)L.^. RusselT KSC Librarian . Date__—« bjA. —J. J7J17___ 3 PREFACE The Documents Department of the KSC Library has frequently been asked if there were available any number of lists con- taining acronyms, abbreviations, initials, code words and phrases generally used at the John F. Kennedy Space Center (KSC). After a careful search, only KSC GP-334, KSC Scheduling Abbreviation Glossary, was found. Therefore, to meet the need of the KSC Community, the Documents Department prepared KSC GP-589, the first selective list of - acronyms and abbreviations, with the issue date of October 28, 1969. This issue is the fourth revision to that list and is the most comprehensive one yet available in this format at KSC. -

Sino-Finnish Paths to International Competitive Advantage Contact Information

Perspective John Jullens Hannu Suonio Tony Tang Sino-Finnish Paths to International Competitive Advantage Contact Information Booz & Company John Jullens Partner Suite 2511, One Corporate Avenue No. 222 Hu Bin Road Shanghai 200021, P.R. China Tel: +86 21 2327 9800 Fax: +86 21 2327 9833 Blog: www.johnjullens.com [email protected] Booz & Company Oy Hannu Suonio Partner Mikonkatu 15B, 7th floor Helsinki 00100, Finland Tel: +358-9-6154 6614 Mobile: +358-40-511 9324 [email protected] Booz & Company It may seem ironic that China’s future depends increasingly on the country’s EXECUTIVE ability to forge new paths for growth through international expansion. Over SUMMARY the last 30 years, China has grown at a breakneck pace, largely because of the West’s insatiable appetite for goods that China produced with its near-limitless supply of low-cost labor. But success breeds its own challenges. Rising wages are gradually eroding China’s low-cost advantage, and the country’s continued progress now increasingly hinges on its ability to transform itself from a low- cost to a high-value economy. Some of China’s best opportunities for target sector is in a “sunrise” or glob- developing the capabilities and acquir- ally mature industry. These criteria ing the technology needed to make serve as the basis for our Market that transition are to be found abroad Opportunity Matrix, which charac- and can be captured only through terizes four broad opportunity sets for partnerships with foreign entities. Finnish and Chinese companies seek- ing international partnerships. Finland also needs its companies to expand internationally to drive overall The first part of this report explains economic growth.