H1 2021 Review of Shareholder Activism

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report and Accounts 2013 Annual Report and Accounts 2013

Annual Report and Accounts 2013 Annual Report and Accounts 2013 Brewin Dolphin Holdings PLC, 12 Smithfield Street, London EC1A 9BD T 020 7246 1000 F 020 3201 3001 W brewin.co.uk E [email protected] Brewin Dolphin provides a range of investment management, financial advice and execution only services in the UK and Eire. “Our priorities are clear. They are to reinforce our high standard of service to clients and ensure an improved return to shareholders. Discretionary Investment Management is currently the core of our business model and our mission is to provide a compelling and consistent offering, relevant to all our clients. Over the past decade we have evolved from a stockbroker into a private client investment manager. Our evolution must continue as we strive to become the leading provider of personal Discretionary Wealth Management in the UK.” David Nicol, Chief Executive Investment proposition • Strong client relationships with a long-term track record of personalised service • Growth market with good long-term prospects • New management team with clear goals and a strategy to achieve them • Our strategy will generate value for all stakeholders We are already creating value in 2013 • Total income grew by 9% to £283.7m • Adjusted profit before tax grew by 22% to £52.3m • Adjusted profit margin increased from 16.5% to 18.5% • Discretionary funds under management (FUM) grew by 17% to £21.3bn • Adjusted earnings per share (EPS) grew by 19.2% to 14.9p (2012: 12.5p) • Full year dividend increased by 20% to 8.6p • Total Shareholder Return was 63% Contents Business review Section 1 Business review Financial Highlights 02 Business Highlights 03 Chairman’s Statement 04 Overview of the Business and Strategy 06 Strategic Report 08 A. -

Making Sense of ESG, SRI and Impact Investing INSIGHTS

Investing with Purpose: Making Sense of ESG, SRI and Impact Investing INSIGHTS Many investors want to bring their portfolios into alignment with their personal values, but don’t know where to start. This Insights outlines the three most common approaches. CARIN L. PAI, CFA® A growing awareness of environmental which companies are making the Executive Vice President, and social issues, along with the most progress in this area, investors Head of Portfolio Management availability of data on corporate can find a comfortable place on responsibility, is changing the way the spectrum between doing well individuals think about investing. financially and doing good things for Increasingly, investors are bringing their the world. portfolios into alignment with their MICHAEL FIRESTONE personal values. Three Common Approaches Managing Director, to Responsible Investing Portfolio Manager There are many different approaches to “responsible investing” and they go Responsible investing means different by different names—including ethical, things to different people, and there is sustainable and green investing. But a broad spectrum of approaches. But they all have one thing in common: the most commonly used techniques They pursue financial rewards while are ESG, SRI and Impact Investing. The approach investors take depends NATALIA LAZAR-GALOIU encouraging positive changes in Senior Investment the world. largely on their personal preferences Associate and which part of the spectrum they Doing Well Financially While find most appropriate—depending on Doing Good Socially how heavily they want to lean toward achieving financial goals versus Traditionally, investment decisions have promoting social causes. been aimed at achieving financial goals, using research on economic trends Environmental, Social, and analyzing a company’s balance Governance (ESG) sheet. -

Fund Selection

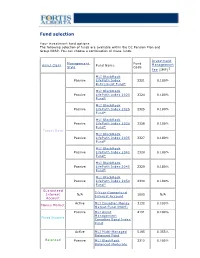

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S

Electric Vehicle Market Status - Update Manufacturer Commitments to Future Electric Mobility in the U.S. and Worldwide September 2020 Contents Acknowledgements ....................................................................................................................................... 2 Executive Summary ...................................................................................................................................... 3 Drivers of Global Electric Vehicle Growth – Global Goals to Phase out Internal Combustion Engines ..... 6 Policy Drivers of U.S. Electric Vehicle Growth ........................................................................................... 8 Manufacturer Commitments ....................................................................................................................... 10 Job Creation ................................................................................................................................................ 13 Charging Network Investments .................................................................................................................. 15 Commercial Fleet Electrification Commitments ........................................................................................ 17 Sales Forecast.............................................................................................................................................. 19 Battery Pack Cost Projections and EV Price Parity ................................................................................... -

MCERA May 5, 2021 Regular Board Meeting Agenda Page 1 of 4 B

AGENDA REGULAR BOARD MEETING MARIN COUNTY EMPLOYEES’ RETIREMENT ASSOCIATION (MCERA) One McInnis Parkway, 1st Floor Retirement Board Chambers San Rafael, CA May 5, 2021 – 9:00 a.m. This meeting will be held via videoconference pursuant to Executive Order N-25-20, issued by Governor Newsom on March 12, 2020, Executive Order N-29-20, issued by Governor Newsom on March 17, 2020, and Executive Order N-35-20, issued by Governor Newsom on March 21, 2020. Instructions for watching the meeting and/or providing public comment, as well as the links for access, are available on the Watch & Attend Meetings page of MCERA’s website. Please visit https://www.mcera.org/retirementboard/agendas-minutes/watchmeetings for more information. The Board of Retirement encourages a respectful presentation of public views to the Board. The Board, staff and public are expected to be polite and courteous, and refrain from questioning the character or motives of others. Please help create an atmosphere of respect during Board meetings. EVENT CALENDAR 9 a.m. Regular Board Meeting CALL TO ORDER ROLL CALL MINUTES April 14, 2021 Board meeting A. OPEN TIME FOR PUBLIC EXPRESSION Note: The public may also address the Board regarding any agenda item when the Board considers the item. Open time for public expression, from three to five minutes per speaker, on items not on the Board Agenda. While members of the public are welcome to address the Board during this time on matters within the Board’s jurisdiction, except as otherwise permitted by the Ralph M. Brown Act (Government Code Sections 54950 et seq.), no deliberation or action may be taken by the Board concerning a non-agenda item. -

Finding the Opportunity In

Finding the ESG disclosures: the bedrock of the opportunity sustainable finance agenda in ESG Executive summary To be successful, the development of sustainable finance in Europe needs to be grounded in access to high quality and meaningful ESG disclosures. While the quality and reliability of ESG data has improved considerably, so has the sophistication of investors and their needs for improved ESG disclosure. Investors find the most value in ESG disclosures when sustainability is embedded in the DNA of the firm as part of their competitive advantage to create long-term value. Companies that create societal value should benefit from changing policy and consumer trends, resulting in more sustainable cash flows, a lower cost of capital and higher valuations. While no standardised reporting framework can ever fully capture and reflect this. Reporting standards should, however, ensure that we move away from boilerplate disclosures and box-ticking approaches to consider the ESG risks and opportunities that are material to each company, industry and sector. While numerous standards already exist in this space, no single regulatory standard provides a comprehensive framework for companies to disclose in a way that would meet investors’ needs. Greater convergence in reporting could fill the gaps in accessing core ESG metrics that investors rely on to develop their ESG screening tools and assessment methodologies. Convergence in ESG reporting standards would also enable such data to be audited, which is becoming increasingly important to investors who base capital allocation decisions on such information. Beyond these core metrics, we need to connect ESG disclosures with real world outcomes, both adverse impacts as well as opportunities for transition. -

Lazard Global Managed Volatililty Fund Commentary

Lazard Global Managed Volatility Fund AUG Commentary 2021 Market Overview e global equity markets continued their historic recovery with a seventh straight monthly gain in August. Momentum was strong as many indices posted multiple all-time highs during the month. e United States, overcoming a decline in consumer condence, continued to lead the major equity markets. Federal Reserve Chairman Jerome Powell calmed investors’ fear of a sharp curtailment in the central bank’s stimulus programs while indicating that economic strength was sufficient for the Fed to consider a modest reduction in its bond repurchase program. e euro area reported surprisingly strong GDP growth for the second quarter, outpacing most major economies, including those of China and the United States. Corporate earnings in Europe recovered further as vaccinations increased and the economy continued to reopen. European sell-side analysts raised their earnings estimates at a historically high rate. Japan also posted a positive month but trailed other markets; its economy grew more than expected in the second quarter, counteracting the effects of the spike in COVID-19 cases that had caused a sell-off in July. e spike will likely temper growth in the third quarter. e favorable economic news and low interest rates benetted the emerging markets, which outpaced the developed markets in August. Sector performance showed only modest dispersion in August, with every sector except materials posting a positive return. Financials were the strongest sector for the month and have taken leadership from energy for the year. Global factor performance was also relatively muted in the month. Risk measures showed mixed results as lower beta stocks and stocks with higher volatility over the past year outperformed. -

Brewin Dolphin Holdings PLC Annual Report and Accounts 2015 Accounts and Report Annual

Brewin Dolphin Holdings PLC Holdings Dolphin Brewin Annual Report and Accounts 2015 Brewin Dolphin Holdings PLC Annual Report and Accounts 2015 Contents Overview 34 Corporate Responsibility 82 Directors’ Responsibilities 96 Consolidated Cash 02 Highlights 40 Resources and Relationships 83 Independent Auditor’s Report Flow Statement 04 Chairman’s Statement 97 Company Cash Flow Statement Governance Financial Statements 98 Notes to the Financial Strategic Report 44 Chairman’s Introduction 90 Consolidated Income Statement Statements 08 Business Overview to Governance 91 Consolidated Statement of 10 Business Model 46 Directors and their Biographies Comprehensive Income Additional Information 12 Market Environment 48 Corporate Governance Report 92 Consolidated Balance Sheet 148 Five Year Record Continuing 14 Our Strategy 53 Board Risk Committee Report 93 Consolidated Statement of Operations (unaudited) 16 Chief Executive’s Statement 56 Audit Committee Report Changes in Equity 149 Appendix – Calculation of KPIs 20 Measuring Our Performance 62 Nomination Committee Report 94 Company Balance Sheet 150 Glossary 23 Results 64 Directors’ Remuneration Report 95 Company Statement of Changes 151 Shareholder Information 30 Principal Risks and Uncertainties 80 Other Statutory Information in Equity 152 Branch Address List Brewin Dolphin Holdings PLC Annual Report and Accounts 2015 Overview Brewin Dolphin provides a range of investment management and financial advice services in the Strategic Report United Kingdom, Channel Islands and the Republic of Ireland. -

Impact Investing Primer

IMPACT INVESTING PRIMER I. What is Impact Investing? II. The Veris Perspective III. Have We Reached a Tipping Point? IV. How to Approach Impact in Public Equity and Fixed Income Investments V. How to Measure Impact VI. Impact Financial Performance Across Asset Classes VII. How to Conceptualize Impact Investing in Your Portfolio VIII. Impact Investing Across All Asset Classes IX. Impact & Mission‐Related Investing Terms X. Other Impact Investing Resources XI. Additional Resources I. What is Impact Investing? Impact Investing utilizes capital markets to address global challenges. Every investment has impact, whether intended or unintended. Impact investors, however, specifically seek out investments whose environmental and social outcomes are positive and definable. As Impact Investing becomes more mainstream, there are increasingly more opportunities to invest with impact. Impact investments are already available in both public and private markets and across all asset classes—including hard assets such as real estate, timber, and agriculture. Impact investments provide capital to innovative private companies providing solutions to global sustainability issues such as climate change, accessible education, and energy and food security. They also support public and private companies with responsible and sustainable business practices. Additionally, impact investments promote community wealth building by creating jobs in low‐income communities; helping in affordable housing initiatives and neighborhood revitalization; making loans to small businesses, and raising funds for vital community services. Impact Investing, whether private or public, stocks or bonds, requires professional management of social, environmental, and financial performance. The Global Impact Investing Network (GIIN), a non‐profit organization dedicated to increasing the scale and effectiveness of Impact Investing, defines it as “investments made into companies, organizations, and funds with the intention to generate measurable social and environmental impact alongside a financial return. -

Impact Investing Whitepaper

Impact Investing Whitepaper In partnership with Clear and Independent Institutional Investment Contents Analysis We provide institutional investors, including pension funds, 03 Introduction insurance companies and consultants, with data and analysis to assess, research and report on their investments. We are 04 Impact Investing Roundtable committed to fostering and nurturing strong, productive Welcome to CAMRADATA’s Impact Investing relationships across the institutional investment sector and are 09 Roundtable Participants Whitepaper continually innovating new solutions to meet the industry’s complex needs. 15 Arisaig Partners: Capturing The Rise Of Emerging Markets We enable institutional investors, including pension funds, Climate change is increasingly at the forefront of the global agenda, with a key focus insurance companies and consultants, to conduct rigorous, 18 Mackenzie Investments: To maximize on a ‘just’ transition to a net zero economy. Impact investing is set to play a crucial evidence-based assessments of more than 5,000 investment your energy transition exposure, think role if targets are to be met. products offered by over 700 asset managers. thematic Impact investors are vital in allocating capital in order to address the abundance of Additionally, our software solutions enable insurance 23 M&G Investments: Targeting solutions social and environmental issues facing the planet. companies to produce consistent accounting, regulatory and for the planet through impact Even as governments and corporations alike are ramping up their climate audit-ready reports. investing commitments, there is much work to be done. Time is running out for climate and social goals to be met. According to a recent To discuss your requirements study by the Rainforest Action Network, in the five years since the Paris Agreement, +44 (0)20 3327 5600 the world’s biggest banks – including the likes of BNP Paribas, Goldman Sachs, and [email protected] JP Morgan – have financed fossil fuels to the tune of $3.8 trillion (€3.2 trillion). -

LAZARD GROUP LLC (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2008 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to 333-126751 (Commission File Number) LAZARD GROUP LLC (Exact name of registrant as specified in its charter) Delaware 51-0278097 (State or Other Jurisdiction of Incorporation (I.R.S. Employer Identification No.) or Organization) 30 Rockefeller Plaza New York, NY 10020 (Address of principal executive offices) Registrant’s telephone number: (212) 632-6000 Securities Registered Pursuant to Section 12(b) of the Act: None Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. -

Private Funds Report 2020 Year in Review and a Look Ahead

PRIVATE FUNDS REPORT 2020 YEAR IN REVIEW AND A LOOK AHEAD VOLUME 1 A NEW PRIVATE FUNDS RESOURCE IN THIS ISSUE WELCOME TO THE FIRST EDITION OF PRIVATE FUNDS n INTRODUCTION 1 REPORT, a new collection of insights that we plan to publish intermittently throughout the year to supple- n FUNDRAISING 2 ment the content we produce already. We hope you’ll find n REGULATORY 7 our articles easily accessible, conversational and to the n SEC ENFORCEMENT 8 point—our goal is to provide topical perspective without burdening you with excess detail that could obscure the n DEPARTMENT OF LABOR key issues on which you might want to focus initially. We RULEMAKING 9 would welcome your feedback on this new resource. n LIBOR TRANSITION FOR THE BUY SIDE 11 2020 was a year dominated by the COVID-19 pan- n SECONDARIES 13 demic (please refer to our Coronavirus Resource Center for further information). The public markets roller-coastered n CREDIT FUNDS 14 up and down, and M&A activity dramatically slowed in n ESG INVESTING 16 the early part of 2020, bouncing back in earnest in the second half of the year. Likewise, fundraising was slow during the second quarter of 2020, but rebounded to a large extent later in the year, with funds ultimately raising similar amounts of capital as they did in 2019, but with a smaller number of large funds stealing the limelight. To supplement the information in this report, we have provided links to other content we have produced on Private Funds Report opens with a more detailed look at these topics, including articles, focused reports and pod- 2020 fundraising trends.