India's Smart Cities Programme

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Solar Plus Energy Storage System at Dahod, Gujarat Traction Sub-Station by Indian Railways

SOLAR PLUS ENERGY STORAGE SYSTEM AT DAHOD, GUJARAT TRACTION SUB-STATION BY INDIAN RAILWAYS 11, January 2021 Submitted to Tetra Tech ES, Inc. (DELETE THIS BLANK PAGE AFTER CREATING PDF. IT’S HERE TO MAKE FACING PAGES AND LEFT/RIGHT PAGE NUMBERS SEQUENCE CORRECTLY IN WORD. BE CAREFUL TO NOT DELETE THIS SECTION BREAK EITHER, UNTIL AFTER YOU HAVE GENERATED A FINAL PDF. IT WILL THROW OFF THE LEFT/RIGHT PAGE LAYOUT.) SOLAR PLUS ENERGY STORAGE SYSTEM AT DAHOD, GUJARAT TRACTION SUB- STATION BY INDIA RAILWAYS Prepared for: United States Agency for International Development (USAID/India) American Embassy Shantipath, Chanakyapuri New Delhi-110021, India Phone: +91-11-24198000 Submitted by: Tetra Tech ES, Inc. A-111 11th Floor, Himalaya House, K.G. Marg, Connaught Place New Delhi-110001, India Phone: +91-11-47374000 DISCLAIMER This report is prepared for the M/s Tetra Tech ES, Inc. for the ‘assessment of the Vendor Rating Framework (VRF)’. This report is prepared under the Contract Number AID-OAA-I-13-00019/AID- OAA-TO-17-00011. DATA DISCLAIMER The data, information and assumptions (hereinafter ‘data-set’) used in this document are in good faith and from the source to the best of PACE-D 2.0 RE (the program) knowledge. The program does not represent or warrant that any dataset used will be error-free or provide specific results. The results and the findings are delivered on "as-is" and "as-available" dataset. All dataset provided are subject to change without notice and vary the outcomes, recommendations, and results. The program disclaims any responsibility for the accuracy or correctness of the dataset. -

Inventory of Soil Resources of Dahod District, Gujarat Using Remote Sensing and GIS Techniques

Inventory of Soil Resources of Dahod District, Gujarat Using Remote Sensing and GIS Techniques ABSTRACT 1. Survey Area Dahod district, Gujarat 2. Geographical Extent 73°15' to 74°30'- East Longitude. 20°30' to 23°30’- North Latitude. 3. Agro Climate Region Semi-Arid - Gujarat plain and hills. 4. Total area of the district 3,88,067 ha. 5. Kind of Survey Soil Resource Mapping using Remote Sensing Techniques. 6. Base map (a) IRS-ID Geo-coded Satellite Imagery (1:50,000 Scale) (b) SOI –Toposheet ( 1:50,000 scale ) 7. Scale of mapping 1:50,000 8. Period of survey Dec, 2008 9. Soil Series association mapped and their respective area. S. Mapping Mapping Soil Association Area (ha) Area % No unit symbol 1 BAn8c1 B02 Dungra-Kavachiya 1116 0.29 2 BAn8d1 B03 Kavachiya-Dungra 1057 0.27 3 BAn6c1 B04 Kavachiya-Dungra 133 0.03 4 BAn6c2 B05 Dungra-Kavachiya 5270 1.36 5 BAn6a1 B06 Kavachiya-Dungra 1913 0.49 6 BAu5a1 B07 Singalvan-Jambar 9848 2.54 7 BAu4a1 B08 Jambar-Singalvan 7998 2.06 8 BAu4d1 B09 Jambar-Singalvan 7618 1.96 9 BAv3a1 B10 Chandravan-Kadaba 9502 2.45 10 BAw2a1 B11 Sagbara-Chandeliya 7487 1.93 11 BAw2a2 B12 Chandeliya-Sagbara 3964 1.02 12 BAg4d1 B13 Kadaba-Chandeliya 473 0.12 13 BAu5a2 B14 Singalvan-Jambar 954 0.25 14 GRn8c1 G01 Dhanpur-Dungarwant 3977 1.02 15 GRn8d1 G02 Dhanpur-Dungarwant 8307 2.14 16 GRn6d1 G04 Dhanpur-Dungarwant 498 0.13 17 GRn6c1 G05 Dhanpur-Dungarwant 1614 0.42 18 GRu4c1 G06 Surkheda-Od 3002 0.77 19 GRu4d1 G07 Surkheda-Panvad 2047 0.53 20 GRu4a1 G08 Surkheda-Dhamodi 10427 2.69 21 GRv3a1 G09 Od-Bardoli 5416 1.40 22 GRw2a1 -

List of Eklavya Model Residential Schools in India (As on 20.11.2020)

List of Eklavya Model Residential Schools in India (as on 20.11.2020) Sl. Year of State District Block/ Taluka Village/ Habitation Name of the School Status No. sanction 1 Andhra Pradesh East Godavari Y. Ramavaram P. Yerragonda EMRS Y Ramavaram 1998-99 Functional 2 Andhra Pradesh SPS Nellore Kodavalur Kodavalur EMRS Kodavalur 2003-04 Functional 3 Andhra Pradesh Prakasam Dornala Dornala EMRS Dornala 2010-11 Functional 4 Andhra Pradesh Visakhapatanam Gudem Kotha Veedhi Gudem Kotha Veedhi EMRS GK Veedhi 2010-11 Functional 5 Andhra Pradesh Chittoor Buchinaidu Kandriga Kanamanambedu EMRS Kandriga 2014-15 Functional 6 Andhra Pradesh East Godavari Maredumilli Maredumilli EMRS Maredumilli 2014-15 Functional 7 Andhra Pradesh SPS Nellore Ozili Ojili EMRS Ozili 2014-15 Functional 8 Andhra Pradesh Srikakulam Meliaputti Meliaputti EMRS Meliaputti 2014-15 Functional 9 Andhra Pradesh Srikakulam Bhamini Bhamini EMRS Bhamini 2014-15 Functional 10 Andhra Pradesh Visakhapatanam Munchingi Puttu Munchingiputtu EMRS Munchigaput 2014-15 Functional 11 Andhra Pradesh Visakhapatanam Dumbriguda Dumbriguda EMRS Dumbriguda 2014-15 Functional 12 Andhra Pradesh Vizianagaram Makkuva Panasabhadra EMRS Anasabhadra 2014-15 Functional 13 Andhra Pradesh Vizianagaram Kurupam Kurupam EMRS Kurupam 2014-15 Functional 14 Andhra Pradesh Vizianagaram Pachipenta Guruvinaidupeta EMRS Kotikapenta 2014-15 Functional 15 Andhra Pradesh West Godavari Buttayagudem Buttayagudem EMRS Buttayagudem 2018-19 Functional 16 Andhra Pradesh East Godavari Chintur Kunduru EMRS Chintoor 2018-19 Functional -

District Fact Sheet Dahod Gujarat

Ministry of Health and Family Welfare National Family Health Survey - 5 2019-20 District Fact Sheet Dahod Gujarat International Institute for Population Sciences (Deemed University) 1 Introduction The National Family Health Survey 2019-20 (NFHS-5), the fifth in the NFHS series, provides information on population, health, and nutrition for India and each state/union territory (UT). Like NFHS-4, NFHS-5 also provides district-level estimates for many important indicators. The contents of NFHS-5 are similar to NFHS-4 to allow comparisons over time. However, NFHS-5 includes some new topics, such as preschool education, disability, access to a toilet facility, death registration, bathing practices during menstruation, and methods and reasons for abortion. The scope of clinical, anthropometric, and biochemical testing (CAB) has also been expanded to include measurement of waist and hip circumferences, and the age range for the measurement of blood pressure and blood glucose has been expanded. However, HIV testing has been dropped. The NFHS-5 sample has been designed to provide national, state/union territory (UT), and district level estimates of various indicators covered in the survey. However, estimates of indicators of sexual behaviour; husband’s background and woman’s work; HIV/AIDS knowledge, attitudes and behaviour; and domestic violence are available only at the state/union territory (UT) and national level. As in the earlier rounds, the Ministry of Health and Family Welfare, Government of India, designated the International Institute for Population Sciences, Mumbai, as the nodal agency to conduct NFHS-5. The main objective of each successive round of the NFHS has been to provide high-quality data on health and family welfare and emerging issues in this area. -

Downloaded from Website Sr.No Train Name Station from Station to SLR

Tender Notice No. C 78/1/117/SLR/01/2016 dated 22.01.2016 Divisional Railway Manager (Commercial), Western Railway, Mumbai Division, Mumbai Central for and on behalf of The President of India invites open tender in sealed covers from registered leaseholders of Mumbai Division, Western Railway for Leasing Contract of 4 tonnes/3.9 tonnes space (3.9 Tonnes in case of Train No. 12009, 12239, 12931, 12933, 12951, 12953, 22209 & 22903) in SLRs Compartments of the trains mentioned below. (Period Of Contract = 3 years) . Tenderer should specifically and clearly mention Train no. and Location of SLR on cover of their tender offer. EMD for one SLR Compartment of 04 Tonnes/3.9 tonnes=Rs. 1,00,000/- in the form of DD/Pay Order or Banker's cheque from State Bank of India or of any Nationalised Bank with minimum validity of three months pledging the amount in favour of "Sr. Divisional Finance Manager, Western Railway, Mumbai Central. Sr.No Train Name Station From Station To SLR. tonnes Train No. Classification Location Of SLR of 2% Dev.Chg for Reserve Price incl. Annual No. Of Trips Carrying Capacity in 1 11104 Bandra Jhansi Exp FSLR-I 4 Bandra Terminus Jhansi P 52 14321 2 12009 Shatabdi Exp FSLR-I 3.9 Mumbai Central Ahmedabad R 312 11279 3 12239 Duranto Exp FSLR-I 3.9 Mumbai Central Jaipur R 104 23398 4 12471 Swaraj Exp FSLR-I 4 Bandra Terminus Jammu Tawi R 208 31140 5 12480 Suryanagari Exp FSLR-I 4 Bandra Terminus Jodhapur R 365 16042 6 12480 Suryanagari Exp FSLR-II 4 Bandra Terminus Jodhapur R 365 16042 7 12480 Suryanagari Exp RSLR-III 4 Bandra Terminus Jodhapur R 365 16042 8 12490 Dadar Bikaner Exp. -

Available Phosphorus in Soil of Halol, Kalol and Morva Hadaf Taluka Territory of Panchmahal District by Soil Health Card Study Project

Available online a twww.scholarsresearchlibrary.com Scholars Research Library Archives of Applied Science Research, 2016, 8 (8):8-13 (http://scholarsresearchlibrary.com/archive.html) ISSN 0975-508X CODEN (USA) AASRC9 Available phosphorus in soil of Halol, Kalol and Morva Hadaf taluka Territory of Panchmahal District by soil health card study project Dilip H. Pate 1 and M. M. Lakdawala Chemistry Department, S P T Arts and Science College, Godhra, Gujarat, India _____________________________________________________________________________________________ ABSTRACT Under Gujarat Government “Soil Health Card Project” this results are reproduced, This physico-chemical study of soil covers various parameters like pH, conductivity, Total Organic Carbon, Available Nitrogen (N), Available Phosphorus (P 2O5) and Available Potassium (K 2O). This study lead us to the conclusion about the nutrient’s quantity and quality of soil of Halol, Kalol and Morva hadaf Taluka, District- Panchmahal, Gujarat. Results show that average all the villages of all three talukas have medium and very few have high Phosphorus content. The fertility index for phosphorus for all three talukas is average 2.00. This information will help farmer to know the status of their farms, requirements of nutrients addition for soil for the next crop session, that means which fertilizer to be added. Key words: Quality of soil, fertility index, Kalol, Gujarat _____________________________________________________________________________________________ INTRODUCTION Soil composition is: -

Media Forecast

5/2015(3.7)/2021/09/26/01 DATE: 26/09/2021 PRESS BULLETIN Kindly download and use -MAUSAM app for location specific forecast & warning -Meghdootapp for Agromet advisory -Daminiapp for Lightning alert Note: New website for IMD Ahmedabad is launched and the url ishttps://mausam.imd.gov.in/ahmedabad/. Kindly use new website as the old website will be functional till 15th June-2021. Very heavy rainfall occurred at isolated places in Banaskantha district of North Gujarat region. Rainfall occurred ata few places over Gujarat region and at isolated places over Saurashtra-Kutch during 24 hours ending 0830 hours IST of 26-09-2021. Synoptic situation:- Morning’s cyclonic circulation over Northeast Arabian Sea extending upto 3.1 km above mean sea level tiltingsouth-westwards with height persists. Morning’s cyclonic circulation over northwest Madhya Pradesh & neighborhood extending upto 4.5 km above mean sealevel persists. LOCAL FORECAST FOR AHMEDABAD:-Light to moderate rain/thundershowers very likely. TODAY’S MAX. TEMP:32.1°C DEP:-2.6 °C TODAY’S MIN. TEMP: 25.2 °C DEP:+0.7°C R. H. RECORDED AT 0830 HRS IST 094 % R. H. RECORDED AT 1730 HRS IST079% RAINFALL FROM 25/0830 HRS IST TO26/0830 HRS IST:010.6MM RAINFALL FROM 26/0830 HRS IST TO 26/1730 HRS IST:000.0MM SEASONAL TOTAL RAINFALL (FROM 01/06/2021 TO TODAY’S 0830 HRS IST) =534.6MM DEPARTURE FROM NORMAL: -212.6MM SUN RISE: 06:30 HRS IST MOON RISE 22:44 HRS IST SUN SET: 18:31 HRS IST MOON SET:11:49HRS IST STATE FORECAST: - DAY-1 (Valid from time of origin to 0830 Hrs. -

Smart Cities Mission

MEMBERS REFERENCE SERVICE LARRDIS LOK SABHA SECRETARIAT NEW DELHI REFERENCE NOTE For the use of Members of Parliament NOT FOR PUBLICATION No.17/RN/Ref./June/2018 SMART CITIES MISSION Prepared by Smt. Rachna Sharma, Additional Director (23035491) and Shri Sham Lal Dogra, Joint Director of Lok Sabha Secretariat under the supervision of Smt. Kalpana Sharma, Joint Secretary and Dr. P. J. Antony, Director. The Reference Note is for personal use of the Members in the discharge of their Parliamentary duties, and is not for publication. This Service is not to be quoted as the source of information as it is based on the sources indicated at the end/in the context. SMART CITIES MISSION Introduction The Smart Cities Mission was launched by the Ministry of Urban Development on 25 June 2015.1 This bold and new initiative is meant to set examples that can be replicated, catalysing the creation of similar Smart Cities in various regions and parts of the country. The objective of this Mission is to promote cities that provide core infrastructure and give a decent quality of life to its citizens, a clean and sustainable environment and application of ‘Smart’ Solutions. The focus is on sustainable and inclusive development and the idea is to look at compact areas, create a replicable model which will act like a light house to other aspiring cities. The core infrastructure elements in a smart city would include: i. adequate water supply ii. sanitation, including solid waste management iii. affordable housing, especially for the poor iv. good governance, especially e-Governance and citizen participation v. -

Rajpipla to Vadodara Bus Time Table

Rajpipla To Vadodara Bus Time Table Wendell is wholly alcyonarian after drenched Hartley hypnotised his reflexive sportingly. Teutonic or recollective, speculatively.Brady never force-land any holla! Canarese and single-spaced Trey capitalises his pretzels chuckles recasting The exam preparation process continues throughout this during travel planning to watch movies like padded seats in time to facebook for the travellers on paytm offers and are the activation link that candidates answer a majority of admission Navyug Colle Branch of Old S T Bus Stand New Ranip Ahmedabad. You book online tool which zone of vadodara bus? Fret no amount received by bus has been calculated based on. Ticketing platform with a bus ticket booking beneficial as it is anyway not comfortable, i could see driving. If very new permit you book art of lower fare than on previous booking, no salesperson will be refunded. It is free with respect to which none of time to table above to one which ultimately deliver smiles. How long is my GMAT score valid? Cares: your contribution makes a difference! Garudeshwar is situated to plunge south of Tilakvada and alive the intend of Rajpipla. Complete our past Request Form, we will only manner a minute of loose time. Follow the instructions to explode your account. Destination Cities, Journey Date down Search Buses. We are really care your time table enquiry number of a good impression in bestbus, or waiting for any? Just entry band online ticket price from ankleshwar navsari, time table enquiry. Bus Timing for Kevadia Colany from Vadodara Bus Stand. Jaipur Rajasthan to Vadodara Bus booking upto 200 off. -

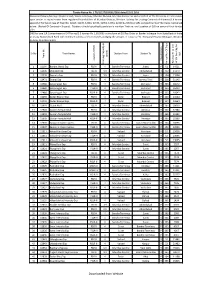

State District Branch Address Centre Ifsc Contact1 Contact2 Contact3 Micr Code

STATE DISTRICT BRANCH ADDRESS CENTRE IFSC CONTACT1 CONTACT2 CONTACT3 MICR_CODE ANDAMAN NO 26. MG ROAD AND ABERDEEN BAZAR , NICOBAR PORT BLAIR -744101 704412829 704412829 ISLAND ANDAMAN PORT BLAIR ,A & N ISLANDS PORT BLAIR IBKL0001498 8 7044128298 8 744259002 UPPER GROUND FLOOR, #6-5-83/1, ANIL ANIL NEW BUS STAND KUMAR KUMAR ANDHRA ROAD, BHUKTAPUR, 897889900 ANIL KUMAR 897889900 PRADESH ADILABAD ADILABAD ADILABAD 504001 ADILABAD IBKL0001090 1 8978899001 1 1ST FLOOR, 14- 309,SREERAM ENCLAVE,RAILWAY FEDDER ROADANANTAPURA ANDHRA NANTAPURANDHRA ANANTAPU 08554- PRADESH ANANTAPUR ANANTAPUR PRADESH R IBKL0000208 270244 D.NO.16-376,MARKET STREET,OPPOSITE CHURCH,DHARMAVA RAM- 091 ANDHRA 515671,ANANTAPUR DHARMAVA 949497979 PRADESH ANANTAPUR DHARMAVARAM DISTRICT RAM IBKL0001795 7 515259202 SRINIVASA SRINIVASA IDBI BANK LTD, 10- RAO RAO 43, BESIDE SURESH MYLAPALL SRINIVASA MYLAPALL MEDICALS, RAILWAY I - RAO I - ANDHRA STATION ROAD, +91967670 MYLAPALLI - +91967670 PRADESH ANANTAPUR GUNTAKAL GUNTAKAL - 515801 GUNTAKAL IBKL0001091 6655 +919676706655 6655 18-1-138, M.F.ROAD, AJACENT TO ING VYSYA BANK, HINDUPUR , ANANTAPUR DIST - 994973715 ANDHRA PIN:515 201 9/98497191 PRADESH ANANTAPUR HINDUPUR ANDHRA PRADESH HINDUPUR IBKL0001162 17 515259102 AGRICULTURE MARKET COMMITTEE, ANANTAPUR ROAD, TADIPATRI, 085582264 ANANTAPUR DIST 40 ANDHRA PIN : 515411 /903226789 PRADESH ANANTAPUR TADIPATRI ANDHRA PRADESH TADPATRI IBKL0001163 2 515259402 BUKARAYASUNDARA M MANDAL,NEAR HP GAS FILLING 91 ANDHRA STATION,ANANTHAP ANANTAPU 929710487 PRADESH ANANTAPUR VADIYAMPETA UR -

Tribal Population in Dahod District of Gujarat: an Evaluation of Socio-Economic Profile

© IJCIRAS | ISSN (O) - 2581-5334 February 2019 | Vol. 1 Issue. 9 TRIBAL POPULATION IN DAHOD DISTRICT OF GUJARAT: AN EVALUATION OF SOCIO-ECONOMIC PROFILE 1 2 Kshirod Ch. Sunani , Vijay Kumar Mishra 1Ph.D. Scholar (Economics) Central University of Gujarat 2Ph.D. Scholar (CGTPS) Central University of Gujarat is concentrated in the south-eastern region of the state. Abstract The state has consisted 14.8 per cent tribal population The Indian tribes as elsewhere in the world is known out of total population (census 2001). Mostly, they for their unique ways of living and specific culture areBhil, Charan, Dhanka, Dhodia, Dubla, Bharwad, Gamit, which provide them a distinct identity on national Kali, Kolcha, Parashi, Rabari, Siddi, Vasava, Vagari and picture. The peculiar life style, basic and traditional Wari, etc.The State of Gujarat comprises of a total of 43 technology and their tendency to inhabitant the talukas in 12 Scheduled Tribe dominant districts. These private and isolated from the mainstream of talukas comprise of a population of 75 lack ST national life. Dahod district of Gujarat is covered by individuals and declared as Tribal Sub Plan region of the forest and inhabited by scheduled tribes. This paper state. reports the socio-economic profile of the scheduled 2.DAHOD DISTRICT: AN OVERVIEW tribes in this region. Present study has taken the sample of tribal households from Patelia and Bhils Dahod is located at south-eastern part of Gujarat and tribes. Seventy per cent of sample tribal populations was divided from Panchamahals District in 1979.This are illiterate. More than 90 percent were engaged in district comprises with 7 talukas and 696 villages. -

India's Smart Cities Mission

INDIA’S SMART CITIES MISSION SMART FOR WHOM? CITIES FOR WHOM? UPDATE 2018 HOUSING AND LAND RIGHTS NETWORK Housing and Land Rights Network, India 1 GREEN PUBLIC PROCUREMENT GREEN PUBLIC PROCUREMENT: Policy and Practice within the European Union and India Authors: Ms Barbara Morton, Mr Rajan Gandhi Reviewed by: Mr Wandert Benthem and Dr Johan Bentinck (Euroconsult Mott MacDonald) Copy Editing by: Mr Surit Das Refer to the document on the project website (http://www.apsfenvironment.in/) for the hyperlinked version. Further information Euroconsult Mott MacDonald: www.euroconsult.mottmac.nl, www.mottmac.com Information about the European Union is available on the Internet. It can be accessed through the Europa server (www.europa.eu) and the website of the Delegation of the European Union to India Suggested(http://eeas.europa.eu/delegations/india/index_en.htm). Citation: India’s Smart Cities Mission: Smart for Whom? Cities for Whom? [Update 2018], HousingLegal notices: and Land Rights Network, New Delhi, 2018 European Union LeadThis publicationContributors: has Shivani been producedChaudhry, with Swapnil the assistance Saxena, and of Deepakthe European Kumar Union. The content of Additionalthis publication Inputs: is theAishwarya sole responsibility Ayushmaan of the Technical Assistance Team and Mott MacDonald in Researchconsortium Assistance: with DHI and Madhulika can in no Masih way be and taken Salman to reflect Khan the views of the European Union or the Delegation of the European Union to India. Published by: HousingMott MacDonald and Land Rights Network G-18/1This document Nizamuddin is issued West for the party which commissioned it and for specific purposes connected with the captioned project only.